Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Qliro AB (QLIRO) presented its Q1 2025 results on April 30, highlighting significant merchant growth and payment volume expansion despite challenging market conditions. The Swedish payment solutions provider continues to pursue its ambition of becoming a leading player in the Nordic payments market, with a particular focus on small and medium-sized enterprises (SMEs).

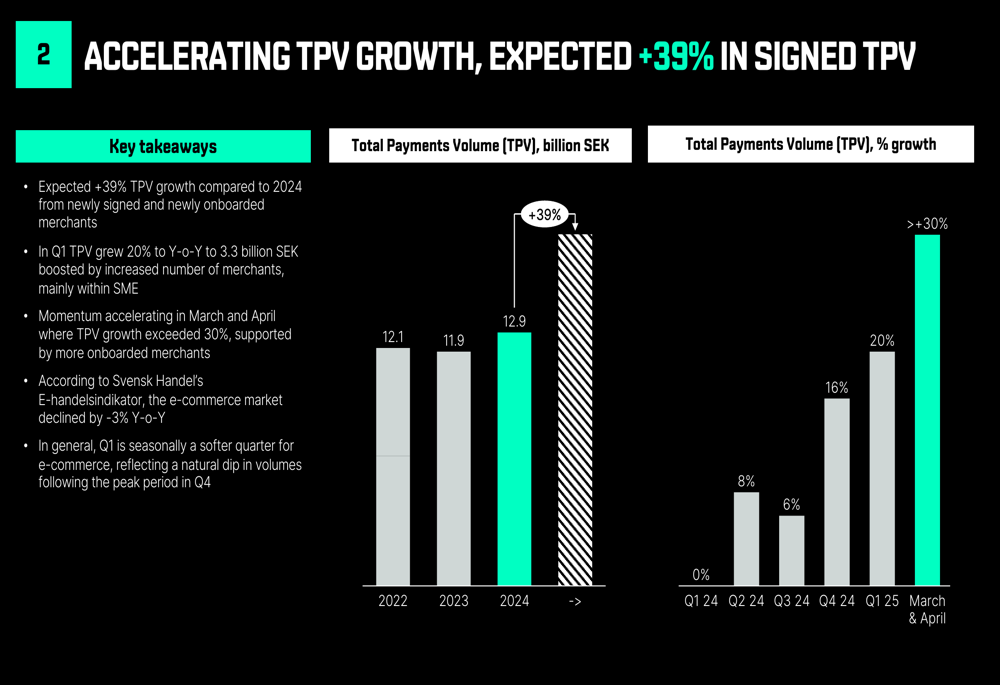

According to Svensk Handel’s E-handelsindikator, the broader e-commerce market declined by 3% year-over-year during the quarter, making Qliro’s growth performance particularly notable. The company’s stock closed at 21.42 SEK on April 30, up 2.26% for the day.

Quarterly Performance Highlights

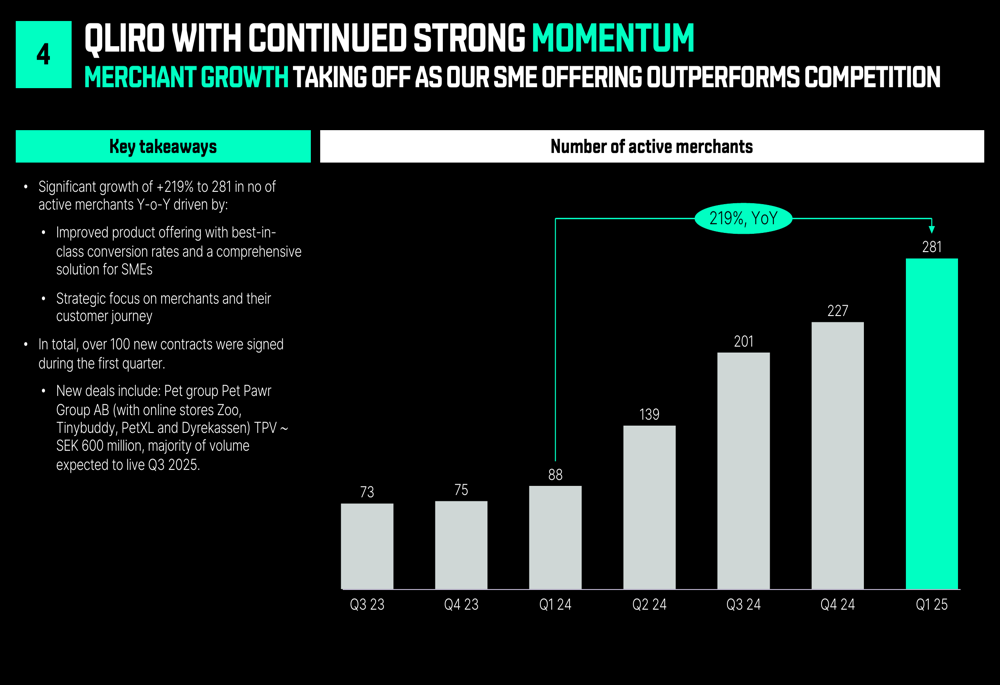

Qliro reported a 20% year-over-year increase in Total (EPA:TTEF) Payment Volume (TPV) to 3.3 billion SEK in Q1 2025, with momentum accelerating in March and April to exceed 30% growth. This expansion was primarily driven by a remarkable 219% increase in the merchant base, which grew from 88 to 281 active merchants compared to the same period last year.

As shown in the following chart, Qliro’s merchant acquisition has maintained strong momentum over several quarters:

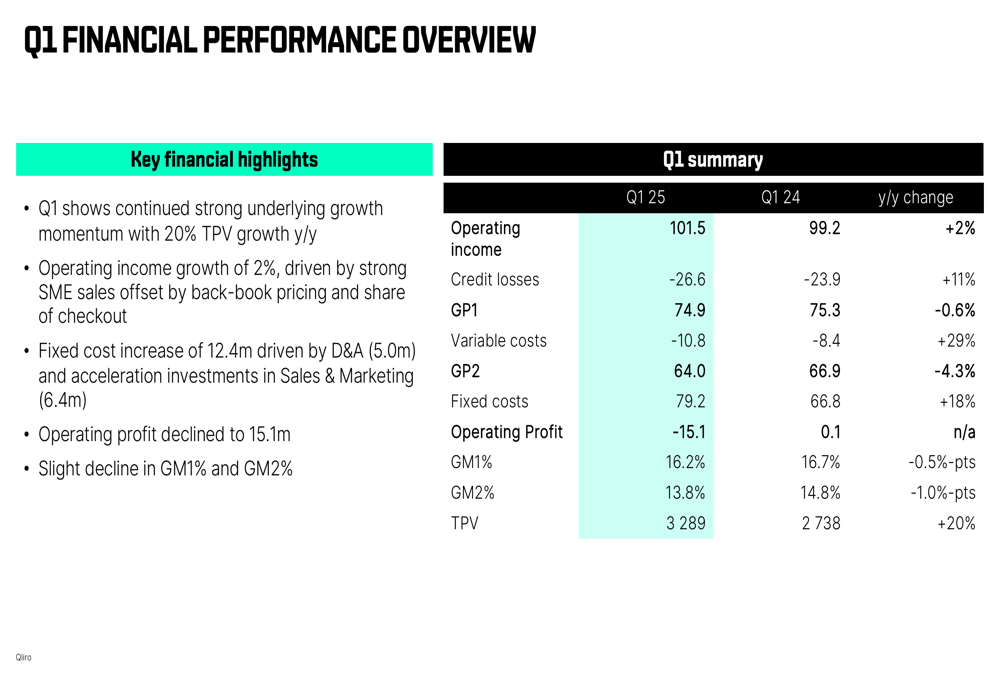

Operating income grew modestly by 2% to 101.5 million SEK, while operating profit declined to -15.1 million SEK from 0.1 million SEK in Q1 2024. This decline in profitability was largely attributed to strategic investments in expansion initiatives, particularly in Norway and Finland.

The following table provides a comprehensive overview of Qliro’s Q1 2025 financial performance:

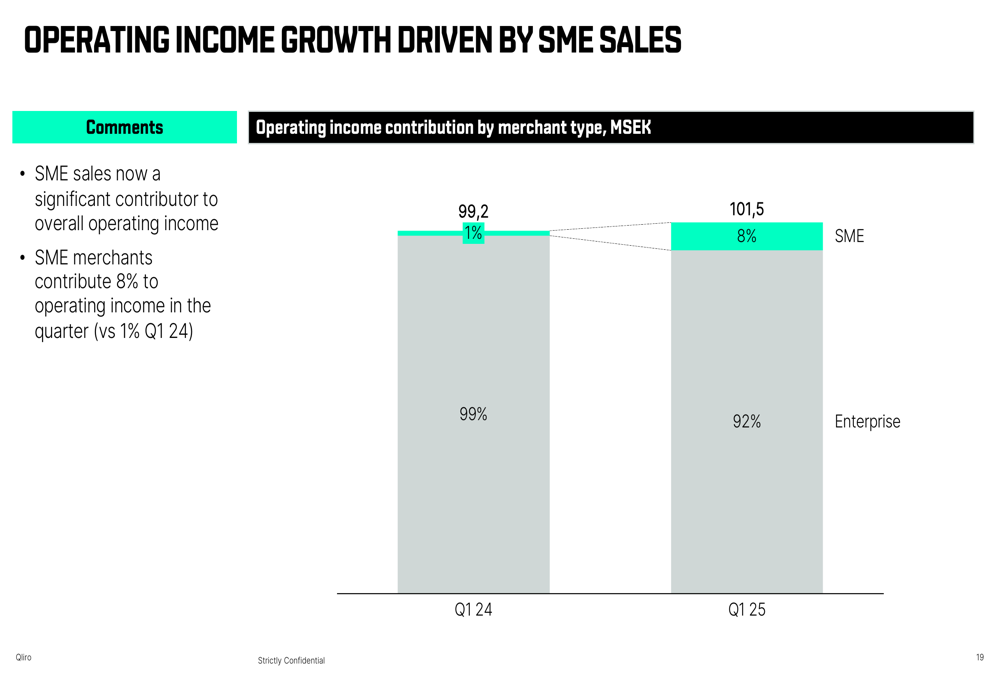

A notable development in Qliro’s business model is the growing contribution from SMEs, which now represent 8% of operating income compared to just 1% in Q1 2024. This shift reflects the company’s strategic focus on expanding its SME customer base with a scalable go-to-market model.

The following chart illustrates this significant change in revenue composition:

Strategic Initiatives & Nordic Expansion

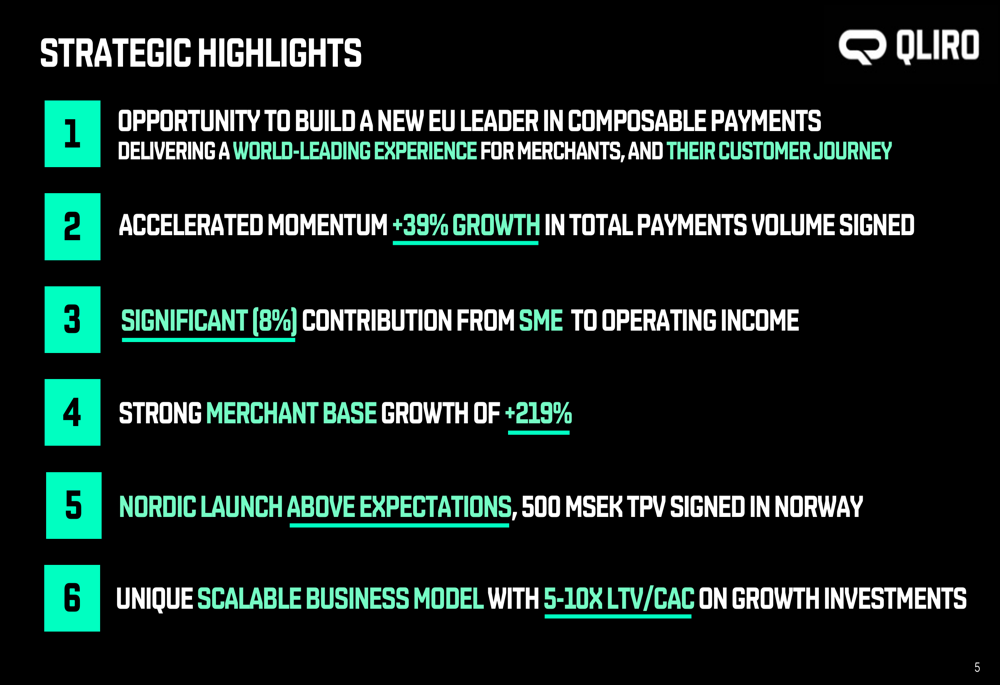

Qliro’s presentation emphasized its vision of "building an EU leader in composable payments, starting in the Nordics, with global capabilities." The company reported strong progress in its Nordic expansion, particularly in Norway, where it has signed contracts representing 500 million SEK in TPV.

CEO Christoffer Rutgersson highlighted that the contracted volumes in Norway alone are expected to bring that market to break-even once fully implemented. Additionally, Qliro has established a local presence in Finland, with a country manager and commercial team of four full-time employees already in place as of Q1 2025.

The company also announced two strategic partnerships during the quarter. A new technical integration with Bits Technology aims to streamline merchant onboarding, reducing lead times from weeks to days. Additionally, a partnership with B2B pay-later provider Two has enabled Qliro to launch a new B2B solution integrated into its checkout platform.

Detailed Financial Analysis

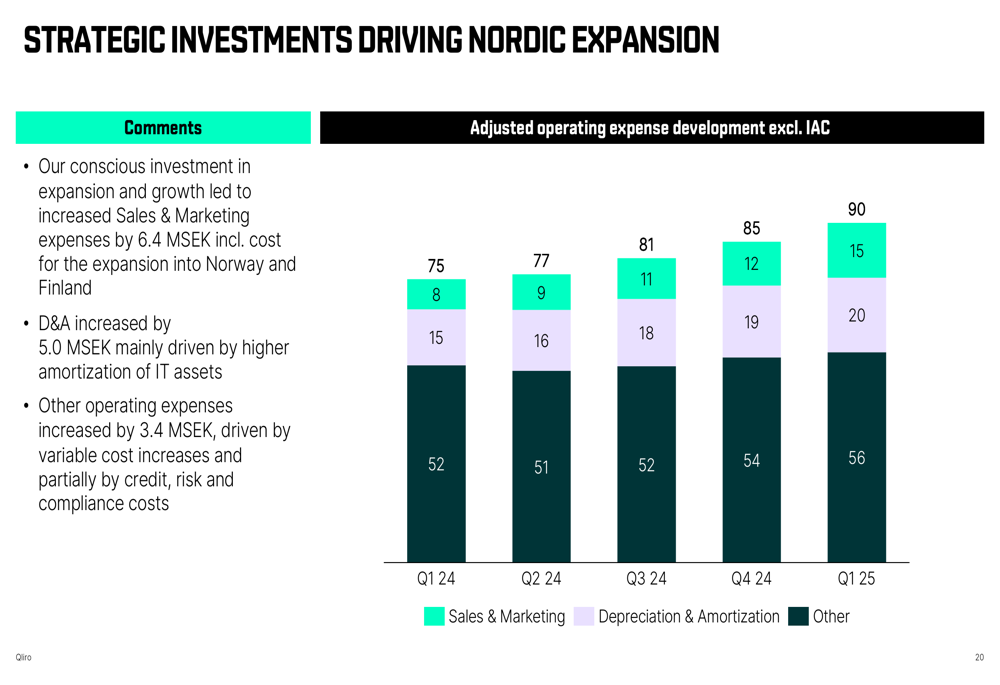

While Qliro’s top-line growth metrics were impressive, the financial details reveal both strengths and challenges. The company’s fixed costs increased by 18% to 79.2 million SEK, driven by higher depreciation and amortization (5.0 million SEK increase) and accelerated investments in sales and marketing (6.4 million SEK increase).

As shown in the following chart, these strategic investments are primarily focused on supporting Nordic expansion:

The company’s payment mix continues to evolve, with Pay Now volumes increasing by 36% to 1.9 billion SEK, while Buy Now Pay Later (BNPL) volumes decreased by 9%. This shift reflects changing consumer preferences and Qliro’s expanding merchant base using the platform for various payment methods.

Despite the increased investments, Qliro maintained a strong capital position with a capital headroom of 8.2 percentage points (182 million SEK) above regulatory requirements. The company successfully issued a 70 million SEK Tier 2 bond in March, further strengthening its financial foundation.

Forward-Looking Statements

Qliro reiterated its guidance of 15-30% income growth in the second half of 2025 and expects TPV growth to exceed 39% compared to 2024, based on newly signed and onboarded merchants. The company emphasized the attractive economics of its growth model, citing a lifetime value to customer acquisition cost (LTV/CAC) ratio of 5-10x.

The following chart illustrates Qliro’s accelerating TPV growth trajectory:

Management indicated that certain headwinds, including volume losses from a major enterprise merchant and negative price impacts from certain enterprise agreements, are expected to affect comparative figures until summer 2025. However, the company remains confident that its strong commercial momentum and Nordic expansion will drive sustainable growth in the medium term.

Qliro’s strategic highlights for the quarter emphasize its positioning and growth trajectory:

While the company continues to prioritize growth and market expansion over short-term profitability, investors will be watching closely to see if the substantial investments in merchant acquisition and geographic expansion translate into improved financial performance in the second half of 2025, as management has projected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.