Oracle: Baird initiates with ‘Outperform’, sees it at center of AI boom

Introduction & Market Context

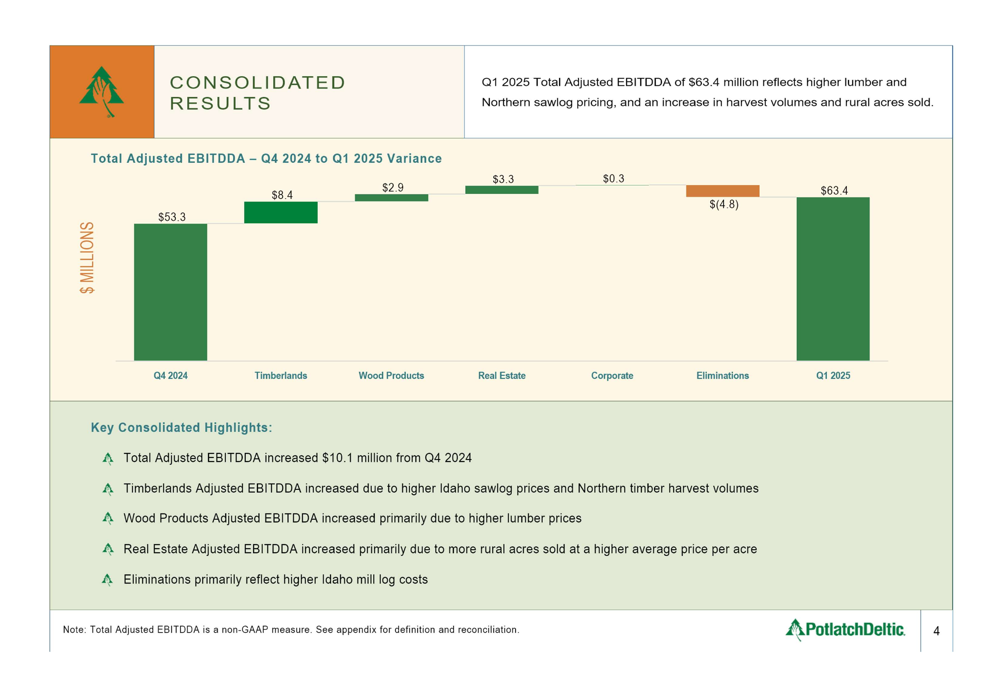

PotlatchDeltic Corporation (NYSE:NASDAQ:PCH) released its first quarter 2025 earnings presentation on April 29, 2025, revealing solid performance across all business segments. The integrated timber REIT reported significant improvements in its Timberlands, Wood Products, and Real Estate divisions, with total Adjusted EBITDDA increasing 19% quarter-over-quarter to $63.4 million.

The company’s stock closed at $39.44 on April 28, 2025, up 0.92% for the day, with a market capitalization of approximately $3.55 billion. PotlatchDeltic maintains a dividend yield of 4.0%, continuing its tradition of returning value to shareholders while maintaining investment-grade credit ratings.

Quarterly Performance Highlights

PotlatchDeltic reported net income of $25.8 million for Q1 2025, translating to diluted earnings per share of $0.33. This represents a substantial improvement from the previous quarter when the company reported EPS of $0.07. Total (EPA:TTEF) Adjusted EBITDDA reached $63.4 million with a 23.6% margin, up from $53.3 million in Q4 2024.

As shown in the following chart of consolidated results, all three business segments contributed to the improved performance:

The increase was primarily driven by higher lumber and Northern sawlog pricing, increased harvest volumes, and more rural acres sold during the quarter. Cash available for distribution (CAD) was reported at $125.3 million, supporting the company’s $142 million annual dividend run rate.

Segment Analysis: Timberlands

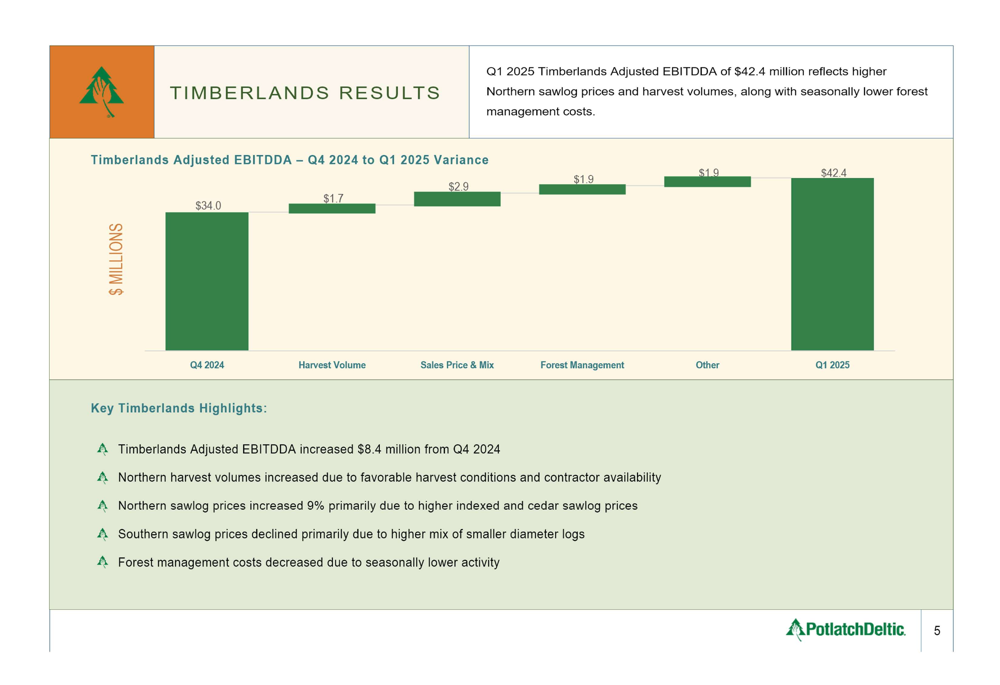

The Timberlands segment delivered the strongest performance among all divisions, with Adjusted EBITDDA increasing from $34.0 million in Q4 2024 to $42.4 million in Q1 2025. This improvement was attributed to higher Northern sawlog prices and harvest volumes, coupled with seasonally lower forest management costs.

The following chart illustrates the key drivers behind the Timberlands performance improvement:

In the Northern Region, sawlog prices increased to $124 per ton while harvest volume reached 354,000 tons. The Southern Region maintained stable performance with sawlog prices at $45 per ton and harvest volume of 654,000 tons. Total fee harvest volume across both regions was 1.94 million tons for the quarter.

Segment Analysis: Wood Products

The Wood Products segment continued its recovery trajectory, with Adjusted EBITDDA increasing by $2.9 million to $11.7 million in Q1 2025. A key highlight was the completion of the Waldo, Arkansas sawmill ramp-up, which was achieved three months ahead of schedule.

The following chart details the Wood Products segment performance:

Average lumber prices increased 2% to $454 per thousand board feet (MBF) in Q1 2025, while shipment volumes reached 290 million board feet. The segment achieved a 7.1% Adjusted EBITDDA margin, reflecting improved operational efficiency and market conditions.

Segment Analysis: Real Estate

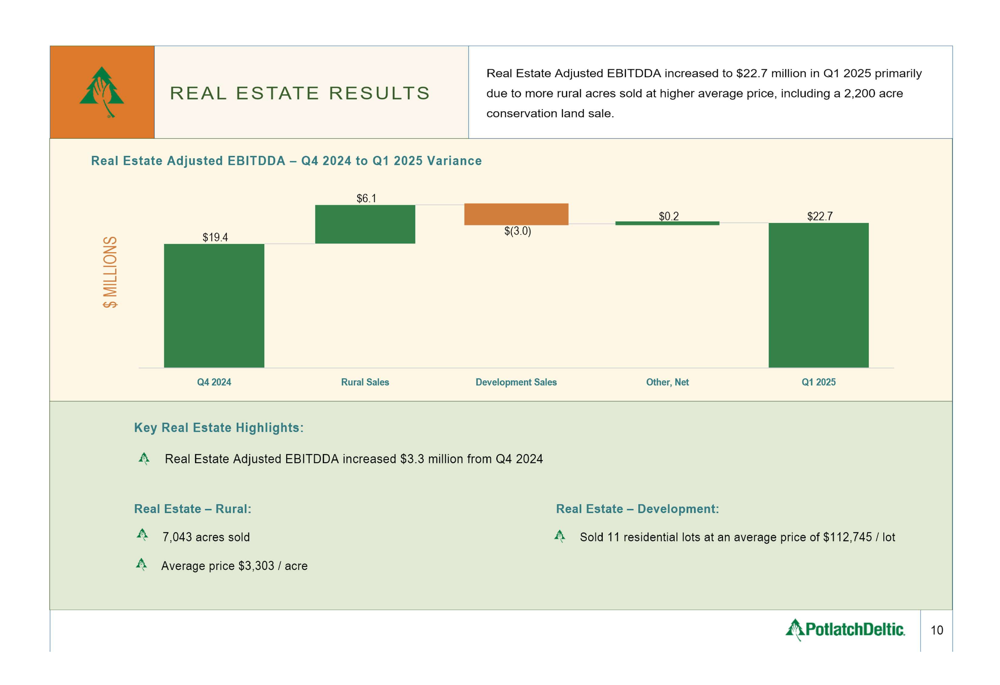

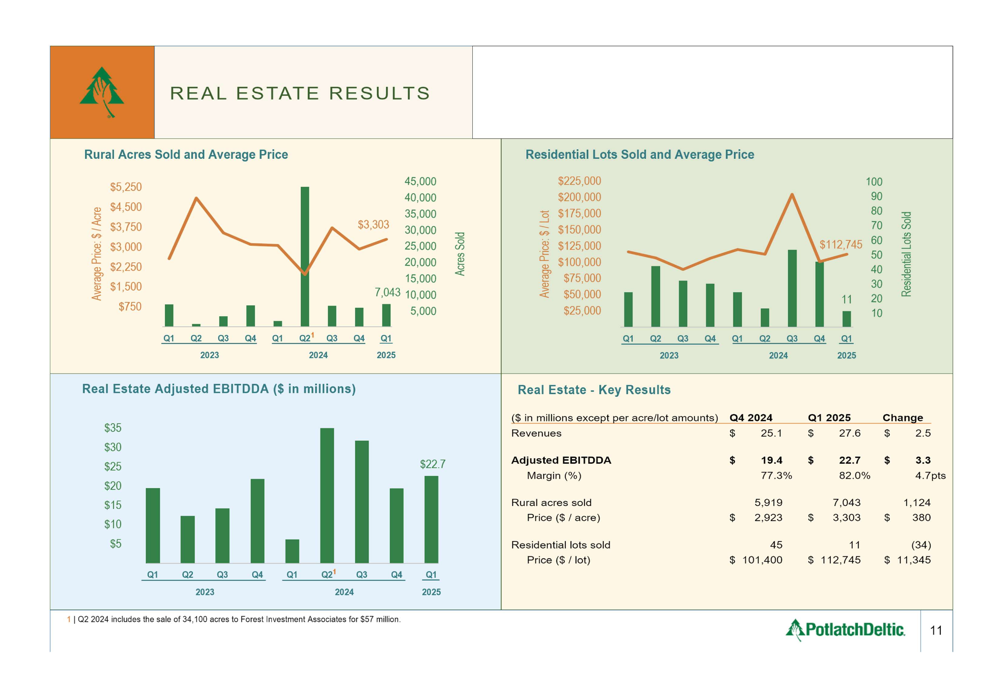

The Real Estate segment showed strong results with Adjusted EBITDDA of $22.7 million, an increase of $3.3 million from the previous quarter. The segment achieved an impressive 82.0% margin, demonstrating the high-value nature of these transactions.

The following chart shows the Real Estate segment’s performance improvement:

During Q1 2025, PotlatchDeltic sold 7,043 rural acres at an average price of $3,303 per acre, along with 11 residential lots at an average price of $112,745 per lot. These results highlight the company’s ability to extract premium value from its land holdings.

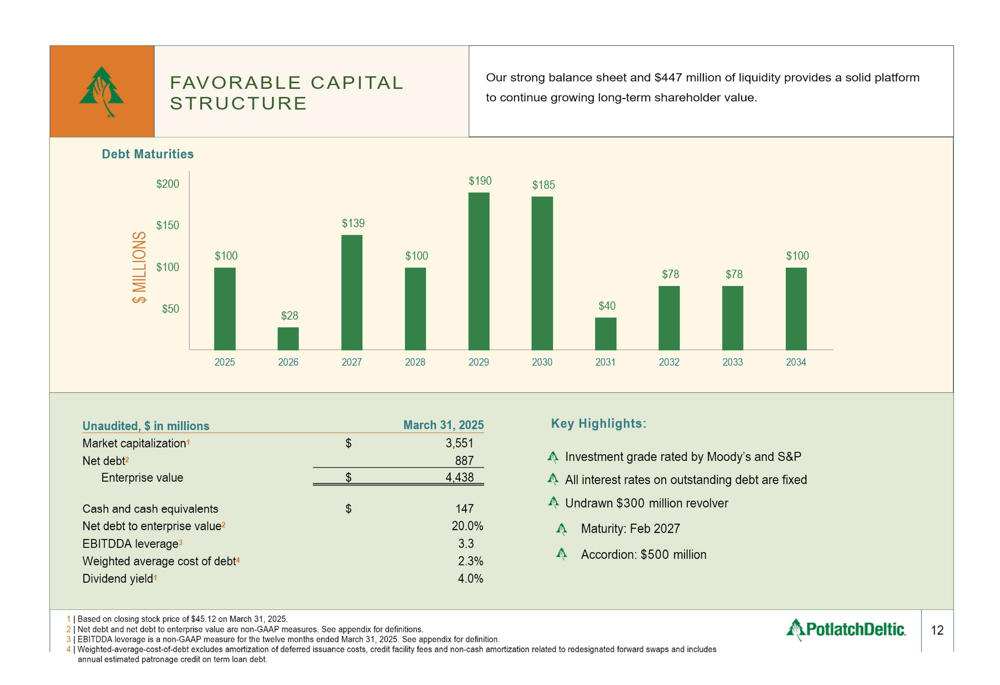

Capital Structure and Allocation

PotlatchDeltic maintains a favorable capital structure with strong liquidity. The company reported net debt of $887 million, representing 20.0% of enterprise value. All outstanding debt carries fixed interest rates with a weighted average cost of 2.3%.

The company’s debt maturity schedule is well-structured, as shown in the following chart:

Capital expenditures totaled $23 million year-to-date, with $60-65 million planned for the full year 2025. PotlatchDeltic maintains an undrawn $300 million revolver with a February 2027 maturity and a $500 million accordion feature, providing substantial financial flexibility.

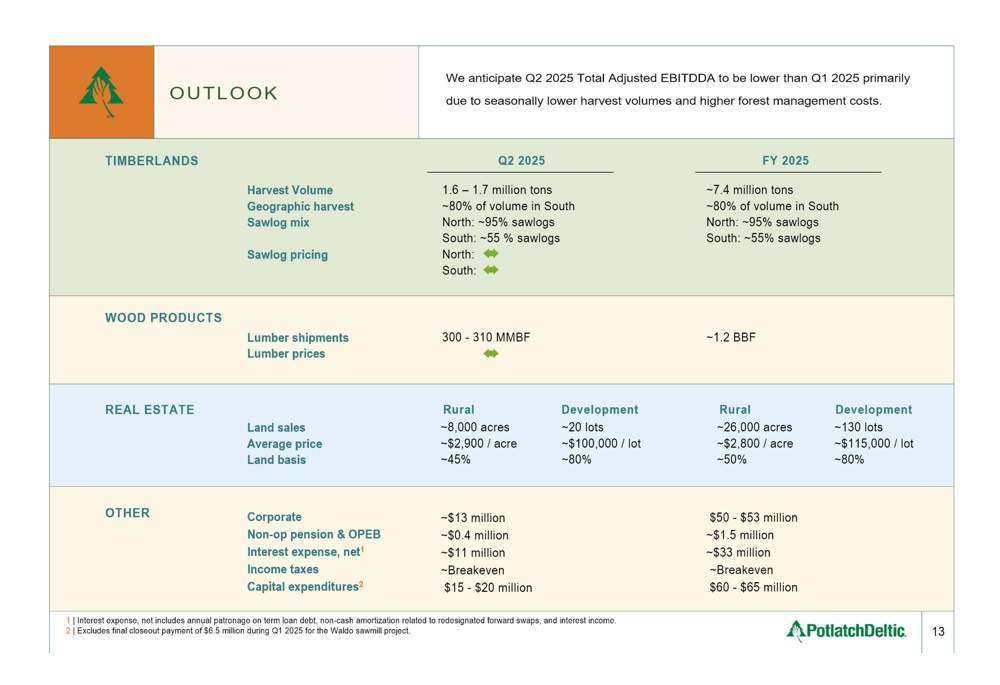

Outlook & Forward-Looking Statements

Looking ahead to Q2 and full-year 2025, PotlatchDeltic provided a cautiously optimistic outlook while noting that Q2 Adjusted EBITDDA is expected to be lower than Q1. The company anticipates lumber shipments of 300-310 million board feet in Q2 and approximately 1.2 billion board feet for the full year.

The following slide details the company’s outlook for the remainder of 2025:

For the Real Estate segment, PotlatchDeltic is targeting sales of 8,000 rural acres in Q2 and 26,000 acres for the full year. Additionally, the company expects to sell 20 development lots in Q2 and 130 lots throughout 2025.

Harvest volume allocation will remain heavily weighted toward the Southern region, with approximately 80% of harvest activity occurring in the South. This geographic distribution aligns with the company’s asset base and market conditions.

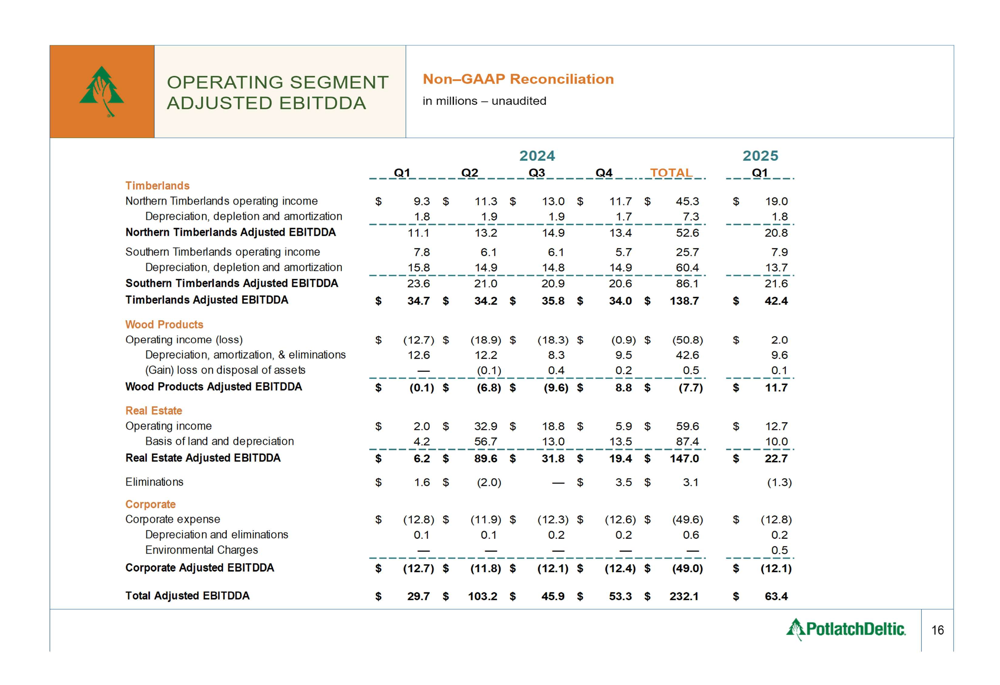

Financial Reconciliation

The detailed segment performance is illustrated in the following reconciliation of operating segment Adjusted EBITDDA:

This comprehensive breakdown shows how each segment contributed to the overall performance, with Timberlands generating $42.4 million, Wood Products $11.7 million, and Real Estate $22.7 million in Adjusted EBITDDA for Q1 2025.

PotlatchDeltic’s Q1 2025 results demonstrate the company’s ability to leverage its diversified business model to generate consistent returns across market cycles. With the successful early completion of the Waldo sawmill ramp-up and strong performance across all segments, the company appears well-positioned to navigate the remainder of 2025, despite expectations for some moderation in Q2 performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.