CTAs keep buying Treasuries, gold longs face stop-loss risk: BofA

Introduction & Market Context

Rapid7 Inc . (NASDAQ:RPD) presented its Q2 2025 corporate overview on August 7, highlighting the company’s strategic positioning in the expanding cybersecurity market while navigating a challenging spending environment. The presentation revealed a company in transition, focusing on profitability improvements while facing moderating growth rates.

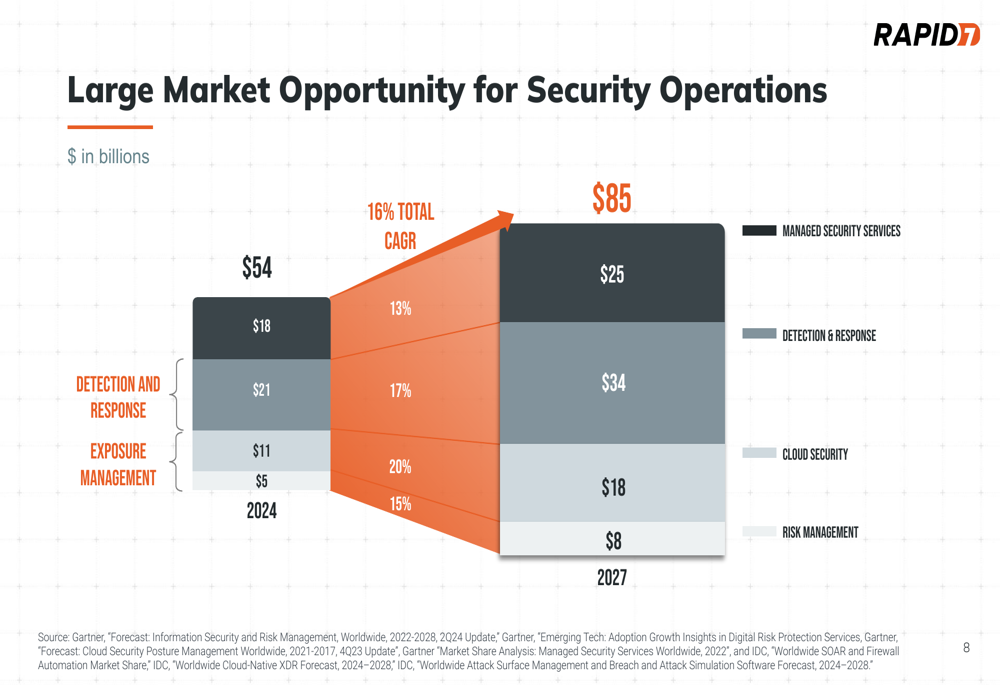

The cybersecurity firm operates in a robust market projected to reach $85 billion by 2027, growing at a 16% CAGR according to data from Gartner (NYSE:IT) and IDC cited in the presentation. Despite this favorable market backdrop, Rapid7’s stock has struggled, closing at $19.82 on August 7, down 0.85% for the day and near its 52-week low of $19.21.

As shown in the following market opportunity breakdown, Rapid7 is targeting multiple high-growth segments within the security operations space:

Quarterly Performance Highlights

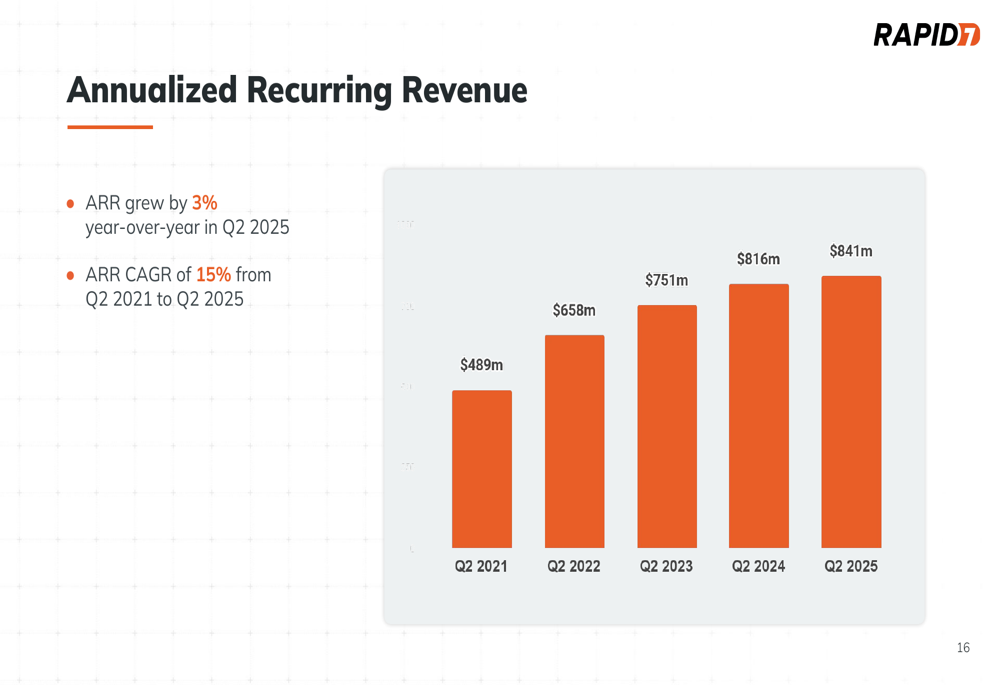

Rapid7 reported Q2 2025 results showing modest growth with ARR reaching $841 million, representing a 3% year-over-year increase. This continues the trend seen in Q1 2025, when the company reported 4% ARR growth to $837 million. While this growth rate marks a significant deceleration from the company’s historical 20% CAGR between 2020-2024, Rapid7 has successfully shifted focus toward improving profitability metrics.

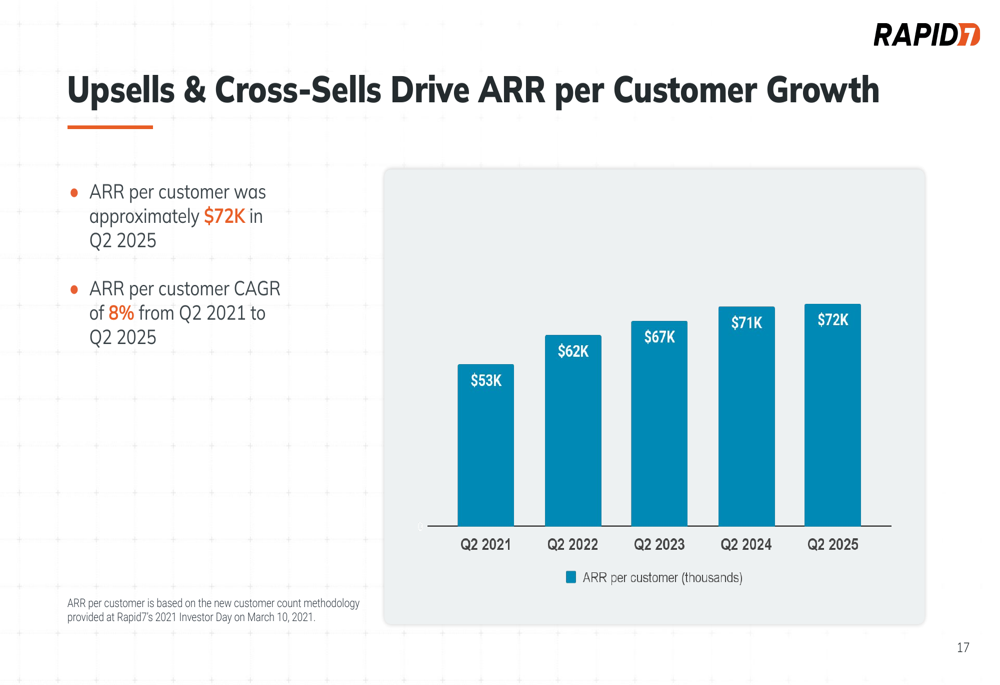

The company’s ARR per customer reached approximately $72,000 in Q2 2025, maintaining the 8% CAGR achieved since Q2 2021. This metric suggests Rapid7 continues to effectively cross-sell and upsell its existing customer base despite challenges in new customer acquisition.

As illustrated in the following chart, Rapid7’s ARR has shown steady but decelerating growth over recent quarters:

The company has also demonstrated consistent improvement in ARR per customer, highlighting its success in expanding relationships with existing clients:

Strategic Initiatives & Market Positioning

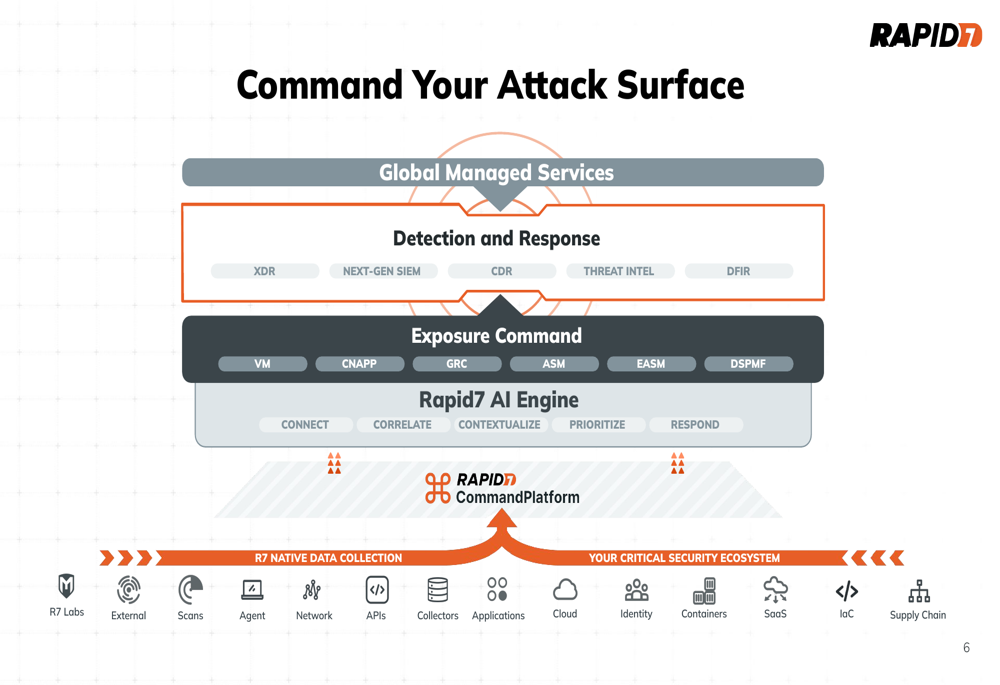

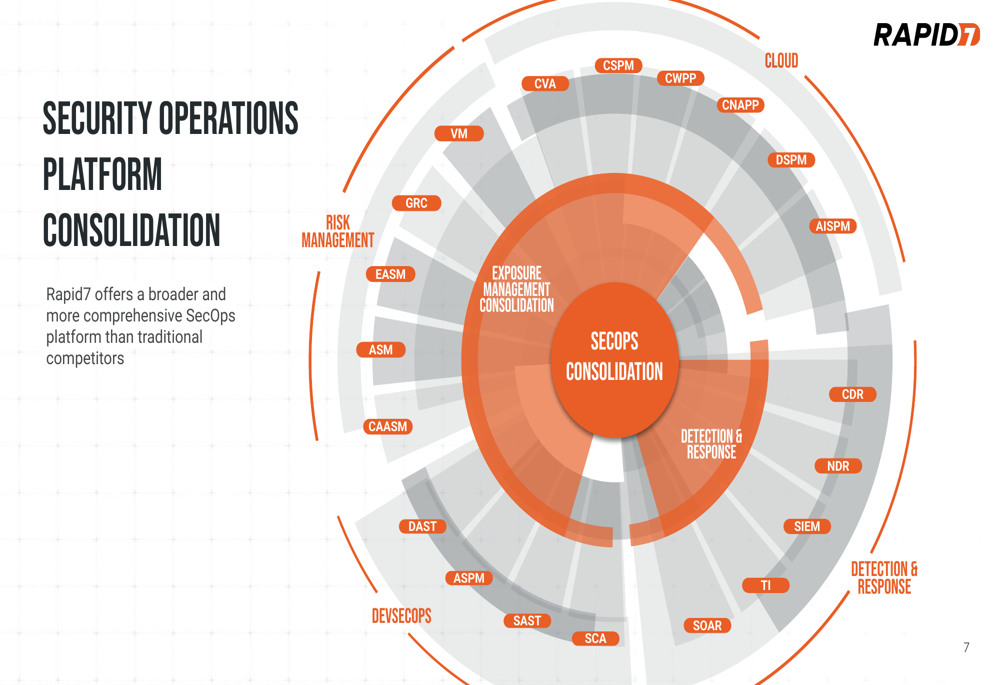

Rapid7’s presentation emphasized its evolution into a comprehensive security operations platform, aiming to consolidate fragmented security tools across cloud security, detection and response, and risk management. The company serves over 11,000 global customers and processes more than 300 trillion events through its threat engine.

The strategic focus on platform consolidation is designed to address what Rapid7 describes as a "fragmented attack surface" where organizations struggle to gain visibility, integrate disparate systems, and prioritize security actions. This approach aligns with industry trends toward unified security platforms that reduce complexity and operational overhead.

As shown in the following architectural overview, Rapid7’s platform strategy encompasses multiple security domains:

The company’s consolidation strategy extends across various security operations categories:

Financial Outlook & Guidance

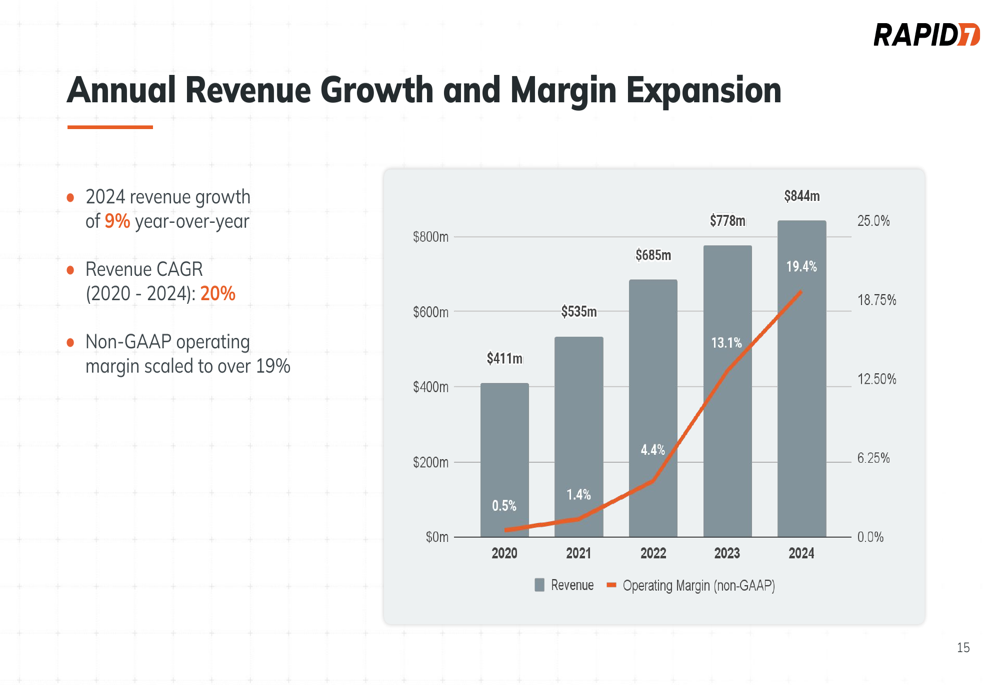

Rapid7’s financial trajectory shows a clear pivot from growth to profitability. While revenue growth has moderated, the company has significantly improved its operating margins, with non-GAAP operating margin expanding from 5% in 2021 to 19.4% in 2024.

The following chart illustrates this shift toward improved profitability:

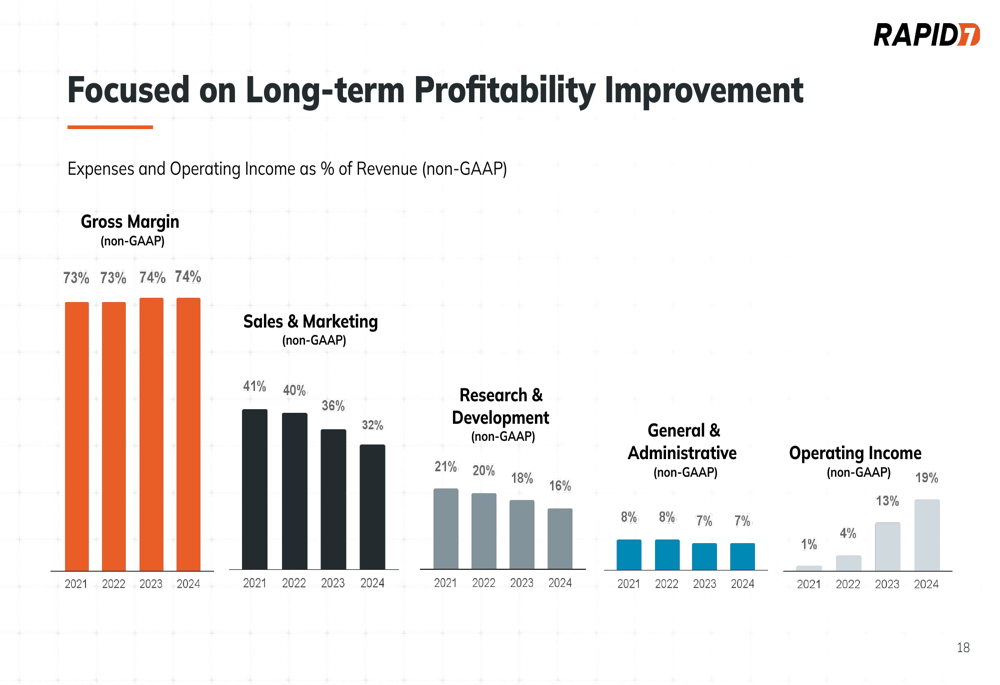

The company has achieved this margin expansion through disciplined expense management, reducing Sales & Marketing costs from 41% of revenue in 2021 to 32% in 2024, while Research & Development expenses decreased from 21% to 16% during the same period:

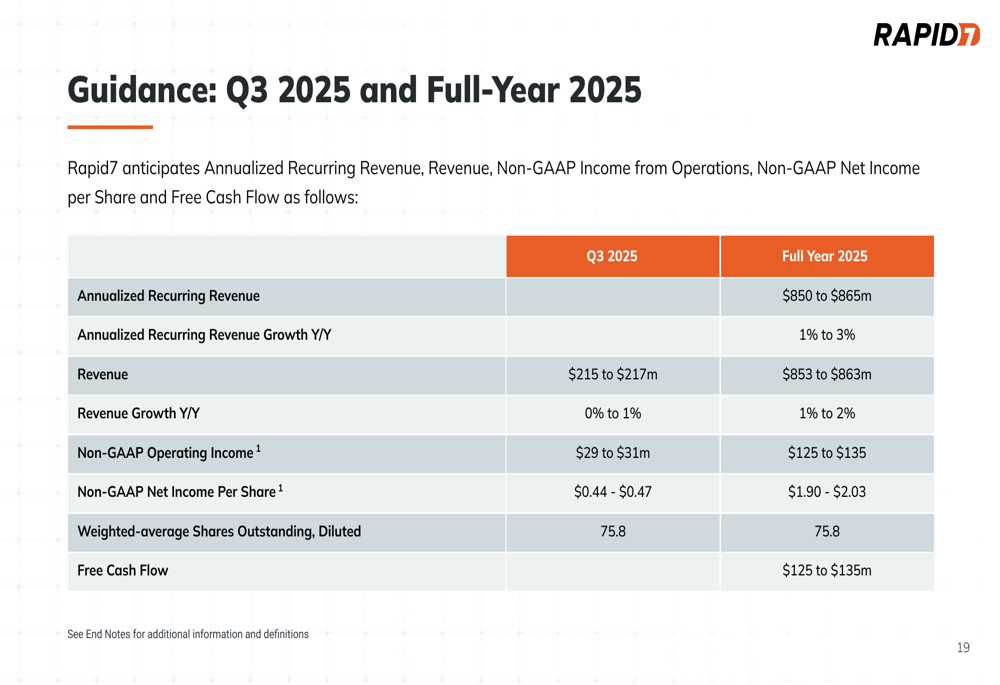

Looking ahead, Rapid7 provided guidance for Q3 and full-year 2025, projecting continued modest growth with ARR expected to reach $850-$865 million (1-3% growth) and revenue of $853-$863 million (1-2% growth) for the full year. The company expects to generate $125-$135 million in free cash flow for 2025.

The detailed guidance figures are presented below:

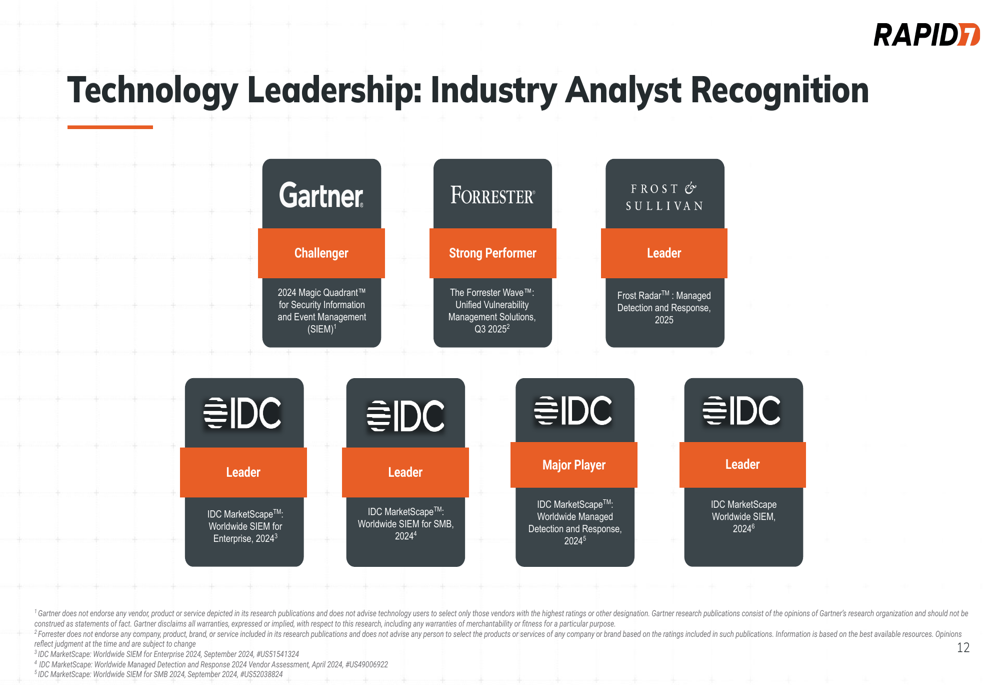

Competitive Industry Position

Rapid7 highlighted its recognition by leading industry analysts, positioning itself as a credible player across multiple security domains. The company is recognized as a "Challenger" in Gartner’s Magic Quadrant for Security Information and Event Management (SIEM), a "Strong Performer" in Forrester’s Wave for Unified Vulnerability Management, and a "Leader" in Frost & Sullivan’s Radar for Managed Detection and Response.

This analyst recognition reinforces Rapid7’s competitive standing in the security market:

The company also emphasized its extensive partner ecosystem, featuring over 500 platform integrations with major technology providers. This integration capability is crucial for Rapid7’s value proposition of unifying disparate security tools and data sources.

Rapid7’s presentation portrays a company navigating the transition from high growth to sustainable profitability in a competitive security market. While growth has moderated significantly compared to historical rates, the company has successfully improved margins and cash flow generation while positioning itself as a comprehensive security operations platform in a market that continues to expand.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.