US stock futures steady with China trade talks, Q3 earnings in focus

Introduction & Market Context

Quadient SA (EURONEXT:QDT) presented its Q1 2025 financial results on June 3, 2025, revealing a mixed performance across its business segments. The company reported total revenue of €258 million, representing a slight decline of 1.1% on a reported basis compared to the same period last year. Despite this overall decrease, Quadient maintained its full-year guidance, citing expectations for stronger performance in the second half of the year.

The company’s stock closed at €17.04 on the day of the presentation, down 0.94% and trading well below its 52-week high of €23.10, reflecting ongoing investor caution about the company’s transition from its traditional mail business to digital solutions and parcel lockers.

Quarterly Performance Highlights

Quadient’s Q1 2025 performance showed significant variation across its three main business segments. While the Digital and Lockers segments demonstrated robust growth, the Mail segment experienced a notable decline, impacting the overall results.

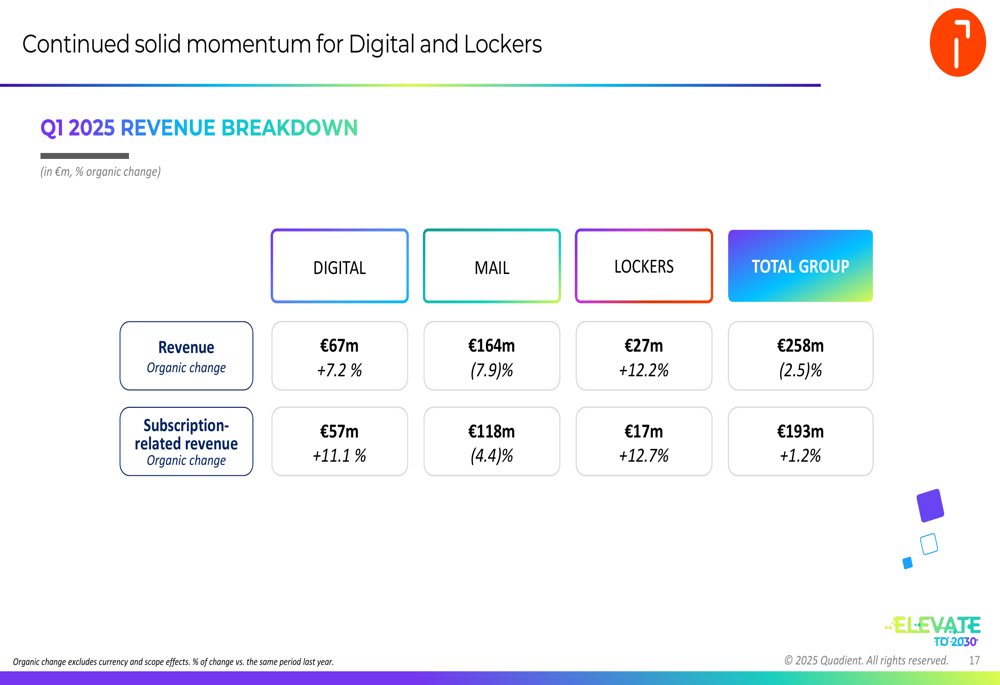

As shown in the following comprehensive revenue breakdown:

The Digital segment generated €67 million in revenue, achieving 7.2% organic growth compared to Q1 2024. The Mail segment, which still represents the largest portion of Quadient’s business at €164 million, saw a 7.9% organic decline. Meanwhile, the Lockers segment continued its strong momentum with €27 million in revenue, representing impressive 12.2% organic growth.

Geographically, North America remains Quadient’s largest market, accounting for 58% of total revenue, though it experienced a 2.4% organic decline. Main European countries and International markets, representing 33% and 9% of revenue respectively, also saw organic declines of 2.8% and 2.0%.

Segment Performance Analysis

Digital Business

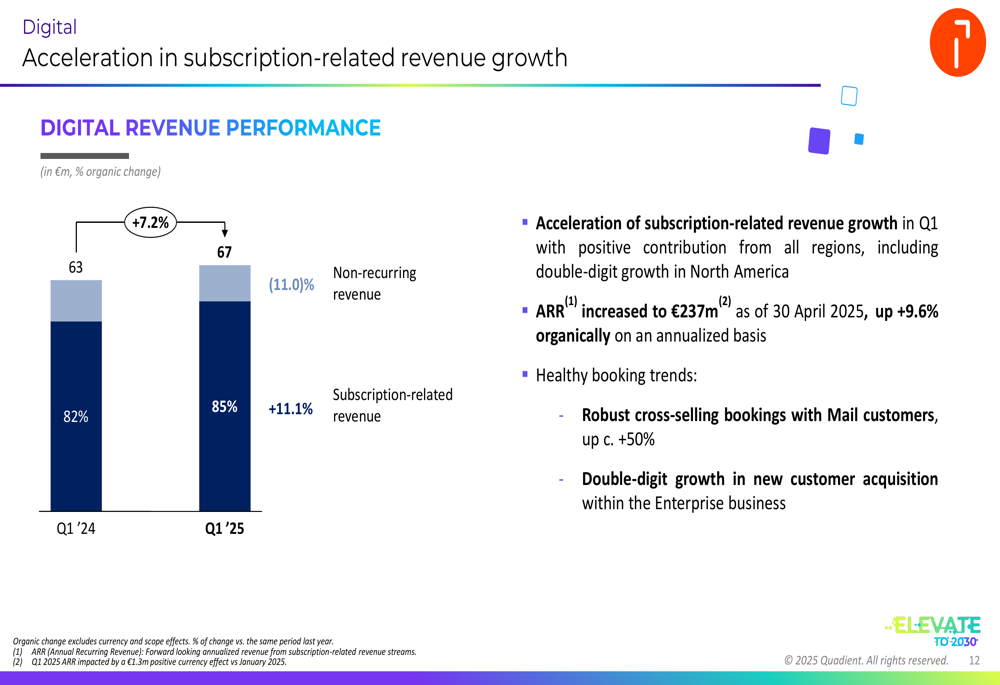

Quadient’s Digital segment continued its strong performance trajectory, bolstered by industry recognition and growing subscription revenue. The company strengthened its global cloud payment capabilities through integration with Nuvei (TSX:NVEI)’s payment technology and received leadership positions in multiple analyst reports, including the 2025 SPARK Matrix for Accounts Receivable and CCM.

The acceleration in subscription-related revenue was particularly noteworthy, as illustrated in this chart:

Annual Recurring Revenue (ARR) increased to €237 million as of April 30, 2025, representing a 9.6% organic increase on an annualized basis. SaaS customers now account for 84.6% of total Digital customers, highlighting the successful transition to a cloud-based business model. Booking (NASDAQ:BKNG) trends showed robust cross-selling with Mail customers (up approximately 50%) and double-digit growth in new customer acquisition within the Enterprise business.

Mail Business

The Mail segment faced significant challenges in Q1 2025, with hardware sales down 15.8% across all regions. This decline was attributed to the "echo effect" of the COVID period and a strong comparison base in Q1 2024, particularly in the US market.

Despite these headwinds, Quadient emphasized that it continues to outperform the broader mail market. The company noted that 44% of its installed base has been upgraded to new technology, and highlighted commercial momentum with double-digit growth in cross-selling to Lockers and a 50% increase in Digital order intake during the quarter.

Management expects Mail performance to improve in the coming quarters, citing a stronger portfolio of contracts up for renewal during the remainder of the year.

Lockers Business

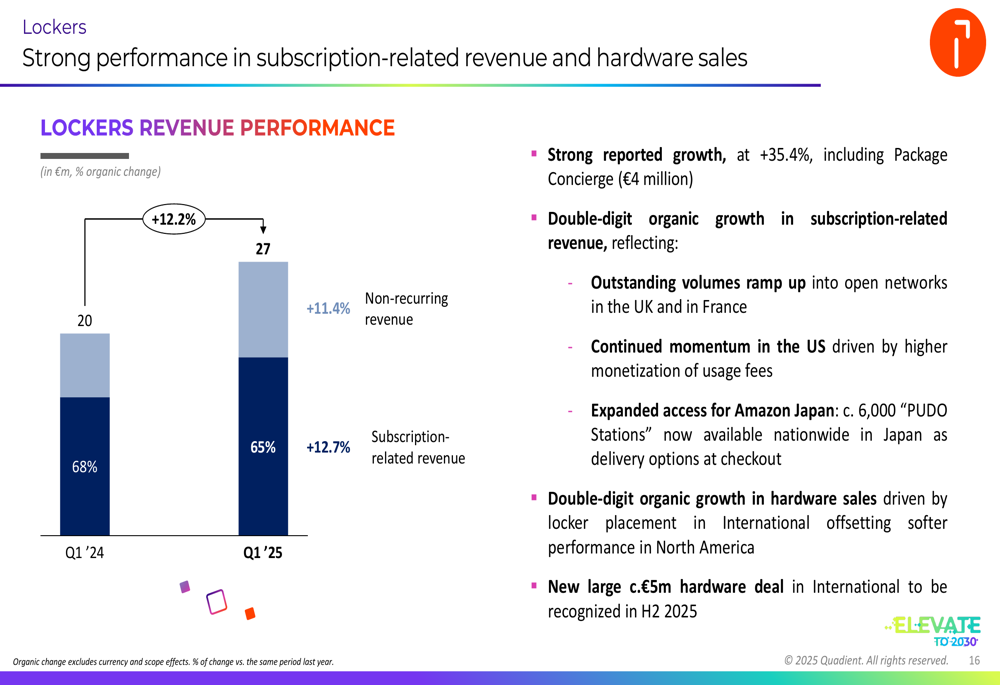

The Lockers segment emerged as the standout performer in Q1 2025, as demonstrated by these impressive results:

The segment achieved 35.4% reported growth, including a €4 million contribution from the recently acquired Package Concierge. Organic growth reached 12.2%, driven by double-digit increases in both subscription-related revenue and hardware sales. The company secured a new large hardware deal worth approximately €5 million during the quarter.

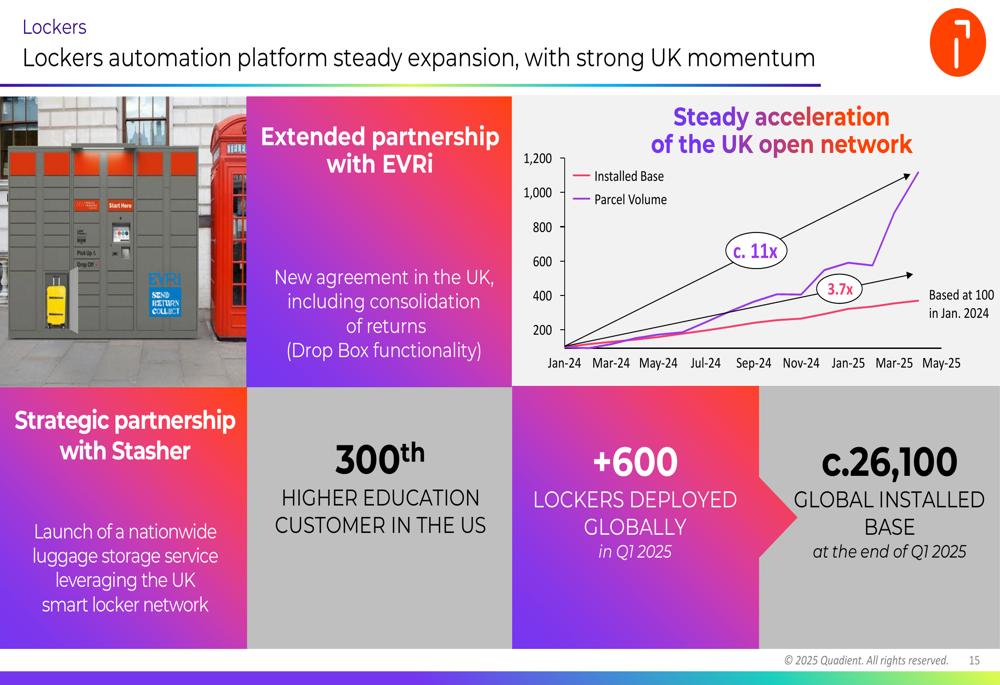

Quadient continued to expand its locker network, deploying 600 additional units globally in Q1 2025, bringing its total installed base to approximately 26,100 lockers. The company extended its partnership with EVRİ to include consolidation of returns through Drop Box functionality and formed a strategic partnership with Stasher to launch a nationwide luggage storage service.

Strategic Initiatives and Acquisitions

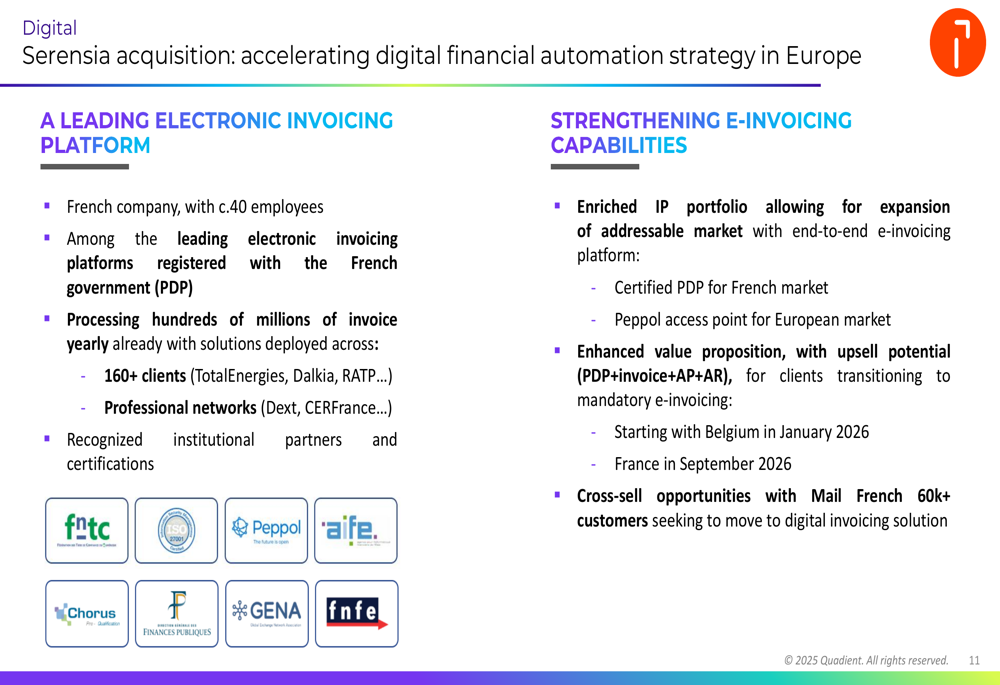

Quadient made strategic moves during Q1 2025 to strengthen its market position, particularly in the digital financial automation space. The company acquired Serensia, a leading electronic invoicing platform in France with approximately 40 employees, to enhance its e-invoicing capabilities ahead of regulatory changes in the European market.

This acquisition enriches Quadient’s IP portfolio and creates cross-selling opportunities with its 60,000+ Mail customers in France. The move aligns with Quadient’s strategy to expand its digital offerings and capitalize on the growing demand for automated financial processes.

The company’s shareholding structure also saw significant changes during the quarter, with VESA Equity Investment increasing its stake to 22.6% and Teleios fully exiting the shareholder base. As of April 4, 2025, other major shareholders include Bpifrance Participations (8.1%) and Janus Henderson Investors UK (5.2%).

Forward-Looking Statements

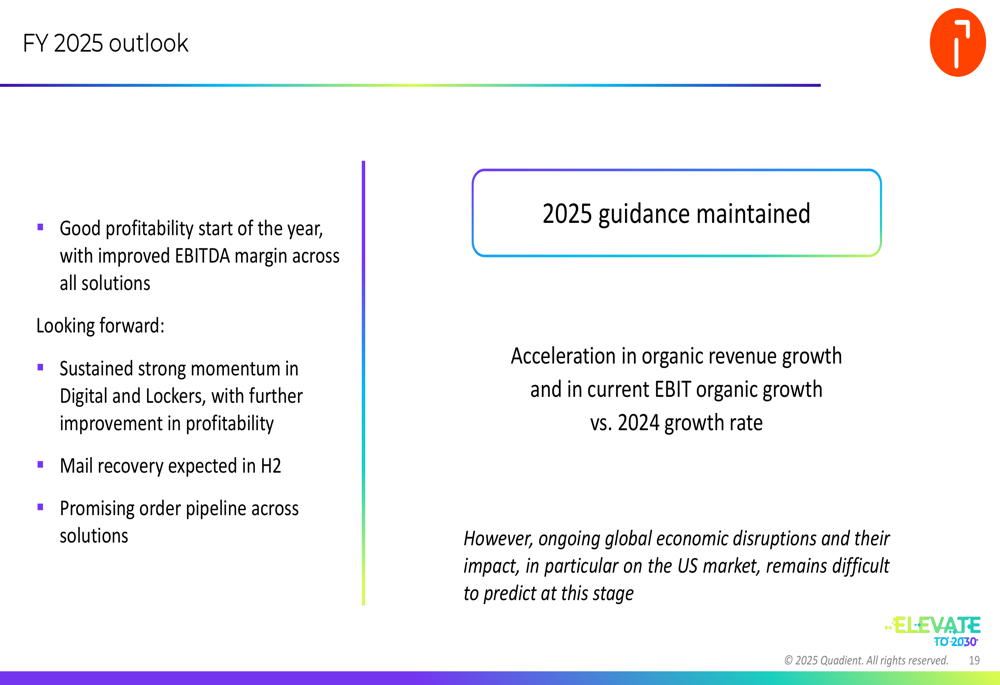

Despite the mixed Q1 results, Quadient maintained its full-year 2025 guidance, projecting an acceleration in both organic revenue growth and current EBIT organic growth compared to 2024. The company cited a good profitability start to the year with improved EBITDA margins across all solutions.

Looking further ahead, Quadient outlined its long-term ambitions for 2026 and 2030. For the Digital segment, the company targets approximately 10% revenue organic CAGR through 2026, with an EBITDA margin exceeding 20%. By 2030, Digital revenue is expected to exceed €500 million with subscription-related revenue comprising over 90% and an EBITDA margin of approximately 30%.

The Mail segment is projected to decline at approximately 3% revenue organic CAGR through 2026, while maintaining an EBITDA margin above 25%. By 2030, Mail revenue is expected to be around €600 million with subscription-related revenue exceeding 65% and an EBITDA margin between 20-25%.

For the Lockers segment, Quadient targets over 10% revenue organic CAGR through 2026, with an EBITDA margin exceeding 10%. By 2030, Lockers revenue is expected to surpass €200 million with an installed base of over 40,000 units and an EBITDA margin of approximately 20%.

Management expressed confidence in the company’s trajectory, highlighting the expected Mail recovery in the second half of 2025, continued momentum in Digital and Lockers segments, and a promising order pipeline to support the full-year outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.