Beamr video compression achieves up to 50% improvement for AVs

Introduction & Market Context

Qoria Ltd (ASX:QOR) released its June Quarter 2025 presentation on July 22, highlighting record Annual Recurring Revenue (ARR) growth and significant improvements in profitability. The company’s stock closed at $0.45, up 2.22% on the day of the presentation.

The online safety and student wellbeing provider reported reaching 27 million students across more than 29,000 schools globally, cementing its position as a market leader with 17% of US students and 40% of UK students using its platforms. The company now serves parents and educational institutions across more than 100 countries.

Quarterly Performance Highlights

Qoria delivered record ARR growth of $29 million (25% YoY) for FY2025, achieving an exit ARR of $145 million despite a $4 million negative impact from the falling USD:AUD exchange rate in the June quarter.

As shown in the following chart of ARR growth:

The June quarter alone saw $14 million of net ARR added, representing a 55% increase compared to the prior corresponding period. This strong performance was achieved while maintaining operating cost growth at under 1%, demonstrating significant operating leverage.

EBITDA surged to $15.4 million, up 670% compared to FY2024, with an EBITDA margin of 13.1%. The company’s service margin improved to 91%, reflecting Qoria’s transition to a more efficient business model.

The company’s global impact is illustrated in this breakdown:

Detailed Financial Analysis

Qoria ended FY2025 with $15.4 million in cash and net debt of $36.8 million. The June quarter saw collections of $21.1 million, up 10% year-over-year. When adjusting for the sale of Migiri and progress to annual billing cycles, effective collections growth was 24%.

The company’s financial performance is illustrated in this multi-dimensional growth chart:

Operating cash flow for FY2025 was $15 million, while free cash flow was negative $11 million. However, management expects to achieve positive free cash flow in calendar year 2025 and FY2026, marking a significant milestone in the company’s financial journey.

Qoria demonstrated strong operating leverage, with fixed cash costs as a percentage of ARR declining from 80% in FY2023 to 65% in FY2025. This improvement in cost efficiency is contributing to the company’s path toward sustainable profitability.

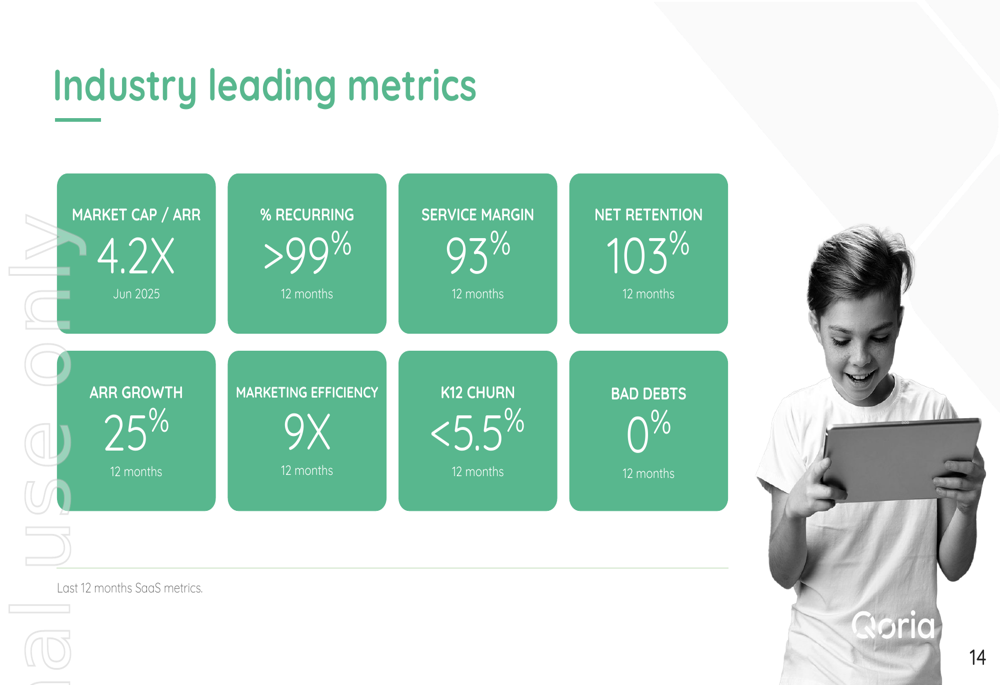

The company’s industry-leading metrics include:

Strategic Initiatives & Regional Performance

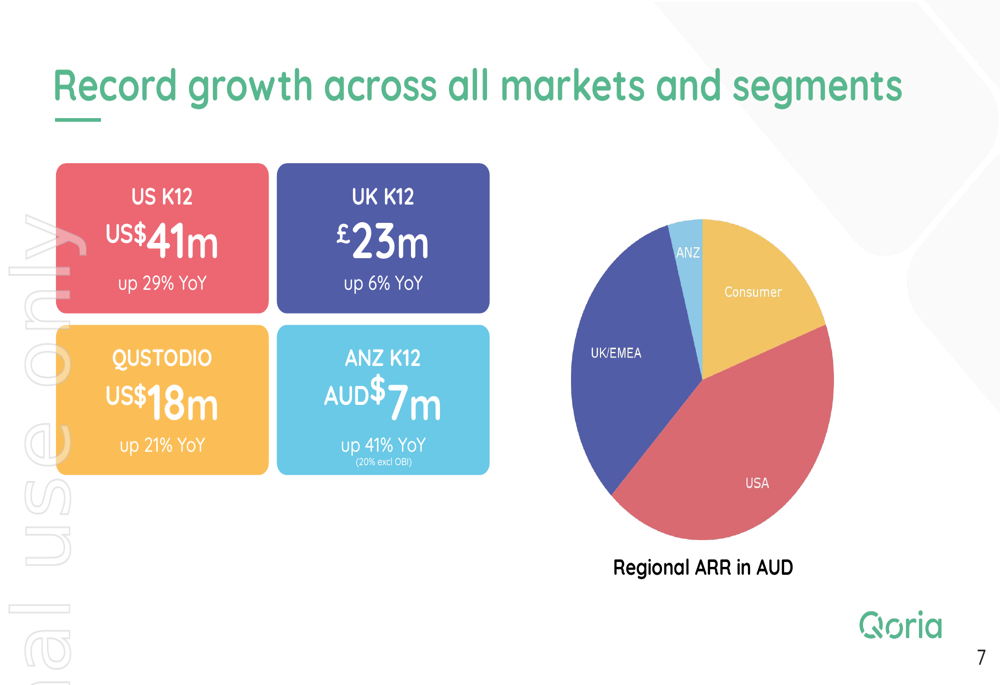

Qoria reported strong growth across all regions, with US K12 (NYSE:LRN) ARR reaching US$41 million (up 29% YoY), UK K12 at £23 million (up 6% YoY), and ANZ K12 at AUD$7 million (up 41% YoY). The consumer business, Qustodio, grew to US$18 million ARR (up 21% YoY).

Regional performance is detailed in the following chart:

A significant strategic win was announced with the Pennsylvania Association of Intermediate Units (PAIU), positioning Qoria as a panel provider and partner for all Pennsylvania districts. This agreement covers Filter, Classwize, Monitor, and Edtech Insights products and provides access to Pennsylvania’s 1.7 million students, the 9th largest state by K12 population.

The company’s K12 division achieved record growth of $12 million in ARR for the quarter, with exit ARR of approximately $118 million. Average Sales Price grew by 20% to $20,600, while maintaining net revenue retention above 100% and churn around 5%.

In the consumer segment, Qoria added $2 million of net ARR in what is typically a slow quarter, with improvements in customer acquisition costs (CAC), average revenue per user (ARPU), and lifetime value (LTV). The company has begun rolling out new user experiences for Qustodio, making it easier for parents to find and manage their children’s accounts.

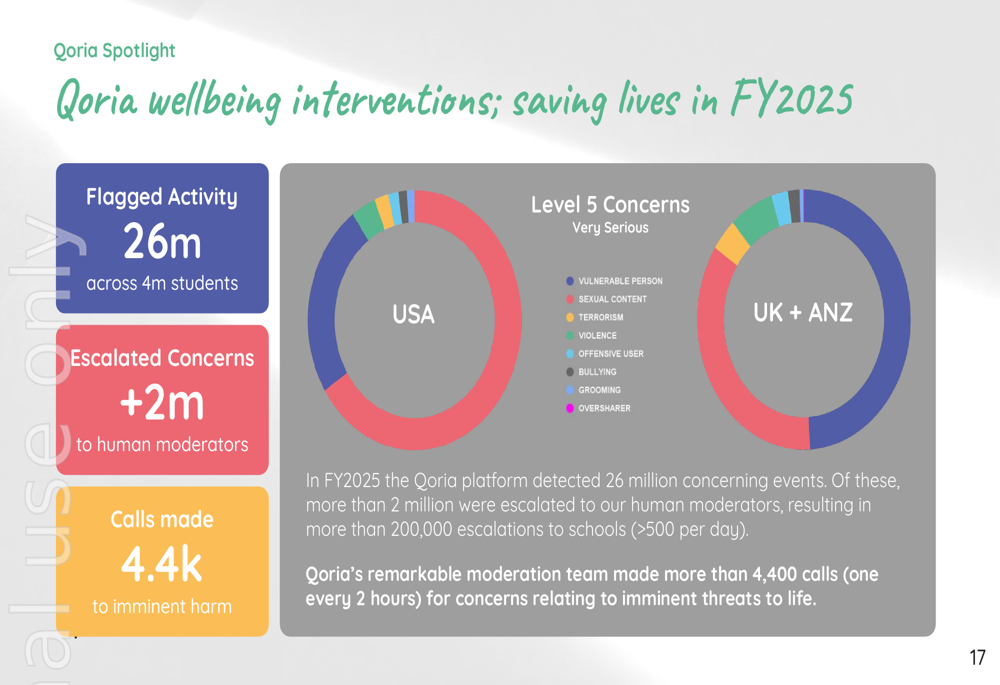

The company’s wellbeing interventions are making a significant impact, as shown in this chart:

Forward-Looking Statements

For FY2026, Qoria provided guidance of:

- Revenue exceeding $140 million

- ARR growth of at least 20%

- EBITDA margin of at least 20%

- Positive free cash flow for the full year

- Cash collections growth of at least 20% in H1 compared to the prior corresponding period

The company enters FY2026 with a record September quarter pipeline of $28 million, with a weighted value of $9 million, positioning it well for a strong calendar year close.

Management expects H1 FY2026 receipts to be up 20% compared to the prior corresponding period, driven by strong end-of-year sales and stabilization of billing cycles. The company also anticipates FY2026 closing net debt to be in line with or lower than FY2025, with material reductions expected in FY2027 and beyond.

As Qoria continues its transition from growth to profitability, the focus remains on expanding its global footprint while maintaining tight cost control and improving margins. With its strong market position in online safety and student wellbeing, the company appears well-positioned to deliver on its financial targets for the coming year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.