Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Introduction & Market Context

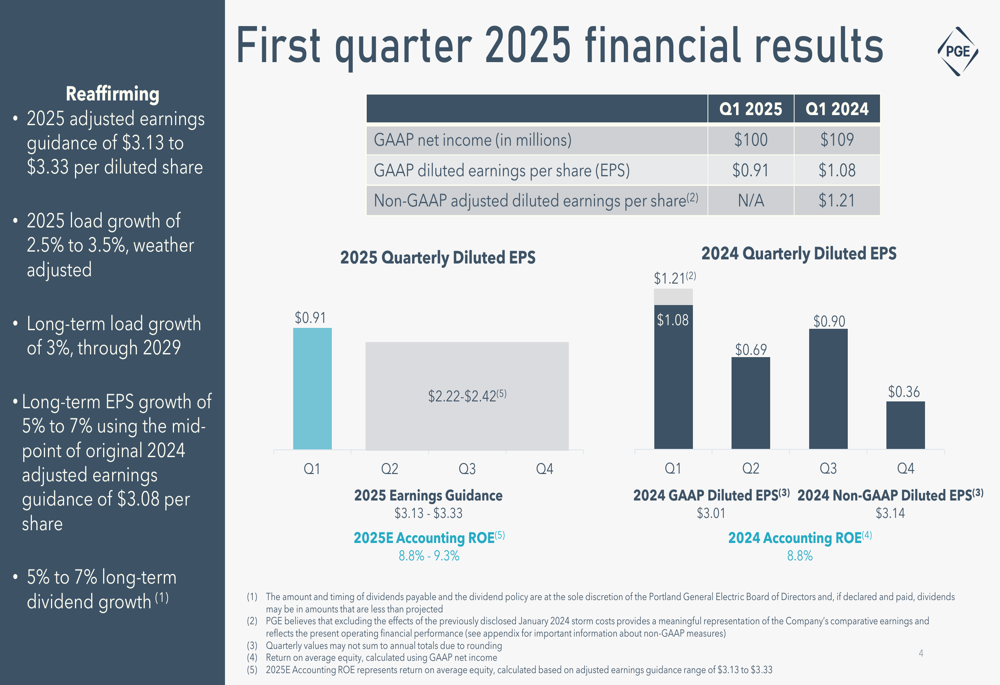

Portland General Electric (NYSE:POR) reported its first quarter 2025 financial results on April 25, showing a year-over-year decline in earnings while maintaining its full-year guidance. The company’s stock responded negatively to the news, dropping 2.8% to $41.77 on the day of the announcement, continuing to trade well below its 52-week high of $49.85.

The utility’s performance comes amid ongoing investments in reliability and resiliency, with a particular focus on battery energy storage systems (BESS) as part of its long-term capital expenditure strategy. Despite the quarterly earnings decline, management expressed confidence in achieving its full-year targets.

Quarterly Performance Highlights

PGE reported GAAP net income of $100 million for Q1 2025, down from $109 million in the same period last year. Diluted earnings per share (EPS) decreased to $0.91 from $1.08 in Q1 2024, representing a 15.7% decline.

As shown in the following financial results summary:

Despite the earnings decline, PGE reaffirmed its 2025 adjusted earnings guidance of $3.13 to $3.33 per diluted share and maintained its load growth projection of 2.5% to 3.5%. The company expects its 2025 accounting return on equity (ROE) to be between 8.8% and 9.3%, compared to 8.8% in 2024.

Detailed Financial Analysis

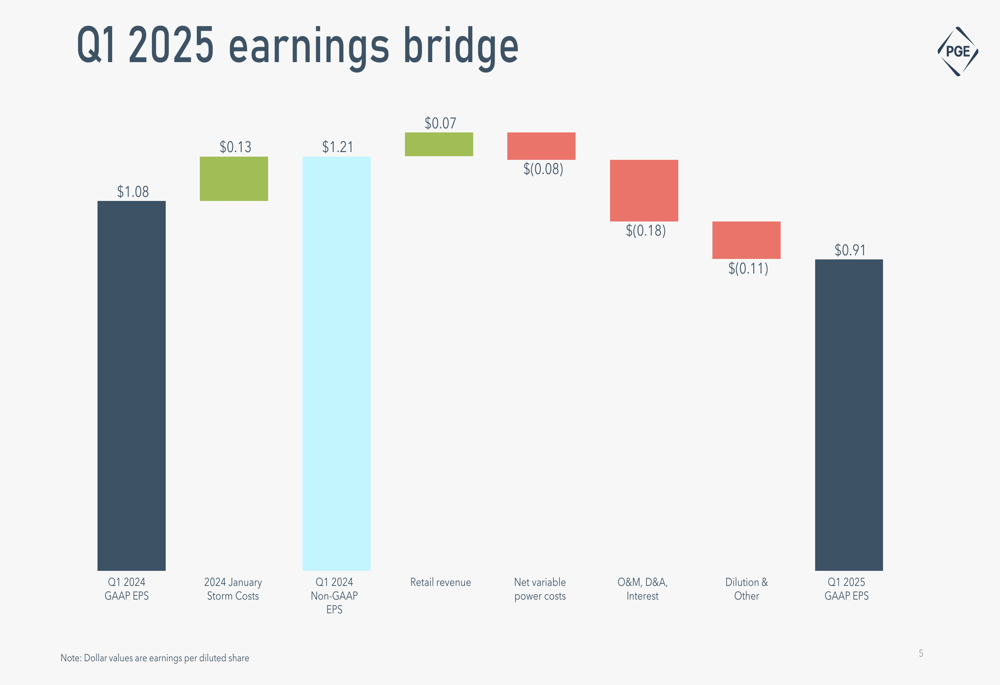

Several factors contributed to the year-over-year decline in earnings. The company provided a detailed breakdown of these drivers in its earnings bridge:

While retail revenue contributed positively with a $0.07 per share increase, this was more than offset by negative factors including:

- Net variable power costs (-$0.08 per share)

- Operations and maintenance, depreciation and amortization, and interest expenses (-$0.18 per share)

- Dilution and other factors (-$0.11 per share)

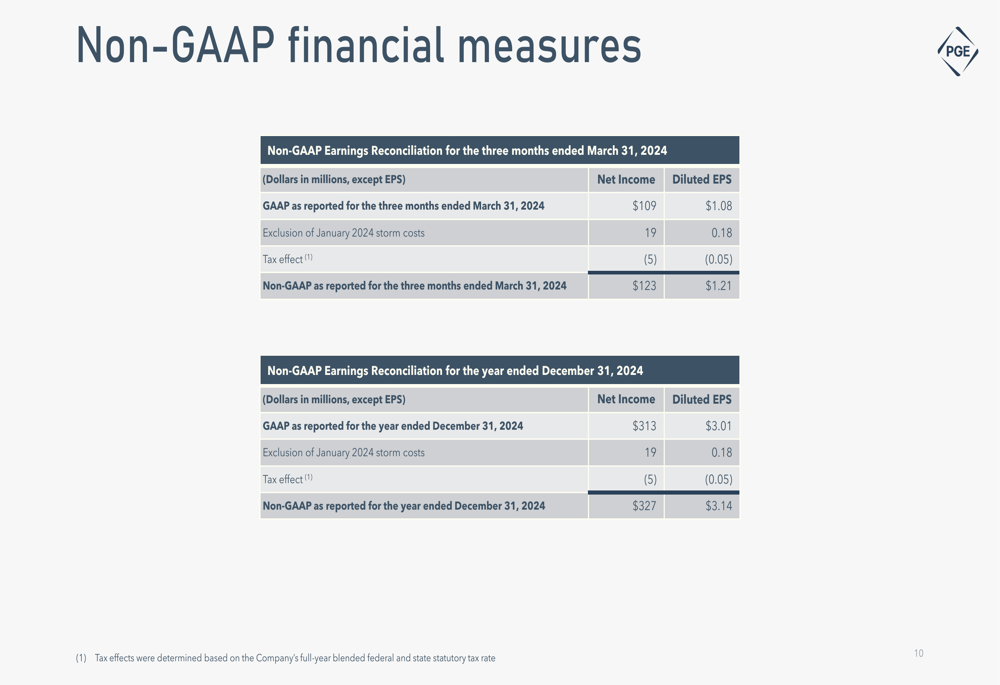

It’s worth noting that Q1 2024 results included $0.13 per share in January storm costs, which were excluded from the non-GAAP adjusted EPS of $1.21 for that quarter.

Liquidity and Financial Position

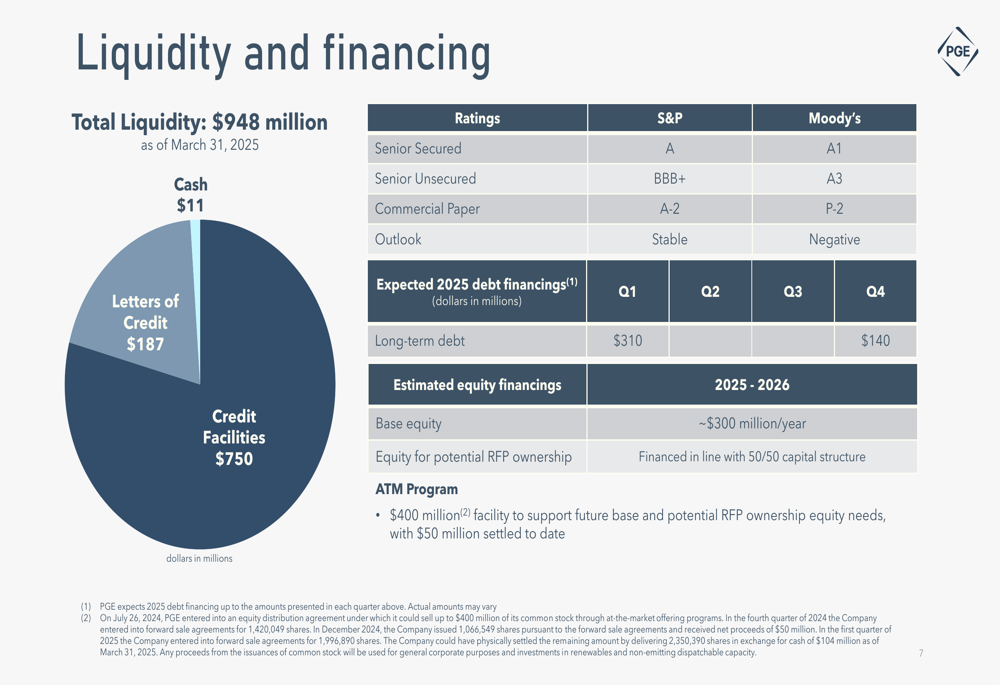

The company maintains a solid liquidity position with $948 million available as of March 31, 2025, consisting of $11 million in cash, $187 million in letters of credit, and $750 million in credit facilities.

As illustrated in the following liquidity and financing overview:

PGE’s credit ratings remain investment grade, with S&P maintaining a stable outlook while Moody’s has assigned a negative outlook. The company completed $310 million in debt financing during Q1 2025 and plans an additional $140 million in Q4. Equity financing is estimated at approximately $300 million per year for 2025-2026, with $50 million already settled through the company’s ATM Program.

Strategic Initiatives

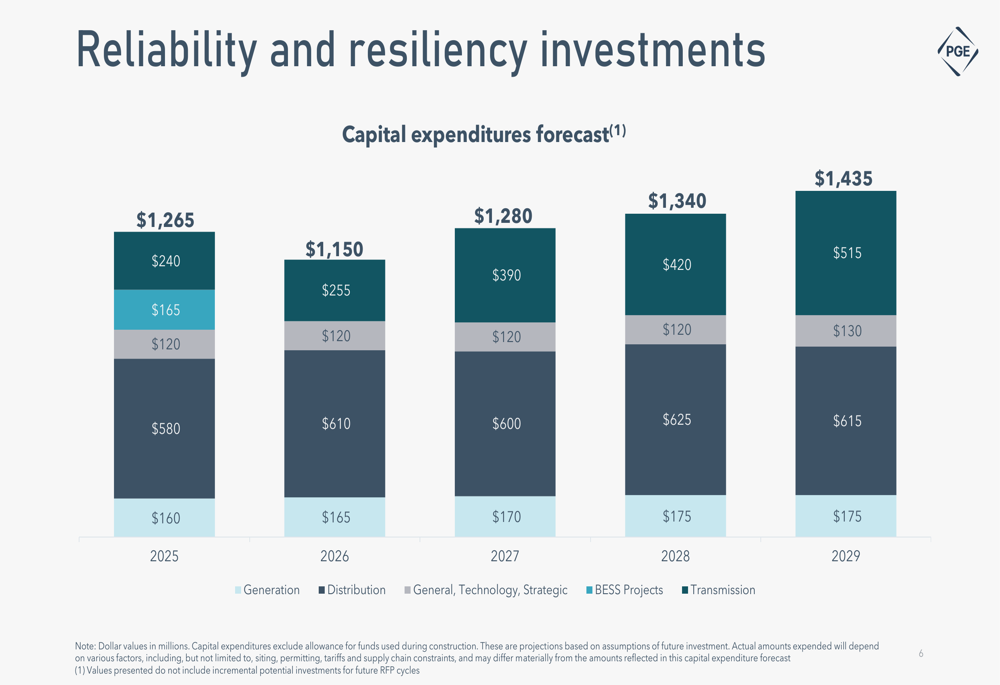

Portland General Electric outlined an ambitious five-year capital expenditure plan totaling over $6.4 billion from 2025 through 2029, with increasing investments in battery energy storage systems (BESS).

The following chart details the company’s capital expenditure forecast:

The most notable trend is the substantial growth in BESS Projects investment, which is projected to more than triple from $165 million in 2025 to $515 million in 2029. Distribution investments remain the largest category throughout the forecast period, reflecting the company’s focus on grid reliability and resilience.

Transmission investments are significant in 2025 at $240 million but are not projected for subsequent years in the current plan. Overall capital expenditures are expected to grow from $1,265 million in 2025 to $1,435 million by 2029, representing a 13.4% increase over the five-year period.

Forward-Looking Statements

Despite the Q1 earnings decline, PGE’s management expressed confidence in meeting its full-year targets. The company’s maintained guidance suggests expectations for improved performance in subsequent quarters, with Q2 2025 projected to deliver significantly higher earnings than the first quarter.

The reconciliation of GAAP to non-GAAP measures provides additional context for understanding the company’s financial reporting:

This transparency in financial reporting helps investors better assess PGE’s underlying operational performance by excluding one-time events like the January 2024 storm costs.

Conclusion

Portland General Electric’s Q1 2025 results present a mixed picture, with lower earnings compared to the previous year but maintained full-year guidance suggesting confidence in future quarters. The company’s substantial capital expenditure plans, particularly in battery energy storage systems, highlight its strategic focus on grid modernization and renewable energy integration.

However, investors should note the contrasting credit rating outlooks from S&P (stable) and Moody’s (negative), which may indicate some financial challenges ahead. The success of PGE’s strategy will depend on its ability to effectively manage costs while executing its ambitious capital investment program in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.