Palantir launches Chain Reaction AI infrastructure platform with CenterPoint and NVIDIA

Introduction & Market Context

Rai Way SpA (BIT:RWAY) presented its first half 2025 results on July 31, showing improved performance compared to its Q1 results released earlier this year. The Italian broadcast infrastructure company reported growth in both its traditional media distribution business and emerging digital infrastructure segments, with management raising full-year guidance based on the strong performance.

The company’s stock closed at €5.84 on the day of the presentation, representing a modest 0.17% increase, as investors assessed the company’s progress in both core operations and diversification initiatives. The results mark a notable improvement from Q1 2025, when the company reported a 5.3% decline in net income despite revenue growth.

Financial Performance Highlights

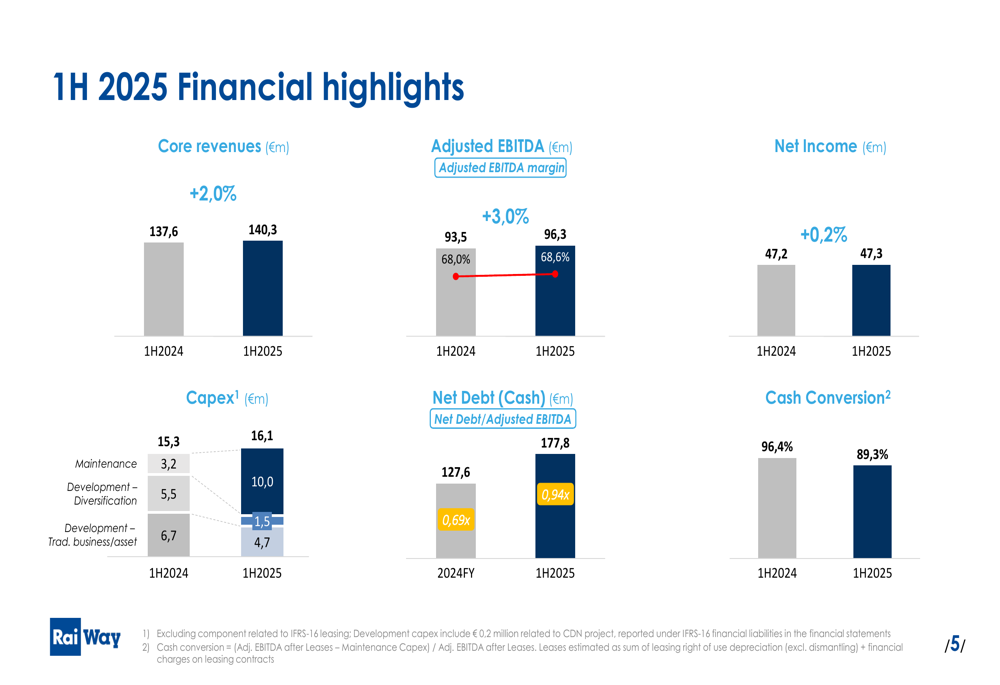

Rai Way delivered solid financial results for the first half of 2025, with core revenues increasing by 2.0% year-over-year to €140.3 million. Adjusted EBITDA grew by 3.0% to €96.3 million, with margins improving to 68.6% from 68.0% in the same period last year. Net income showed a slight increase of 0.2% to €47.3 million.

As shown in the following comprehensive financial overview:

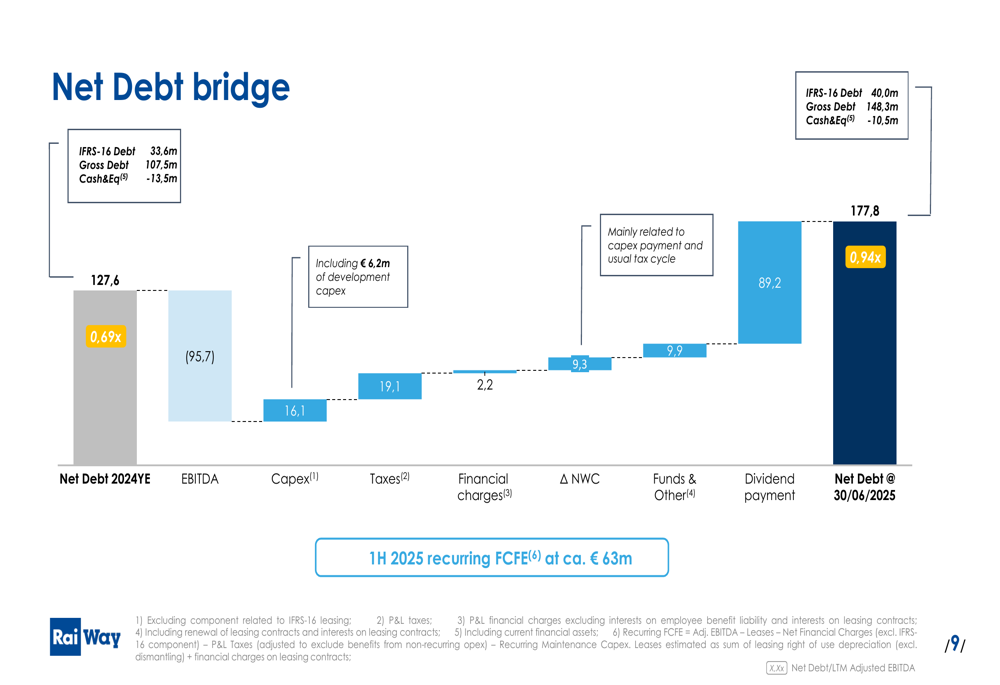

Capital expenditures increased slightly from €15.3 million to €16.1 million, while net debt rose to €177.8 million (representing 0.94x Net Debt/Adjusted EBITDA) from €127.6 million at the end of 2024. The increase in debt was primarily due to dividend payments of €89.2 million, as illustrated in the company’s net debt bridge:

Despite the higher debt level, Rai Way maintained a strong financial position with a leverage ratio well below 1x, indicating conservative financial management even while funding both dividends and growth initiatives.

Revenue and Cost Analysis

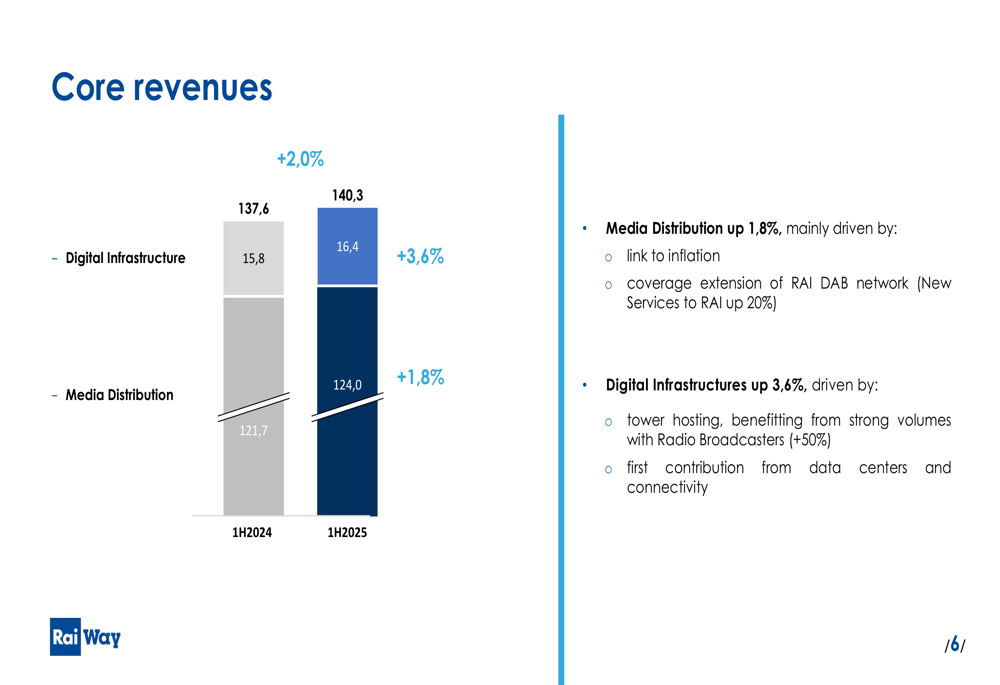

The company’s revenue growth was driven by positive performance across both of its core business segments. Media Distribution revenues, which account for approximately 88% of total core revenues, increased by 1.8% to €124.0 million, supported by inflation-linked contracts and the extension of RAI’s DAB network coverage.

Digital Infrastructure revenues showed stronger growth of 3.6% to €16.4 million, benefiting from increased tower hosting volumes, particularly from radio broadcasters (up 50%), and initial contributions from data centers and connectivity services.

The following chart illustrates the revenue breakdown by segment:

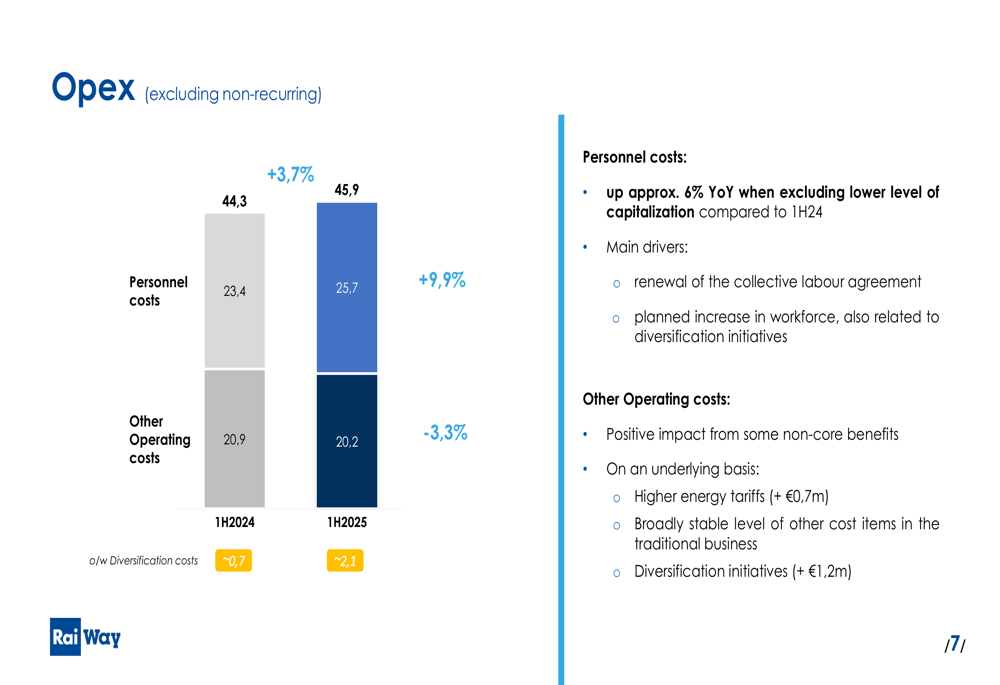

On the cost side, operating expenses excluding non-recurring items increased by 3.7% year-over-year. Personnel costs rose by 9.9% to €25.7 million, reflecting the renewal of the collective labor agreement and planned workforce expansion related to diversification initiatives. Meanwhile, other operating costs decreased by 3.3% to €20.2 million, benefiting from some non-core items despite higher energy tariffs.

The cost structure evolution is presented in the following chart:

CFO Adalberto Pellegrino noted during the presentation that the company is managing its cost base efficiently while investing in future growth areas, a strategy that appears to be paying off with the improved EBITDA margins.

Strategic Initiatives and Diversification

Rai Way continued to make progress on its diversification strategy during the first half of 2025. The company secured framework agreements with three of the main live streaming content providers in Italy for its Content Delivery Network (CDN) services, positioning it to capture growth in the digital content distribution market.

In the Edge Data Centers segment, Rai Way announced a partnership with Cubbit, a geo-distributed cloud storage enabler, to power its cloud storage solutions and jointly exploit market opportunities. This strategic alliance aims to better address the needs of medium-sized enterprises, which represent approximately half of Rai Way’s priority market for Edge DC services.

The company’s go-to-market strategy for Edge Data Centers is illustrated here:

Progress was also reported on the Hyperscale Data Center front, with the finalization of a draft concession agreement with the municipality, expected to be signed in the upcoming weeks. These initiatives align with Rai Way’s strategy to leverage its existing infrastructure and nationwide presence to expand beyond its traditional broadcasting business.

Updated Outlook and Guidance

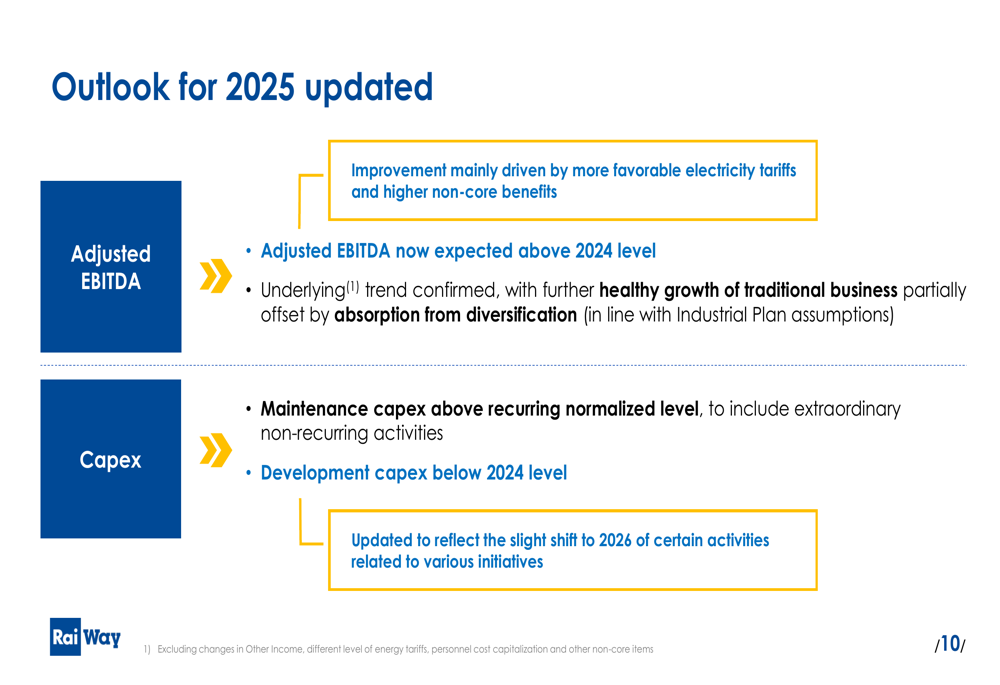

Based on the strong first-half performance, Rai Way raised its full-year 2025 Adjusted EBITDA guidance, now expecting it to exceed 2024 levels. The improvement is primarily driven by more favorable electricity tariffs and higher non-core benefits, while the underlying trend remains in line with previous expectations.

The company updated its capital expenditure outlook, with development capex now expected to be below 2024 levels, reflecting a slight shift of certain activities to 2026. Maintenance capex is projected to remain above the recurring normalized level due to extraordinary non-recurring activities.

The updated guidance is summarized in the following slide:

CEO Roberto Cecatto commented during the presentation that the company is also progressing with its analysis of potential sector consolidation opportunities, suggesting that Rai Way may be exploring strategic M&A activities to further strengthen its market position.

This represents a more optimistic outlook compared to the Q1 2025 earnings call, where the company maintained its previous guidance despite showing revenue growth. The improved performance in Q2 and favorable cost developments have clearly increased management’s confidence in the full-year outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.