Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Q2 Holdings (NYSE:QTWO) presented its second quarter 2025 financial results on July 30, highlighting strong performance across key metrics despite facing headwinds in its stock price. The digital banking solutions provider demonstrated robust growth in its subscription-based business model while successfully transitioning from net losses to profitability.

The company’s presentation comes at a challenging time for its stock, which has declined nearly 39% year-to-date according to market data, trading near its 52-week low despite the positive operational performance.

Quarterly Performance Highlights

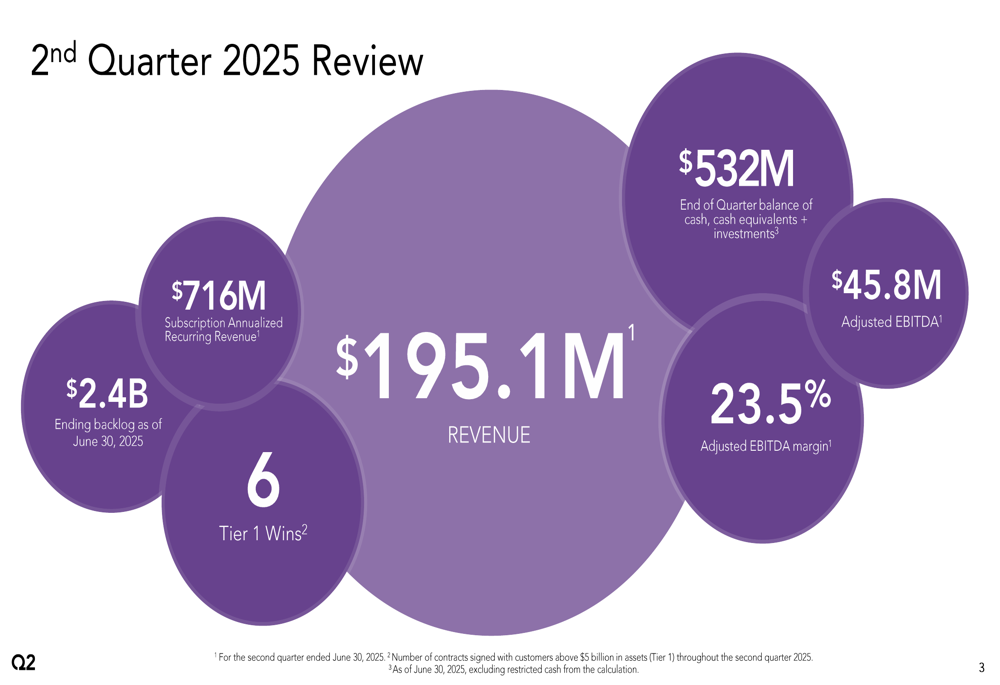

Q2 Holdings reported revenue of $195.1 million for the second quarter of 2025, representing a 13% increase compared to the same period last year. The company’s subscription-based model continued to show strength, with Subscription Annualized Recurring Revenue (ARR) reaching $716 million, up 13% year-over-year.

As shown in the following summary of Q2 2025 key metrics:

Perhaps most notably, Q2 Holdings achieved a significant improvement in profitability, with adjusted EBITDA of $45.8 million, representing a 53% increase year-over-year. The adjusted EBITDA margin expanded to 23.5%, demonstrating the company’s ability to scale efficiently.

The company’s Chairman and CEO Matt Flake highlighted the strong performance in a statement included in the presentation: "We delivered strong financial results in the second quarter." This positive sentiment reflects the company’s successful execution of its growth strategy and operational improvements.

Detailed Financial Analysis

A deeper look at Q2’s financial results reveals substantial improvements across multiple metrics. The company successfully transitioned from a net loss of $13.1 million in Q2 2024 to a net income of $11.8 million in Q2 2025. Gross profit increased by 20% year-over-year, while non-GAAP gross profit grew by 17%.

The following table provides a comprehensive comparison of Q2 2025 results with the same period last year:

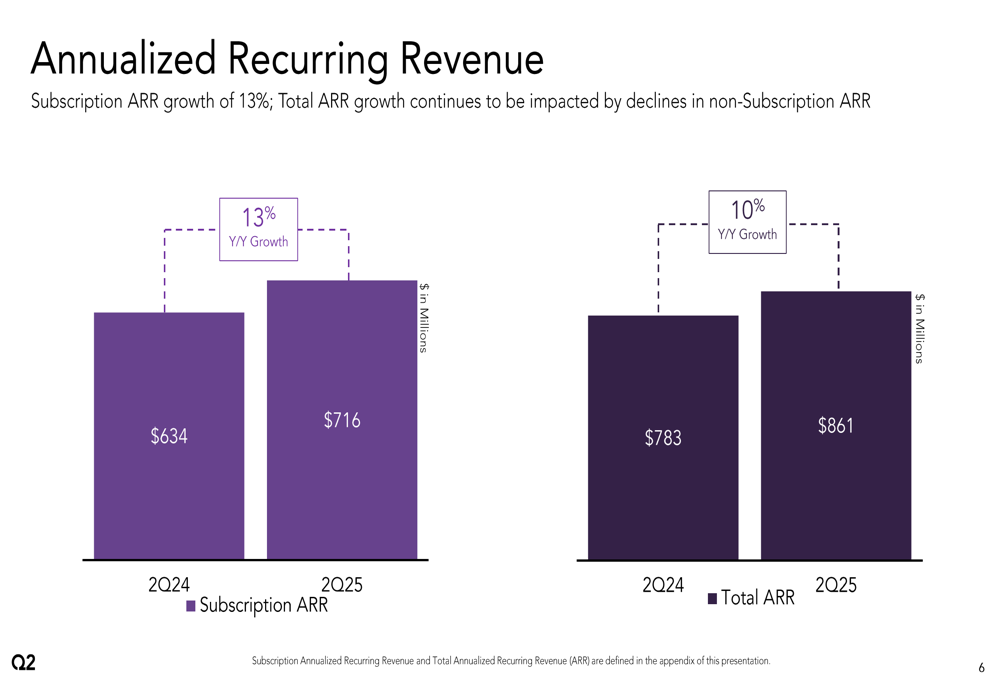

The company’s recurring revenue streams continue to strengthen, with Total Annualized Recurring Revenue reaching $861 million, up 10% year-over-year. While subscription ARR grew at 13%, the total ARR growth was partially offset by declines in non-subscription ARR.

As illustrated in the ARR growth chart:

Q2 Holdings’ backlog, also referred to as Remaining Performance Obligations (RPO), reached $2.4 billion as of June 30, 2025, representing a 21% increase year-over-year and a 3% sequential increase from the previous quarter. This growing backlog provides strong visibility into future revenue potential, with 54% expected to be recognized within the next 24 months.

Customer Base and Revenue Diversification

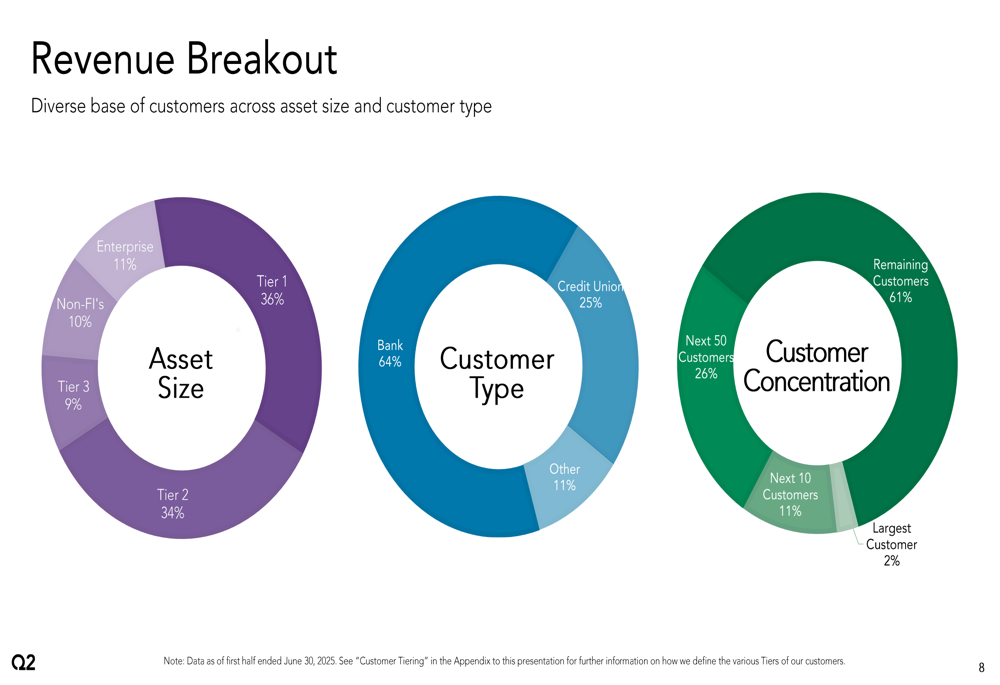

The company’s revenue is well-diversified across different customer segments, reducing concentration risk. Q2 Holdings serves over 1,300 customers, with banks accounting for 64% of revenue, credit unions for 25%, and other institutions for 11%.

The revenue distribution by customer size shows a balanced approach, with Tier 1 customers (those with assets exceeding $5 billion) representing 36% of revenue, Tier 2 at 34%, Enterprise at 11%, Non-Financial Institutions at 10%, and Tier 3 at 9%.

The company’s customer concentration risk remains low, with the largest customer accounting for only 2% of total revenue, while the next 10 largest customers represent 11%, and the next 50 account for 26%.

As shown in the revenue breakout charts:

Forward-Looking Statements

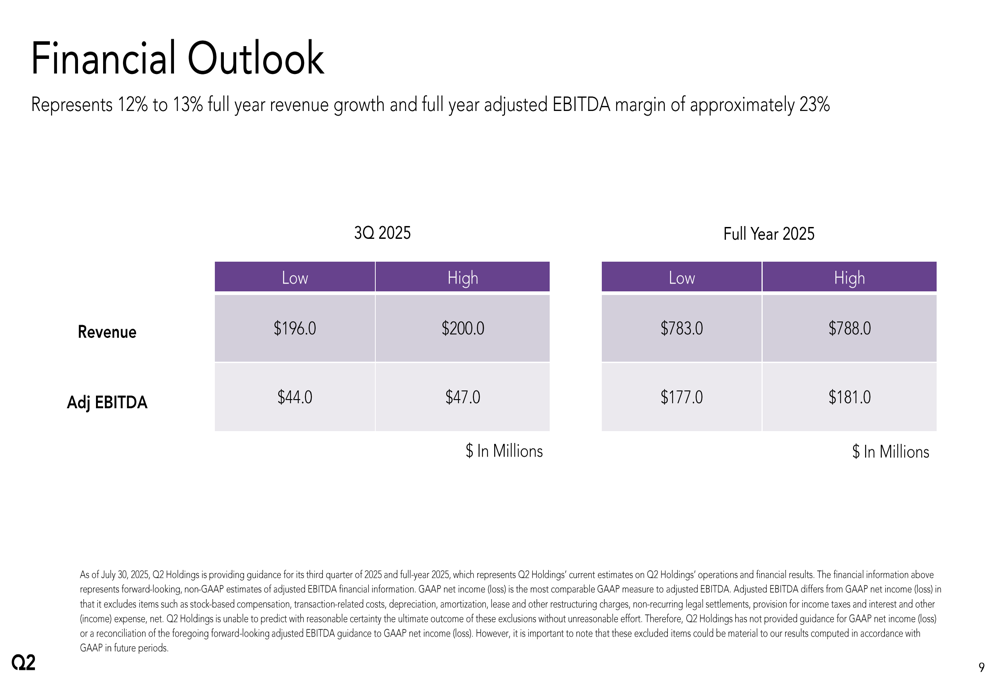

Q2 Holdings provided an optimistic outlook for the remainder of 2025. For the third quarter, the company expects revenue between $196.0 and $200.0 million, with adjusted EBITDA between $44.0 and $47.0 million.

For the full year 2025, Q2 Holdings raised its guidance to revenue between $783.0 and $788.0 million, representing 12% to 13% annual growth. The company also expects adjusted EBITDA between $177.0 and $181.0 million, maintaining an adjusted EBITDA margin of approximately 23%.

The following financial outlook details the company’s expectations:

Looking further ahead, Q2 Holdings outlined its financial targets for 2024-2026, aiming for average annual subscription revenue growth of approximately 15%, driven by strong market demand. The company also targets average annual adjusted EBITDA margin expansion of approximately 360 basis points and free cash flow conversion exceeding 90% by full year 2026.

Stock Performance Context

Despite the strong operational performance and positive outlook, Q2 Holdings’ stock has faced significant pressure in 2025. According to market data, the stock was trading at $60.46 in pre-market on October 14, 2025, down 1.82% and near its 52-week low of $60.28. This represents a substantial decline of nearly 39% year-to-date, creating a notable disconnect between the company’s financial performance and its stock market valuation.

The company maintains a market capitalization of approximately $3.83 billion with a moderate debt level. The stock’s underperformance despite improving fundamentals may present both challenges and opportunities for the company and its investors as Q2 Holdings continues to execute on its growth strategy.

Long-Term Growth Potential

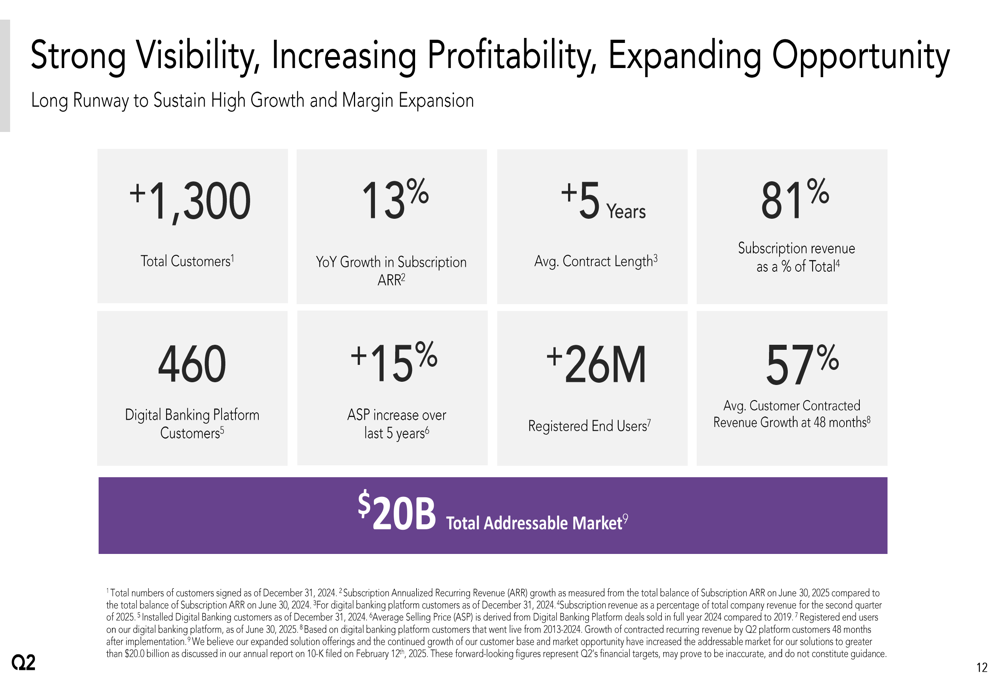

Q2 Holdings emphasized several factors supporting its long-term growth potential in the presentation. The company estimates its total addressable market at $20 billion, suggesting significant room for expansion. With average contract lengths exceeding five years and average customer contracted revenue growth of 57% at 48 months, Q2 Holdings has demonstrated its ability to not only retain customers but also expand relationships over time.

The company’s focus on digital transformation in financial services positions it well in an increasingly digital banking environment. With over 26 million registered end users and a 15% increase in average selling price over the last five years, Q2 Holdings continues to demonstrate the value of its solutions to financial institutions of various sizes.

As shown in the following summary of key growth metrics:

With subscription revenue now accounting for 81% of total revenue and a clear strategy for continued growth and margin expansion, Q2 Holdings appears well-positioned to capitalize on the ongoing digital transformation in the financial services industry, despite the current disconnect between its operational performance and stock market valuation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.