Bitcoin price today: steadies after record high over $126k amid "Uptober" optimism

Introduction & Market Context

Privia Health Group Inc (NASDAQ:PRVA) presented its second quarter 2025 results on August 7, 2025, highlighting strong performance across all key metrics and raising its full-year guidance. Despite the positive operational results, the company’s shares plunged 16.53% to $16.51 in pre-market trading, suggesting investors may have found reasons for concern beyond the headline numbers.

The healthcare provider, which operates one of the largest primary care networks in the United States, reported significant growth in practice collections, implemented providers, and profitability metrics. CEO Parth Mehrotra and CFO David Mountcastle led the presentation, emphasizing the company’s differentiated business model and consistent execution.

Quarterly Performance Highlights

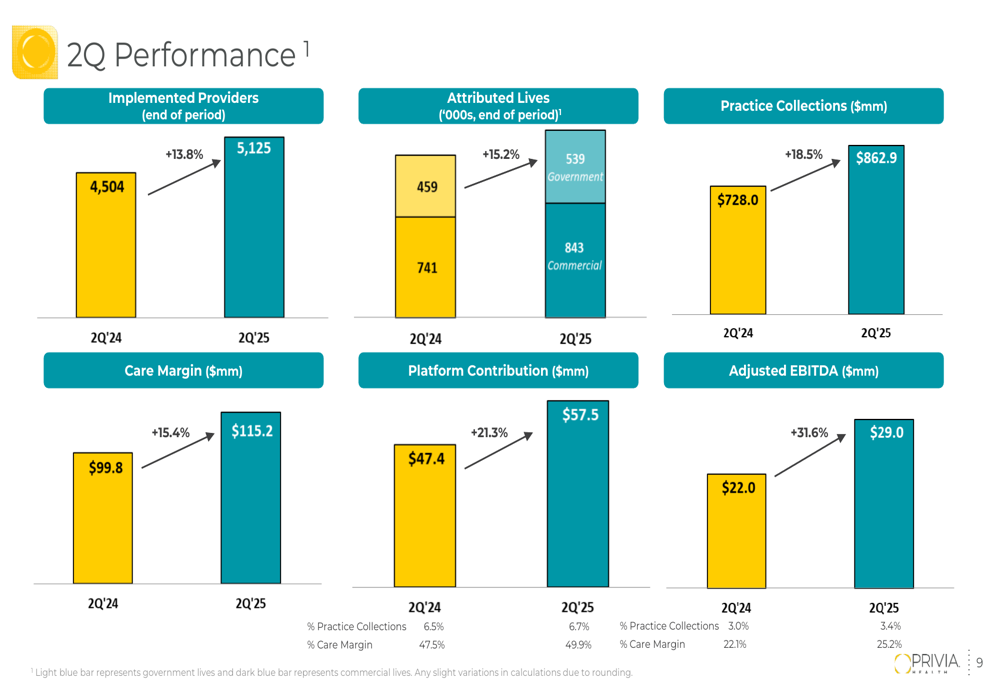

Privia Health delivered impressive growth across all key performance indicators in the second quarter of 2025. The company’s implemented providers increased by 13.8% year-over-year to 5,125, while attributed lives grew by 15.2% to 1.38 million across both commercial and government programs.

Practice collections, a key revenue metric for the company, jumped 18.5% compared to Q2 2024, reaching $862.9 million. This acceleration from the 12.8% growth reported in Q1 2025 demonstrates strengthening momentum in the company’s core business.

As shown in the following chart detailing Q2 performance metrics:

Profitability showed even stronger improvement, with Adjusted EBITDA increasing by 31.6% year-over-year to $29.0 million. The Adjusted EBITDA margin expanded to 25.2%, representing a 310 basis point improvement compared to the same period last year. Platform contribution, another key profitability metric, grew by 21.3% to $57.5 million.

Financial Analysis

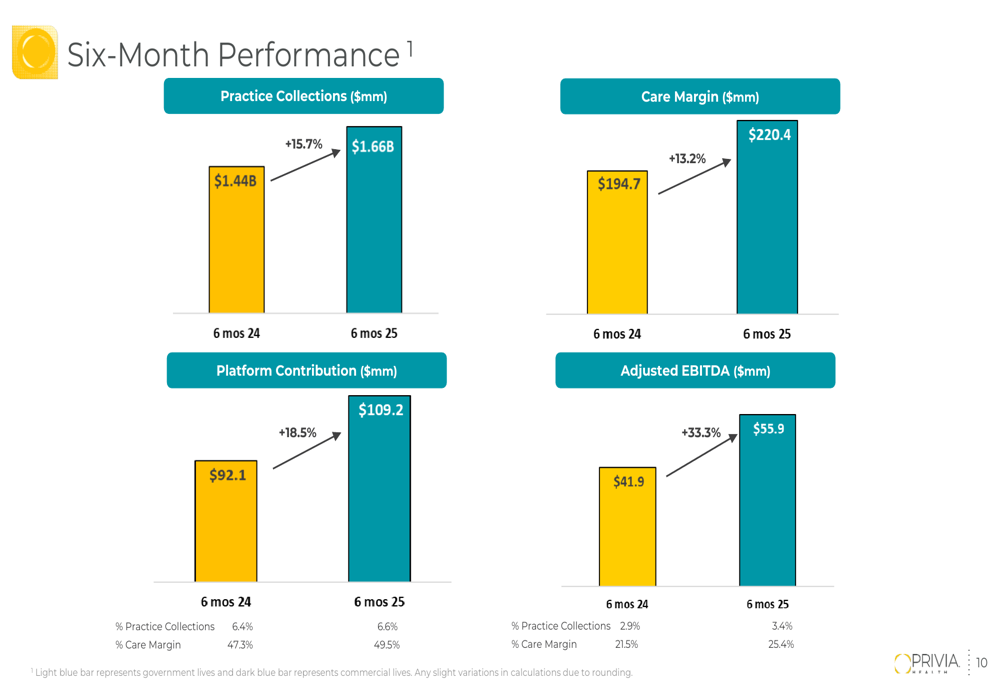

The six-month performance figures further reinforce Privia’s growth trajectory, with practice collections up 15.7% to $1.66 billion and Adjusted EBITDA increasing by 33.3% to $55.9 million compared to the first half of 2024.

The company’s six-month results demonstrate consistent execution across all financial metrics:

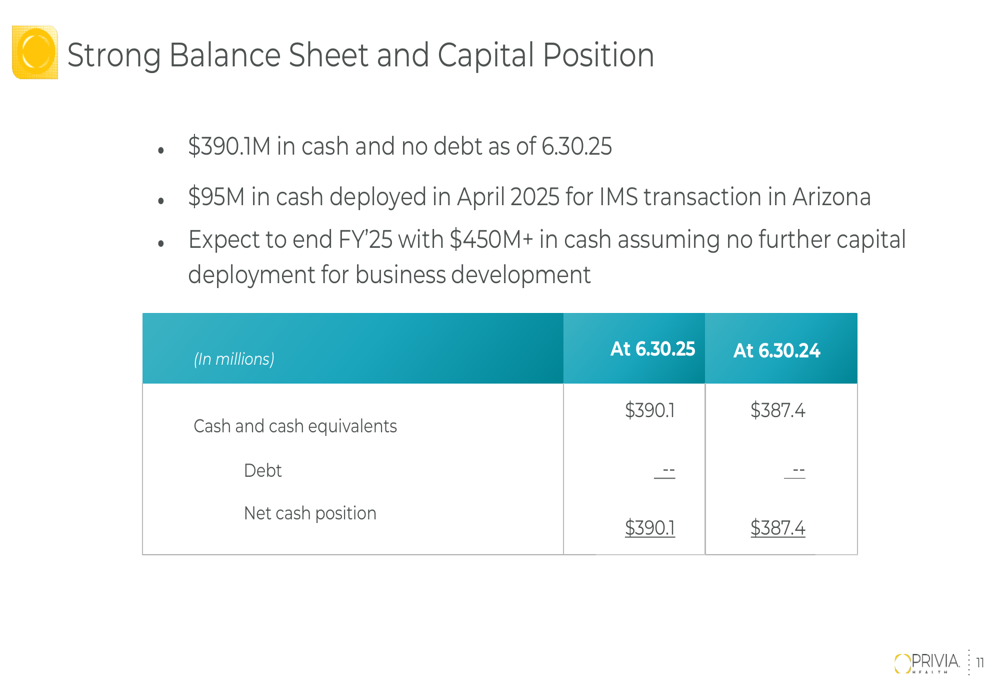

Privia maintains a strong balance sheet with $390.1 million in cash and no debt as of June 30, 2025. The company deployed $95 million in April 2025 for the IMS transaction in Arizona, expanding its geographic footprint. Management expects to end fiscal year 2025 with over $450 million in cash, assuming no further capital deployment for business development.

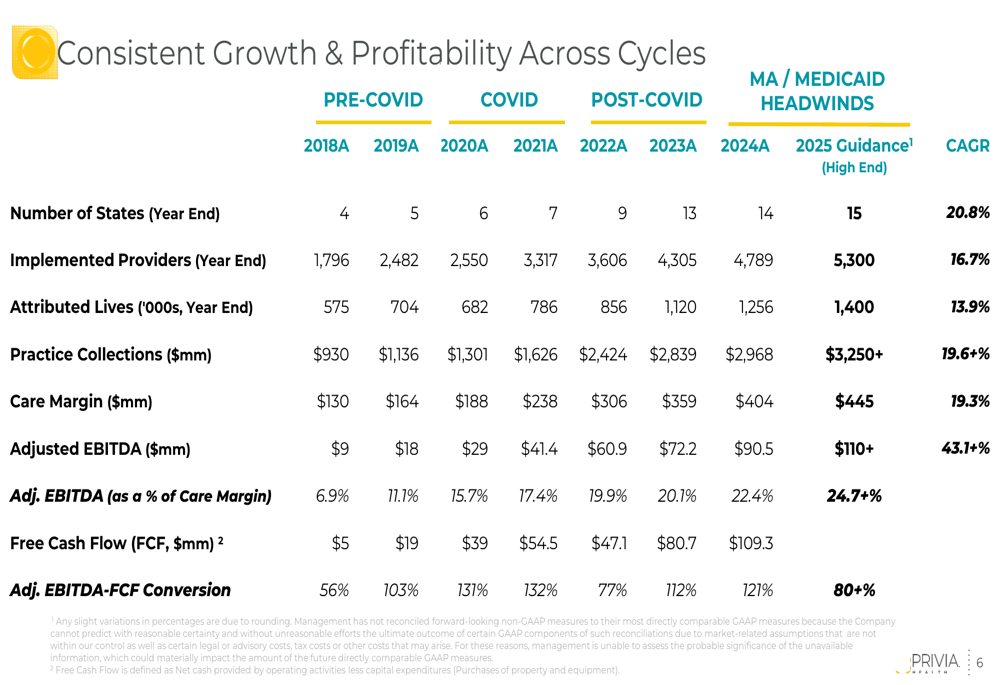

The company’s long-term financial performance shows consistent growth across different economic cycles, with impressive compound annual growth rates (CAGRs) from 2018 to projected 2025 figures:

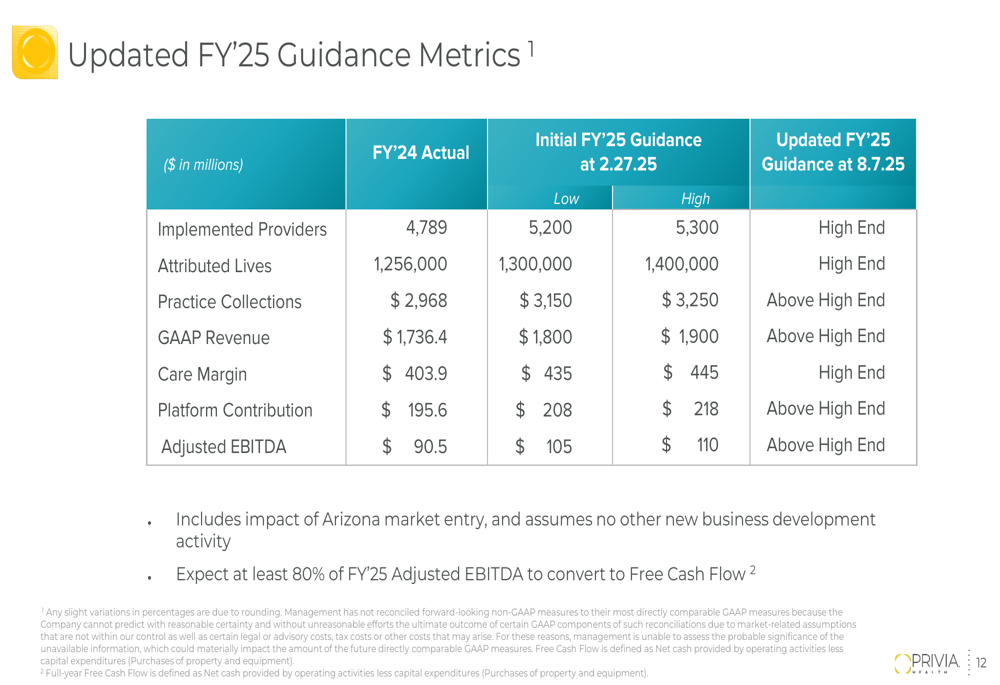

Updated Guidance

Based on the strong first-half performance, Privia Health raised its full-year 2025 guidance above the high end of its previous range for several key metrics, including practice collections, GAAP revenue, platform contribution, and Adjusted EBITDA.

The updated guidance table below shows the company’s increased confidence in its 2025 outlook:

The company expects at least 80% of FY 2025 Adjusted EBITDA to convert to free cash flow, highlighting the capital efficiency of its business model. The guidance includes the impact of the Arizona market entry but assumes no other new business development activity for the remainder of the year.

Strategic Positioning

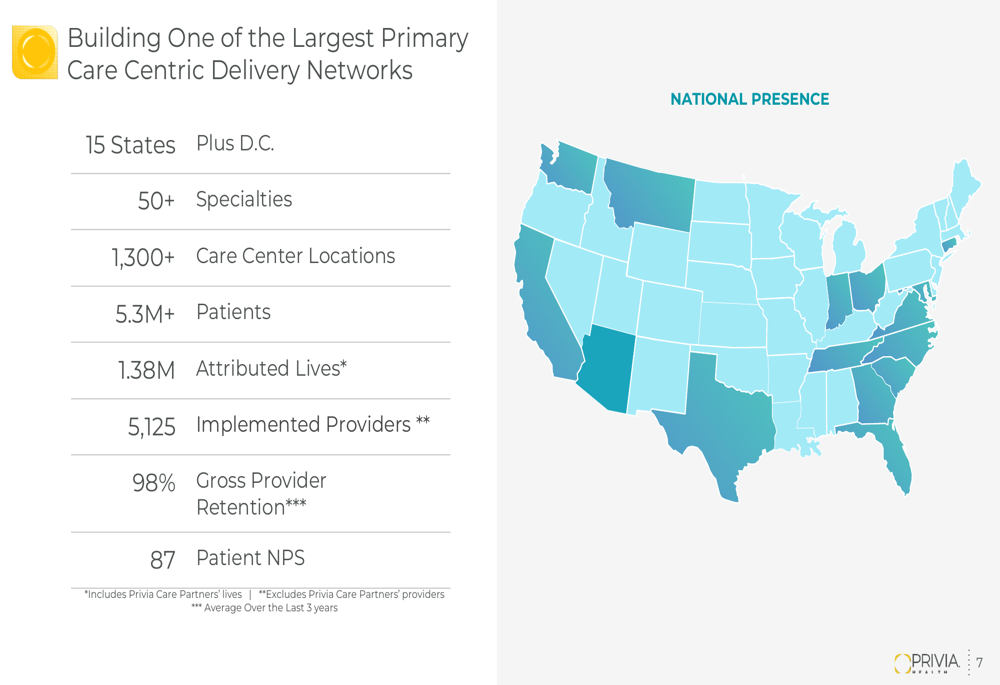

Privia Health continues to build one of the largest primary care-centric delivery networks in the United States, now operating in 15 states plus Washington D.C. The company offers 50+ specialties across 1,300+ care center locations, serving 5.3+ million patients with a strong 87 Net Promoter Score and 98% gross provider retention.

The company’s geographic footprint and scale are illustrated in this map:

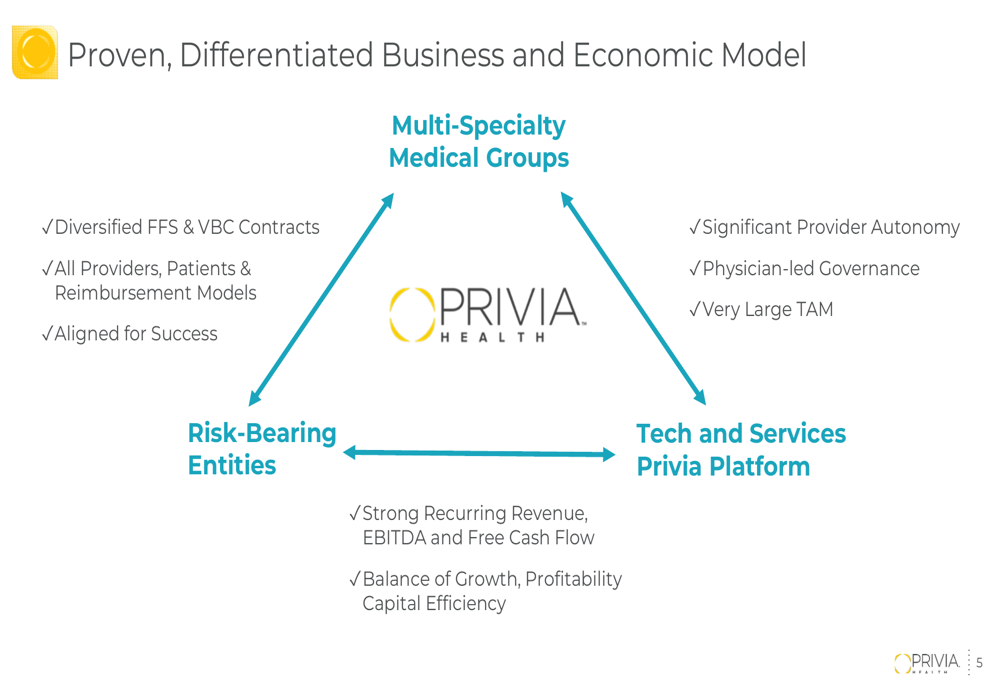

Privia’s business model is built on three interconnected pillars: multi-specialty medical groups, a proprietary technology and services platform, and risk-bearing entities. This model allows the company to balance fee-for-service revenue with value-based care arrangements.

The company’s differentiated business model is visualized in this triangle diagram:

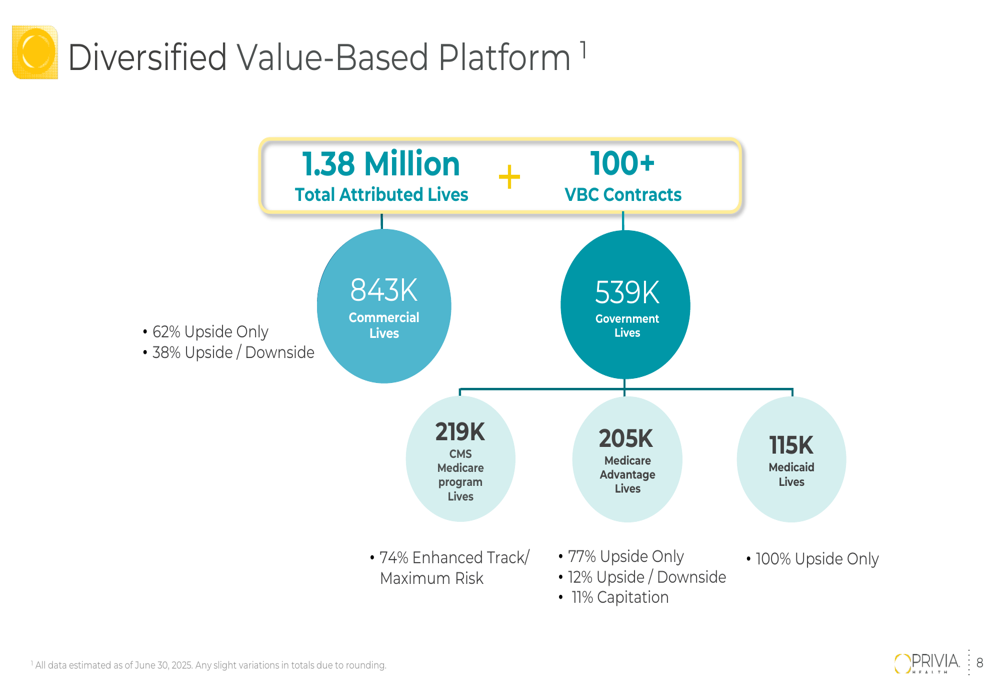

Privia has developed a diversified value-based platform with 1.38 million attributed lives across more than 100 value-based care contracts. The portfolio includes a mix of commercial lives (843,000) and government lives (539,000), with varying levels of risk arrangements from upside-only to full capitation.

Forward-Looking Statements

Despite the strong operational results and raised guidance, investors appear concerned about something not immediately evident in the presentation slides. The significant pre-market drop of 16.53% suggests that either comments made during the earnings call or other factors may have raised concerns about future growth or profitability.

In the previous quarter’s earnings call, CEO Parth Mehrotra had expressed confidence in the company’s strategy, stating, "We are one of the survivors in this industry" and "Our performance speaks for itself." He had also highlighted the company’s cautious approach to full-risk contracts, particularly in Medicare Advantage, which remains a challenging environment.

The disconnect between strong operational performance and negative stock reaction may relate to concerns about the sustainability of growth, competitive pressures, or potential regulatory changes affecting value-based care arrangements. Investors may also be reacting to valuation concerns, as the company was trading at a high earnings multiple prior to this report.

As Privia Health continues to execute its growth strategy, the company’s ability to maintain its strong operational performance while navigating the complex healthcare landscape will be critical to regaining investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.