S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Premium Brands Holdings Corporation (TSX:PBH) presented its second quarter 2024 results on August 8, 2024, highlighting record performance and continued momentum in its growth strategy. The specialty food manufacturer and distributor reported significant progress in its U.S. expansion initiatives while maintaining a robust acquisition pipeline.

The company’s stock closed at $87.84 on August 1, 2025, down 0.83% for the day, but has shown resilience with a 52-week range of $72.57 to $97.10. Premium Brands continues to position itself as a consolidator in the specialty foods sector, with particular emphasis on protein-based products and bakery offerings.

Quarterly Performance Highlights

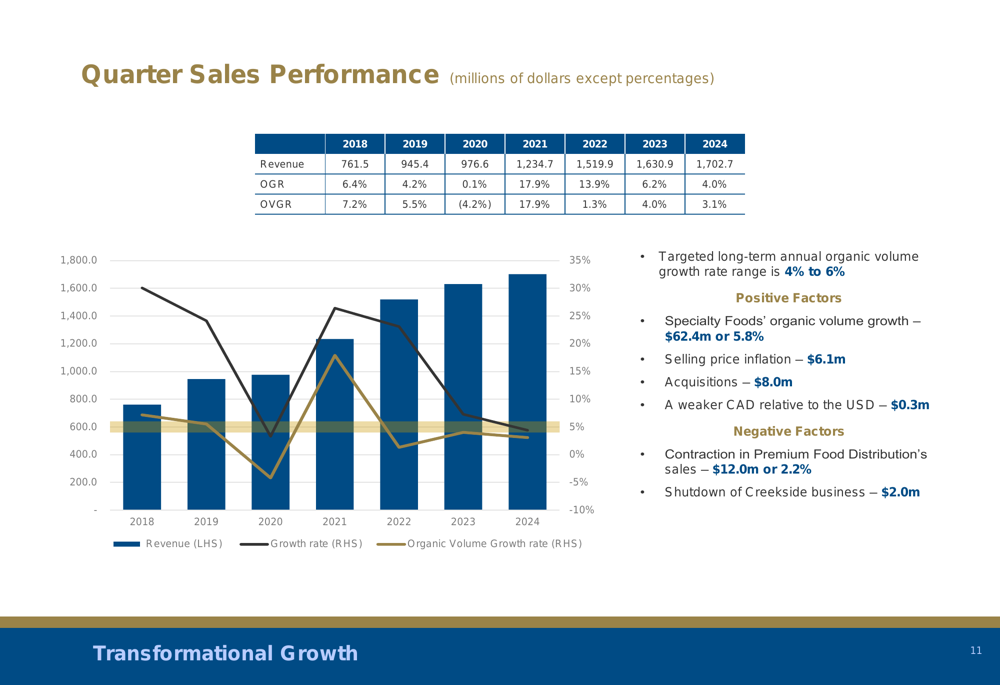

Premium Brands achieved record second quarter revenue of $1.7 billion, representing a 4.4% increase ($71.8 million) compared to the second quarter of 2023. This growth was primarily driven by strong organic volume growth in the Specialty Foods segment, which contributed $62.4 million or 5.8% to the overall increase.

As shown in the following chart of quarterly revenue performance, the company has maintained consistent growth despite market challenges:

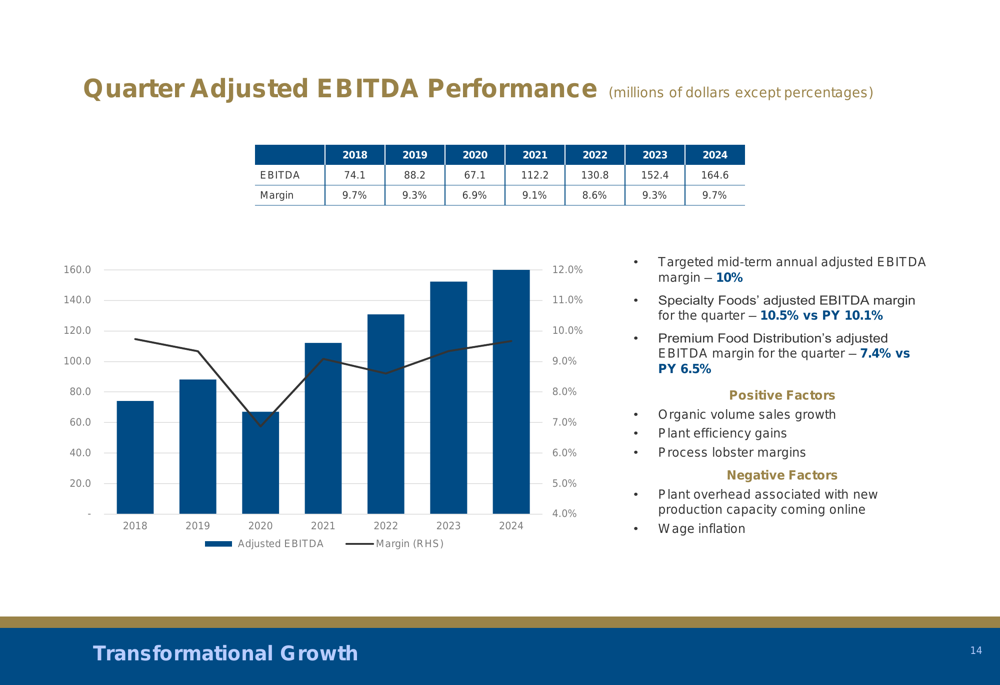

The company also reported record second quarter adjusted EBITDA of $164.6 million, an 8.0% increase ($12.2 million) from the prior year. More importantly, adjusted EBITDA margin improved to 9.7%, up from 9.3% in Q2 2023, moving closer to the company’s mid-term target of 10%.

The following chart illustrates Premium Brands’ quarterly adjusted EBITDA performance:

Specialty Foods’ adjusted EBITDA margin continued to normalize, reaching 10.5% for the quarter, a 40-basis point improvement compared to Q2 2023. Meanwhile, Premium Food Distribution’s adjusted EBITDA margin increased to 7.4% from 6.5% in the prior year period.

U.S. Growth Strategy

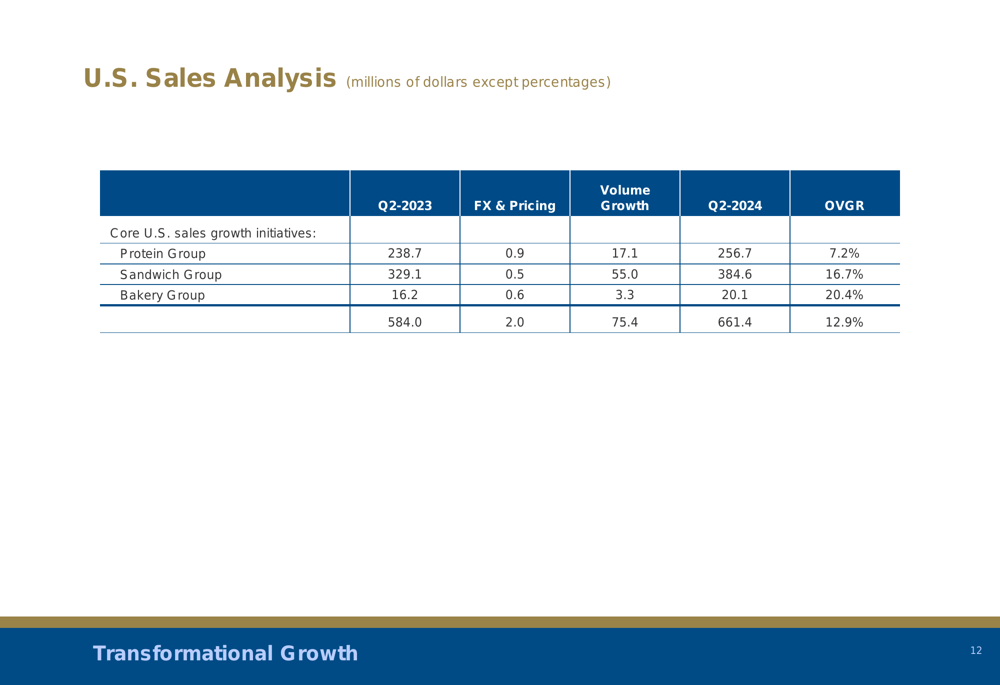

A standout element of Premium Brands’ Q2 performance was the strong progress on its core U.S. growth initiatives. The company’s U.S. operations generated an impressive 12.9% organic volume growth rate, with total sales reaching $661.4 million.

The breakdown of U.S. sales growth by segment reveals particularly strong performance in the Sandwich and Bakery groups:

The Protein Group achieved 7.2% organic volume growth, while the Sandwich Group delivered 16.7% growth and the Bakery Group posted an impressive 20.4% increase. These results align with the company’s long-term strategy of expanding its U.S. presence across multiple specialty food categories.

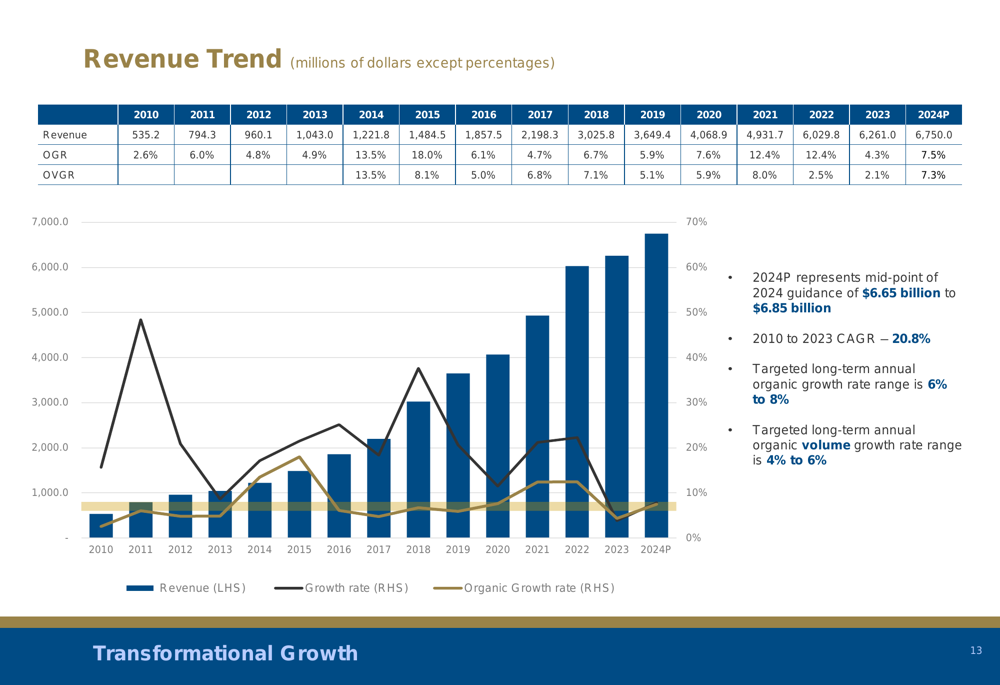

Looking at the longer-term revenue trend, Premium Brands has maintained consistent growth, projecting 2024 revenue of $6.75 billion, representing a 20.8% CAGR since 2010:

Acquisition Pipeline and Expresco Foods

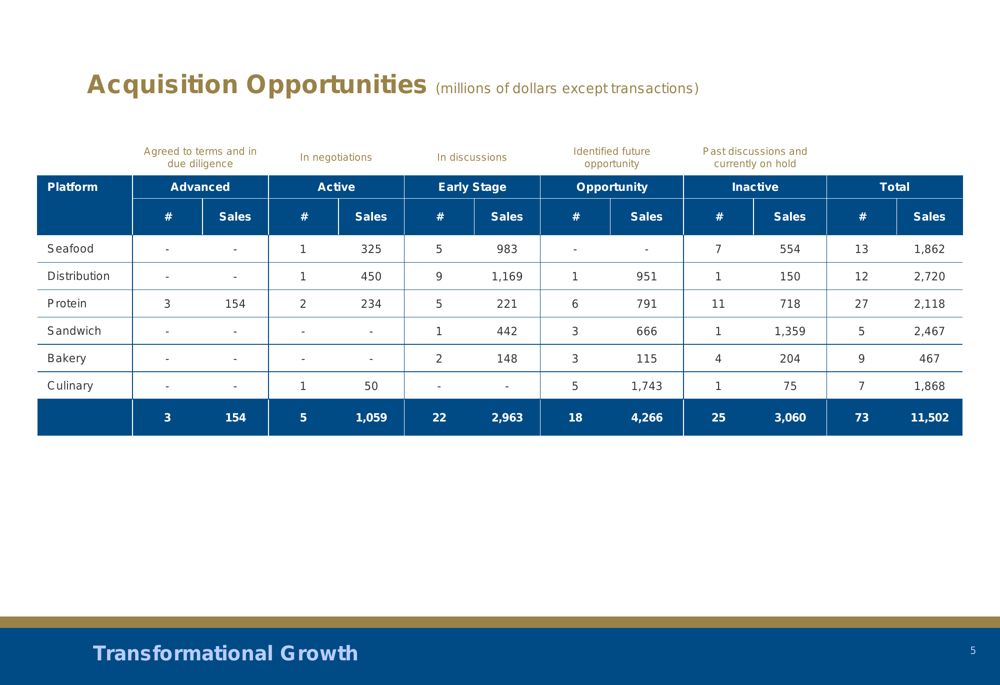

Premium Brands continues to pursue its acquisition-driven growth strategy, with a robust pipeline of potential targets. The company is currently tracking 73 acquisition opportunities representing $11.5 billion in sales across its various platforms.

The following table provides a detailed breakdown of the acquisition pipeline:

Of particular note are the 3 advanced-stage acquisitions with $154 million in sales and 5 active-stage opportunities representing over $1 billion in potential revenue. The company’s disciplined approach to acquisitions has been a cornerstone of its growth strategy.

During the presentation, Premium Brands highlighted its recent acquisition of Expresco Foods, a custom manufacturer of fully cooked grilled protein products for foodservice and retail customers across North America. Expresco operates a 75,000 square foot facility with four modern cooking lines and proprietary skewer-making technology, employing approximately 450 people.

Financial Position and Capital Allocation

Premium Brands’ long-term EBITDA growth trajectory remains strong, with projected 2024 adjusted EBITDA of $640 million, representing a 20.8% CAGR since 2010:

The company reported significant capital expenditures of $94.7 million during the quarter, with $83.2 million allocated to major projects. Management expects to spend an additional $230 million on approved major projects over the next five quarters, with all initiatives expected to generate additional production capacity and improved operating efficiencies.

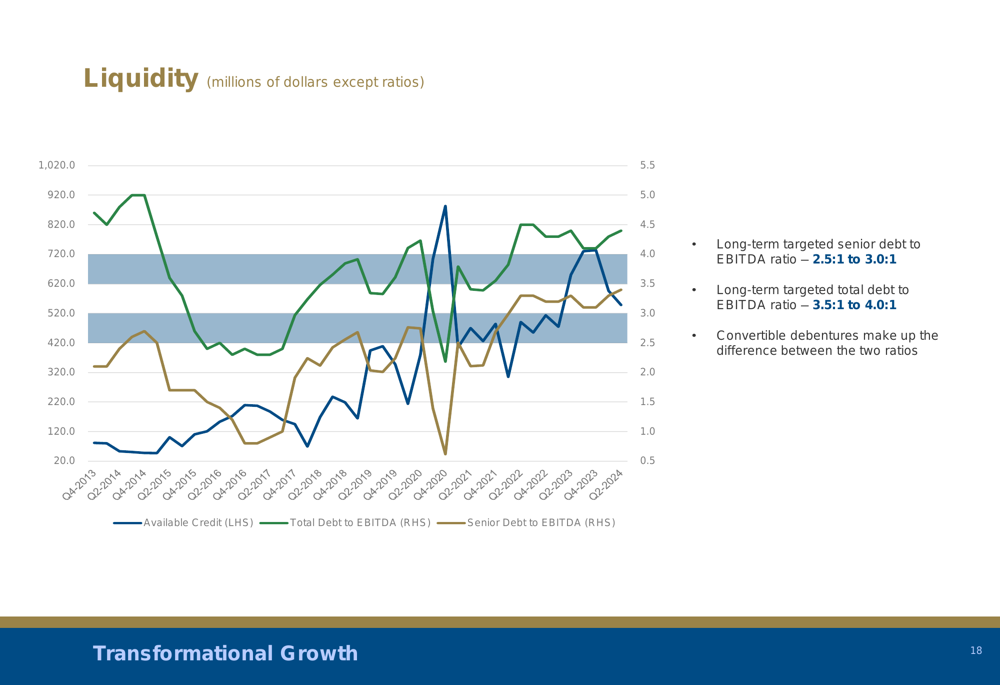

Premium Brands maintains a disciplined approach to leverage, targeting a long-term senior debt to EBITDA ratio of 2.5:1 to 3.0:1 and a total debt to EBITDA ratio of 3.5:1 to 4.0:1. The company’s free cash flow per share is projected to reach $5.70 in 2024, supporting its dividend of $3.40 per share with a payout ratio of 54.3%.

The following chart illustrates the company’s free cash flow and dividend trends:

Forward-Looking Statements

Premium Brands’ presentation emphasized its "Transformational Growth" strategy, focusing on both organic growth initiatives and strategic acquisitions. The company targets long-term annual organic volume growth of 4-6% and overall organic growth of 6-8%.

Management expects continued margin improvement, with a mid-term adjusted EBITDA margin target of 10%. The company’s significant investments in production capacity are anticipated to support future growth, with potential sale and leaseback transactions for the real estate associated with at least two major projects currently in progress.

The company’s robust acquisition pipeline, particularly in the U.S. market, remains a key element of its growth strategy. With 30 potential acquisitions in advanced or active stages representing over $1.2 billion in sales, Premium Brands is well-positioned to continue its consolidation strategy in the specialty foods sector.

Given the company’s consistent execution of its growth strategy and improving margins, Premium Brands appears well-positioned to continue its trajectory of record performance in the coming quarters, despite ongoing challenges in certain market segments and temporary headwinds from capacity expansion investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.