US stock futures flounder amid tech weakness, Fed caution

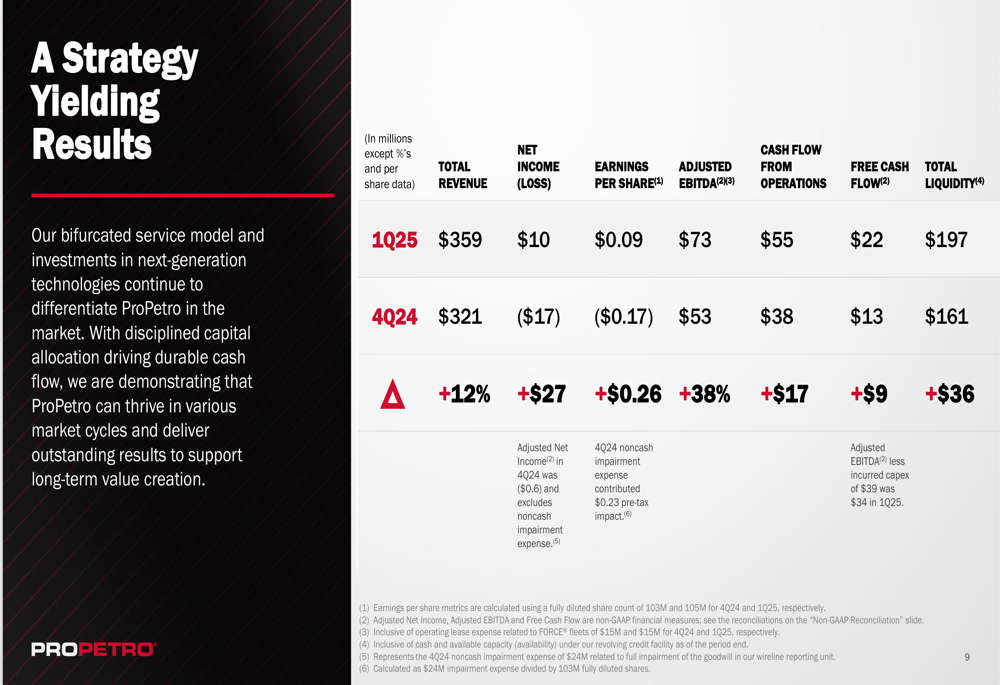

ProPetro Holding Corp (NYSE:PUMP) delivered a strong financial rebound in the first quarter of 2025, with significant improvements across key metrics compared to the previous quarter. The Permian Basin-focused energy services provider presented its latest investor slides on April 29, 2025, highlighting substantial quarter-over-quarter growth and progress on strategic initiatives.

Quarterly Performance Highlights

ProPetro reported Q1 2025 revenue of $359 million, representing a 12% increase from Q4 2024. More impressively, the company swung to profitability with net income of $10 million, compared to a $17 million loss in the previous quarter. Adjusted EBITDA surged 38% to $73 million, while free cash flow increased to $22 million from $13 million in Q4.

As shown in the following financial performance comparison chart, the company demonstrated improvement across all key metrics:

This financial recovery follows a challenging Q4 2024, when the company missed analyst expectations with a negative EPS of $0.17. The Q1 results indicate that ProPetro’s strategic initiatives may be gaining traction, particularly its focus on fleet transformation and operational efficiency.

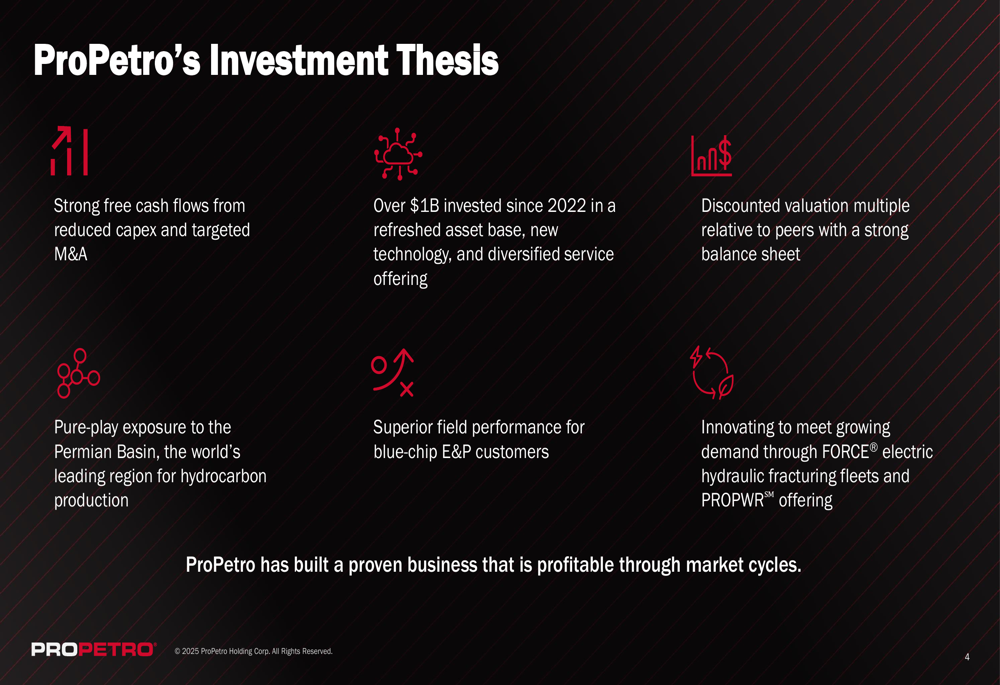

Strategic Initiatives

ProPetro’s investment thesis centers on generating strong free cash flows through reduced capital expenditure and targeted acquisitions, while maintaining a strong balance sheet and leveraging its pure-play exposure to the Permian Basin.

The following slide outlines the key elements of ProPetro’s investment approach:

The company has invested over $1 billion since 2022 in refreshing its asset base, adopting new technologies, and diversifying its service offerings. This investment strategy has included strategic acquisitions such as SILVERTIP (wireline services) in 2022, PAR FIVE (cementing) in 2023, and AQUA PROP (wet sand solutions) in 2024.

ProPetro’s revenue mix currently consists of hydraulic fracturing (75%), wireline (15%), and cementing (10%), reflecting its focus on premium completions services for the Permian Basin.

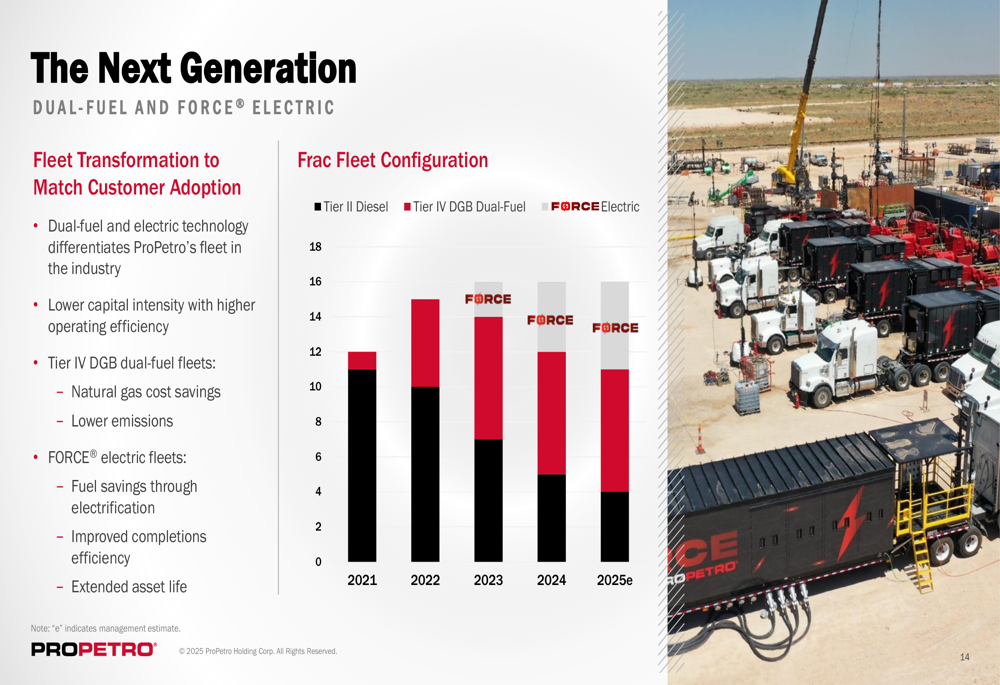

A central element of ProPetro’s strategy is its fleet transformation initiative, which focuses on transitioning to more efficient and environmentally friendly technologies. The company is increasingly deploying dual-fuel and electric-powered equipment to reduce emissions and operating costs.

The following slide illustrates ProPetro’s fleet transformation progress:

The company reported that its Tier IV DGB dual-fuel fleets are achieving natural gas substitution rates exceeding 60% on average, with the rate improving from 40% in 2022 to 67% in 2024. This transition helps reduce both costs and emissions for customers.

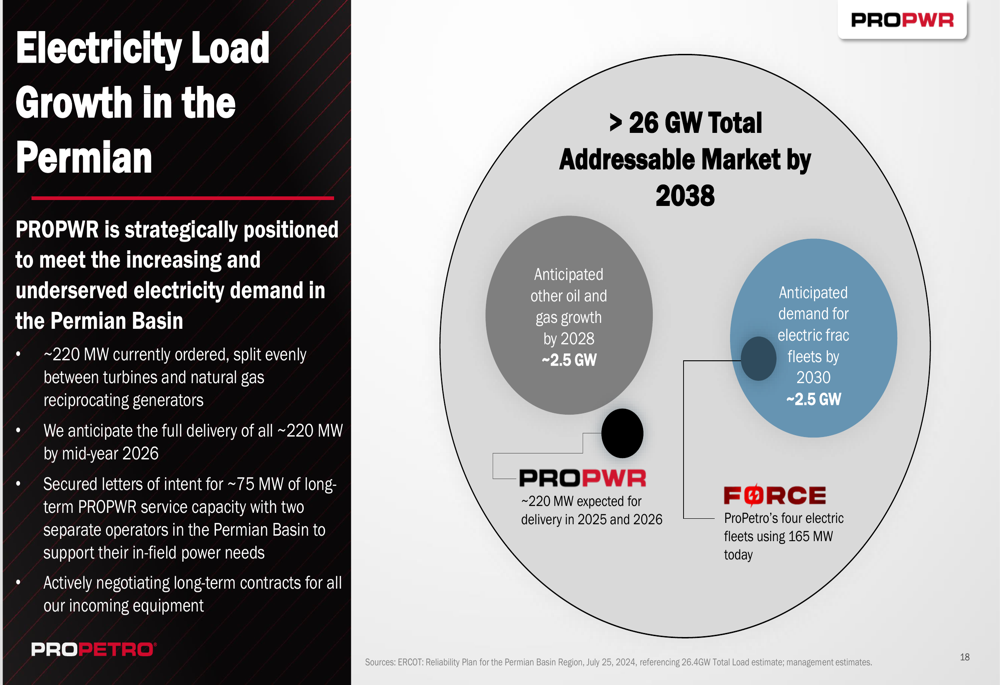

PROPWR Initiative and Growth Opportunities

A significant focus of ProPetro’s presentation was its PROPWR initiative, which aims to capitalize on growing power demand in the Permian Basin and beyond. The company has ordered approximately 220 megawatts of power generation capacity, split evenly between turbines and natural gas reciprocating generators, with full delivery expected by mid-2026.

ProPetro has secured letters of intent for approximately 75 megawatts of long-term PROPWR service capacity with two separate operators in the Permian Basin. The company sees substantial growth potential in this area, citing anticipated load growth of over 4 gigawatts in the Permian and over 35 gigawatts for U.S. data centers.

The following chart illustrates the electricity load growth opportunity in the Permian Basin:

CEO Sam Sledge emphasized in the previous quarter’s earnings call that "the demand for reliable low emissions power solutions is vast and increasing," positioning PROPWR to capitalize on multiple high-growth verticals.

Competitive Industry Position

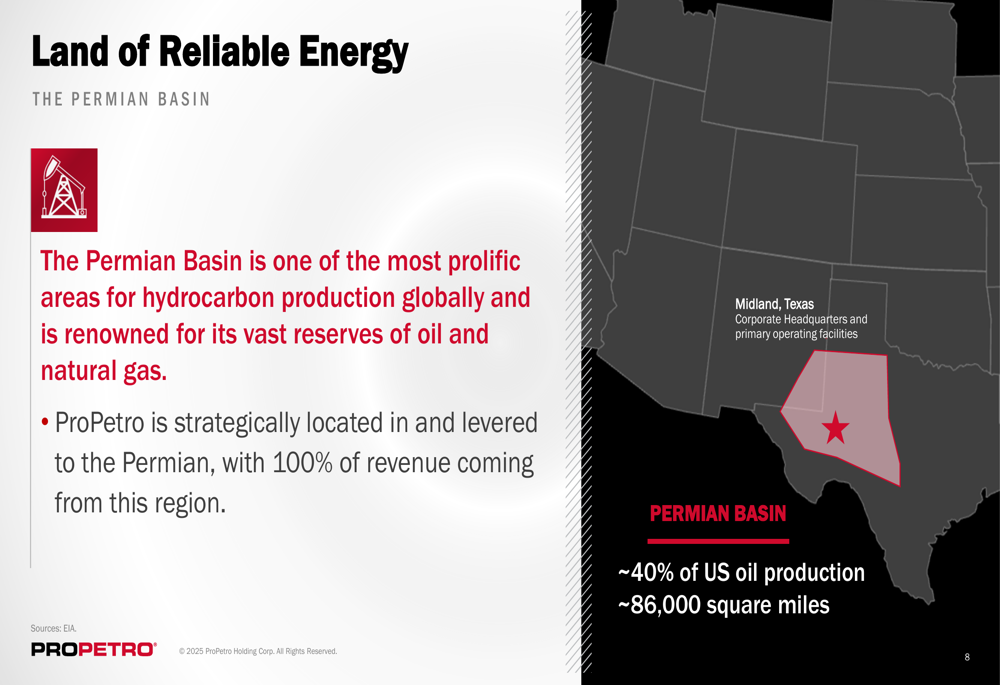

ProPetro maintains a strategic focus on the Permian Basin, which accounts for approximately 40% of U.S. oil production. This concentrated geographic approach allows the company to leverage its local expertise and infrastructure.

The following map highlights ProPetro’s strategic positioning in the Permian Basin:

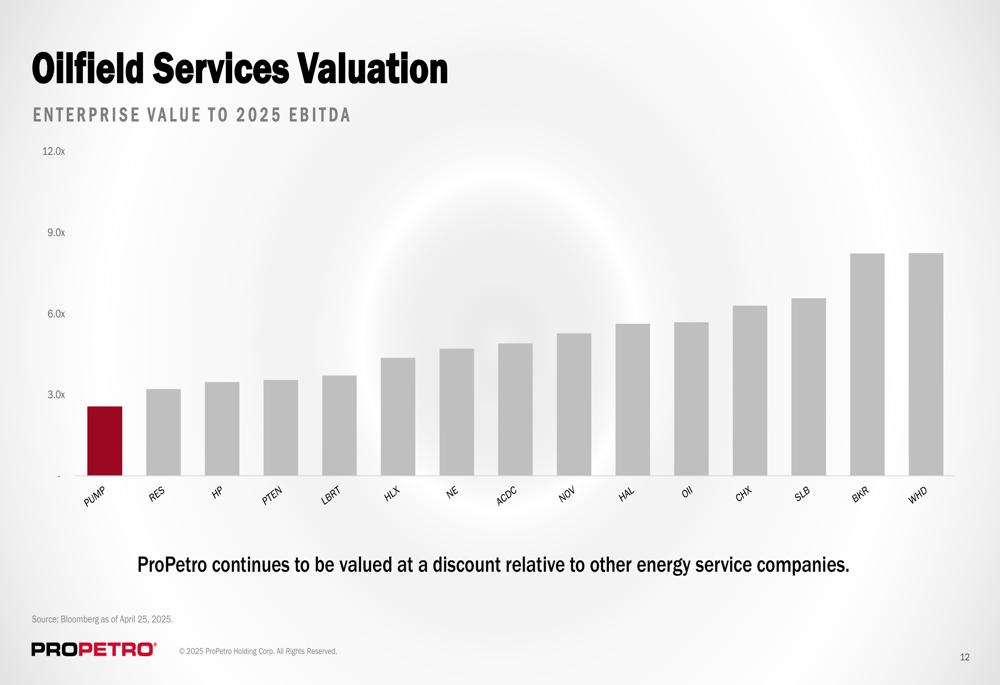

A key point emphasized in the presentation is ProPetro’s valuation relative to peers. The company currently trades at an enterprise value to 2025 EBITDA multiple of 3.0x, which it argues is significantly discounted compared to other oilfield services companies trading between 5.0x and 8.0x.

This valuation comparison is illustrated in the following chart:

Capital Allocation and Shareholder Returns

ProPetro highlighted its $200 million share repurchase program, of which $111 million has been utilized to date, with $89 million remaining. The company has retired approximately 13 million shares, representing 11% of outstanding shares, since the program’s inception through March 31, 2025.

The board increased the repurchase authorization by $100 million on April 24, 2024, and extended the program to May 2025. Management indicated they intend to further extend the program before it expires next month, subject to board approval.

Forward Outlook

While ProPetro did not provide specific guidance for the remainder of 2025, the company’s presentation emphasized its focus on generating durable earnings and free cash flow through its industrialized business model. The company’s strong liquidity position of $197 million as of Q1 2025 provides flexibility to pursue its strategic initiatives.

The transition to more efficient fleet configurations and expansion into power generation services represent key growth vectors for ProPetro as it seeks to capitalize on energy transition opportunities while maintaining its core competencies in oilfield services.

With its pure-play exposure to the Permian Basin, focus on blue-chip customers, and ongoing fleet modernization efforts, ProPetro appears positioned to benefit from continued demand for energy services in the region, though execution of its strategic initiatives will be crucial to sustaining the positive momentum demonstrated in Q1 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.