AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Prologis Inc (NYSE:PLD), the global leader in logistics real estate, released its second quarter 2025 supplemental information on July 16, showing continued revenue growth despite pressure on earnings. The company’s stock responded positively in pre-market trading, rising by 3.03% to $111.91, suggesting investors focused more on long-term growth prospects than the earnings miss.

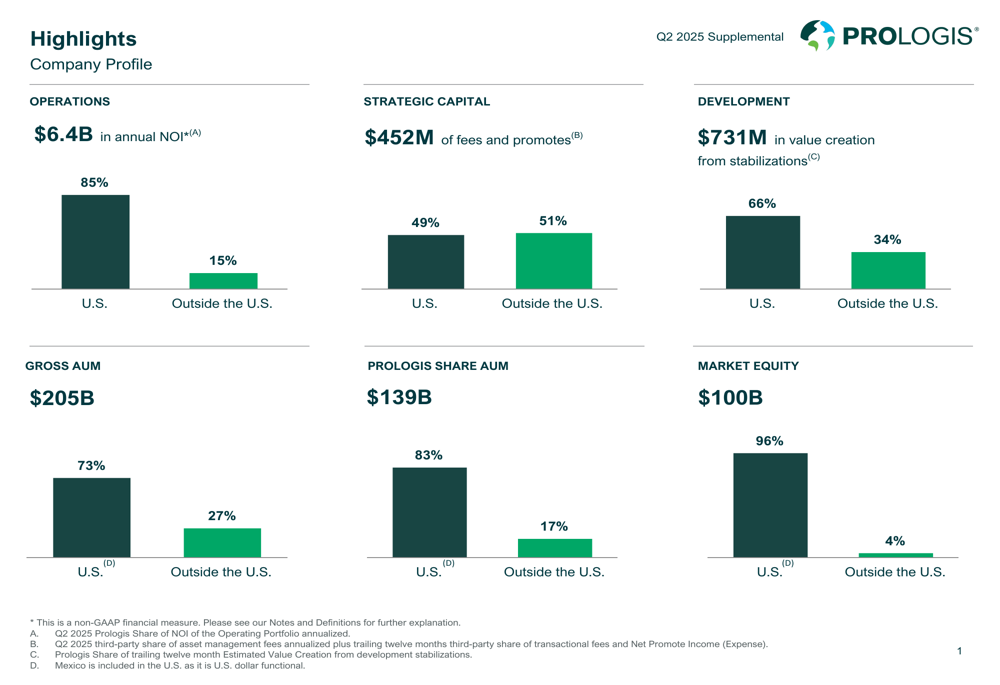

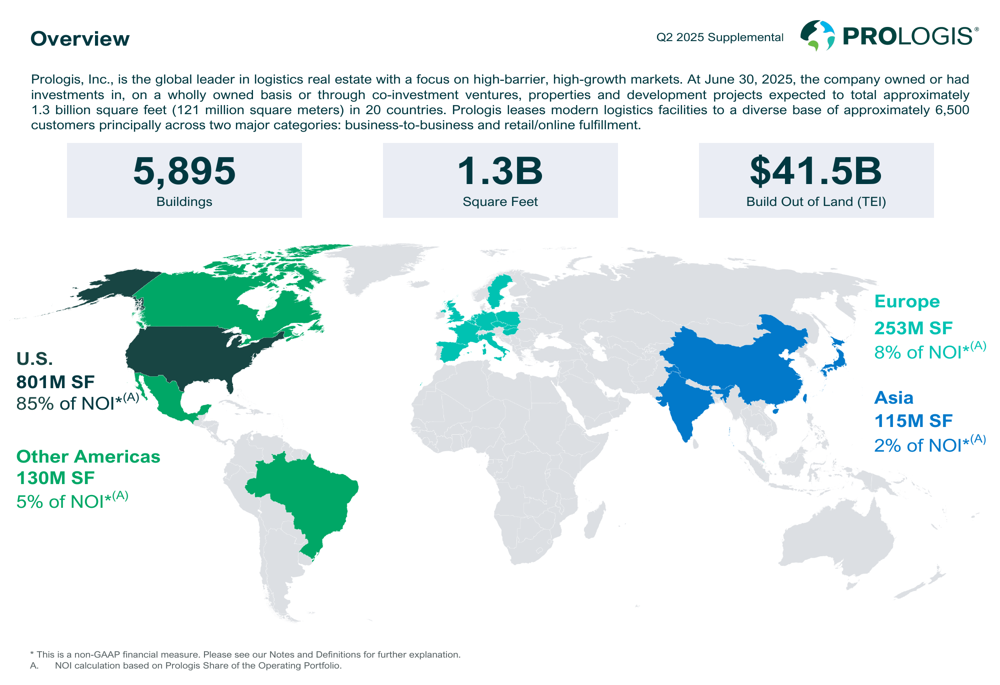

With approximately 1.3 billion square feet across 20 countries, Prologis maintains its dominant position in the logistics real estate sector, leveraging its extensive portfolio of 5,895 buildings and substantial land bank valued at $41.5 billion for future development.

Quarterly Performance Highlights

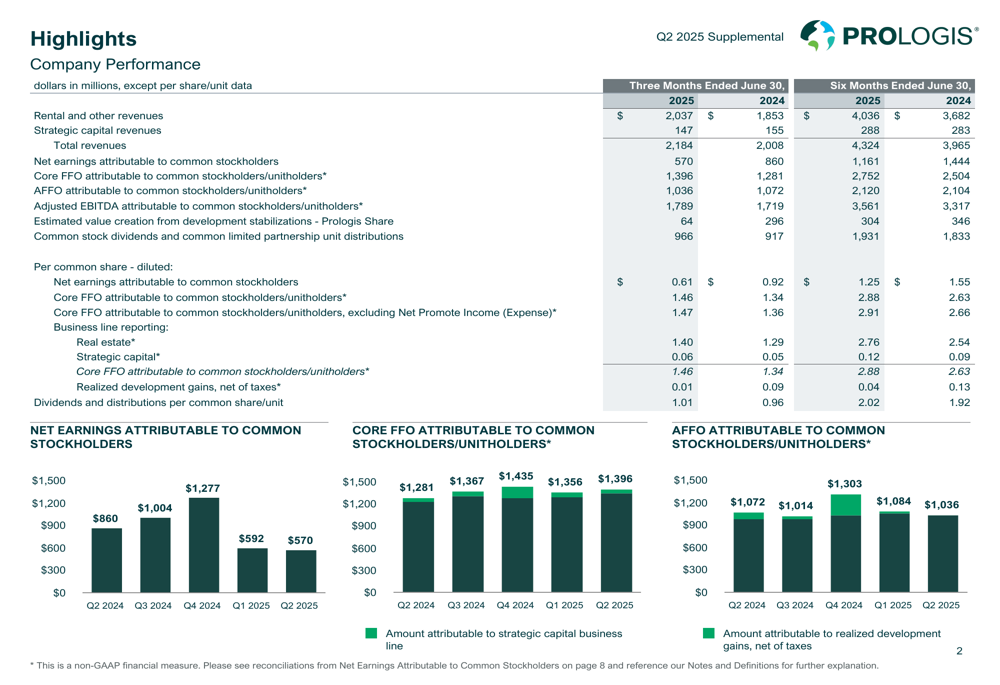

Prologis reported Q2 2025 rental and other revenues of $2.037 billion, up from $1.853 billion in the same period last year, exceeding analyst expectations of $2.01 billion. However, net earnings attributable to common stockholders declined to $570 million ($0.61 per share) from $860 million ($0.92 per share) in Q2 2024, missing the forecasted $0.69 per share.

Core funds from operations (FFO), a key metric for REITs, showed stronger performance, increasing to $1.396 billion ($1.46 per share) from $1.281 billion ($1.34 per share) in Q2 2024.

As shown in the following chart of quarterly financial performance:

The company’s occupancy rate ended the quarter at 95.1%, slightly down 10 basis points from the previous quarter but still within the company’s target range. This reflects Prologis’ ability to maintain high occupancy levels despite market challenges.

Detailed Financial Analysis

Prologis generates an annual net operating income (NOI) of $6.4 billion, with 85% coming from U.S. operations and 15% from international markets. The company’s strategic capital business contributes significantly to revenue, with fees and promotes totaling $452 million, almost evenly split between U.S. (49%) and international operations (51%).

The following breakdown illustrates the company’s diverse revenue streams and geographic distribution:

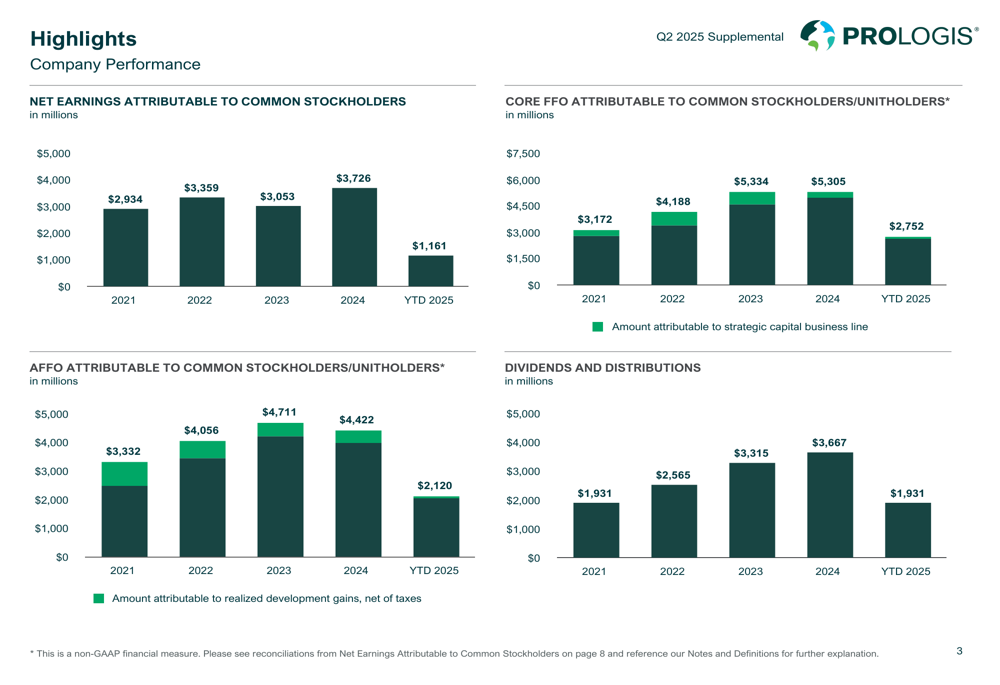

Looking at longer-term trends, Prologis has demonstrated consistent growth in core FFO, which increased from $3,172 million in 2021 to $5,305 million in 2024, with year-to-date 2025 figures reaching $2,752 million. This growth trajectory has continued despite more volatile performance in net earnings.

CEO Hamid Mogadam emphasized future growth opportunities during the earnings call, stating, "Every bit of business that’s delayed is going to translate to more business in the future," highlighting the company’s confidence in its long-term strategy despite short-term challenges.

Strategic Initiatives & Global Positioning

Prologis maintains a strong global presence with properties across 20 countries, though the U.S. market remains dominant, representing 85% of NOI. The company’s total assets under management (AUM) reached $205 billion, with 73% in the U.S. and 27% internationally.

The company’s global footprint is illustrated in this regional breakdown:

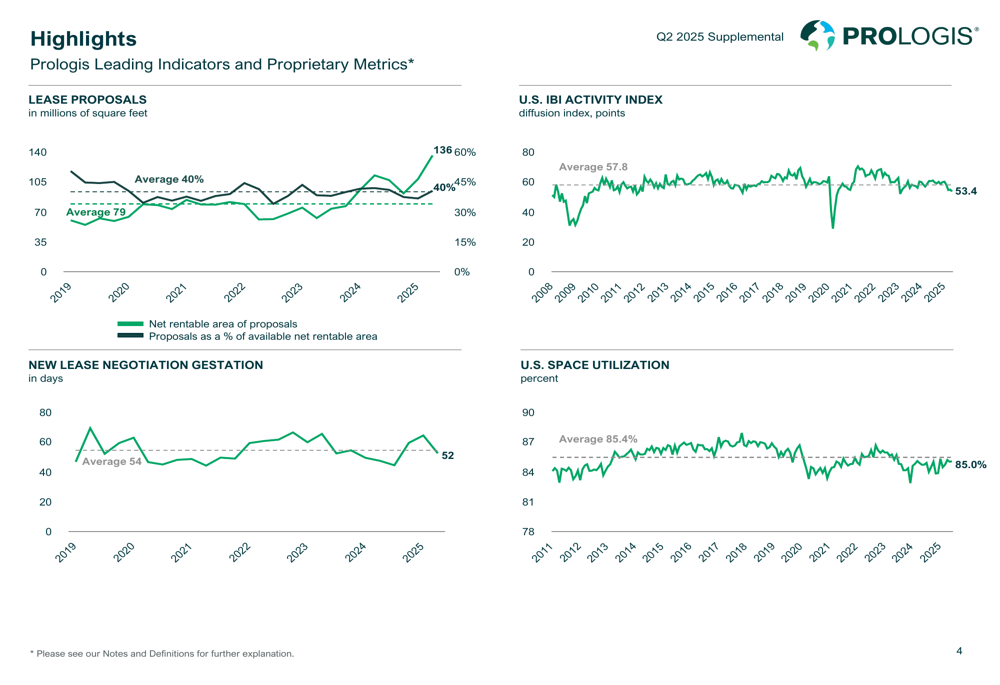

Prologis leverages proprietary metrics to gain market insights and guide strategy. The U.S. IBI Activity Index, which measures customer activity levels, registered 53.4 in 2025, above the neutral level of 50 but below the historical average of 57.8. Meanwhile, U.S. space utilization stands at 85.0%, slightly below the historical average of 85.4%, indicating stable but not exceptional warehouse usage.

These leading indicators provide valuable context for understanding market dynamics:

During the earnings call, management highlighted significant investment in data center development, particularly in Austin, Texas, reflecting the company’s strategic diversification beyond traditional logistics facilities. CFO Tim Arendt emphasized that "well located logistics real estate has proved to be a strategic asset," underscoring the company’s focus on prime locations.

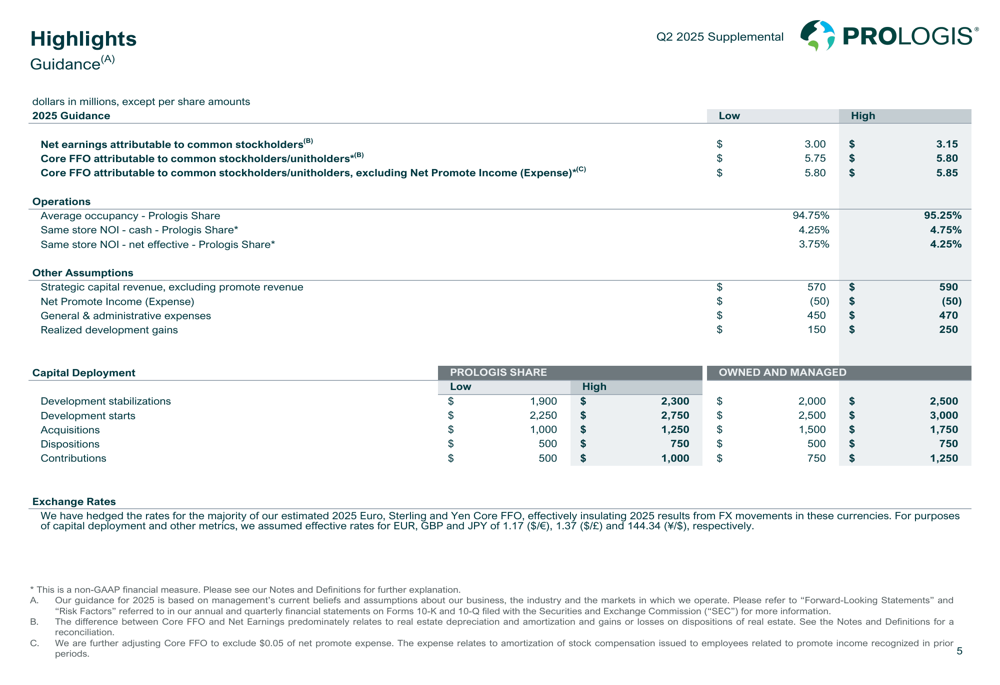

Forward-Looking Statements & Guidance

Prologis maintained its core FFO guidance for 2025 at $5.75 to $5.80 per share, while projecting net earnings per share between $3.00 and $3.15. The company expects average occupancy rates to remain strong at 94.75% to 95.25%, with same-store NOI growth of 4.25% to 4.75% on a cash basis.

The detailed 2025 guidance provides insight into Prologis’ expectations across multiple metrics:

The company increased its development starts guidance to $2.25-$2.75 billion, reflecting confidence in growth opportunities despite market uncertainties. Acquisition targets range from $1.0 to $1.75 billion, while dispositions are expected to be between $500 million and $750 million, indicating selective portfolio optimization.

Potential challenges include tariff uncertainties affecting leasing decisions, market saturation in key regions, and fluctuating market rents, which declined 1.4% in the quarter. Additionally, increased power demand from warehouse automation may strain resources, while broader economic pressures could impact customer spending and lease renewals.

Despite these challenges, Prologis’ strong market position, diverse revenue streams, and strategic focus on prime logistics locations position the company to navigate market uncertainties while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.