Can anything shut down the Gold rally?

Introduction & Market Context

Qualitas Controladora (BMV:Q), Mexico’s leading auto insurer, presented its second quarter 2025 earnings results on July 21, highlighting continued premium growth and strong profitability metrics. The company’s stock has risen 1.43% following the presentation, trading at 172.96 pesos, building on the positive momentum seen after its strong Q1 results when the stock surged 13.7%.

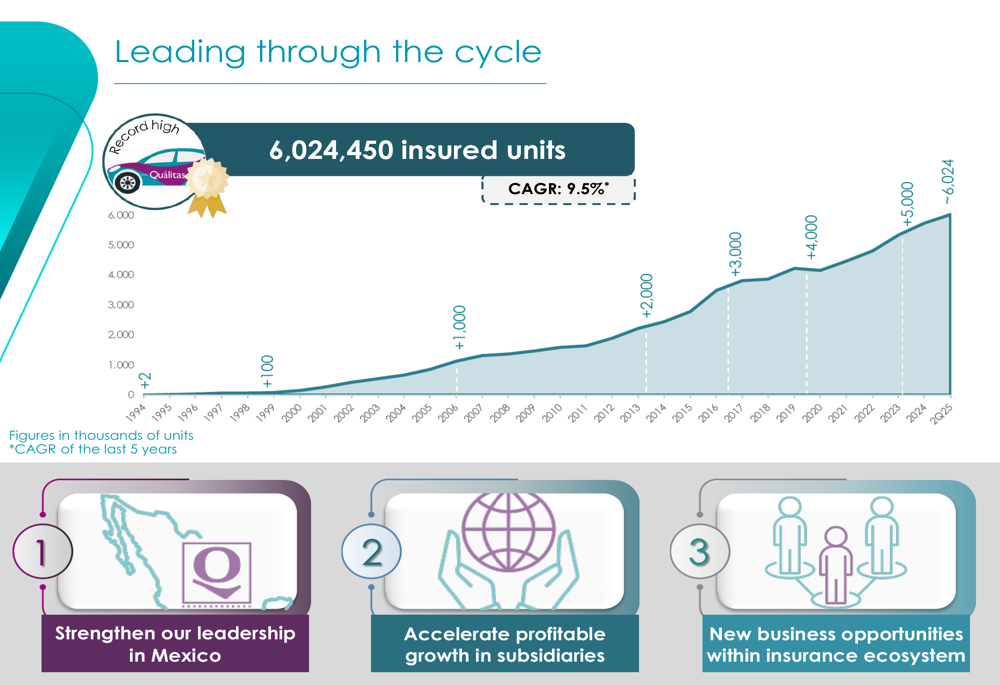

The Q2 results demonstrate Qualitas’ ability to maintain growth trajectory despite cautious macroeconomic projections. The company continues to execute on its three-pillar strategy: strengthening leadership in Mexico, accelerating profitable growth in subsidiaries, and exploring new business opportunities within the insurance ecosystem.

Quarterly Performance Highlights

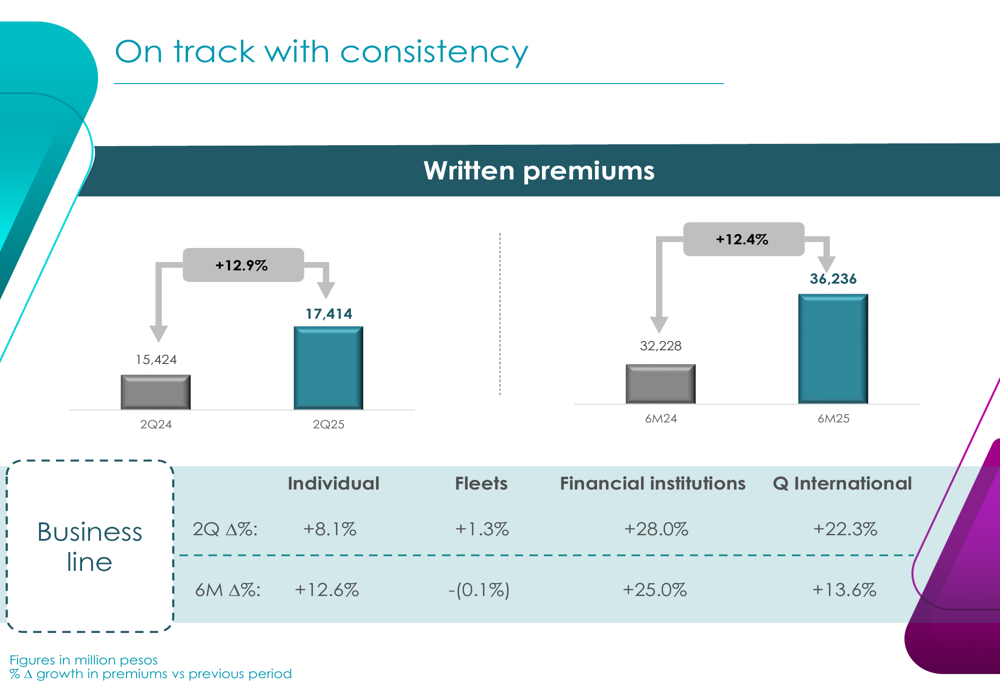

Qualitas reported written premiums of 17,414 million pesos in Q2 2025, representing a 12.9% increase compared to the same period last year. For the first half of 2025, written premiums reached 36,236 million pesos, up 12.4% year-over-year, showing consistent growth in line with the 12% increase reported in Q1.

As shown in the following chart of written premiums by business segment:

The Financial Institutions segment led growth with a 28.0% increase in Q2 and 25.0% for the first half of 2025. Individual policies grew by 8.1% in Q2 and 12.6% for the half-year, while the Fleet segment showed modest growth of 1.3% in Q2 but a slight contraction of 0.1% for the six-month period.

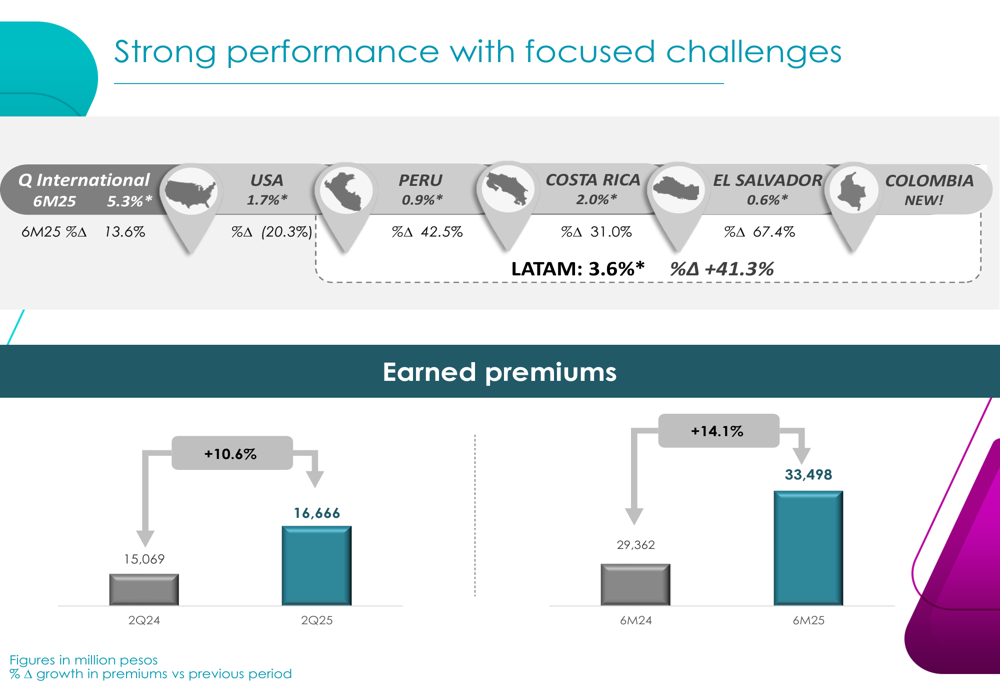

Earned premiums, which represent the portion of written premiums that are recognized as revenue during the period, grew by 10.6% to 16,666 million pesos in Q2 and by 14.1% to 33,498 million pesos for the first half of 2025.

The company’s international operations demonstrated strong performance, as illustrated in this breakdown:

Detailed Financial Analysis

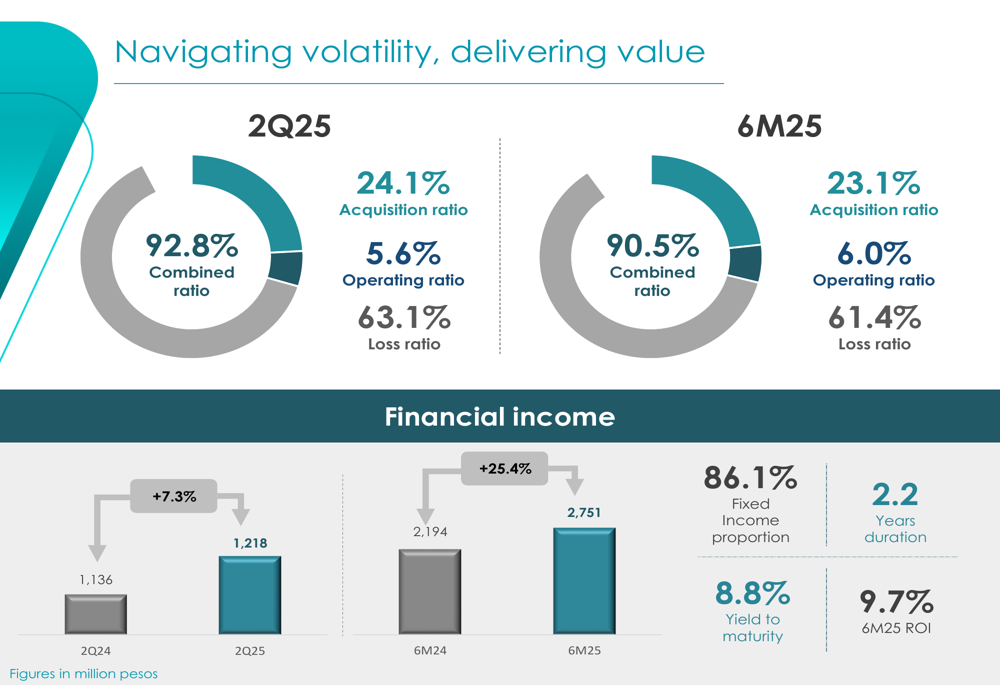

Qualitas maintained strong underwriting profitability with a combined ratio of 92.8% in Q2 2025 and 90.5% for the first half of the year. The combined ratio, a key metric in the insurance industry, measures the sum of loss ratio, acquisition ratio, and operating ratio, with figures below 100% indicating underwriting profit.

The following chart details the components of the combined ratio and financial income:

The company’s loss ratio stood at 63.1% for Q2 and 61.4% for the first half, while acquisition costs represented 24.1% and 23.1% of earned premiums, respectively. Operating expenses accounted for 5.6% in Q2 and 6.0% for the six-month period.

Financial income grew by 7.3% to 1,218 million pesos in Q2 2025 and by an impressive 25.4% to 2,751 million pesos for the first half of the year. The investment portfolio maintains a conservative approach with 86.1% allocated to fixed income instruments, an average duration of 2.2 years, and a yield to maturity of 8.8%. The return on investment for the first half of 2025 reached 9.7%.

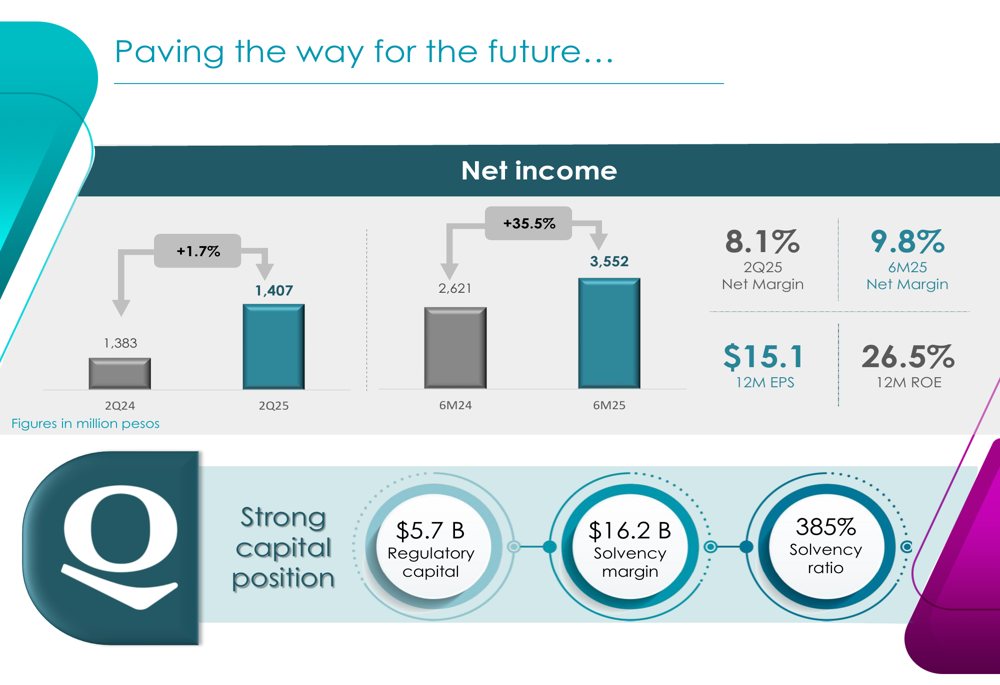

Net income showed modest growth of 1.7% in Q2 2025, reaching 1,407 million pesos, but demonstrated substantial growth of 35.5% for the first half of the year at 3,552 million pesos. This performance is consistent with the strong Q1 results reported earlier, which showed the second-highest quarterly net income in the company’s history.

The company’s profitability metrics and capital position are illustrated in this chart:

International Expansion Strategy

Qualitas continues to execute its international growth strategy, with operations now spanning five countries outside Mexico. The company recently entered the Colombian market, adding to its existing presence in the United States, Peru, Costa Rica, and El Salvador.

The Latin American operations collectively grew by 41.3%, demonstrating the success of the company’s regional expansion efforts. This international diversification represents a key component of Qualitas’ second strategic pillar focused on accelerating profitable growth in subsidiaries.

As shown in the following long-term growth chart, Qualitas has expanded its insured units from approximately 2,000 in 1994 to over 6 million in 2025, achieving a compound annual growth rate of 9.5% over the last five years:

Capital Position and Outlook

Qualitas maintains a robust capital position with 5.7 billion pesos in regulatory capital, 16.2 billion pesos in solvency margin, and a solvency ratio of 385%. This represents an improvement from the 362% solvency ratio reported in Q1 2025, providing the company with substantial financial flexibility to pursue its strategic initiatives.

The 12-month return on equity (ROE) stands at 26.5%, up from 24.2% reported after Q1, indicating improved capital efficiency. The 12-month earnings per share reached 15.1 pesos, with net margins of 8.1% for Q2 and 9.8% for the first half of 2025.

While the presentation did not provide specific forward guidance, the consistent execution of the company’s three-pillar strategy and the strong financial results suggest Qualitas is well-positioned to continue its growth trajectory. The company’s focus on strengthening its leadership in Mexico while expanding internationally and exploring new business opportunities within the insurance ecosystem provides multiple avenues for future growth.

The stock currently trades at 172.96 pesos, significantly above its 52-week low of 130.01 pesos but still below its 52-week high of 237.18 pesos, potentially indicating room for further appreciation if the company continues to deliver strong results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.