AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

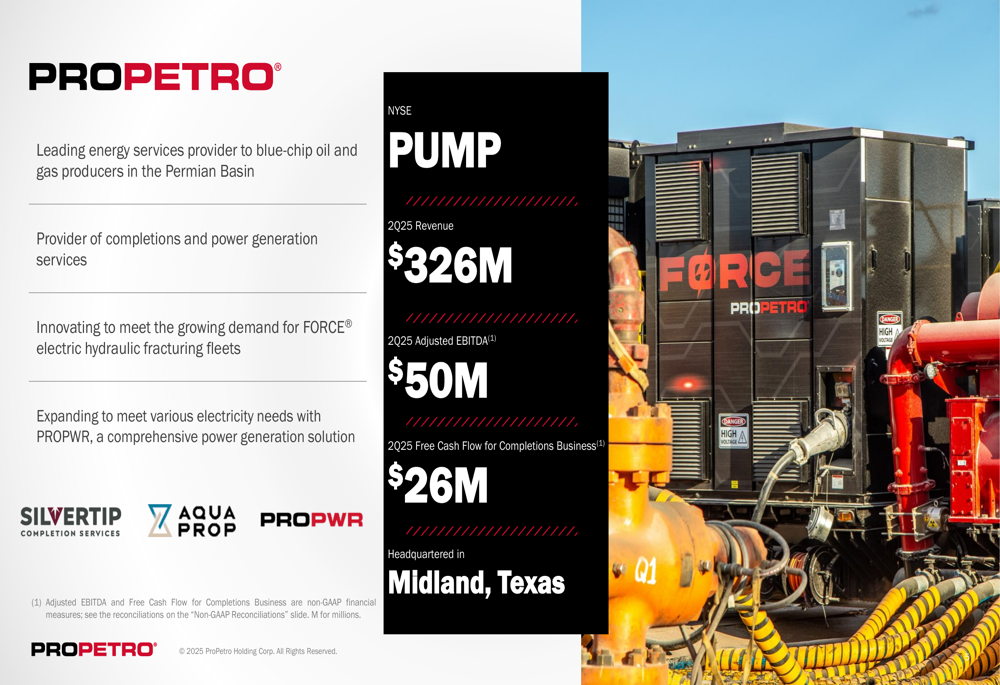

ProPetro Holding Corp (NYSE:PUMP) released its Q2 2025 investor presentation on July 30, 2025, revealing a challenging quarter with declining financial metrics as the company continues its strategic transformation toward electrification and power generation services. The Permian Basin-focused energy services provider reported a 9% sequential revenue decline and swung to a net loss, even as it emphasized its long-term strategy of becoming a premier power services provider in the region.

The presentation comes amid significant premarket pressure on the stock, which was down 13.72% to $5.47 in early trading following the results, erasing the 2.76% gain from the previous session.

As shown in the following snapshot of the company’s core business and recent performance:

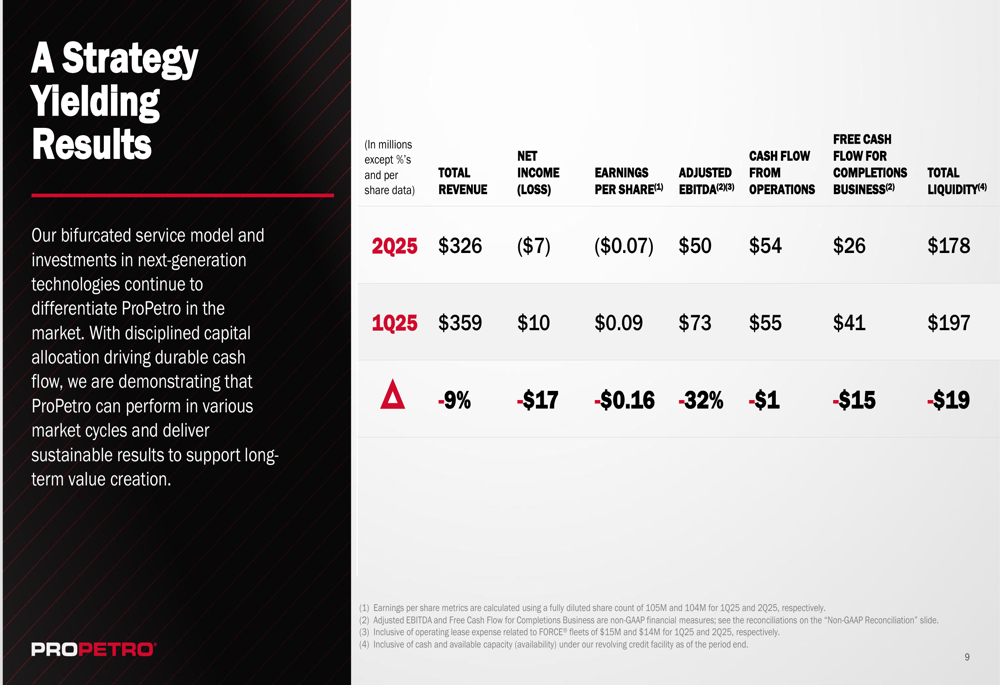

Quarterly Performance Highlights

ProPetro reported Q2 2025 revenue of $326 million, down 9% from $359 million in Q1 2025. More concerning for investors, the company swung to a net loss of $7 million (EPS of -$0.07) compared to a net income of $10 million (EPS of $0.09) in the previous quarter. Adjusted EBITDA declined significantly by 32% to $50 million from $73 million in Q1.

Despite these challenges, the company maintained relatively stable cash flow from operations at $54 million, just slightly below the $55 million reported in Q1. Free cash flow for the completions business fell to $26 million from $41 million in the previous quarter.

The following chart clearly illustrates the quarter-over-quarter decline across key financial metrics:

ProPetro’s revenue mix continues to be dominated by hydraulic fracturing, which accounted for 75% of Q2 2025 revenue, followed by wireline services at 15% and cementing at 10%. The company remains exclusively focused on the Permian Basin, which accounts for approximately 40% of U.S. oil production.

Strategic Initiatives

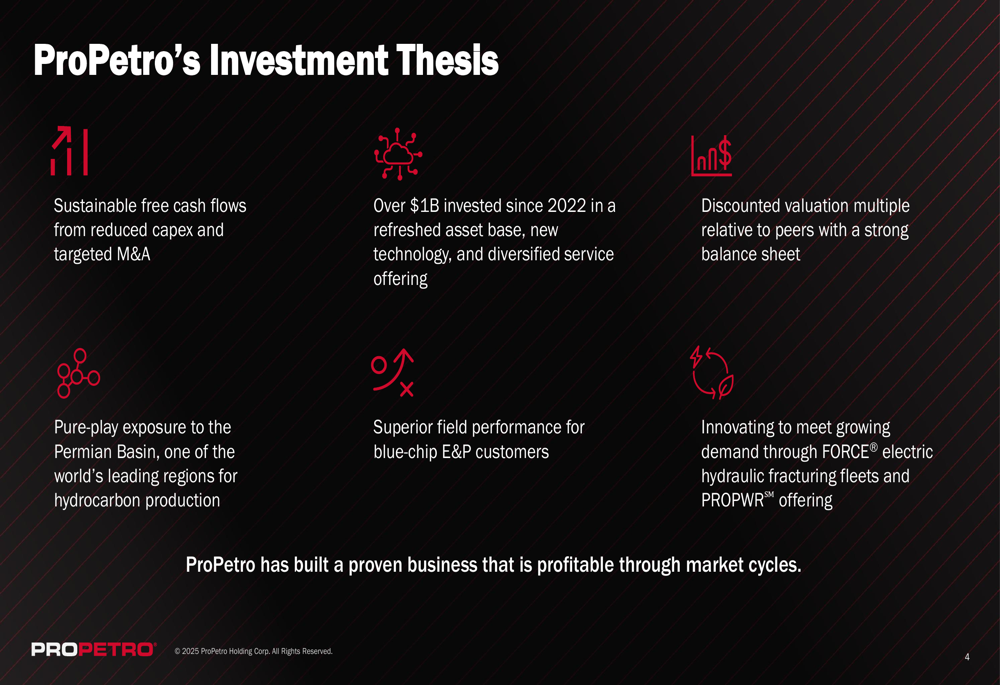

ProPetro’s investor presentation emphasized its ongoing strategic transformation, particularly its investment in the PROPWR business and fleet electrification. The company has positioned these initiatives as key to addressing growing power demand in the Permian Basin and differentiating itself from competitors.

The company’s investment thesis highlights sustainable free cash flows, over $1 billion invested since 2022 in refreshed assets and new technology, and its pure-play exposure to the Permian Basin:

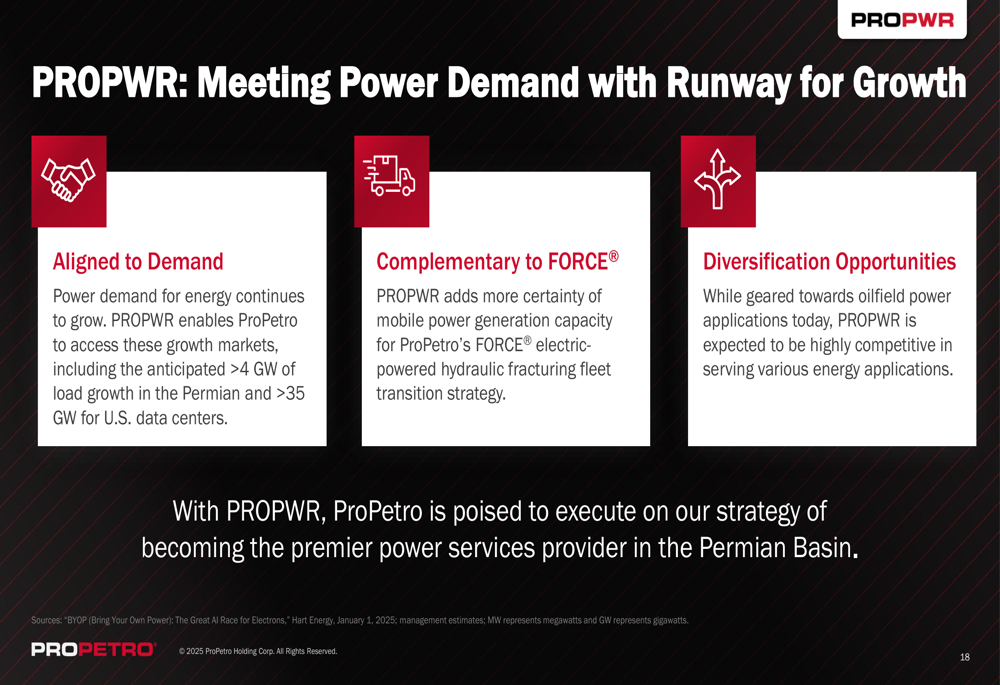

A significant focus of the presentation was the company’s PROPWR business, which aims to capitalize on growing electricity demand in the Permian Basin. ProPetro estimates a total addressable market of over 26 GW by 2038, with anticipated demand for electric frac fleets reaching approximately 2.5 GW by 2030. The company expects to deliver approximately 220 MW of power generation capacity in 2025 and 2026.

ProPetro also highlighted its fleet transformation strategy, with an increasing focus on Tier IV DGB dual-fuel and FORCE® electric fleets. The company now has four FORCE® electric fleets operating under contract, which it claims offer lower emissions, quieter operations, and significant fuel savings through 100% diesel displacement.

The company’s M&A strategy has focused on complementary service offerings, with three acquisitions since 2022: SILVERTIP Completion Services (wireline), PAR FIVE Energy Services (cementing), and AQUA PROP (wet sand solutions).

Competitive Industry Position

ProPetro emphasized its discounted valuation relative to peers in the oilfield services sector, suggesting potential for multiple expansion as the company continues its transformation toward an industrialized model.

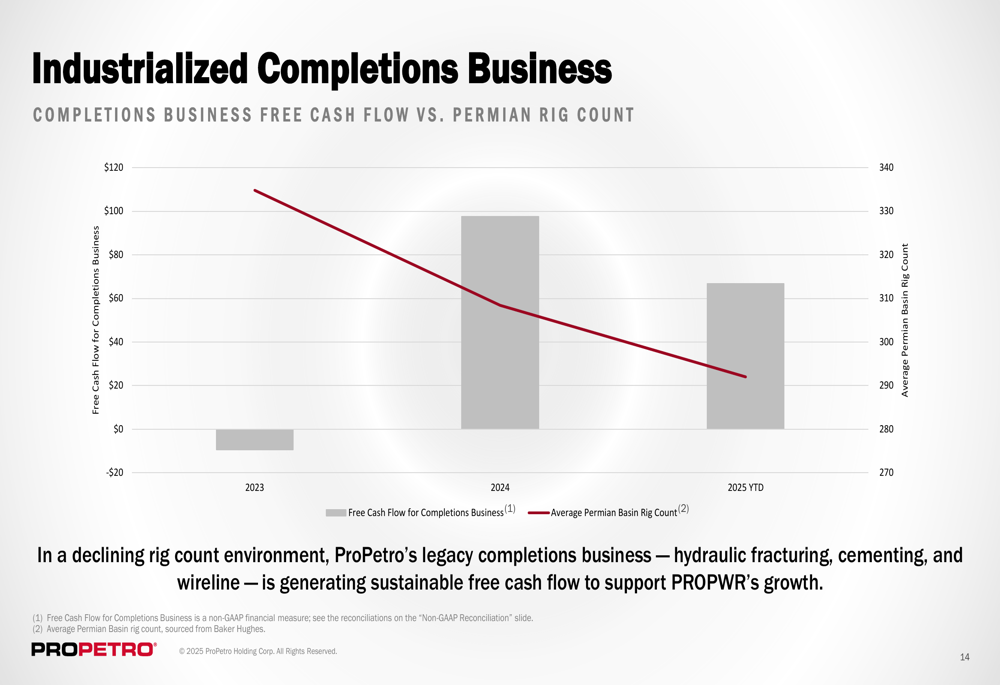

The presentation highlighted that the company’s completions business continues to generate sustainable free cash flow despite a declining rig count environment in the Permian Basin. This cash flow is being used to support the growth of the PROPWR business.

The company also noted its $200 million share repurchase program, which has been extended to December 2026. To date, ProPetro has repurchased $111 million worth of shares, retiring approximately 13 million shares (11% of outstanding) since the program’s inception. However, the company acknowledged it did not repurchase any shares in 2025 as it prioritized the launch and scaling of its PROPWR business.

Forward-Looking Statements

Looking ahead, ProPetro remains focused on its transformation toward an industrialized business model, which it believes deserves a valuation rerating. The company cited improved capital discipline, deployment of industrial technologies, and a greater focus on cash flow generation as reasons for potential multiple expansion in the oilfield services sector.

The company’s presentation emphasized its commitment to meeting growing power demand in the Permian Basin, with its PROPWR business positioned as a key growth driver. ProPetro stated it is "poised to execute on our strategy of becoming the premier power services provider in the Permian Basin."

However, the significant decline in financial performance from Q1 to Q2 2025 raises questions about near-term execution challenges. The premarket stock decline suggests investors may be concerned about the company’s ability to navigate the transition while maintaining financial performance.

The company’s Q2 results represent a notable reversal from its Q1 2025 performance, when it exceeded market expectations with EPS of $0.09 versus a forecast of $0.06. That earnings beat had driven a 5.5% stock price increase at the time, but the momentum appears to have stalled with the latest results.

As ProPetro continues its strategic pivot toward power generation and fleet electrification, investors will be watching closely to see if the company can return to profitability while successfully scaling its new business initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.