Figma Shares Indicated To Open $105/$110

QVC Group Inc. (NASDAQ:QVCGA) shares plunged over 21% in aftermarket trading following the release of its Q1 2025 earnings presentation on May 7, which revealed accelerating revenue declines and significant margin compression across all business segments.

Quarterly Performance Highlights

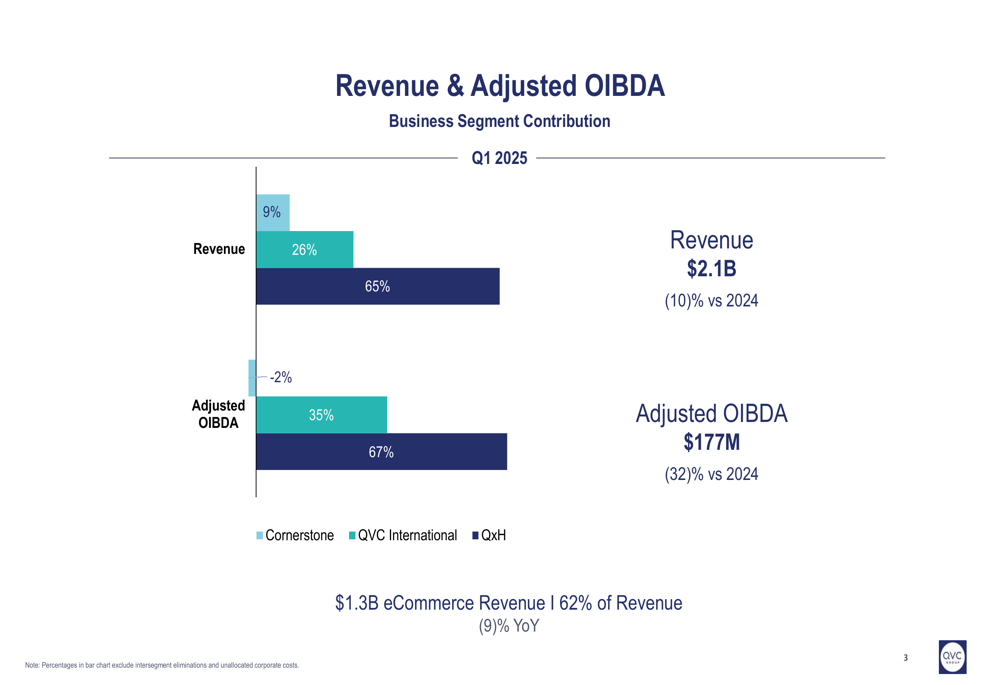

The home shopping and e-commerce retailer reported total revenue of $2.1 billion for the first quarter, representing a 10% year-over-year decline. This marks a deterioration from the 6% revenue drop reported in Q4 2024. More concerning was the 32% decrease in adjusted OIBDA (Operating Income Before Depreciation and Amortization), which fell to $177 million.

As shown in the following revenue and adjusted OIBDA breakdown by business segment:

The company’s largest segment, QxH (comprising QVC and HSN in the US), which accounts for 65% of total revenue, experienced an 11% revenue decline. QVC International fared slightly better with a 6% decrease, while Cornerstone saw the steepest drop at 13%. E-commerce revenue, representing 62% of total sales at $1.3 billion, declined 9% year-over-year.

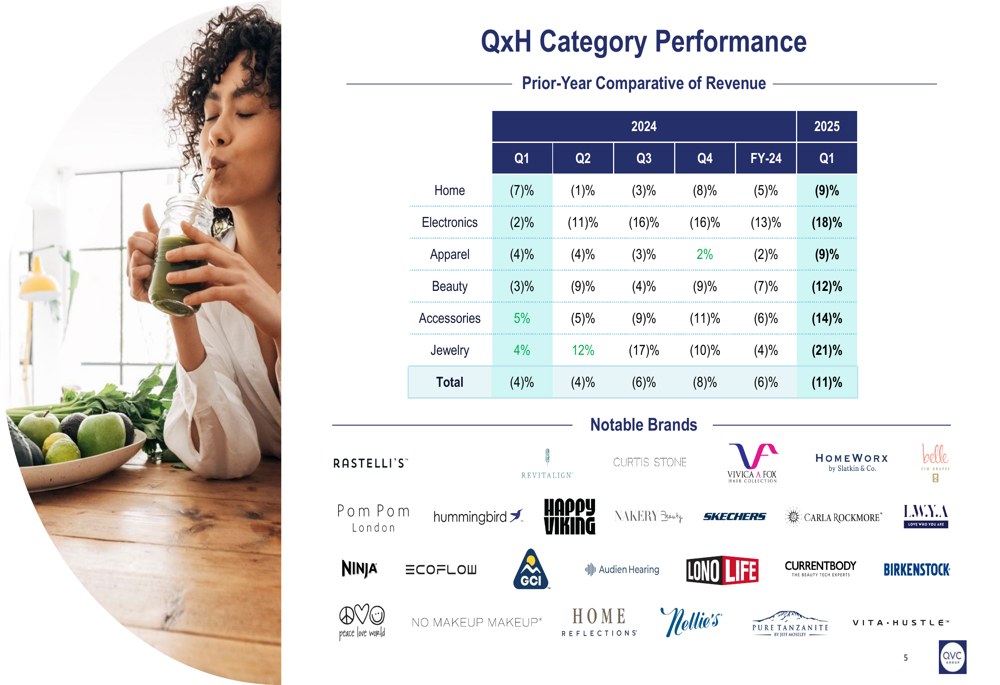

The company’s performance deteriorated across all product categories, with particularly steep declines in high-margin segments:

Detailed Financial Analysis

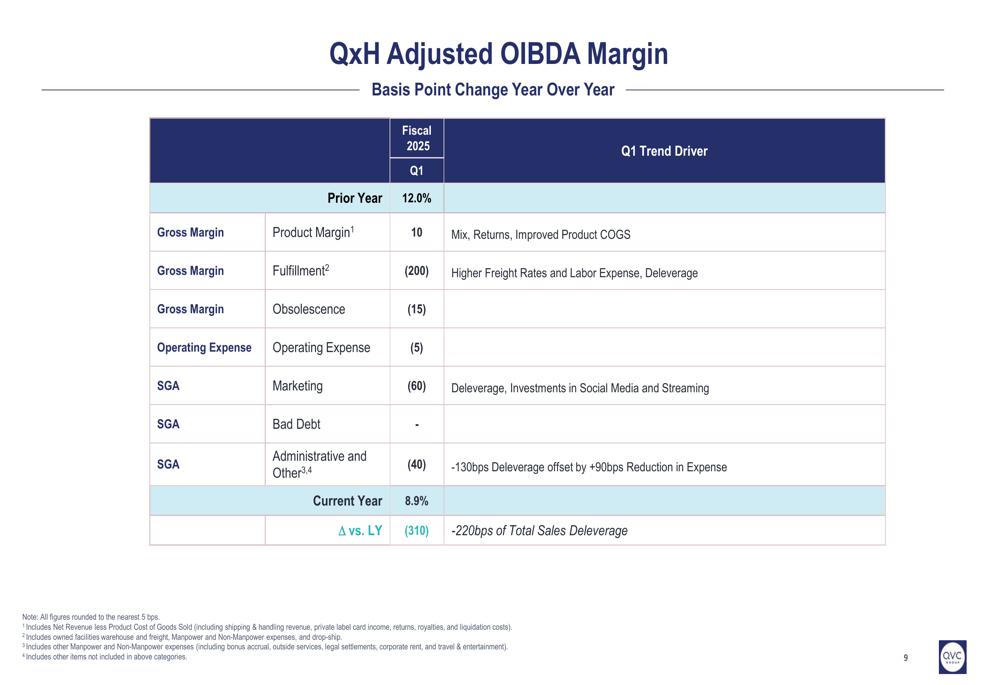

QVC’s adjusted OIBDA margin for its core QxH segment contracted significantly, falling from 12.0% in Q1 2024 to 8.9% in Q1 2025. The 310 basis point decline was primarily attributed to sales deleverage (220 bps) and fulfillment challenges (200 bps), partially offset by modest improvements in product margin and administrative expenses.

The following chart details the factors contributing to margin compression:

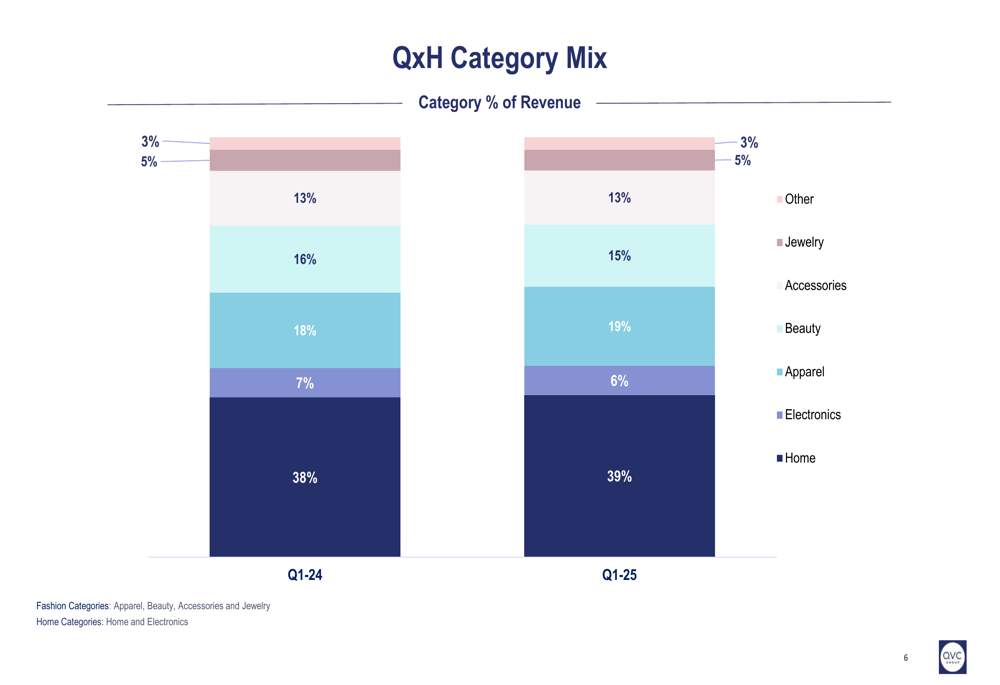

The company’s product category mix showed subtle shifts year-over-year, with Home and Apparel slightly increasing their share of revenue, while Beauty decreased from 18% to 15% of total sales:

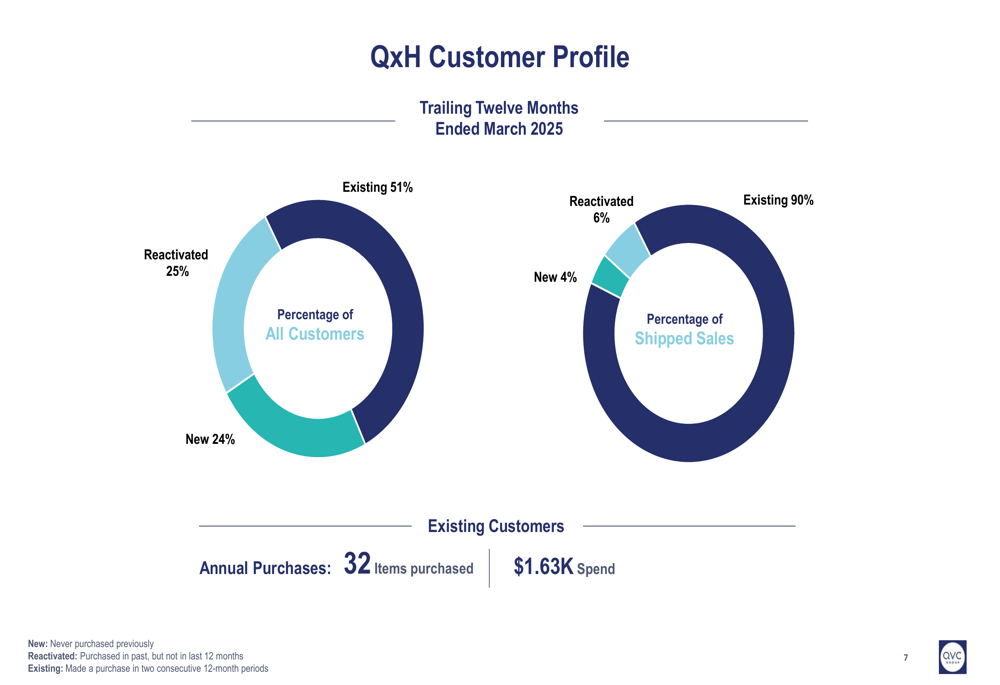

QVC’s customer profile analysis revealed that existing customers continue to drive the vast majority of revenue. While existing customers represent 51% of the total customer base, they account for 90% of shipped sales, spending an average of $1,630 annually across 32 items:

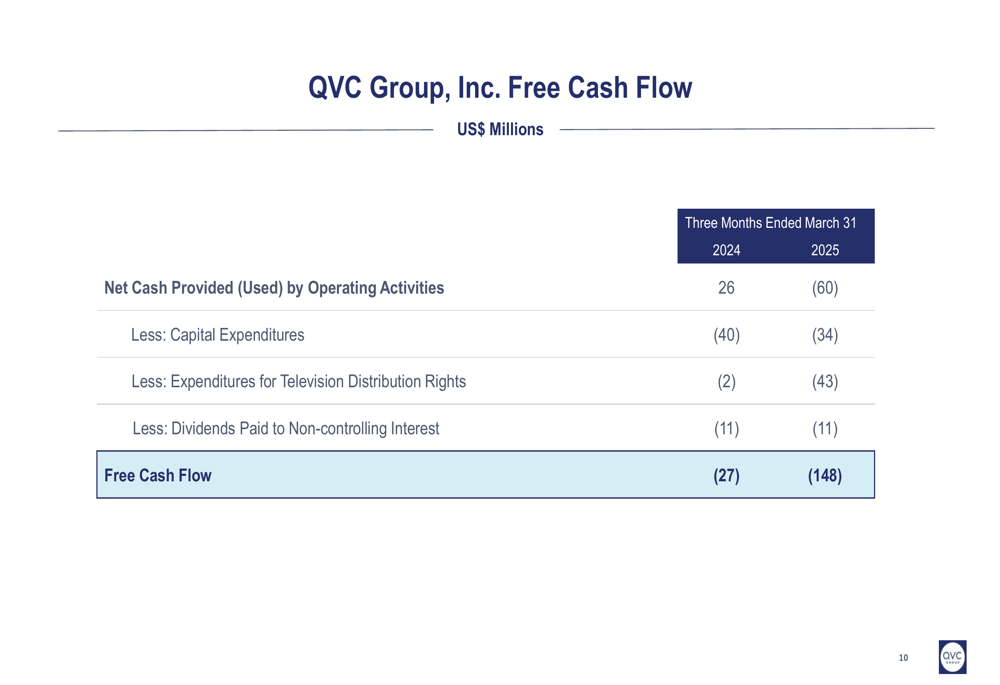

Free cash flow deteriorated significantly, with the company reporting negative $148 million for Q1 2025 compared to negative $27 million in the same period last year. The decline was driven by a $60 million cash outflow from operating activities and increased expenditures for television distribution rights:

Forward-Looking Statements

Despite the challenging results, QVC Group maintained compliance with its debt covenants. The company reported a leverage ratio of 3.7x as of March 31, 2025, below the 4.5x covenant requirement for its credit facility. However, the company noted that its consolidated leverage ratio exceeded the 3.5x threshold for the restricted payment test under its bond indentures.

The presentation did not include specific forward guidance, in contrast to the Q4 2024 earnings call where management had characterized 2025 as a "transition year" focused on accelerating revenue from social and streaming platforms. The previous call had targeted a $100 million OIBDA improvement by year-end and double-digit OIBDA margins.

The stock’s sharp decline in aftermarket trading, falling to $0.15 per share, reflects investor concerns about the accelerating revenue decline and profitability challenges. This represents a significant deterioration from the previous close of $0.24 and continues the downward trend that has seen the stock lose over 70% of its value in the past year.

While the company continues to maintain a strong existing customer base with high annual spend, the persistent decline across all business segments and product categories suggests QVC Group faces significant headwinds in reversing its negative trajectory in the competitive retail landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.