TSX jumps amid Fed rate cut hopes, ongoing U.S. government shutdown

Introduction & Market Context

PT BUMA Internasional Grup Tbk (IDX:DOID) presented its nine-month 2024 company update on December 19, highlighting a significant transformation in its business model. The company, formerly known as PT Delta Dunia Makmur Tbk, is strategically diversifying from its traditional thermal coal focus to include metallurgical coal and copper assets, primarily through acquisitions in Australia.

Despite challenging weather conditions affecting operations, DOID has maintained stable revenue while substantially growing its order book, positioning the company for long-term growth. The stock closed at 490, up 2.04% on the day of the presentation, trading within its 52-week range of 328-810.

Executive Summary

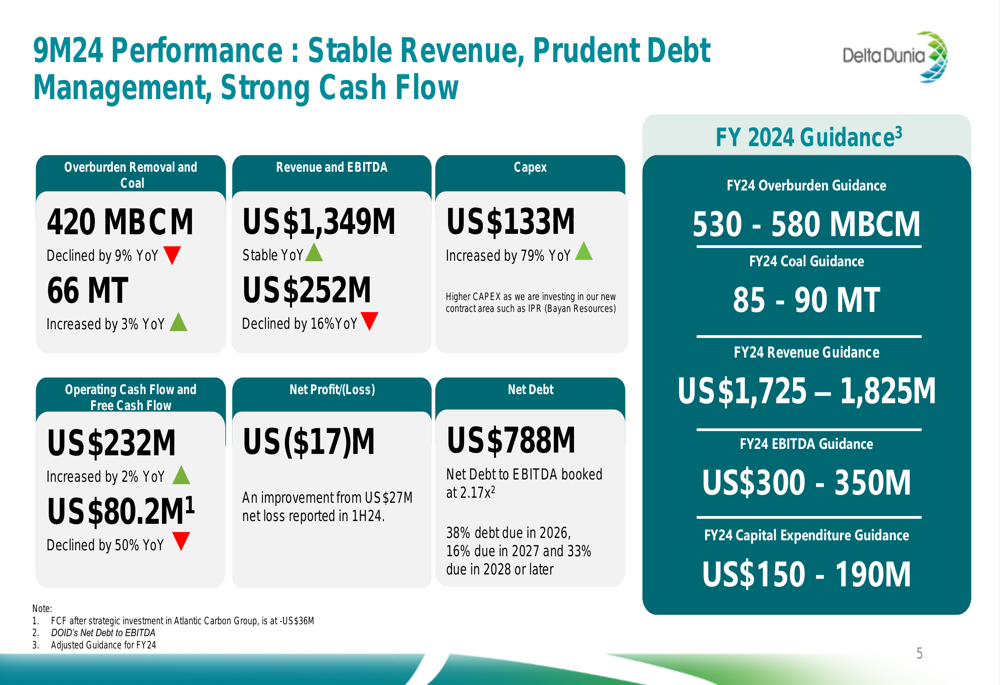

DOID reported stable revenue of US$1.35 billion for the first nine months of 2024, despite a 9% year-over-year decline in overburden removal to 420 MBCM. The company’s EBITDA decreased by 16% to US$252 million, with margins contracting to 21.5%. However, the most significant development was the tripling of the order book to US$12.7 billion, providing substantial revenue visibility for the coming years.

As shown in the following performance summary:

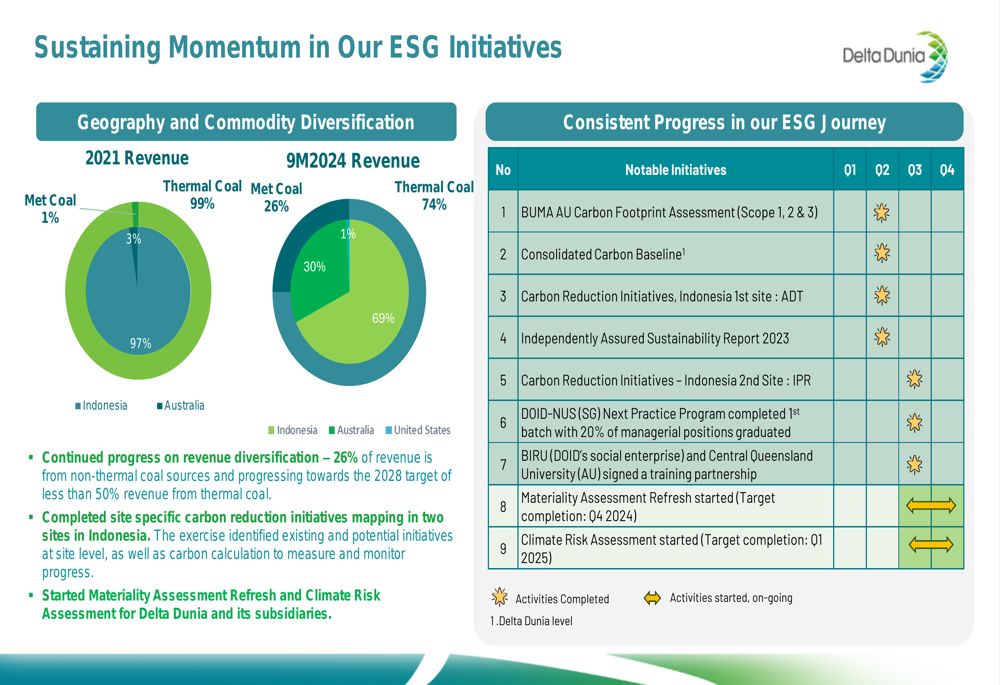

The company’s strategic shift is evident in its commodity mix, with metallurgical coal now representing 26% of revenue, up from just 1% in 2021. This diversification is primarily driven by the acquisition of a 51% stake in the Dawson Mine Complex in Australia and a 19.9% equity investment in copper producer 29Metals Ltd.

Quarterly Performance Highlights

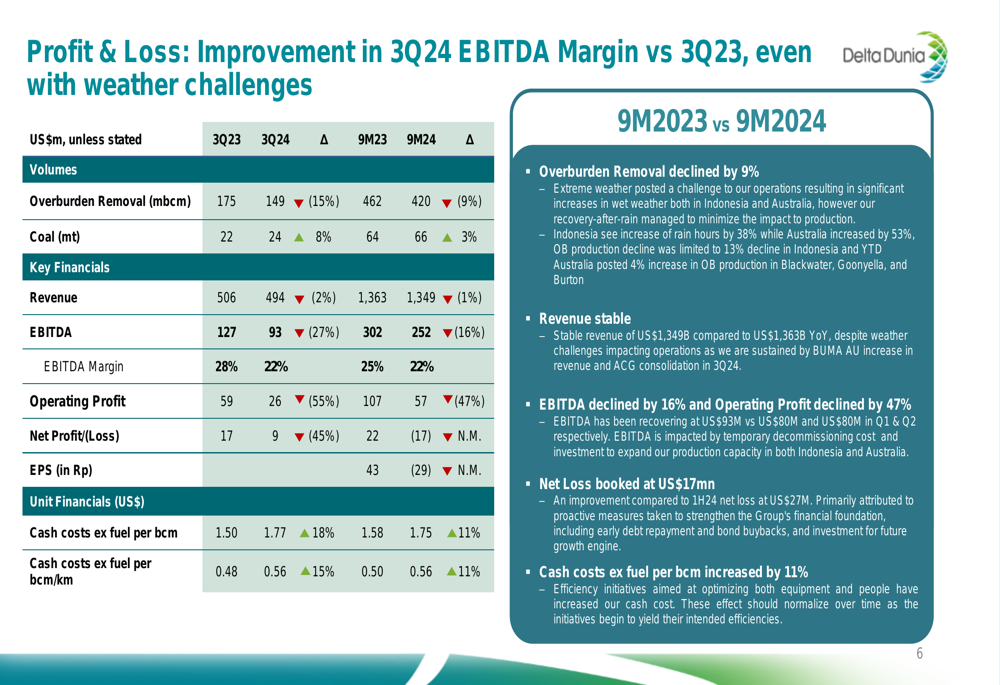

DOID’s third-quarter performance showed signs of improvement compared to the first half of 2024. While the company reported a net loss of US$17 million for the nine-month period, this represented an improvement from the US$27 million loss reported in the first half of the year. The third quarter alone generated a net profit of US$9 million, though this was down 45% from the same period last year.

Coal production increased by 3% year-over-year to 66 million tonnes, partially offsetting the decline in overburden removal. Operating cash flow remained positive at US$232 million, a slight increase of 2% compared to the same period last year.

The detailed profit and loss comparison reveals the impact of weather challenges on operations:

Cash costs excluding fuel increased by 11% to US$1.75 per bcm, reflecting inflationary pressures and operational challenges. Despite these headwinds, the company maintained stable revenue, demonstrating resilience in its core operations.

Strategic Initiatives and Diversification

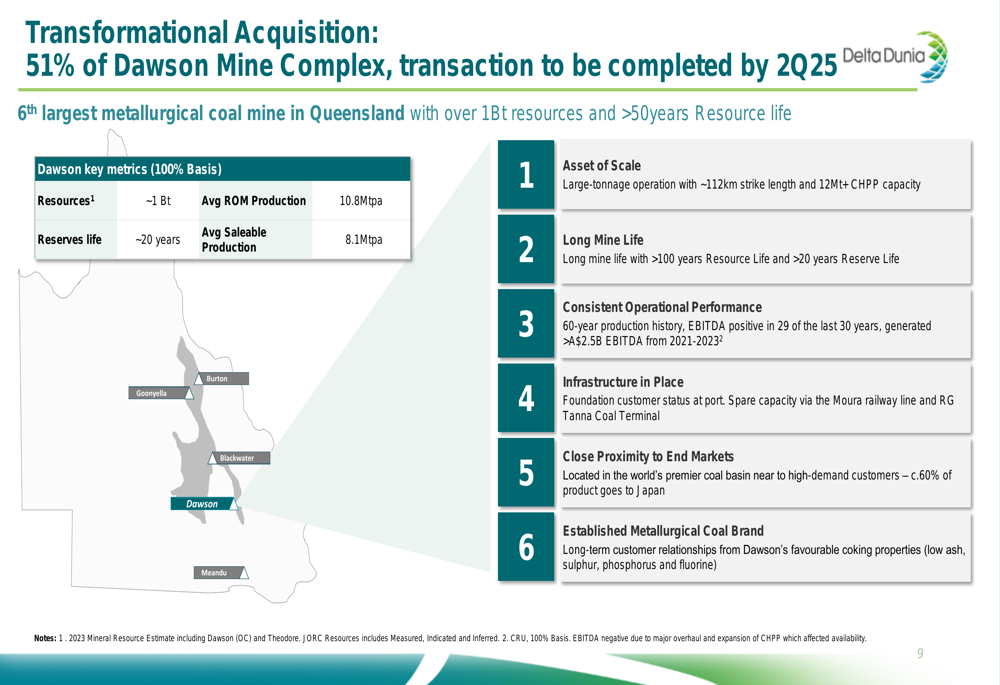

DOID’s most significant strategic moves involve its expansion into metallurgical coal and copper through Australian acquisitions. The company acquired a 51% controlling interest in the Dawson Mine Complex, the sixth largest metallurgical coal mine in Queensland, with resources of approximately 1 billion tonnes and a reserve life of over 20 years.

The following details highlight the strategic importance of the Dawson acquisition:

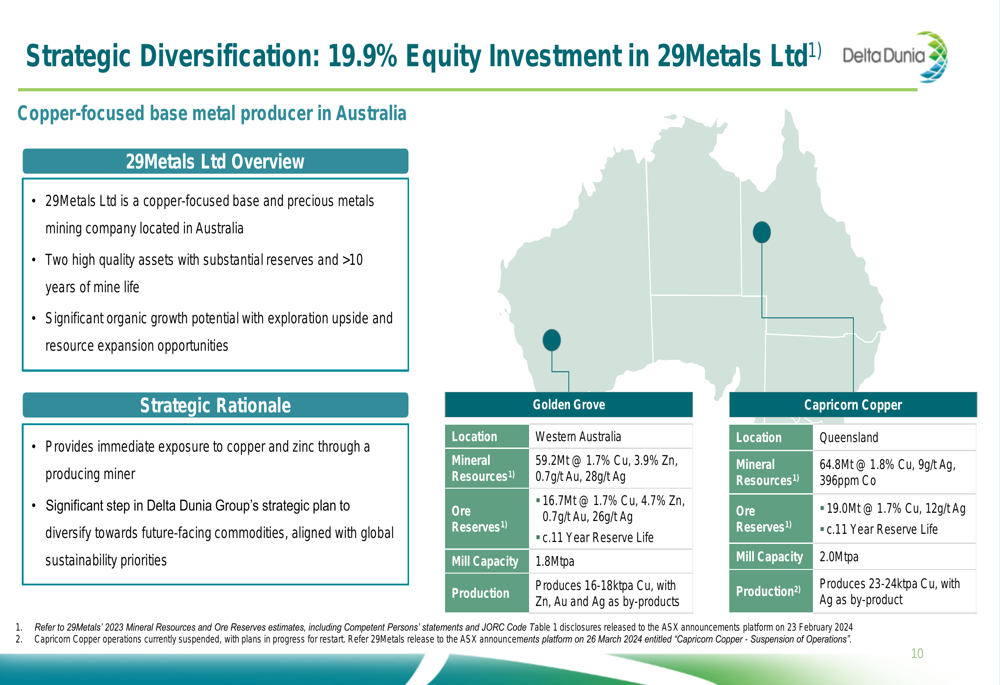

Complementing this acquisition, DOID increased its minority interest to 19.9% in 29Metals Ltd, a copper-focused base metal producer in Australia. This investment provides immediate exposure to copper and zinc, aligning with the company’s strategic plan to diversify toward future-facing commodities.

As illustrated in the following overview of the 29Metals investment:

These strategic initiatives have dramatically shifted DOID’s revenue composition. In 2021, thermal coal accounted for 99% of revenue, but by 9M 2024, this had decreased to 74%, with metallurgical coal now representing 26%. This diversification reduces the company’s exposure to thermal coal markets and positions it to benefit from the growing demand for metallurgical coal and copper.

Balance Sheet and Debt Management

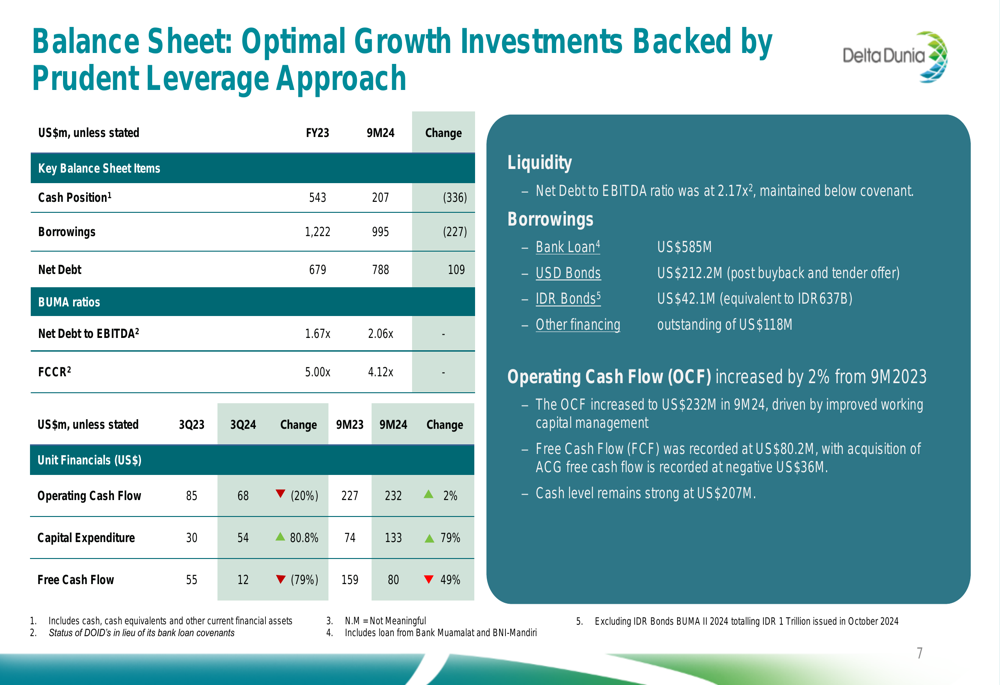

DOID’s balance sheet reflects its strategic investments, with cash position decreasing to US$207 million from US$543 million at the end of 2023. Net debt increased to US$788 million, resulting in a Net Debt/EBITDA ratio of 2.17x, up from 1.67x at the end of 2023.

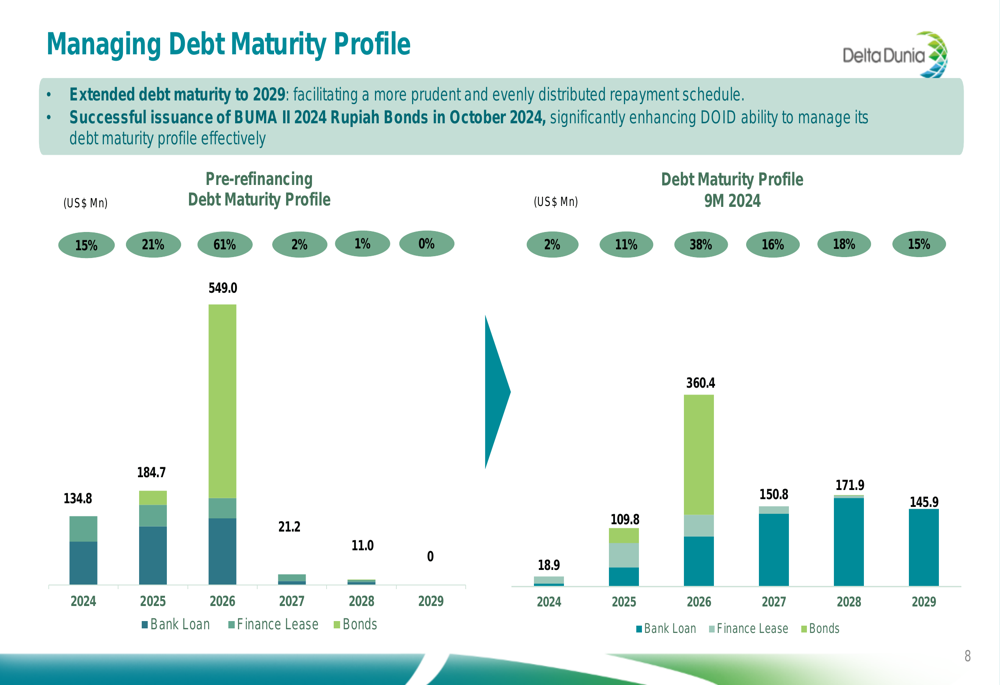

The company has prudently managed its debt profile, extending maturities to 2029 and creating a more evenly distributed repayment schedule:

Capital expenditure increased significantly by 79% year-over-year to US$133.1 million, reflecting the company’s investments in growth initiatives. Free cash flow declined by 50% to US$80.2 million, primarily due to the increased capital expenditure.

Despite the higher leverage, DOID maintains that its debt levels remain manageable, with a fixed charge coverage ratio of 4.12x. The company’s debt maturity profile has been restructured to reduce near-term repayment pressures, with only 13% of debt due in 2024-2025, compared to 36% before refinancing.

Forward-Looking Statements

Looking ahead, DOID provided guidance for the full year 2024, projecting overburden removal of 530-580 MBCM and coal production of 85-90 million tonnes. The company expects revenue of US$1,725-1,825 million and EBITDA of US$300-350 million, with capital expenditure projected at US$150-190 million.

The company’s order book growth provides significant revenue visibility, supported by a landmark contract extension and expansion of US$7.8 billion with PT Indonesia Pratama, a new contract of US$755 million with PT Persada Kapuas Prima, and an extension in Meandu valued at AUD400 million.

DOID is also advancing its ESG initiatives, including carbon footprint assessments, carbon reduction initiatives, and an independently assured sustainability report. These efforts align with the company’s strategic shift toward more environmentally sustainable operations and commodities.

The combination of strategic diversification, order book growth, and debt management positions DOID to navigate current operational challenges while pursuing long-term growth opportunities in both traditional and future-facing commodities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.