CCH Holdings prices IPO at $4 per share on NASDAQ

Introduction & Market Context

Promotora de Informaciones SA (BME:PRS), the Spanish media and education group, presented its H1 2025 results on July 29, highlighting operational improvements and financial stabilization despite currency headwinds. The company reported growth in its digital subscription business and detailed the positive impact of its recent refinancing agreement, which has provided greater financial flexibility.

PRISA’s presentation emphasized the company’s continued focus on digital transformation across both its education platform Santillana and its media properties, with subscription growth serving as a key performance indicator. The results come at a time when media companies globally are navigating the transition to digital-first business models while managing macroeconomic challenges.

Executive Summary

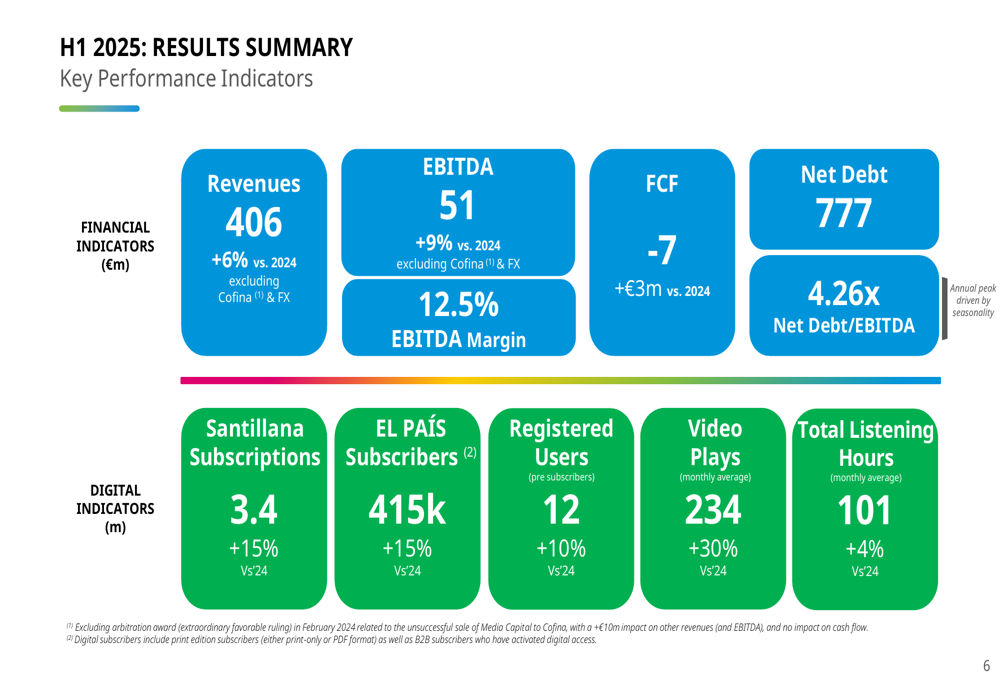

PRISA reported positive operating performance in H1 2025, with Group EBITDA growing by 9% and revenues increasing by 6% on a constant currency basis, excluding the extraordinary impact of the Cofina (ELI:CFN) arbitration award from the previous year. The company highlighted significant subscription growth, with Santillana’s Learning Systems subscriptions rising to 3.4 million (+15%) and El País reaching 426,000 subscribers (+13%).

As shown in the following comprehensive results summary, the company achieved these results while maintaining a strong liquidity position:

The second quarter delivered particularly strong results, with revenue up 3% (20% at constant currency) and a significant improvement in reported EBITDA, which turned from -€3 million in Q2 2024 to +€5 million in Q2 2025. Free cash flow improved by 31% in H1 2025, reflecting the company’s focus on operational efficiency.

Detailed Financial Analysis

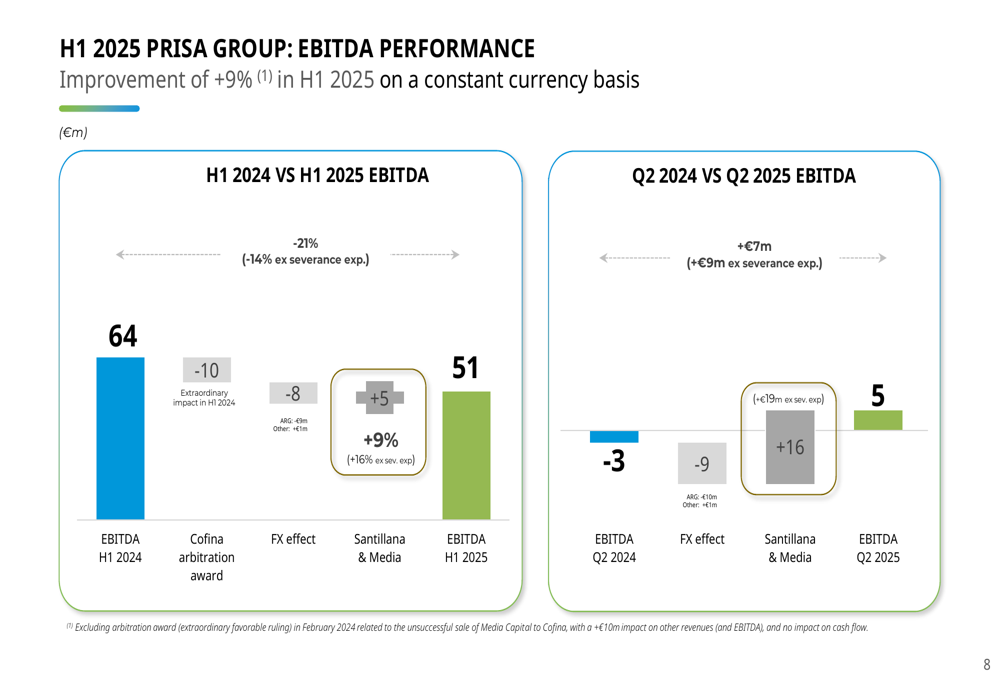

PRISA’s EBITDA performance shows improvement when adjusted for currency effects and one-off items. The company’s H1 2025 EBITDA reached €51 million, compared to €64 million in H1 2024, with the difference primarily attributed to the Cofina arbitration award (-€10 million) and FX effects (-€8 million). On a comparable basis, the underlying business showed a €5 million improvement.

The following chart illustrates the EBITDA evolution:

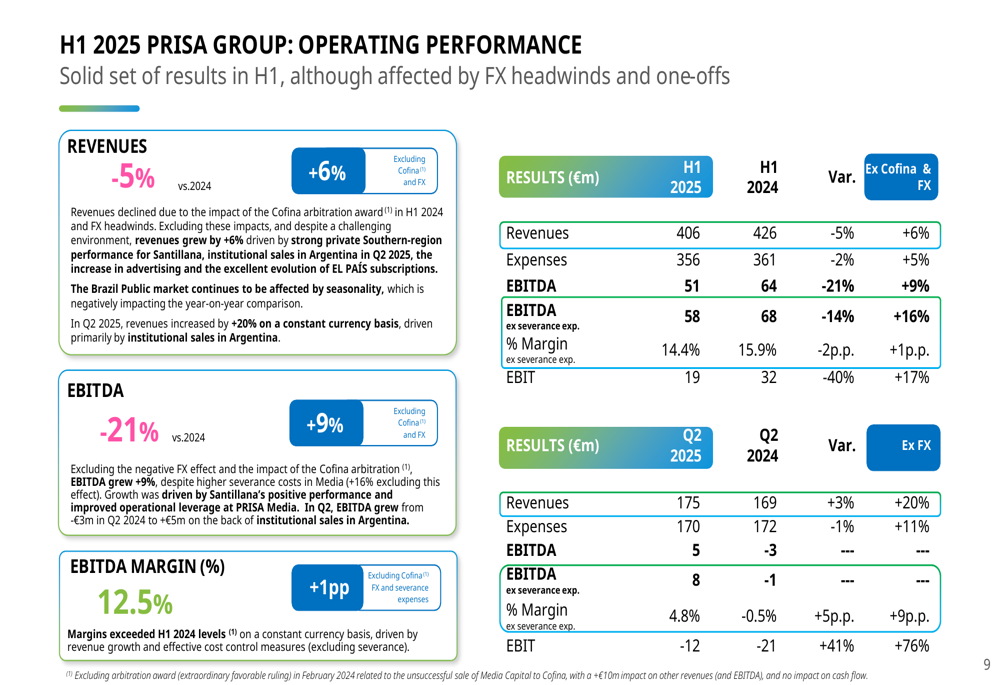

The company’s operating performance was solid despite reported figures being affected by currency headwinds and one-offs. Excluding these factors, revenues grew by 6% and EBITDA by 9% compared to H1 2024:

Net income showed significant improvement, particularly in Q2 2025, driven by the positive impact of the refinancing agreement. Financial results improved due to lower interest expenses (-16%) and a positive accounting impact from the refinancing agreement in Q2 2025 (+€10 million), which offset negative FX effects and hedging revenues recorded in 2024.

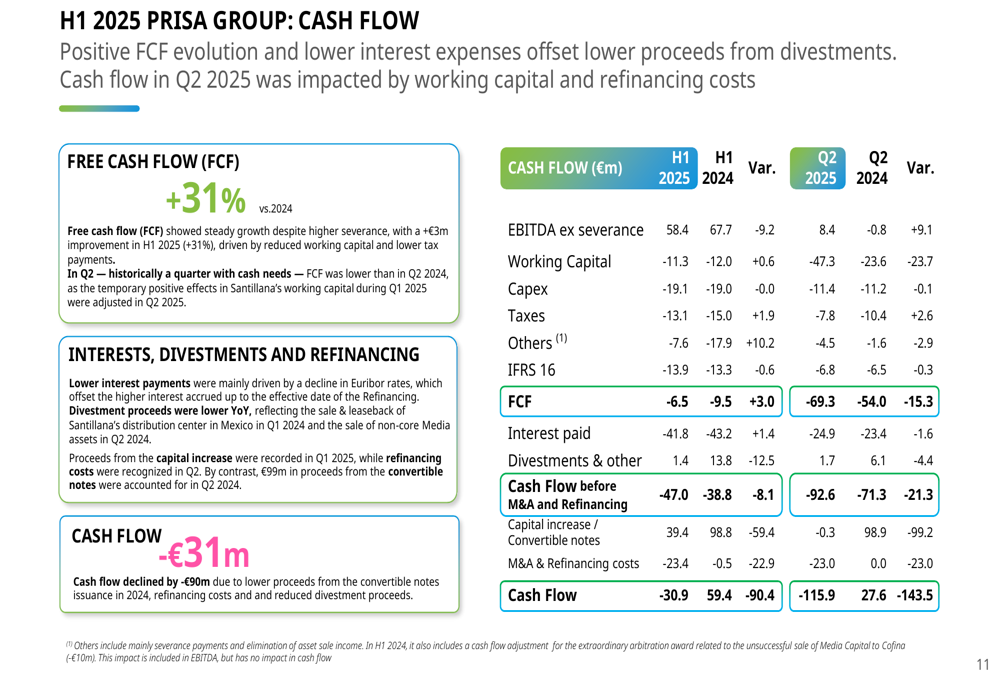

PRISA’s cash flow evolution was positive, with free cash flow improving by 31% compared to 2024:

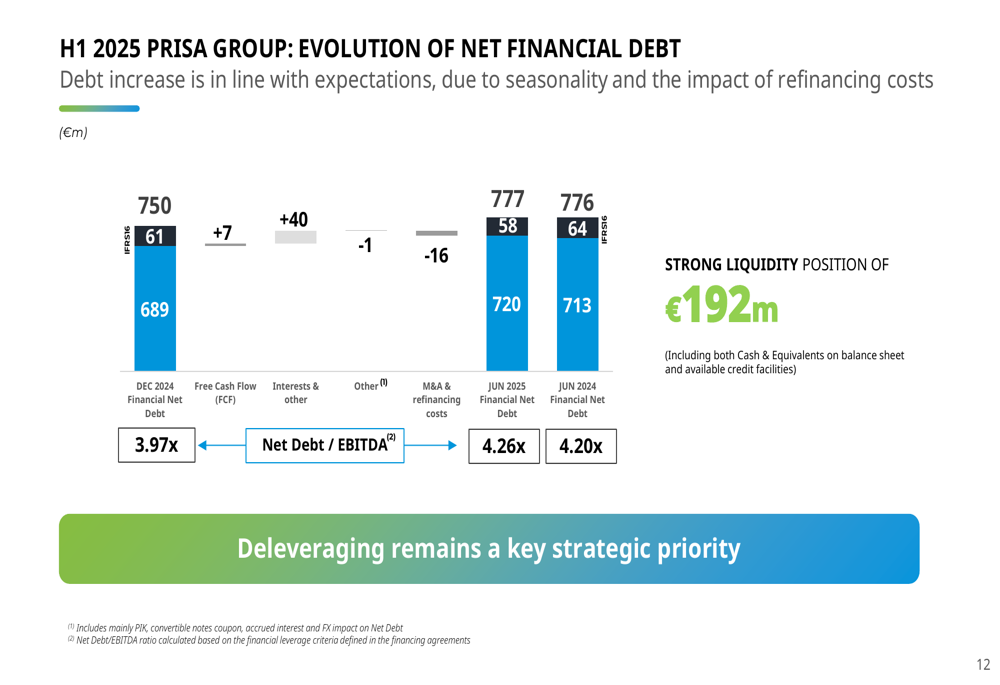

The company’s net financial debt increased slightly, in line with expectations due to seasonality and the impact of refinancing costs. As of June 2025, financial net debt stood at €720 million (€777 million including IFRS16), resulting in a Net Debt/EBITDA ratio of 4.26x. The company maintained a strong liquidity position of €192 million.

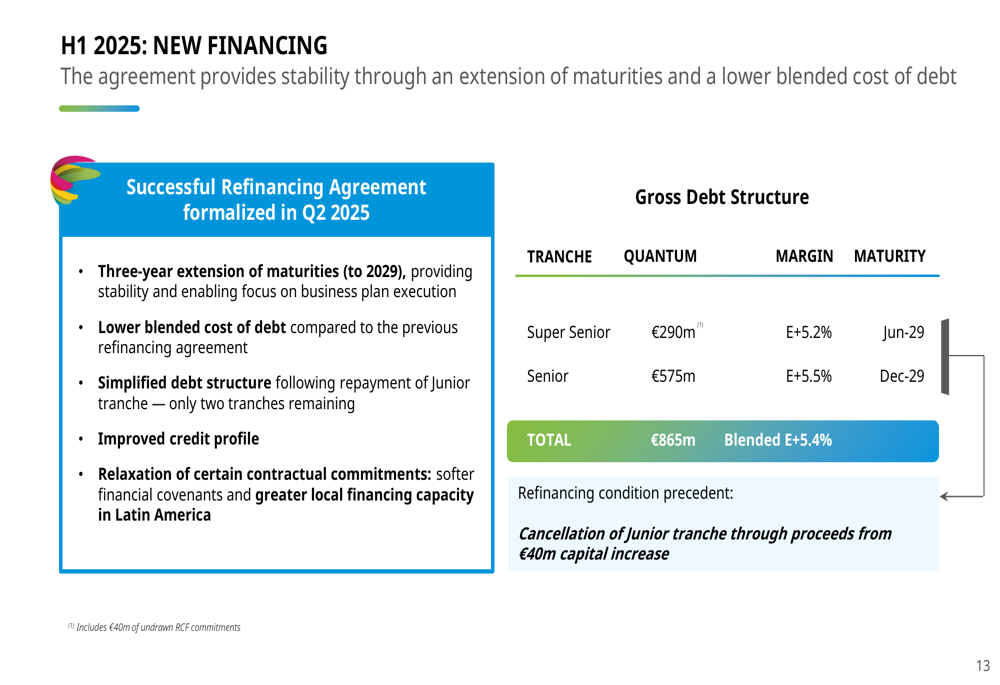

A key development in Q2 was the formalization of PRISA’s refinancing agreement, which provides stability through an extension of maturities and a lower blended cost of debt. The agreement extends maturities by three years (to 2029), simplifies the debt structure, and improves the company’s credit profile:

Strategic Initiatives

PRISA continues to focus on its two core business segments: education (Santillana) and media.

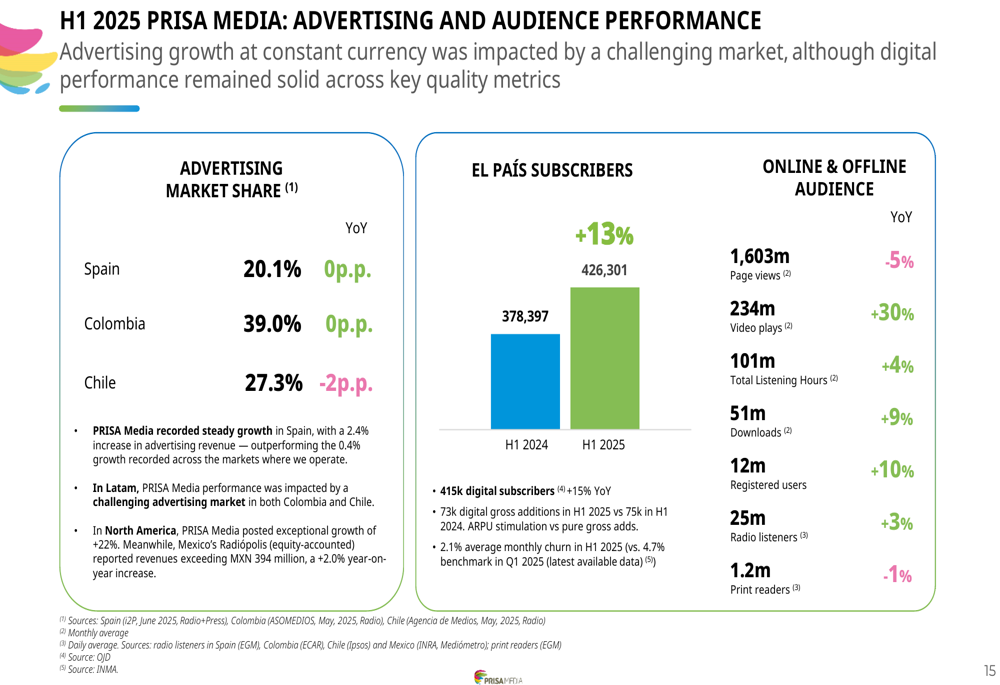

In the media segment, the company maintained stable market share in its key advertising markets: Spain (20.1%), Colombia (39.0%), and Chile (27.3%). Digital engagement metrics showed strong growth, with video plays increasing by 30% year-over-year and total listening hours up 4%. El País, the company’s flagship newspaper, reached 426,301 subscribers, representing 13% growth compared to H1 2024.

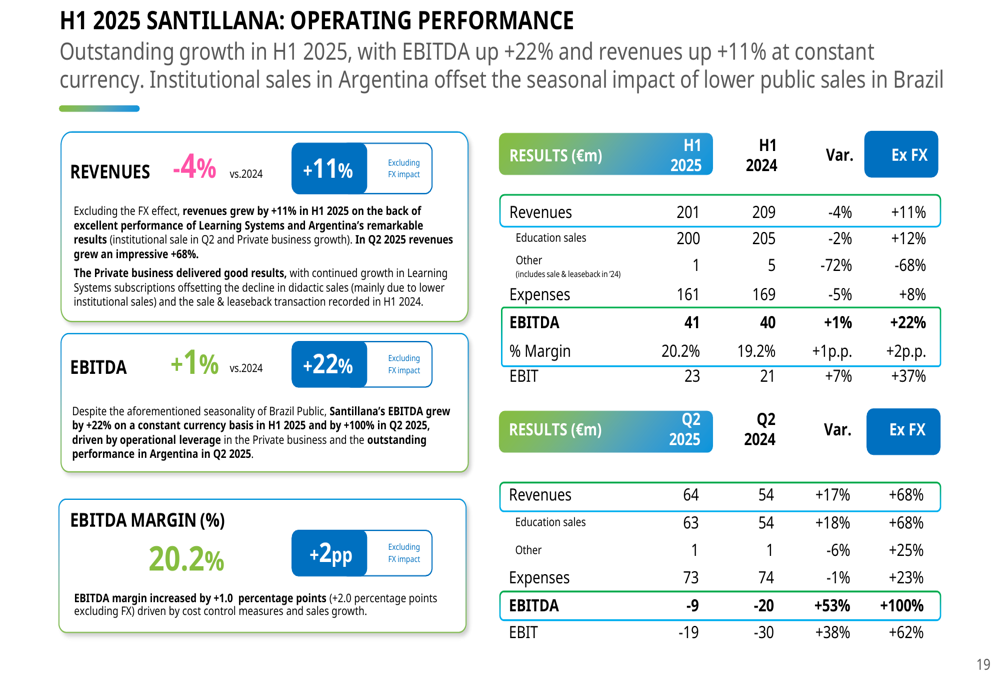

The education segment, Santillana, showed robust performance, particularly in learning systems subscriptions, which grew by 15%. Despite currency headwinds, Santillana’s revenues grew by 11% and EBITDA by 22% on a constant currency basis:

PRISA also emphasized its commitment to sustainability, highlighting a joint awareness campaign with the UN Global Compact Spain called ’Act for the Sustainability of the Planet.’ The company continues to focus on responsible governance and creating positive impact on people and society.

Forward-Looking Statements

Looking ahead, PRISA’s management indicated that results are on track with expectations despite a challenging environment. The company continues to work on its Strategic Plan, focusing on digital transformation, subscription growth, and financial stability.

The refinancing agreement completed in Q2 2025 provides a more stable financial foundation, with extended maturities and lower interest costs. This should allow the company to focus on operational improvements and strategic initiatives in the coming quarters.

PRISA remains committed to its dual focus on education and media, with digital transformation at the core of both segments. The growth in subscriptions for both Santillana’s learning systems and El País indicates that this strategy is gaining traction, though currency volatility remains a challenge for the company’s international operations.

The company’s management expressed confidence that the positive operating performance seen in H1 2025 will continue, supported by the strengthened financial position resulting from the new refinancing agreement and ongoing cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.