European stocks retreat on tech valuation concerns; U.K. economic woes

Introduction & Market Context

Quad Graphics Inc (NYSE:QUAD) presented its second quarter 2025 results on July 30, highlighting the company’s ongoing transformation from a traditional print business to what it calls a "Marketing Experience" (MX) company. While the presentation revealed continued revenue challenges, management emphasized progress in its strategic initiatives and improved earnings per share despite top-line pressure.

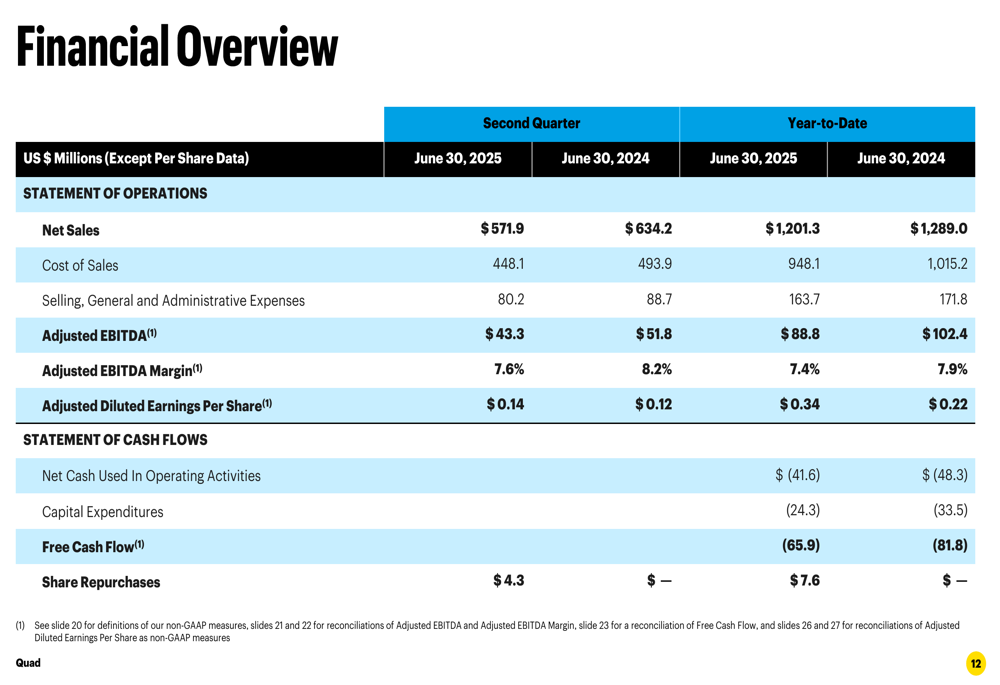

The company reported Q2 2025 net sales of $571.9 million, down 9.8% from $634.2 million in the same period last year, as the print industry continues to face headwinds from digital alternatives. However, Quad’s adjusted diluted earnings per share increased to $0.14, up from $0.12 in Q2 2024, suggesting improved operational efficiency despite revenue challenges.

Quarterly Performance Highlights

Quad’s financial results for Q2 2025 showed mixed performance across key metrics. While revenue declined, the company managed to improve its bottom line and free cash flow position.

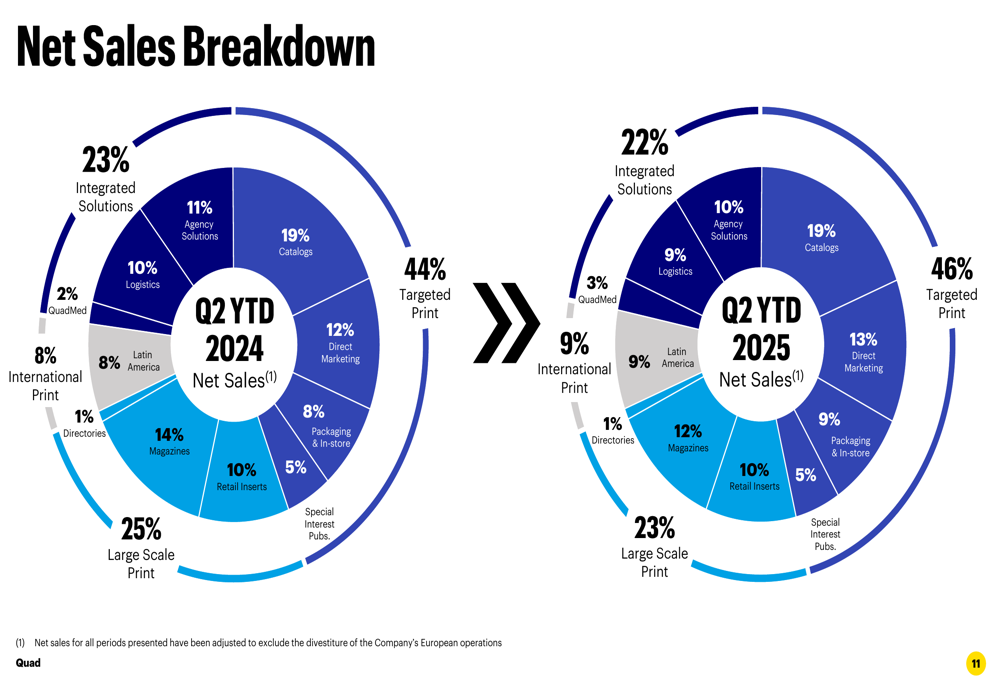

"We continue to build momentum as a marketing experience or MX company," CEO Joel Quadracci stated during the presentation, highlighting the company’s strategic pivot. This transformation is reflected in the company’s evolving sales mix, with targeted print offerings growing from 44% to 46% of total sales, while large-scale print declined from 25% to 23%.

As shown in the following financial overview chart, Quad’s adjusted EBITDA was $43.3 million in Q2 2025, down from $51.8 million in Q2 2024, with adjusted EBITDA margin contracting slightly to 7.6% from 8.2% in the prior year:

The company’s net sales breakdown reveals the ongoing shift in its business mix, with targeted print and packaging segments gaining share while traditional magazine and large-scale print offerings continue to decline:

Strategic Initiatives

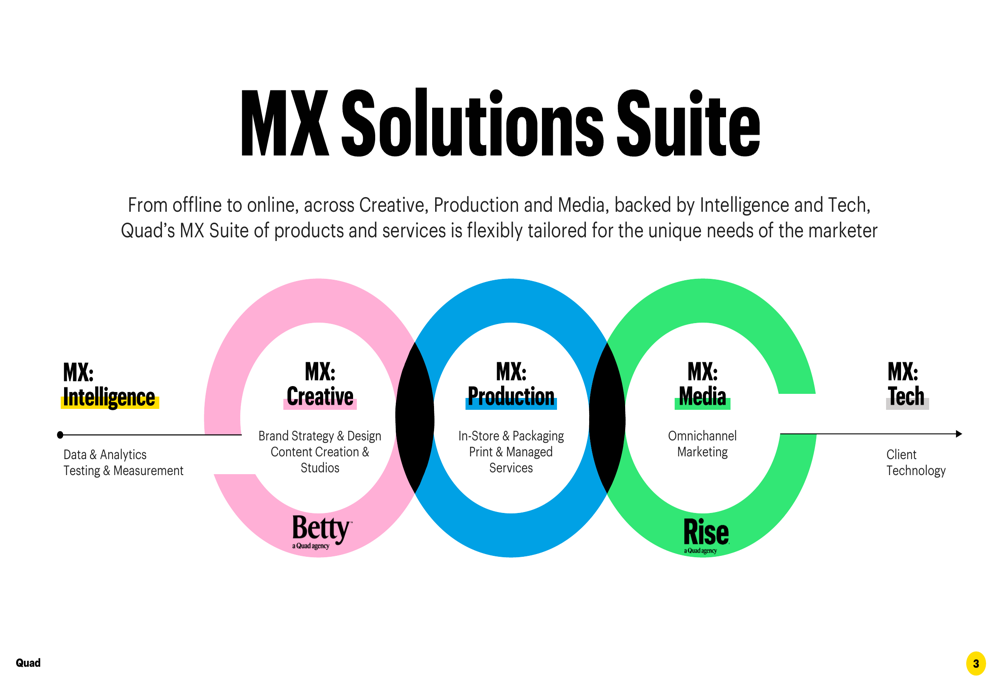

Central to Quad’s transformation is its MX Solutions Suite, which spans five interconnected areas: Creative, Production, Media, Intelligence, and Tech. This integrated approach aims to provide marketers with comprehensive solutions across both offline and online channels.

The company’s MX Solutions Suite is visualized as follows:

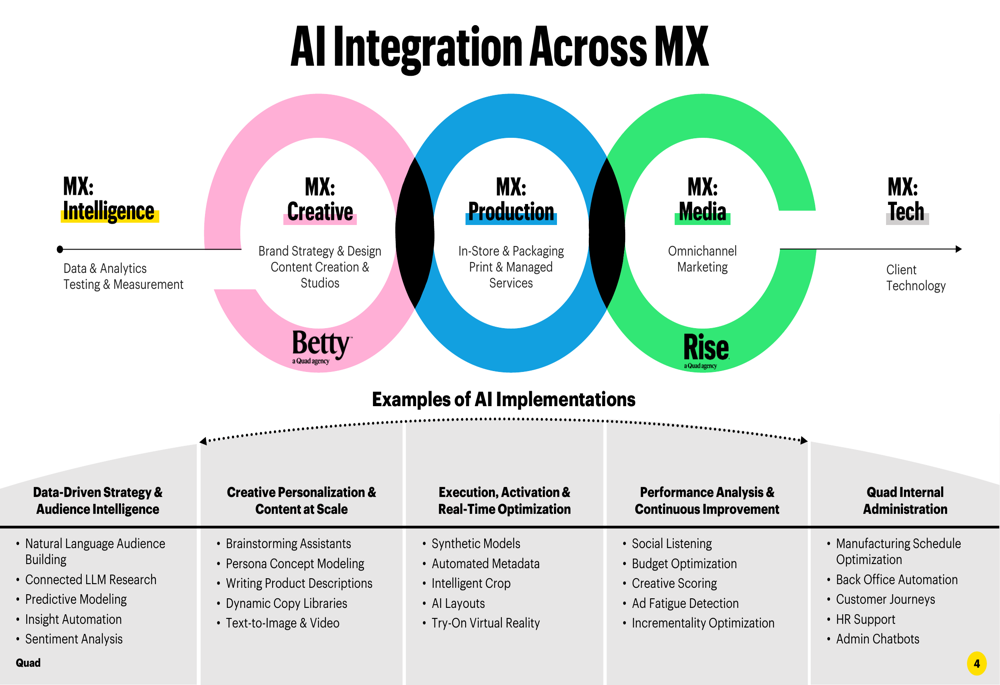

A key differentiator in Quad’s strategy is its integration of artificial intelligence across all aspects of its MX offerings. The company detailed specific AI implementations in each area, from natural language audience building and predictive modeling in Intelligence to brainstorming assistants and text-to-image capabilities in Creative:

Quad is also leveraging its proprietary data capabilities to enhance its marketing solutions. The company highlighted its household-based data stack, which features information on 250 million consumers mapped to physical addresses, reaching 92% of US households with over 3 billion continuously validated data points.

The company’s In-Store Connect retail media solution continues to expand, with new partnerships with regional grocery chains including Vallarta Supermarkets and The Save Mart Companies. This offering demonstrates Quad’s ability to drive brand awareness and product sales in physical retail environments.

Detailed Financial Analysis

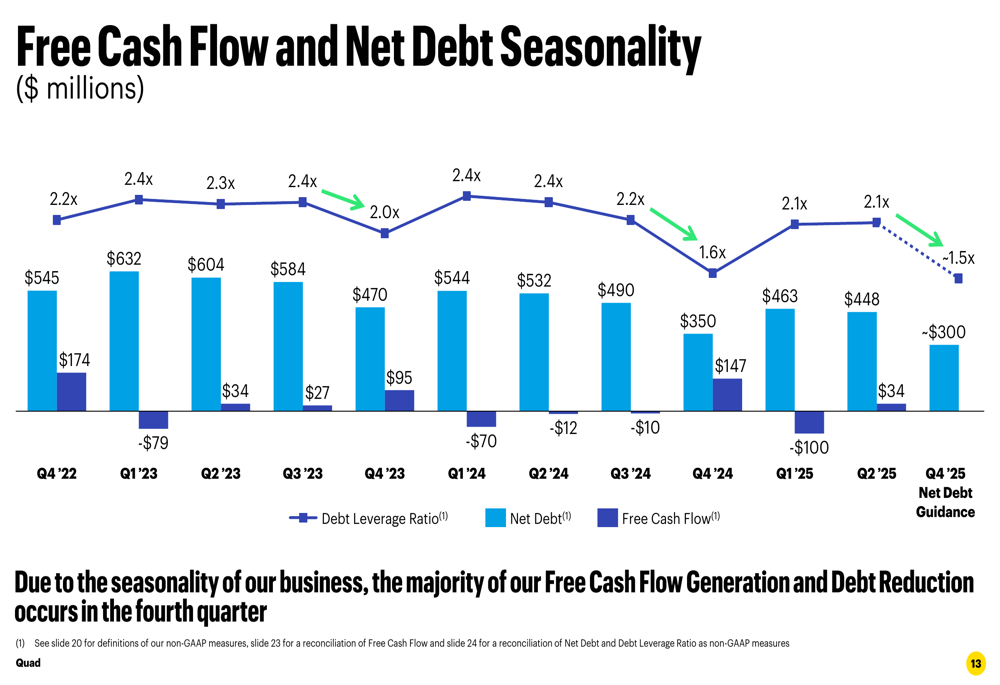

Quad’s financial position shows a seasonal pattern in cash flow and debt levels, with the company typically generating the majority of its free cash flow and achieving debt reduction in the fourth quarter. As of June 30, 2025, Quad reported net debt of $448 million with a debt leverage ratio of 2.13x.

The following chart illustrates this seasonality in the company’s free cash flow and net debt:

The company’s debt capital structure includes a blended interest rate of 7.2%, with 86% of interest expense subject to decreases when interest rates decline. Notably, Quad’s next significant debt maturity is not until October 2029, providing financial flexibility in the near term.

Quad’s capital allocation strategy balances growth investments, shareholder returns, and debt reduction. The company reported returning $15 million to shareholders and repurchasing 1.4 million shares, demonstrating its commitment to shareholder value despite the challenging revenue environment.

Forward-Looking Statements

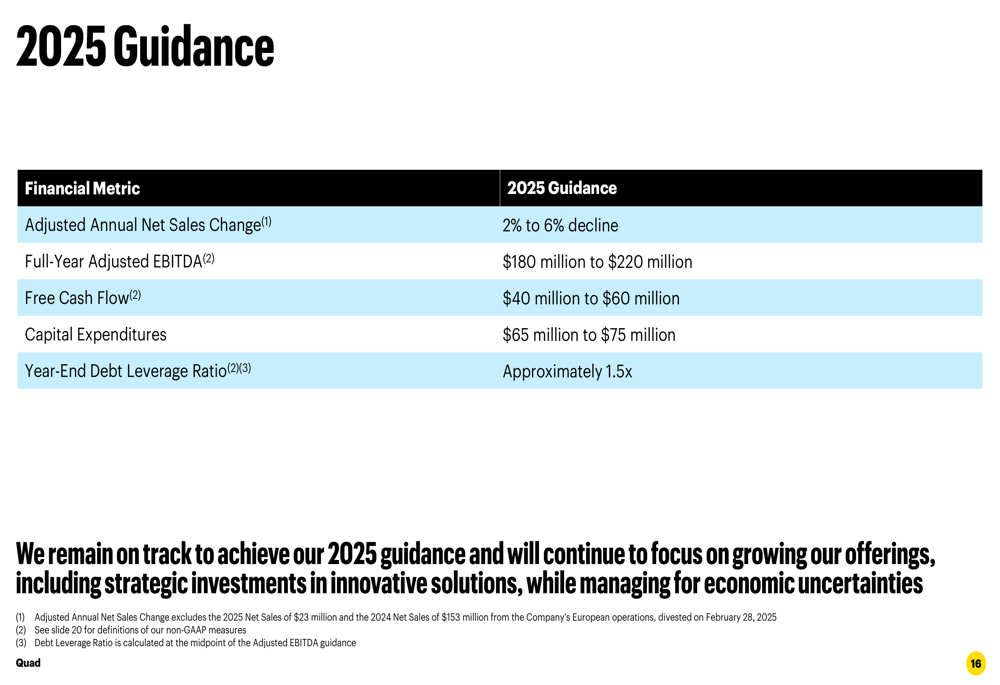

Looking ahead, Quad provided guidance for the full year 2025, projecting an adjusted annual net sales change of -2% to -6% and full-year adjusted EBITDA between $180 million and $220 million. The company expects free cash flow of $40 million to $60 million and capital expenditures between $65 million and $75 million:

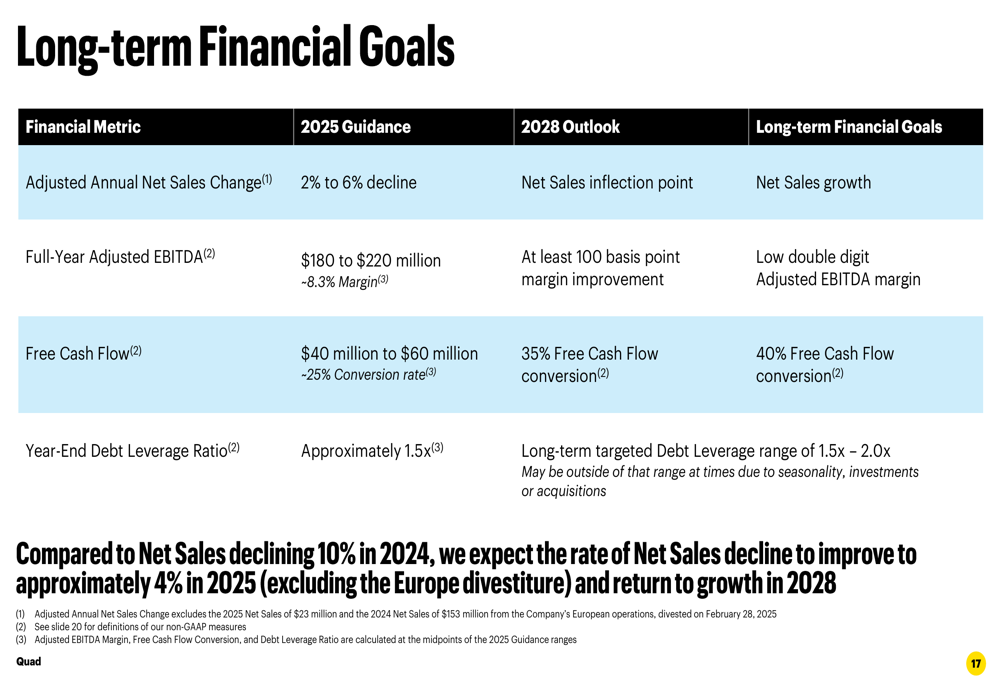

More significantly, Quad outlined its long-term financial goals, including a return to net sales growth by 2028 after reaching an inflection point that year. The company aims to improve its adjusted EBITDA margin by at least 100 basis points by 2028, with a long-term goal of achieving low double-digit margins:

These targets reflect management’s confidence in the company’s strategic transformation, despite current revenue headwinds. The company’s emphasis on data-driven marketing solutions, AI integration, and retail media networks positions it to capitalize on evolving marketing trends while leveraging its traditional print expertise.

Quad’s presentation reinforces its commitment to balancing innovation with operational efficiency as it navigates the challenging print industry landscape. While revenue declines persist, the improvement in earnings per share and free cash flow suggests the company’s transformation strategy may be gaining traction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.