C3is Inc. closes $2 million registered direct offering

Introduction & Market Context

Priority Technology Holdings, Inc. (NASDAQ:PRTH) reported its first quarter 2025 financial results on May 6, 2025, showcasing continued growth across all business segments. The payment technology company maintained its momentum from the previous quarter, with revenue and profitability metrics exceeding comparable periods from the prior year.

The company’s stock closed at $7.57 on May 5, down 2.95% for the day, but showed signs of recovery in after-hours trading with a 2.11% gain to $7.73. This performance comes amid a broader market environment where payment processors face both opportunities from digital transformation and challenges from rising competition.

Quarterly Performance Highlights

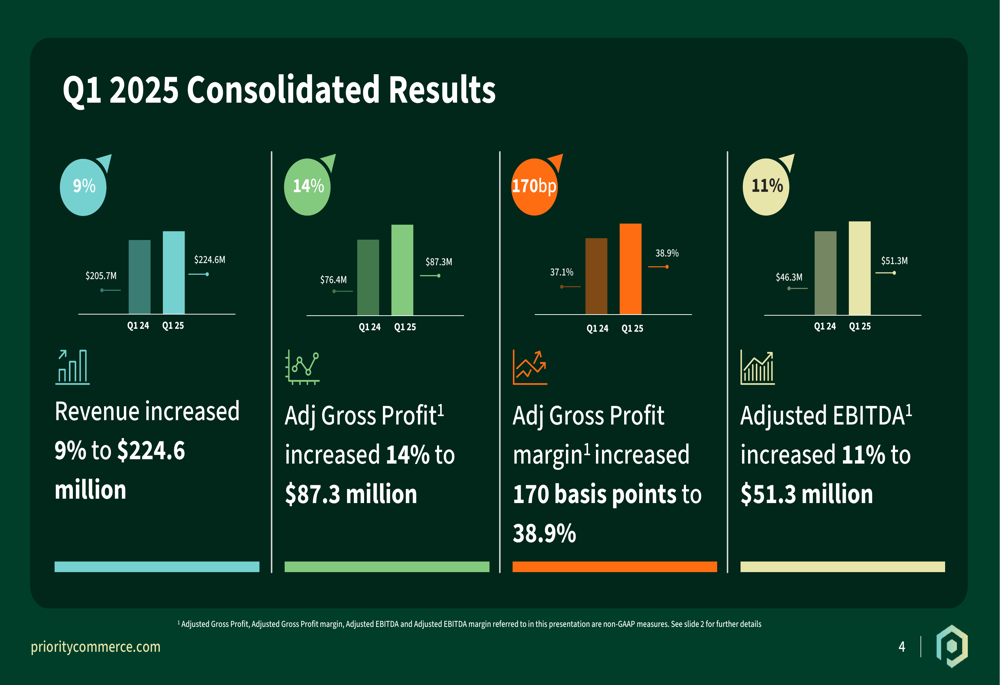

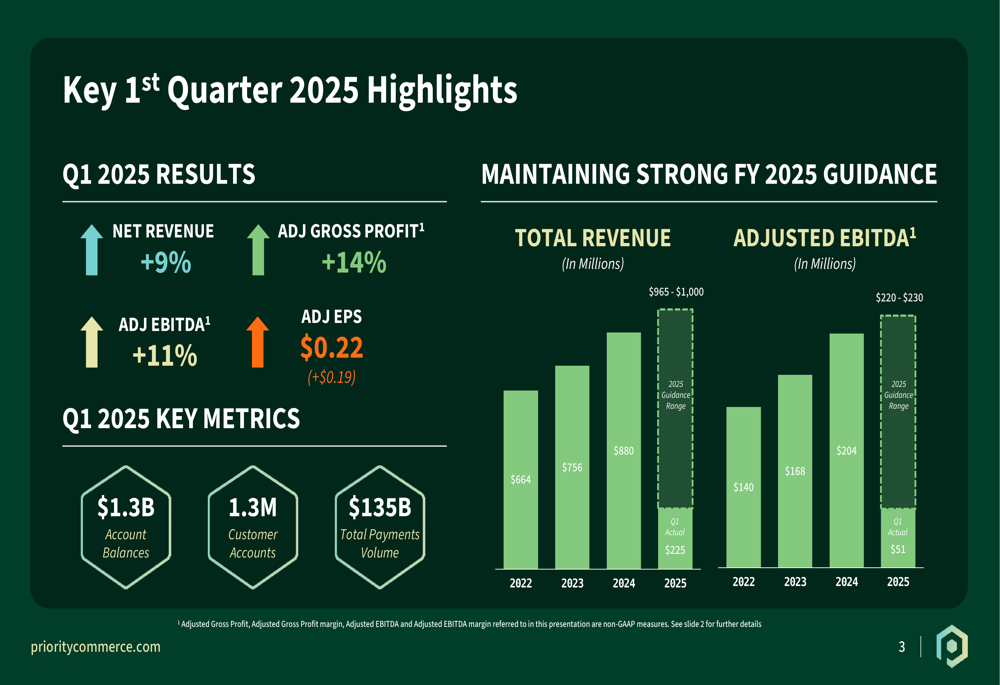

Priority Technology delivered solid financial results for Q1 2025, with revenue increasing 9% year-over-year to $224.6 million. The company reported significant improvements across key profitability metrics, with Adjusted EBITDA growing 11% to $51.3 million and Adjusted Gross Profit rising 14% to $87.3 million compared to Q1 2024.

As shown in the following consolidated results chart:

Notably, the company’s Adjusted Gross Profit margin expanded by 170 basis points to 38.9%, reflecting Priority’s successful shift toward higher-margin business segments. Adjusted earnings per share increased to $0.22, representing a $0.19 improvement year-over-year.

The company also reported impressive operational metrics, including $1.3 billion in account balances, 1.3 million customer accounts, and total payments volume of $135 billion for the quarter.

Segment Analysis

Priority Technology operates through three main segments: SMB (Small and Medium Business), B2B (Business-to-Business), and Enterprise. Each segment demonstrated growth in Q1 2025, though at varying rates.

The SMB segment, which historically represented the largest portion of Priority’s business, grew revenue by 5% year-over-year to $151.7 million. This growth was primarily driven by a 10% increase in core business, partially offset by attrition in the historical residual portfolio and risk-paring in specialized acquiring. The segment processed $17.7 billion in card volumes, a 3% increase from the prior year.

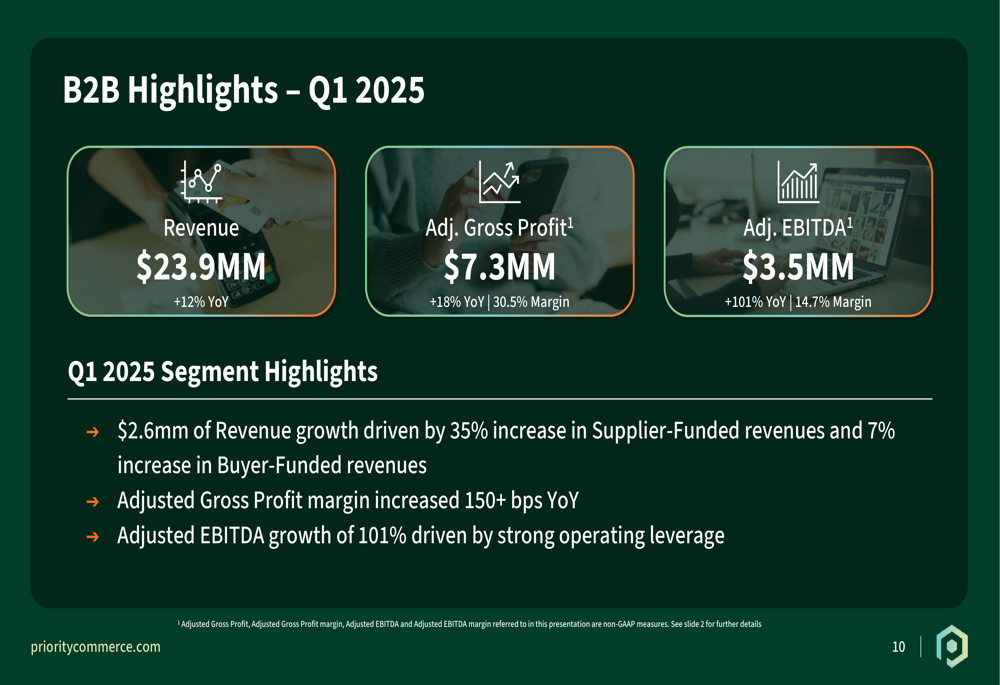

The B2B segment showed stronger growth, with revenue increasing 12% year-over-year to $23.9 million. This growth was driven by a 35% increase in Supplier-Funded revenues and a 7% increase in Buyer-Funded revenues. Most impressive was the segment’s Adjusted EBITDA, which grew 101% year-over-year to $3.5 million, demonstrating significant operating leverage.

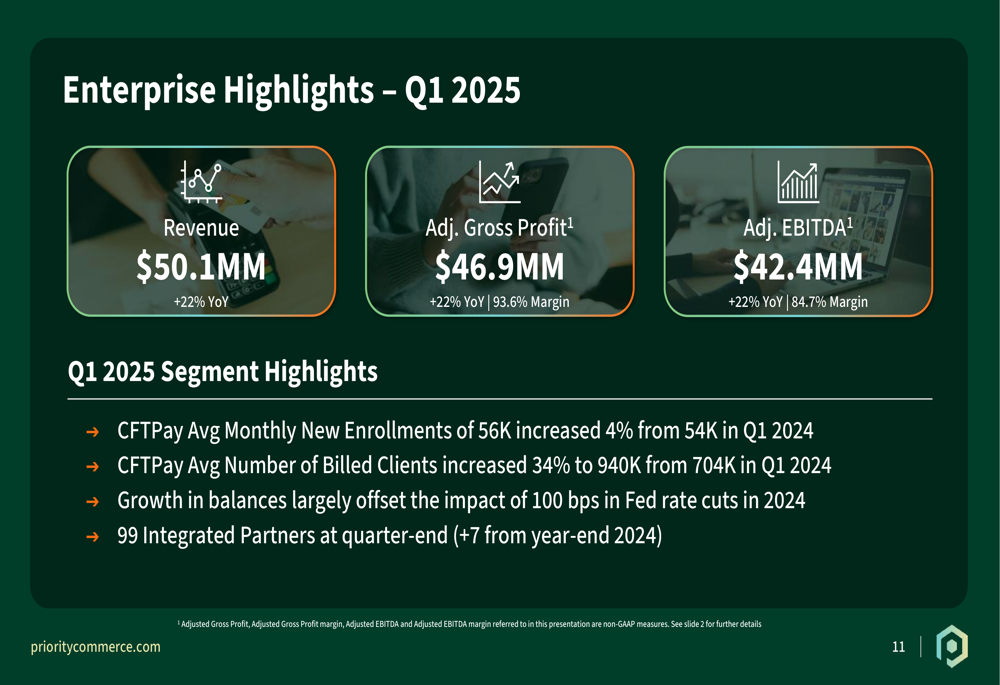

The Enterprise segment delivered the strongest performance, with revenue growing 22% year-over-year to $50.1 million. This segment maintains exceptionally high margins, with a 93.6% Adjusted Gross Profit margin and 84.7% Adjusted EBITDA margin. Key drivers included a 34% increase in average billed clients to 940,000 and continued growth in partner integrations, which reached 99 by quarter-end.

Strategic Initiatives & Business Mix

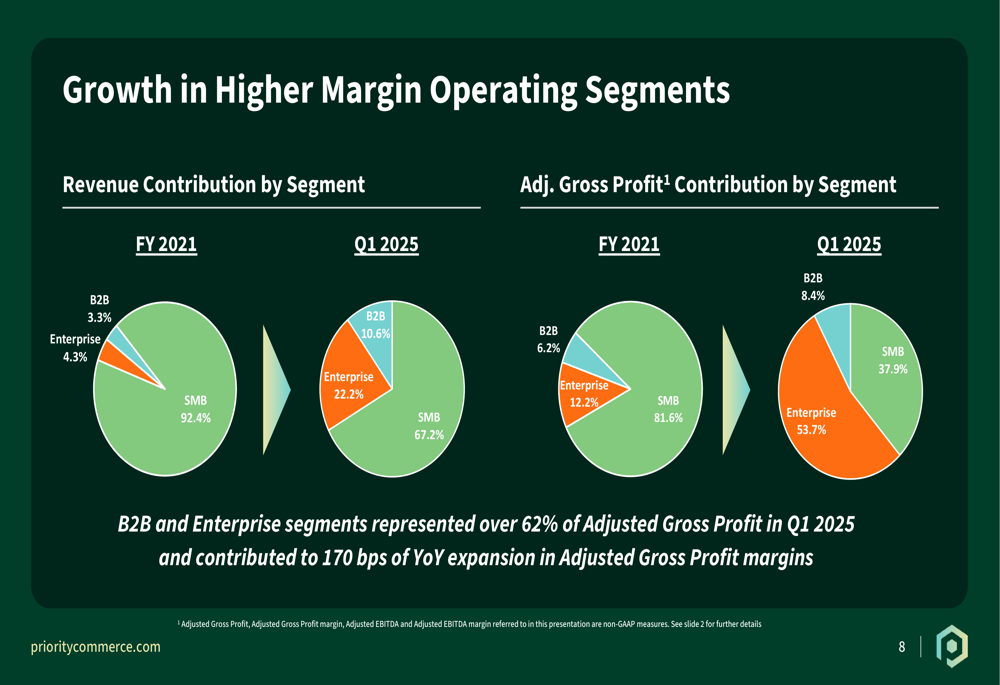

A significant strategic shift is evident in Priority’s business mix, with higher-margin Enterprise and B2B segments now representing a much larger portion of the company’s overall profit. As illustrated in the following chart, these segments accounted for over 62% of Adjusted Gross Profit in Q1 2025, compared to just 18.4% in FY 2021:

This transformation has been instrumental in driving the company’s margin expansion. The Enterprise segment, with its near-94% gross profit margin, now contributes 53.7% of total Adjusted Gross Profit, up dramatically from 12.2% in FY 2021.

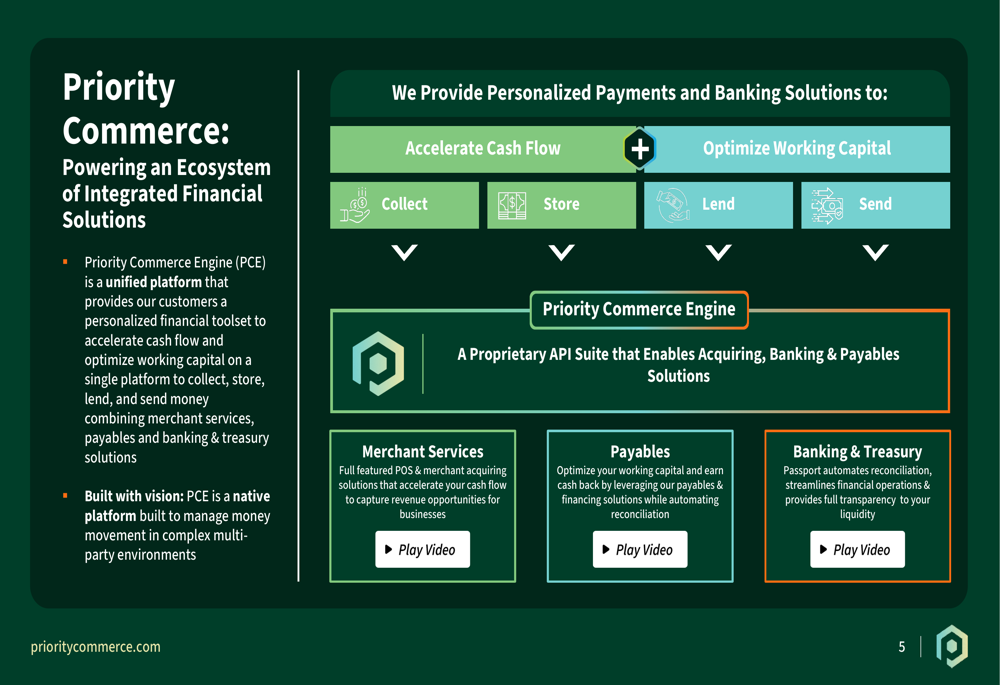

Priority’s business model centers around its Priority Commerce Engine (PCE), a unified platform that provides integrated financial solutions. The platform combines merchant services, payables, and banking & treasury solutions to help customers accelerate cash flow and optimize working capital.

The company generates revenue through multiple streams, including monthly platform SaaS fees, interchange on card volume, payment processing fees, and float income on funds held in Passport accounts.

Financial Position & Outlook

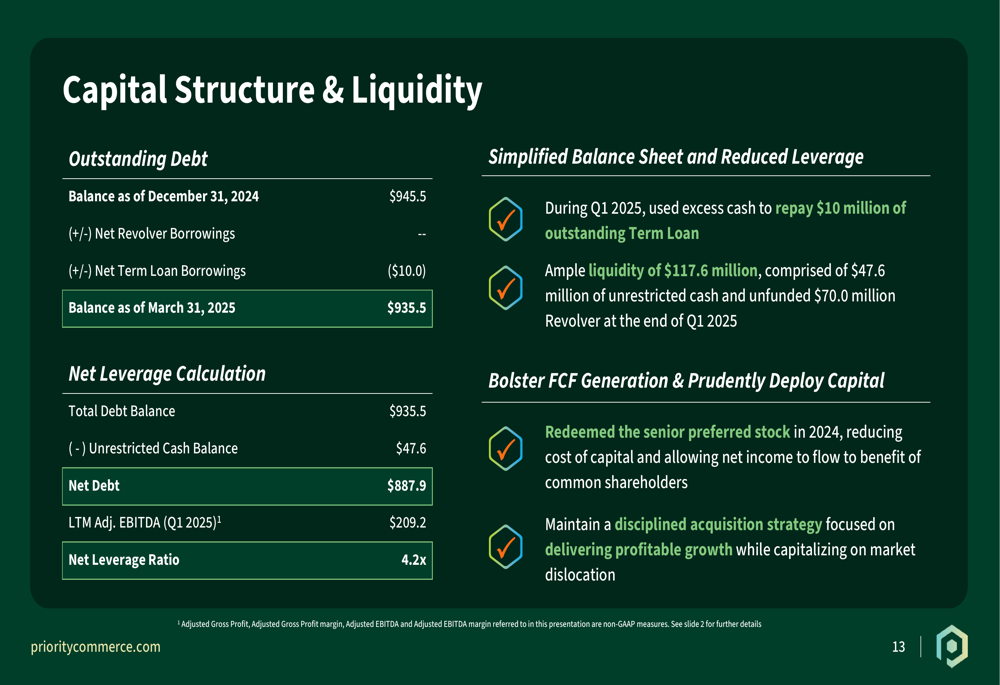

Priority Technology maintained a solid financial position in Q1 2025, using excess cash to reduce its term loan by $10 million. As of March 31, 2025, the company reported total debt of $935.5 million, unrestricted cash of $47.6 million, and a net leverage ratio of 4.2x based on last twelve months Adjusted EBITDA of $209.2 million.

The company maintained strong liquidity of $117.6 million, comprising $47.6 million in unrestricted cash and an unfunded $70 million revolver. This financial flexibility positions Priority well for both organic growth and potential strategic acquisitions.

Looking ahead, Priority Technology reaffirmed its full-year 2025 guidance, projecting total revenue between $965 million and $1 billion and Adjusted EBITDA between $220 million and $230 million. This outlook represents continued growth from 2024, when the company reported full-year revenue of $879.7 million.

The company’s Q1 performance, with revenue growth of 9%, appears to be tracking toward the lower end of its full-year guidance range of 10-14% growth. However, the continued shift toward higher-margin segments suggests that profitability metrics may outperform revenue growth, as evidenced by the 11% increase in Adjusted EBITDA during the quarter.

As Priority Technology continues to execute its strategy of expanding higher-margin business segments while maintaining disciplined capital allocation, investors will be watching closely to see if the company can maintain its growth trajectory in an increasingly competitive payment processing landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.