TSX jumps amid Fed rate cut hopes, ongoing U.S. government shutdown

Introduction & Market Context

PTT Exploration and Production PCL DRC (PTTEP) released its second quarter 2025 results on July 29, showing a decline in profits despite maintaining stable sales volumes. The company’s stock price decreased by 1.27% following the announcement, closing at $4.66, as investors reacted to the earnings report that met but did not exceed market expectations.

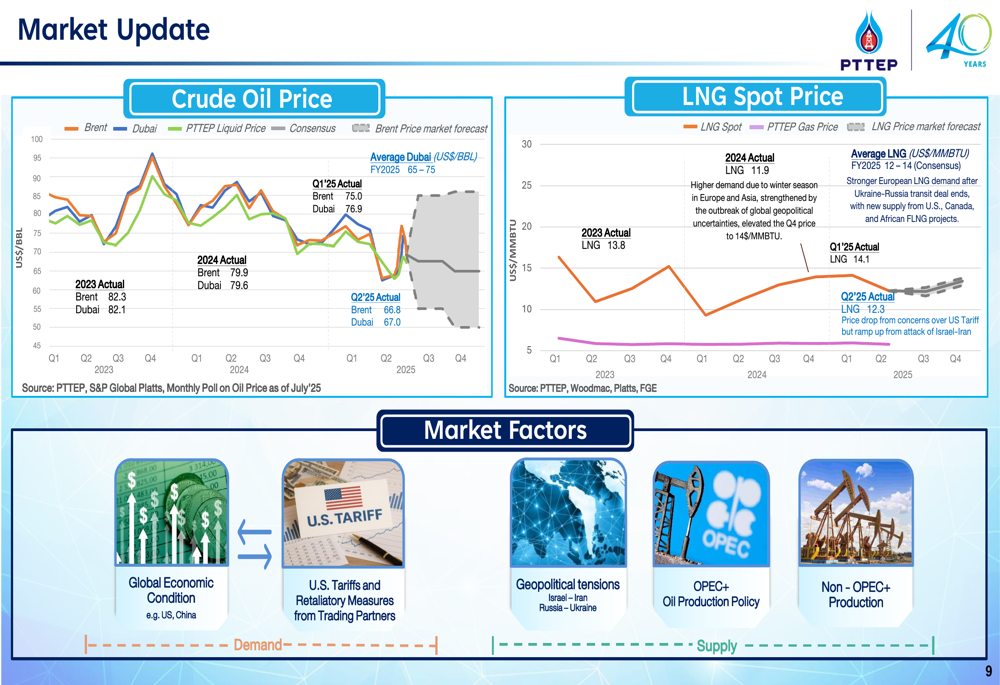

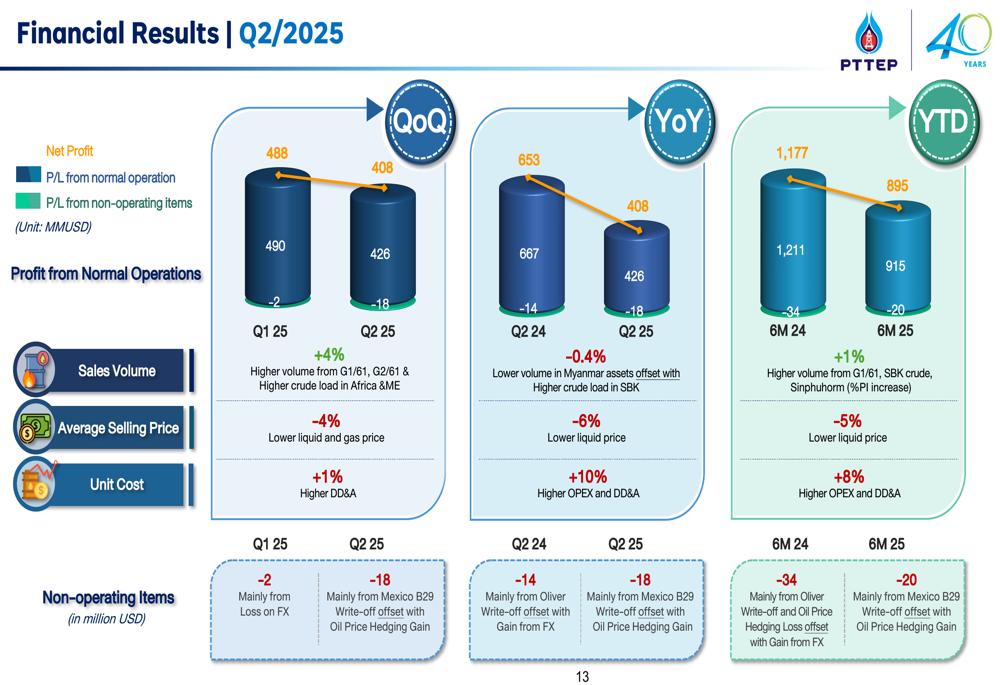

PTTEP reported net profit of $408 million for Q2 2025, down from $488 million in the previous quarter and $653 million in the same period last year. This decline occurred against a backdrop of lower crude oil prices, with Dubai crude averaging $67.0 per barrel in Q2 2025 compared to $76.9 in Q1 and $85.3 in Q2 2024.

As shown in the following chart of crude oil and LNG price trends, market factors including global economic conditions, U.S. tariffs, geopolitical tensions, and OPEC+ production policies have influenced energy prices:

Quarterly Performance Highlights

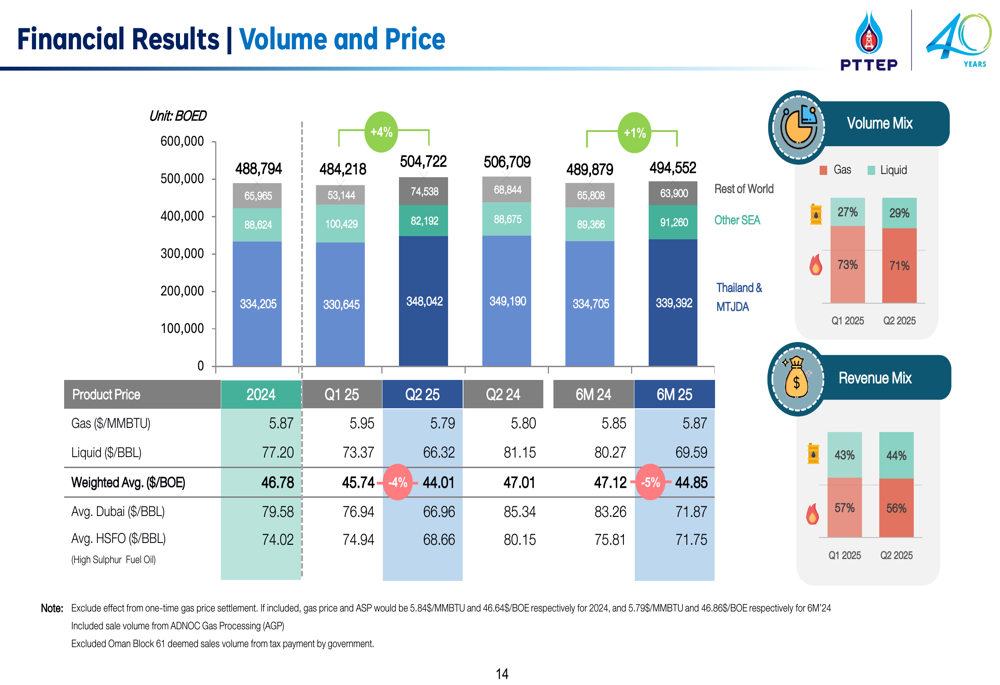

PTTEP’s financial results for Q2 2025 show mixed performance across key metrics. While sales volume increased by 4% quarter-on-quarter to approximately 505,000 barrels of oil equivalent per day (BOED), average selling prices declined by 4% to $44.01 per BOE. The company maintained a strong EBITDA margin of 72%, demonstrating operational efficiency despite challenging market conditions.

The following chart illustrates the company’s financial performance across multiple periods, highlighting the downward trend in net profit:

The company’s revenue mix remained relatively stable, with gas accounting for 71% of volume but only 44% of revenue in Q2 2025. This reflects the higher value of liquid products in the company’s portfolio:

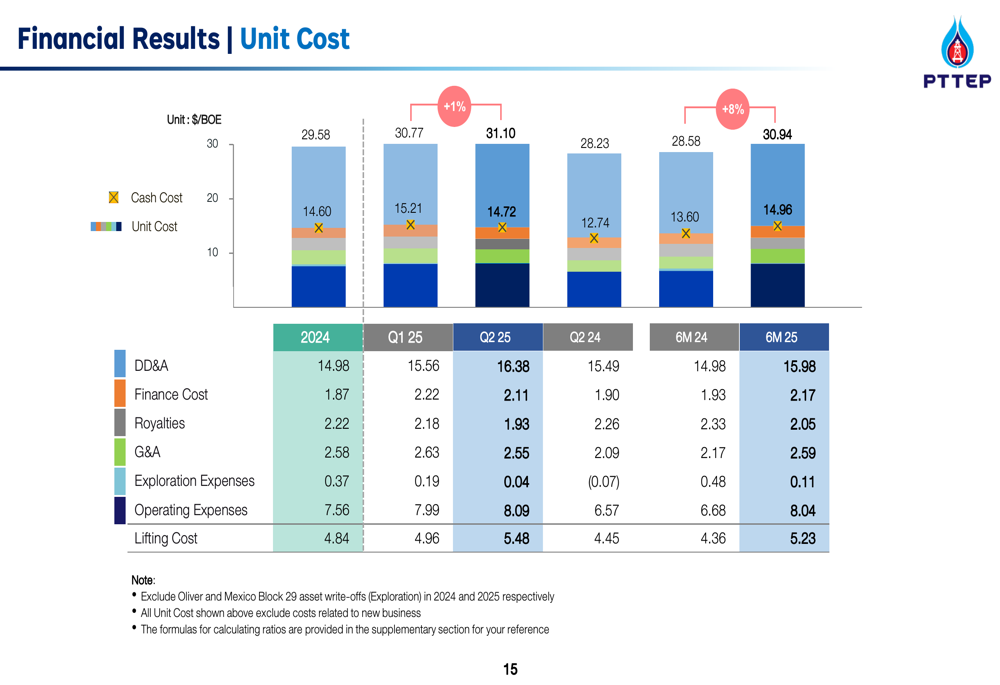

Unit costs increased by 1% quarter-on-quarter and 10% year-on-year, reaching $23.97 per BOE in Q2 2025. This increase was primarily driven by higher depreciation, depletion, and amortization (DD&A) costs, which rose to $16.38 per BOE:

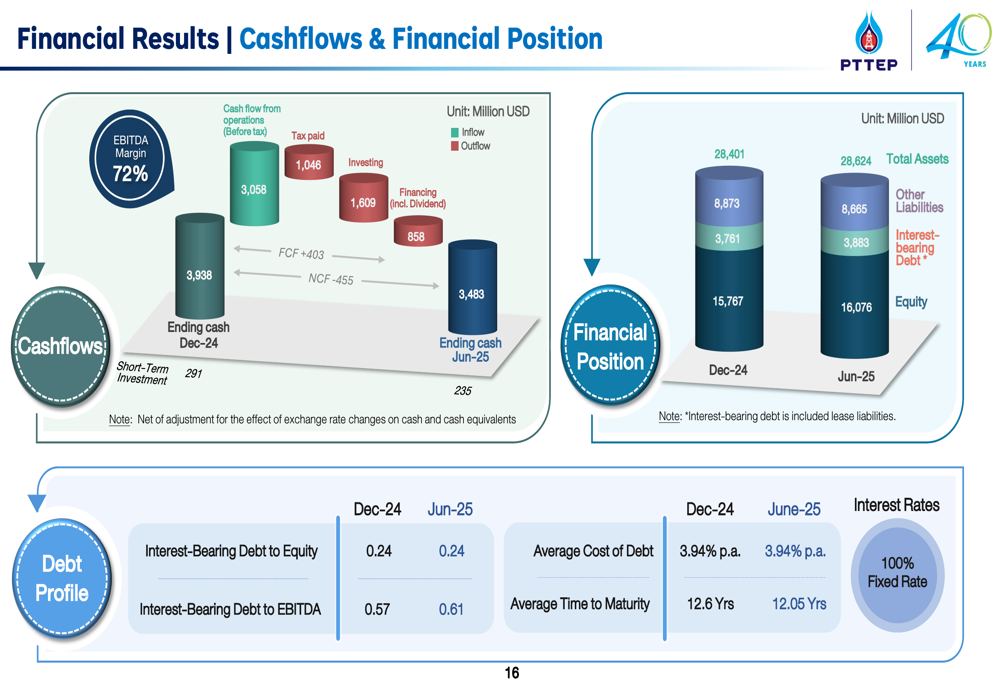

PTTEP maintained a strong financial position with $3.48 billion in cash as of June 2025 and a low interest-bearing debt to equity ratio of 0.24. The company’s average cost of debt stands at 3.94% per annum, with 100% fixed rate financing providing stability in the current interest rate environment:

Strategic Initiatives

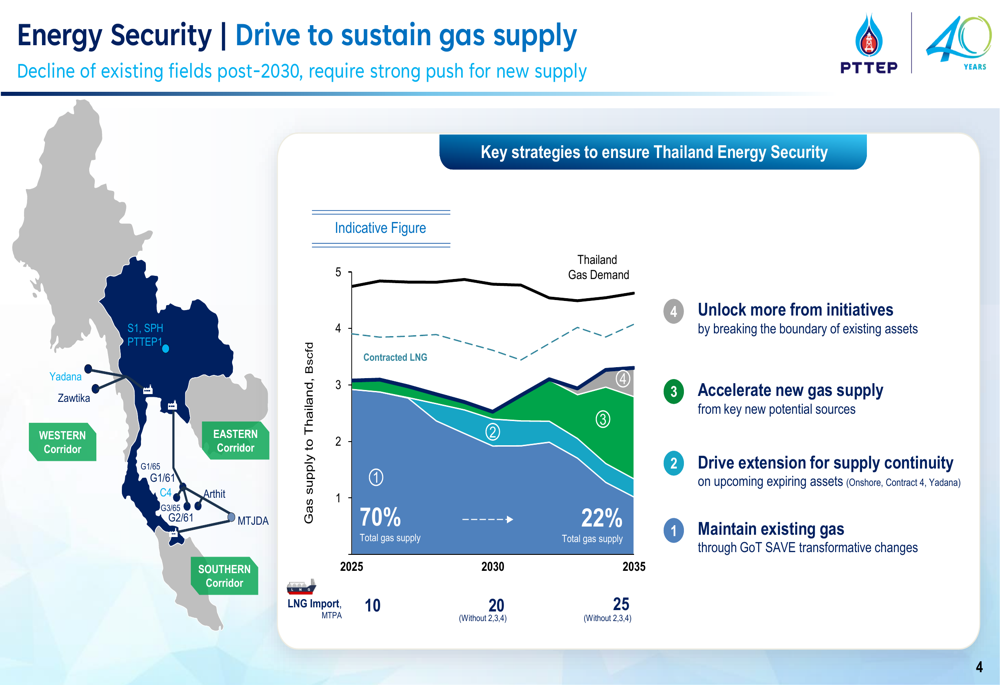

A key focus of PTTEP’s strategy is ensuring Thailand’s energy security amid declining production from existing fields post-2030. The company outlined a comprehensive approach to sustain gas supply through maintaining existing fields, extending supply from expiring assets, accelerating new gas development, and optimizing existing assets:

PTTEP’s growth strategy emphasizes value over volume, with a selective approach to exploration and acquisitions. The company prioritizes gas projects in late exploration and early production stages within focus areas, collaborating with strategic partners to enhance value creation:

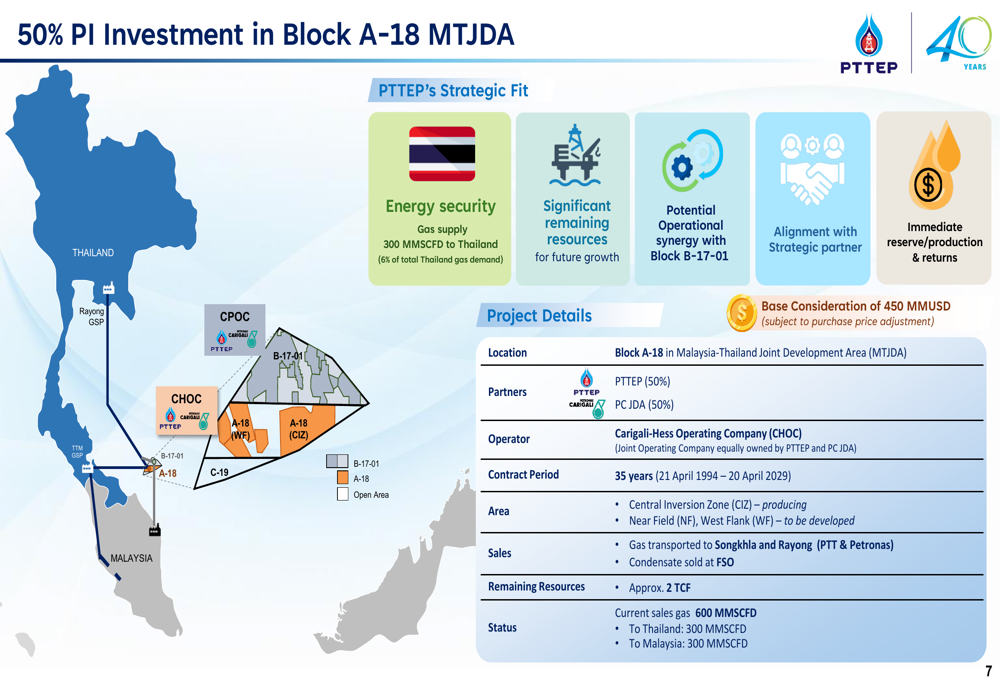

A significant strategic move during the quarter was PTTEP’s acquisition of a 50% participating interest in Block A-18 MTJDA (Malaysia-Thailand Joint Development Area) for $450 million. This acquisition aligns with the company’s energy security objectives and provides immediate reserves, production, and returns:

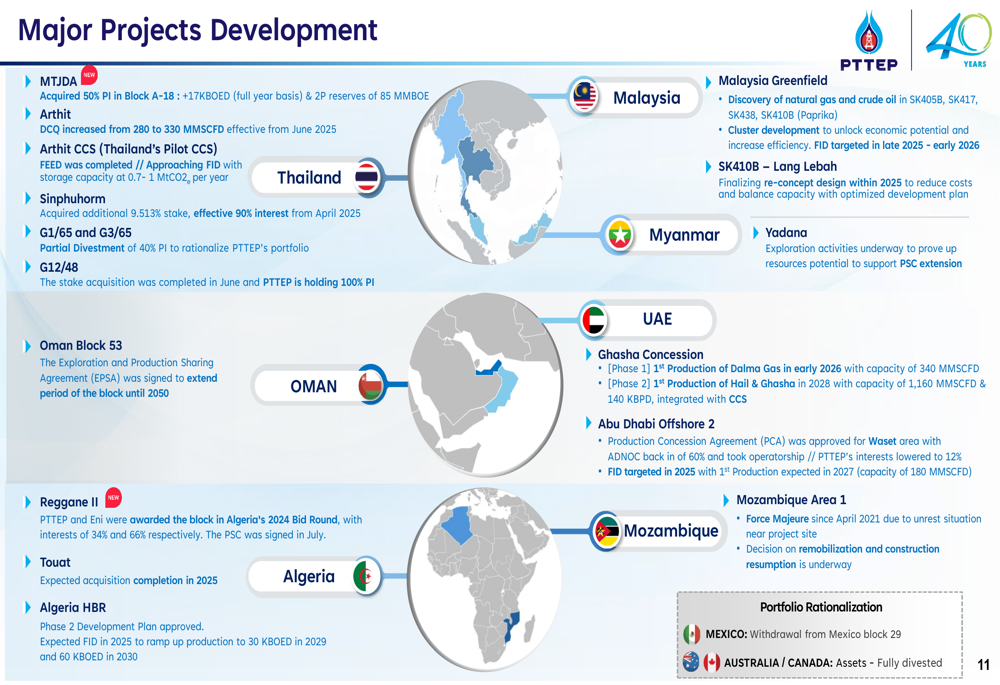

The company also provided updates on major projects across its global portfolio, including increased daily contract quantity at Arthit, progress on carbon capture and storage projects, and new discoveries in Malaysia:

Forward-Looking Statements

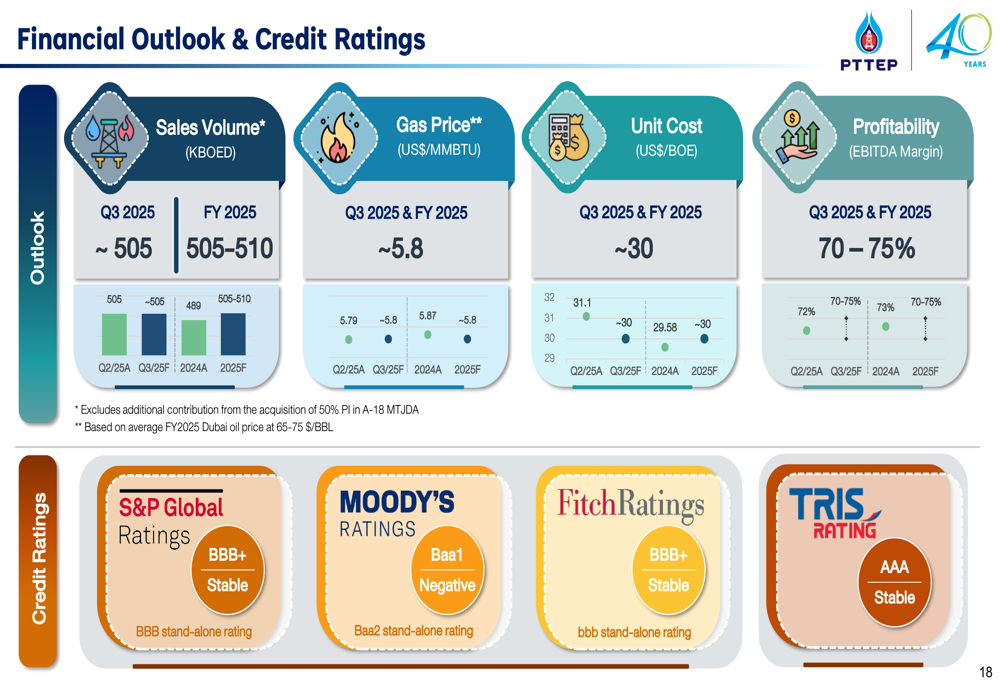

For Q3 2025, PTTEP forecasts sales volume of approximately 505,000 BOED with an average gas price of $5.8 per MMBTU and unit cost of around $30 per BOE. The company expects to maintain profitability in the range of 70-75%. For the full year 2025, PTTEP projects sales volume between 505,000 and 510,000 BOED:

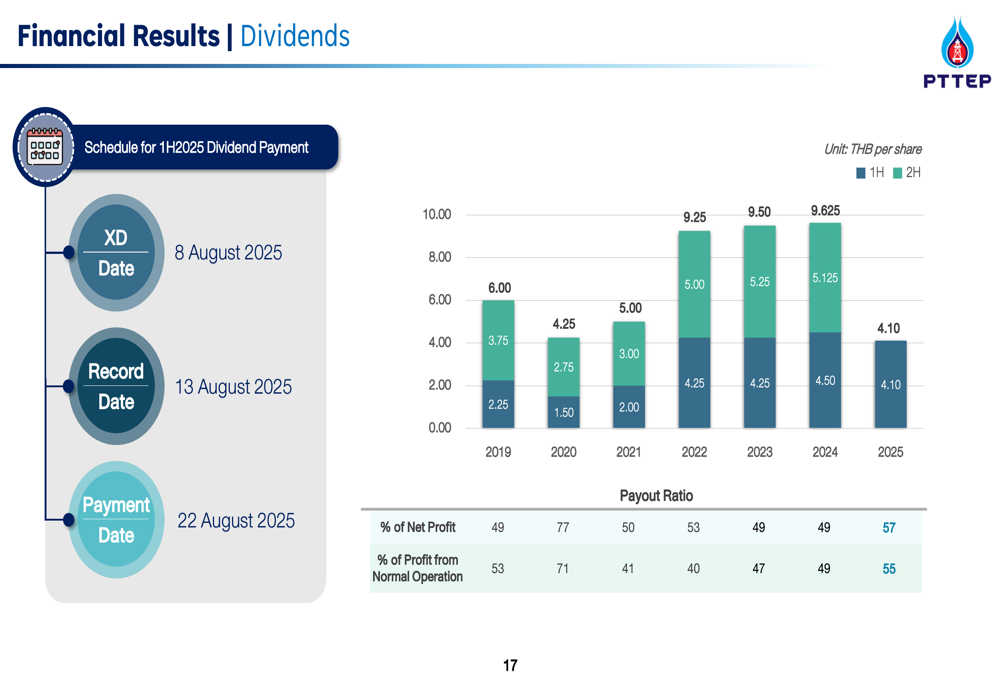

The company announced its dividend payment schedule for the first half of 2025, with an XD date of August 8, record date of August 13, and payment date of August 22. PTTEP has maintained a consistent dividend policy, with the payout ratio increasing from 49% in 2019 to 57% in 2025:

Conclusion

PTTEP’s Q2 2025 results reflect the challenges of operating in a volatile energy market, with lower selling prices and higher unit costs impacting profitability despite stable production volumes. The company’s strategic focus on energy security, selective acquisitions, and operational efficiency demonstrates a long-term approach to value creation.

With a strong financial position, low debt levels, and consistent dividend payments, PTTEP appears well-positioned to navigate market uncertainties. However, the stock’s negative reaction to the earnings announcement suggests investors may have expected stronger results or more detailed guidance on future growth initiatives, particularly regarding the company’s hinted investments in Mexico and Japan.

The company’s ability to execute its strategic initiatives while managing costs in a challenging price environment will be crucial for improving financial performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.