TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Qualcomm Incorporated (NASDAQ:QCOM) reported record financial results for its first quarter of fiscal 2025, with strong performance across all business segments. Despite exceeding analyst expectations, the company’s stock fell approximately 4.62% in aftermarket trading, likely due to weaker-than-expected guidance for the second quarter.

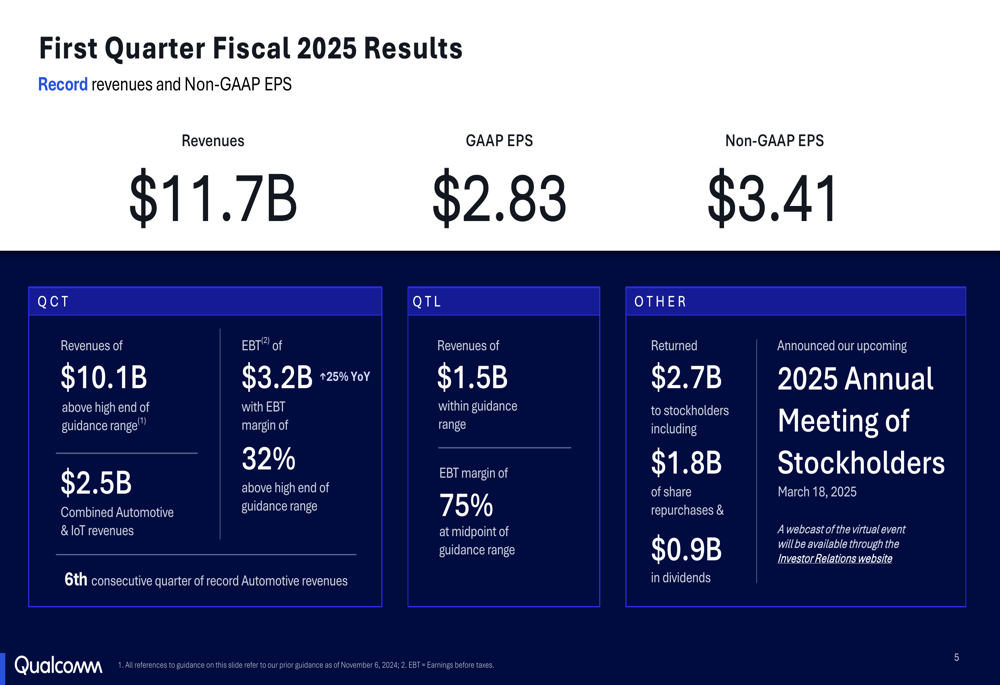

The chipmaker delivered non-GAAP revenues of $11.7 billion, up 18% year-over-year, and non-GAAP earnings per share of $3.41, representing a 24% increase from the same period last year. Both figures surpassed the high end of the company’s guidance range.

Quarterly Performance Highlights

Qualcomm’s presentation highlighted exceptional performance across its business segments, with particularly strong results in its QCT (Qualcomm CDMA Technologies) division, which achieved record revenues of $10.1 billion.

As shown in the following financial summary slide, the company saw growth across all its key business segments compared to the same quarter last year:

Handset revenues, which remain Qualcomm’s largest business segment, increased 13% year-over-year to $7.57 billion. However, the most impressive growth came from the automotive segment, which surged 61% to $961 million, marking the sixth consecutive quarter of record revenues in this category. The IoT (Internet of Things) segment also performed well, with revenues increasing 36% to $1.55 billion.

The company’s QTL (Qualcomm Technology Licensing) segment generated revenues of $1.53 billion, up 5% year-over-year, with an EBT margin of 75%. Qualcomm also reported finalizing renewal negotiations for long-term licenses with two key Chinese OEMs and signing a long-term 4G license to Transsion.

The following slide provides a comprehensive overview of Qualcomm’s first quarter fiscal 2025 results:

Qualcomm’s financial discipline was also evident in its shareholder returns, with the company returning $2.7 billion to stockholders during the quarter, including $1.8 billion in share repurchases and $0.9 billion in dividends.

Strategic Initiatives

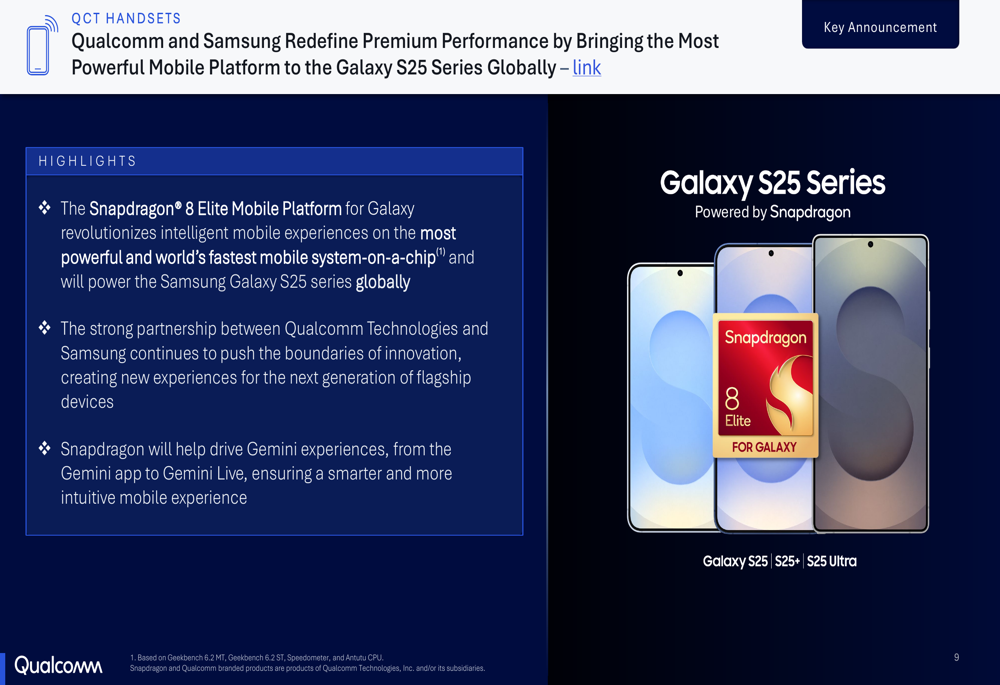

During the quarter, Qualcomm announced several strategic partnerships and product launches that position the company for future growth. One of the most significant announcements was the adoption of the Snapdragon 8 Elite Mobile Platform in Samsung (KS:005930)’s Galaxy S25 series globally.

As illustrated in the following slide, this partnership represents a continuation of Qualcomm’s strong relationship with Samsung and highlights the company’s leadership in premium mobile processors:

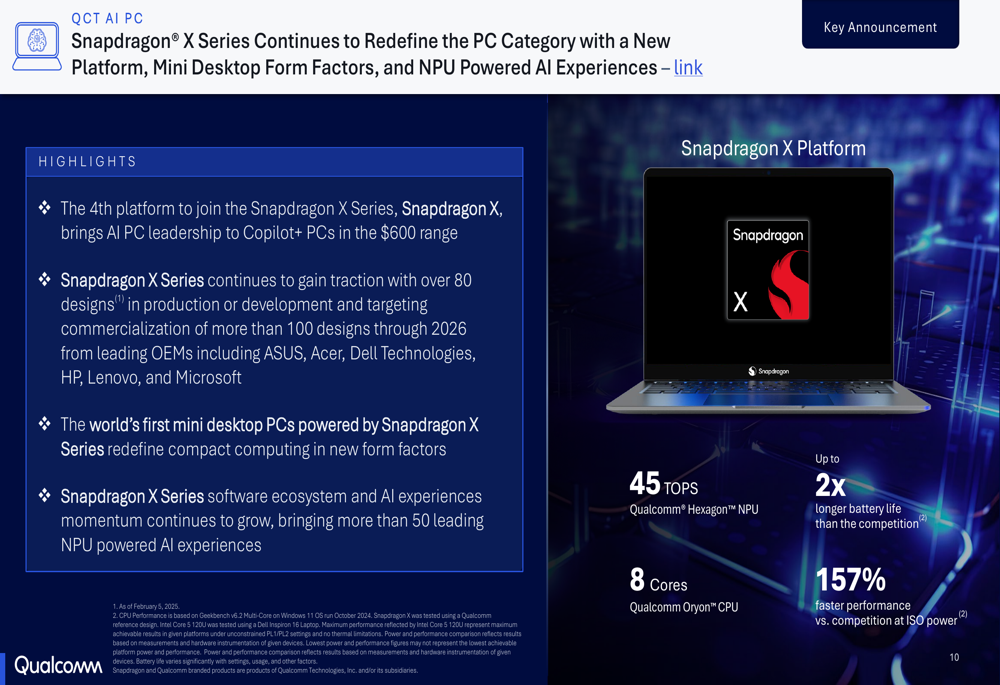

In the computing space, Qualcomm is expanding its Snapdragon X Series for PCs, with over 80 designs currently in production or development. The company is targeting commercialization of more than 100 designs through 2026 from leading OEMs including ASUS, Acer (TW:2353), Dell Technologies (NYSE:DELL), HP (NYSE:HPQ), Lenovo, and Microsoft (NASDAQ:MSFT).

The following slide details Qualcomm’s progress in the PC market:

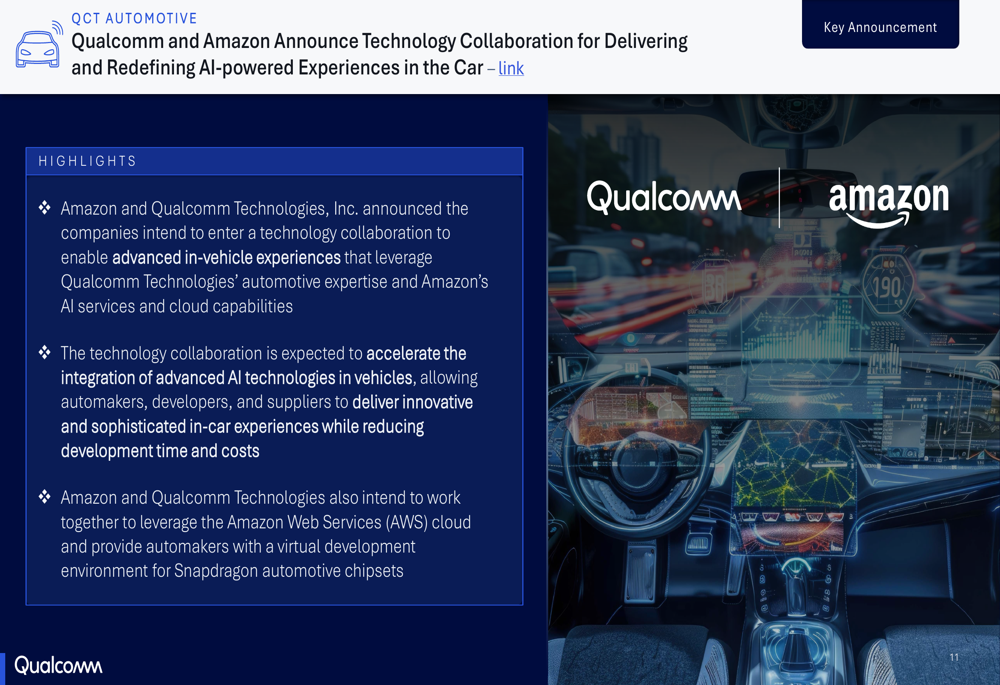

Qualcomm is also strengthening its position in the automotive sector through a collaboration with Amazon (NASDAQ:AMZN) to deliver AI-powered experiences in vehicles. This partnership aims to accelerate the integration of advanced AI technologies in vehicles while reducing development time and costs for automakers.

The company’s focus on AI extends beyond automotive applications, as Qualcomm positions itself to benefit from the broader AI innovation cycle. The company highlighted that AI models are becoming more capable and efficient, enabling on-device AI experiences.

Forward-Looking Statements

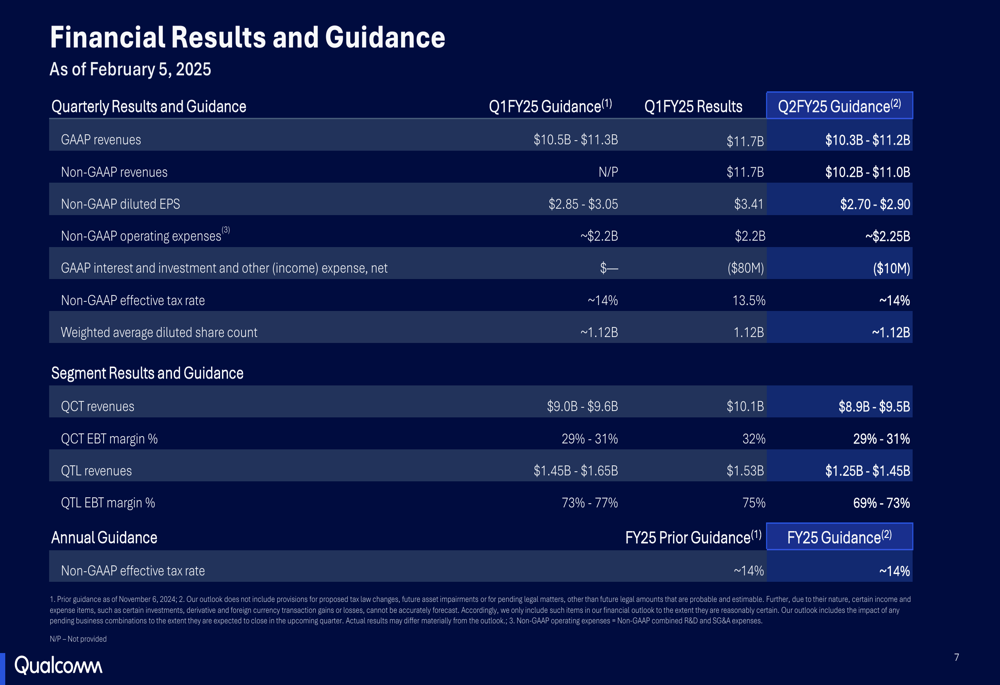

Despite the strong Q1 performance, Qualcomm’s guidance for the second quarter of fiscal 2025 suggests a sequential decline, which likely contributed to the negative market reaction. The company expects Q2 non-GAAP revenues between $10.2 billion and $11.0 billion, and non-GAAP EPS between $2.70 and $2.90.

The following slide compares Q1 results with Q2 guidance:

For the QCT segment, Qualcomm projects Q2 revenues between $8.9 billion and $9.5 billion, with an EBT margin of 29-31%. QTL revenues are expected to be between $1.25 billion and $1.45 billion, with an EBT margin of 69-73%.

Analyst Perspectives

During the earnings call, analysts inquired about potential subsidies in the China smartphone market, Qualcomm’s modem business expectations, and the sustainability of gross margins. The company addressed these concerns by emphasizing its strategic focus on innovation and market expansion.

According to CEO Cristiano Amon, "We are off to a great start in fiscal ’twenty five," highlighting the company’s robust performance and strategic initiatives. CFO Akash Palkhiwala noted, "The primary driver here is that there is a consumer demand for more capable smartphones," underscoring Qualcomm’s strong position in the premium smartphone market.

Despite the positive Q1 results, investors appear concerned about the sequential decline in Q2 guidance and potential challenges ahead. According to available data, Qualcomm’s stock closed at $146.88 on April 30, 2025, before falling to approximately $141.60 in aftermarket trading.

The market reaction suggests that while Qualcomm delivered impressive year-over-year growth in Q1, investors may be concerned about the sustainability of this growth trajectory, particularly given the sequential decline projected for Q2. Nevertheless, the company’s diversification beyond handsets, with strong growth in automotive and IoT segments, along with its strategic positioning in AI, provides multiple avenues for long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.