CTAs are almost max long in equities, have very limited room to buy: UBS

Introduction & Market Context

PRA Group, Inc. (NASDAQ:PRAA) reported its first quarter 2025 financial results on May 5, showing continued portfolio growth and record estimated remaining collections (ERC) despite modest earnings. The debt buyer’s stock fell 6.25% in after-hours trading to $18.00, suggesting investors may have expected stronger bottom-line results despite the company’s operational improvements.

The global leader in acquiring and collecting nonperforming loans delivered $4 million in net income attributable to PRA Group, a 5% year-over-year increase, while maintaining its focus on portfolio purchases and cash collections growth. This performance comes as the company prepares for a leadership transition in June.

Quarterly Performance Highlights

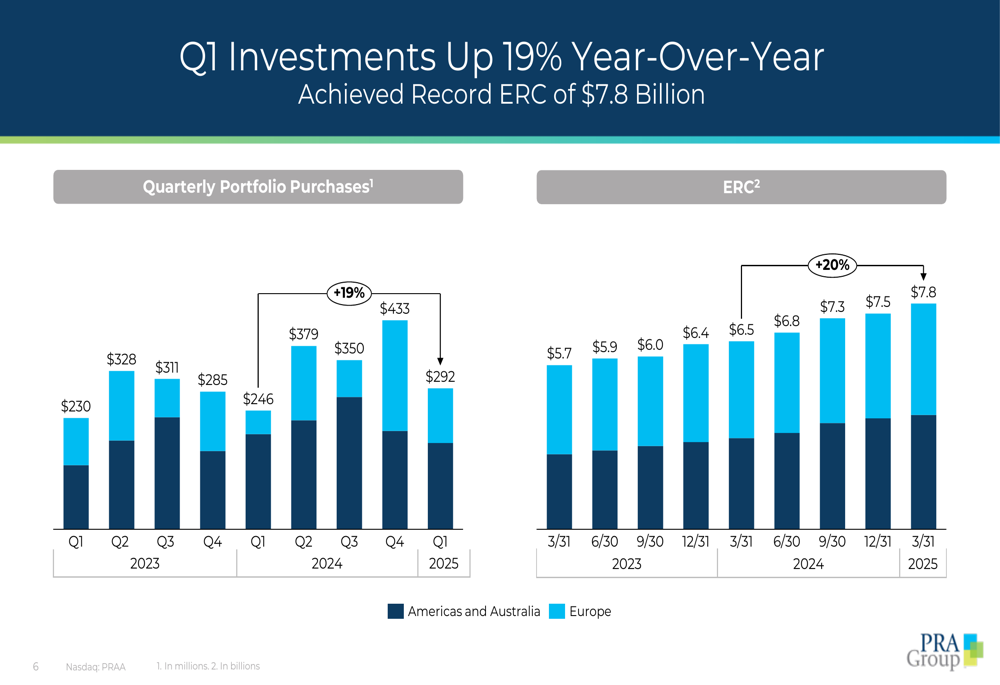

PRA Group reported significant growth across several key metrics in Q1 2025 compared to the same period last year. Portfolio purchases increased 19% to $292 million, driving estimated remaining collections (ERC) to a record $7.8 billion, representing a 20% year-over-year increase.

As shown in the following chart of portfolio purchases and ERC growth:

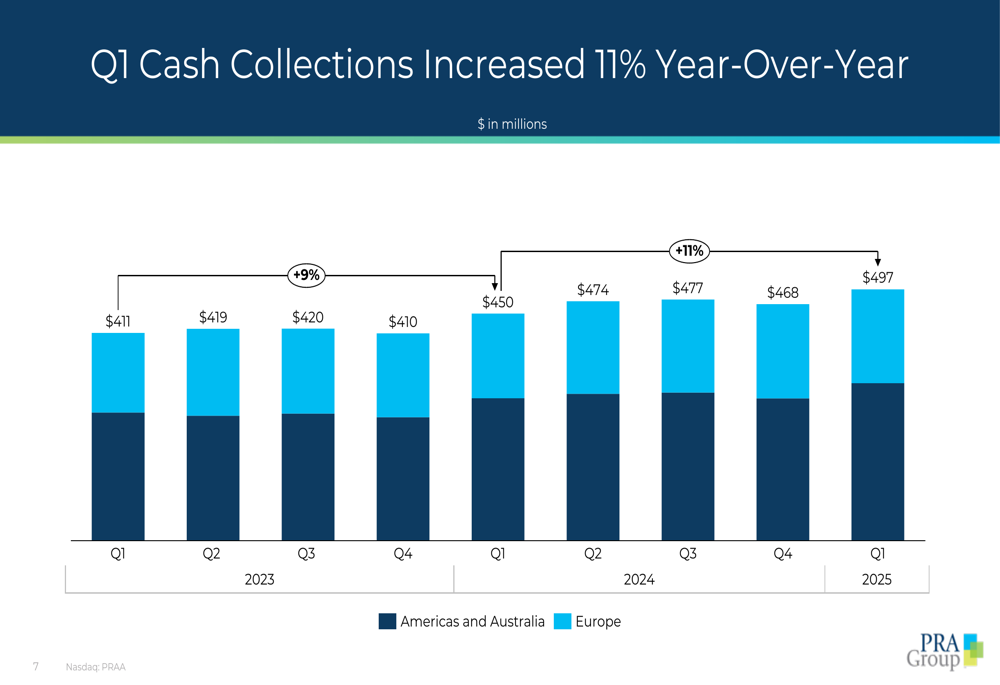

Cash collections grew 11% year-over-year to $497 million, marking the fourth consecutive quarter of double-digit growth in this critical metric. The company also improved its cash efficiency ratio by 284 basis points to 60.8%.

The following chart illustrates the cash collections growth across regions:

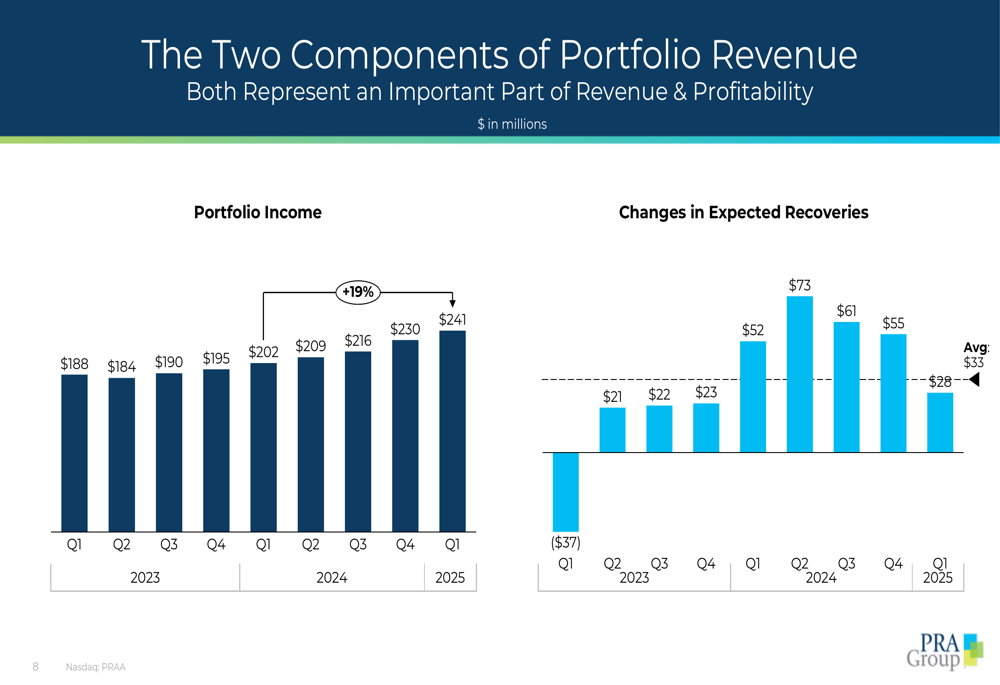

Portfolio revenue consists of two components: portfolio income and changes in expected recoveries. Portfolio income increased 19% to $241 million in Q1 2025, while changes in expected recoveries decreased 46% to $28 million compared to the prior year.

The company’s revenue components are broken down in this chart:

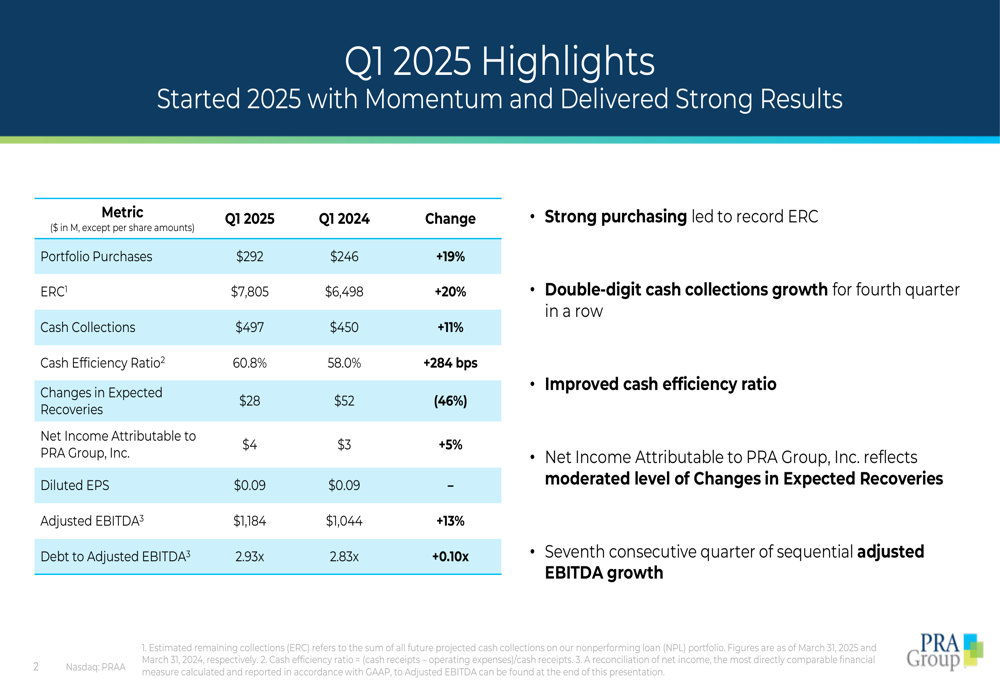

Despite the strong operational metrics, net income attributable to PRA Group was a modest $4 million, with diluted earnings per share of $0.09. This represents a significant decline from the $27 million net income ($0.69 per diluted share) reported in Q3 2024, indicating potential pressure on profit margins despite growing collections.

The following slide summarizes the company’s Q1 2025 financial results:

Strategic Initiatives

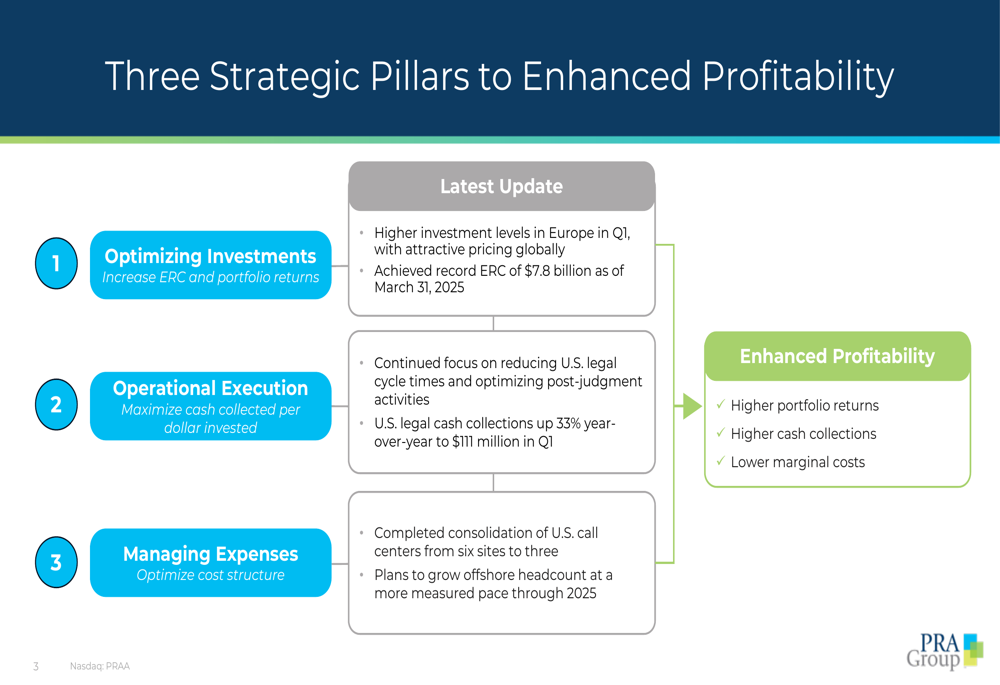

PRA Group continues to execute on its three strategic pillars aimed at enhancing profitability: optimizing investments, operational execution, and managing expenses. The company highlighted its progress in each area during the quarter.

The strategic framework is illustrated in this slide:

In terms of operational execution, the company reported that U.S. legal cash collections increased 33% year-over-year to $111 million in Q1, reflecting its focus on reducing legal cycle times and optimizing post-judgment activities. This growth rate, while impressive, represents a slowdown from the 51% year-over-year increase in U.S. legal collections reported in Q3 2024.

On the expense management front, PRA Group completed the consolidation of its U.S. call centers from six sites to three, which should contribute to improved operational efficiency. The company also indicated plans to grow its offshore headcount at a more measured pace through 2025, balancing cost efficiency with operational needs.

Leadership Transition

A significant development highlighted in the presentation is the upcoming leadership change. Martin Sjolund will become President and CEO effective June 17, 2025, succeeding current CEO Vik Atal, who will serve as a senior advisor through year-end.

The following slide details Sjolund’s background and qualifications:

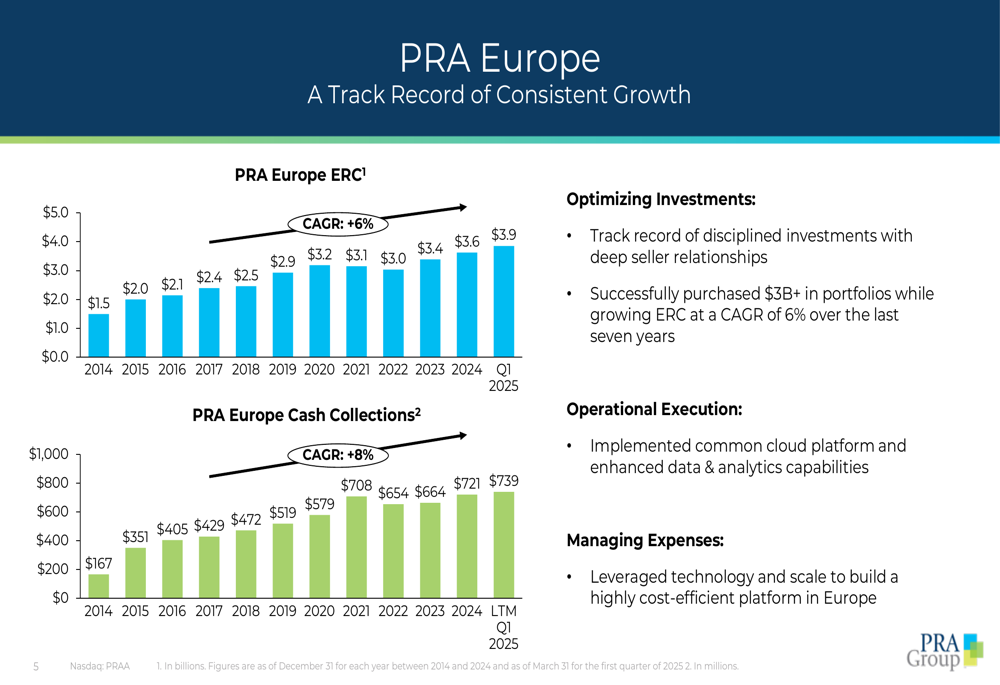

Sjolund brings 13 years of experience at PRA Group, including seven years as President of PRA Group Europe. Under his leadership, the European division has shown consistent growth, with ERC increasing at a compound annual growth rate (CAGR) of 6% from $1.5 billion in 2014 to $3.9 billion in Q1 2025. Similarly, European cash collections have grown at an 8% CAGR over the same period.

The European business performance under Sjolund’s leadership is illustrated in this chart:

Financial Position

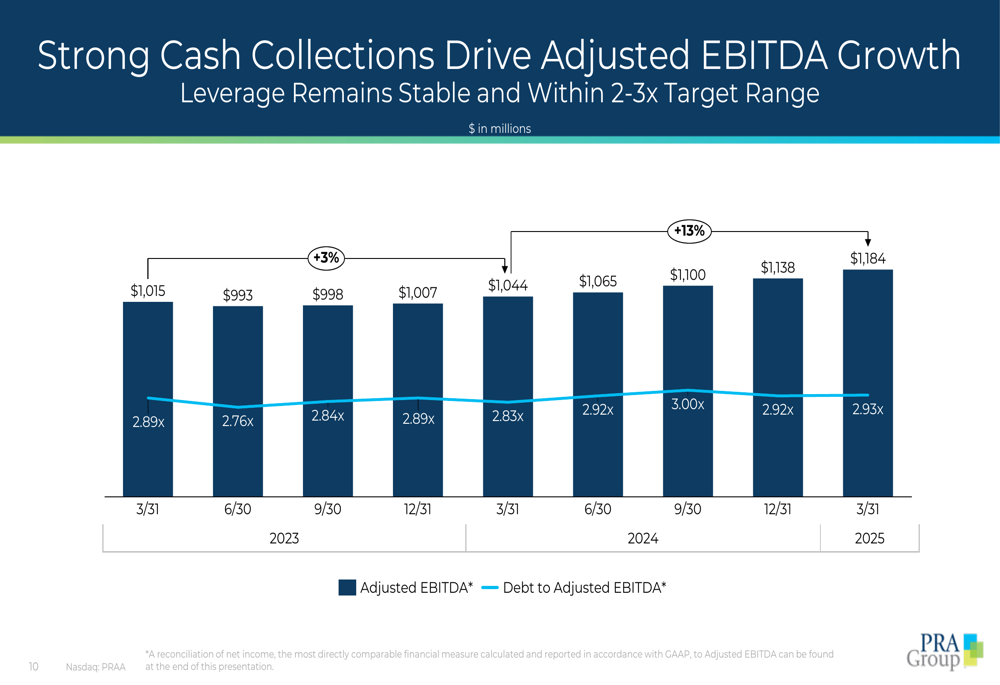

PRA Group maintained a relatively stable financial position with a debt-to-adjusted EBITDA ratio of 2.93x, slightly higher than the previous year. Adjusted EBITDA grew 13% year-over-year to $1,184 million, marking the seventh consecutive quarter of sequential growth in this metric.

The company’s adjusted EBITDA growth and leverage trends are shown here:

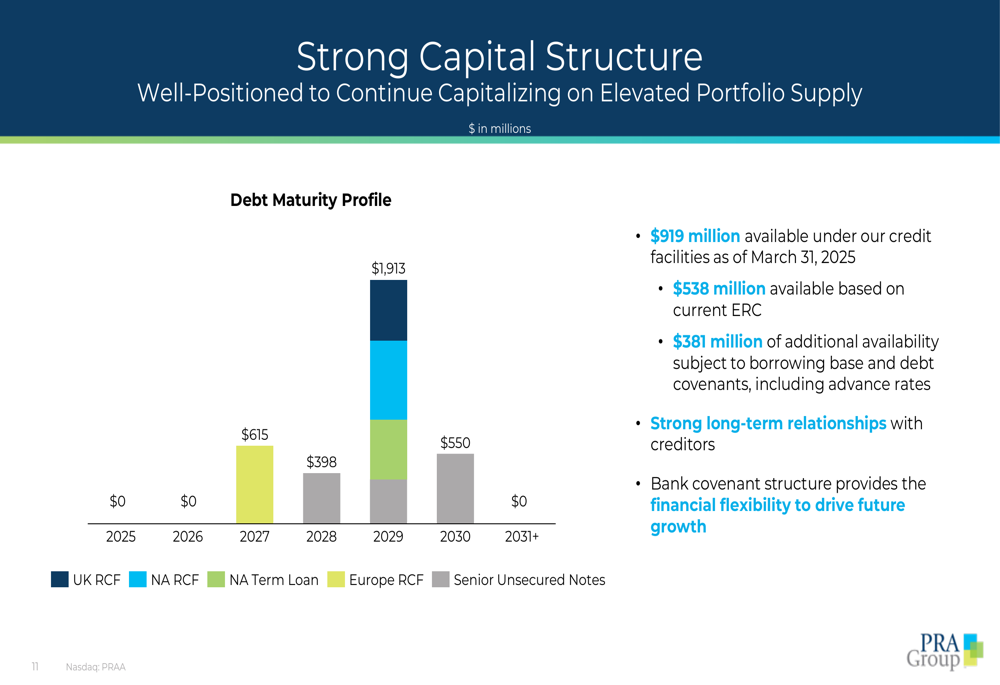

The debt buyer reported $919 million available under its credit facilities as of March 31, 2025, with $538 million available based on current ERC and an additional $381 million subject to borrowing base and debt covenants. This liquidity position provides financial flexibility to support continued portfolio investments.

The company’s debt maturity profile is illustrated in this chart:

Forward-Looking Statements

PRA Group expressed confidence in its business trajectory, citing a positive start to the year with encouraging results on key financial metrics. Management indicated the company is well-positioned for continued success with the upcoming transition to a new CEO.

The company’s European business model, which has shown consistent growth under incoming CEO Martin Sjolund, is expected to inform the global strategy moving forward. This includes continued focus on disciplined investments, technological enhancements, and cost efficiency.

While specific guidance for the remainder of 2025 was limited, the company’s strategic focus on portfolio investments, operational execution, and expense management suggests continued emphasis on growing ERC and cash collections while improving operational efficiency.

The after-hours stock decline of 6.25% indicates investors may have concerns about the modest net income despite strong operational metrics, potentially signaling expectations for more substantial bottom-line improvement in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.