Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

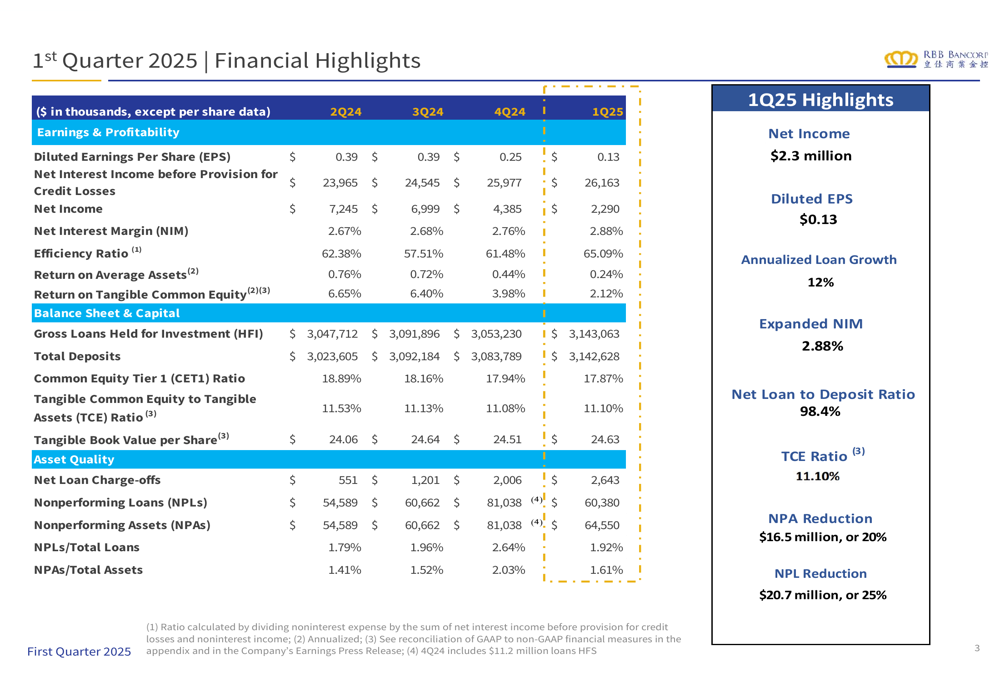

RBB Bancorp (NASDAQ:RBB) released its first quarter 2025 earnings presentation, revealing a mixed financial performance characterized by improved asset quality metrics but continued pressure on profitability. The bank reported net income of $2.3 million and diluted earnings per share (EPS) of $0.13, down significantly from $0.25 in the previous quarter. Despite the earnings decline, RBB Bancorp’s stock closed at $15.65 on April 28, 2025, down 1.07% for the day.

The company’s presentation highlighted several positive developments, including a 12% annualized loan growth, expanded net interest margin (NIM), and substantial reductions in non-performing assets. These improvements come as the bank continues to execute its strategy under new CEO Johnny Lee, who recently took over leadership of the institution.

Quarterly Performance Highlights

RBB Bancorp’s first quarter 2025 financial results showed declining profitability despite growth in key balance sheet metrics. Net income fell to $2.3 million, resulting in diluted EPS of $0.13, compared to $0.39 in both Q2 and Q3 of 2024, and $0.25 in Q4 2024. This downward trend in earnings occurred despite an increase in net interest income before provision for credit losses, which rose to $26.2 million from $26.0 million in the previous quarter.

As shown in the following comprehensive financial highlights table, the bank’s net interest margin expanded to 2.88%, continuing an upward trend from previous quarters, while the efficiency ratio deteriorated to 65.09%, indicating increased operating costs relative to revenue:

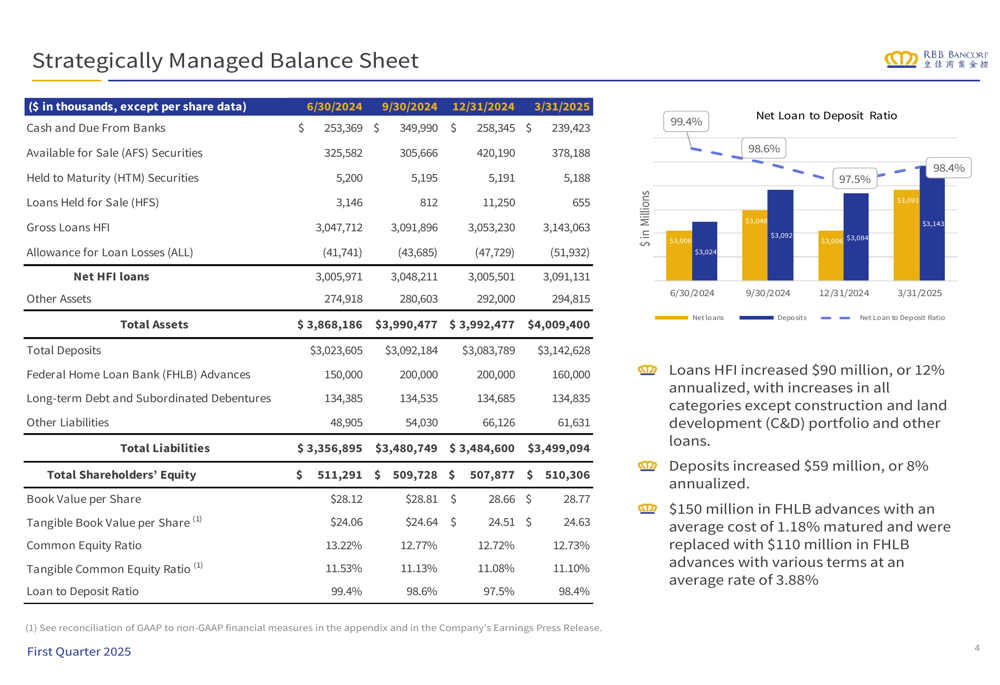

The bank’s balance sheet showed healthy growth, with total assets increasing to $4.01 billion as of March 31, 2025. Loans held for investment grew by $90 million or 12% annualized, while deposits increased by $59 million or 8% annualized. The net loan-to-deposit ratio stood at 98.4%, reflecting a well-balanced funding structure.

The following chart illustrates the company’s strategically managed balance sheet, showing the growth in loans and deposits while maintaining strong capital ratios:

Loan Portfolio and Asset Quality

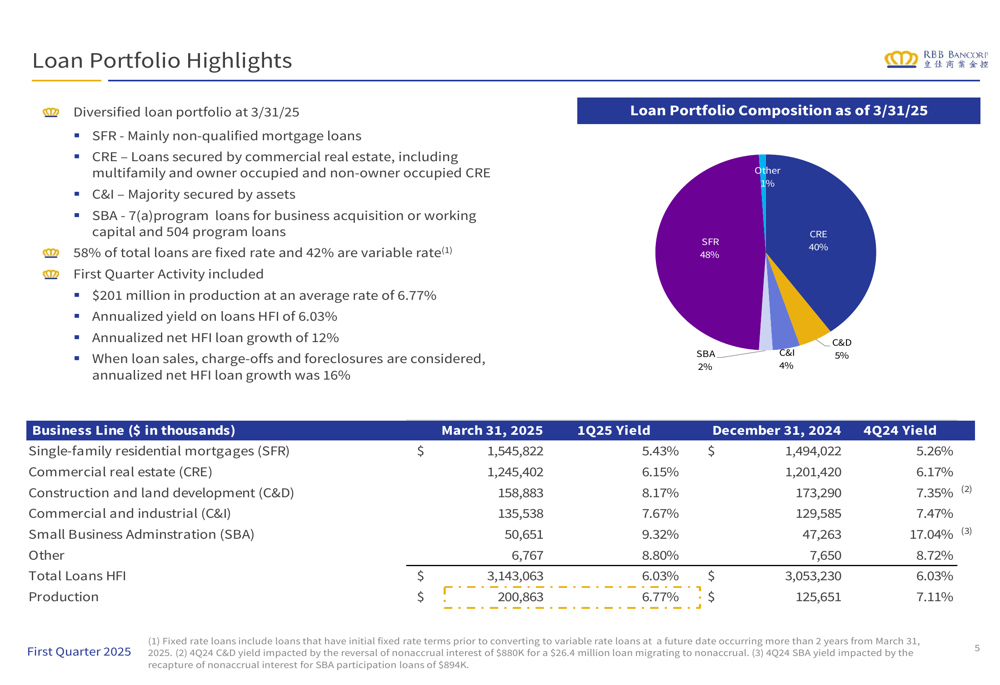

RBB Bancorp maintains a diversified loan portfolio, with single-family residential mortgages comprising 48% of total loans, followed by commercial real estate at 40%. The remaining portfolio consists of construction and development (5%), commercial and industrial (4%), Small Business Administration (2%), and other loans (1%). The bank’s loan production in the first quarter totaled $201 million at an average rate of 6.77%.

The following chart provides a detailed breakdown of the bank’s loan portfolio composition and yields:

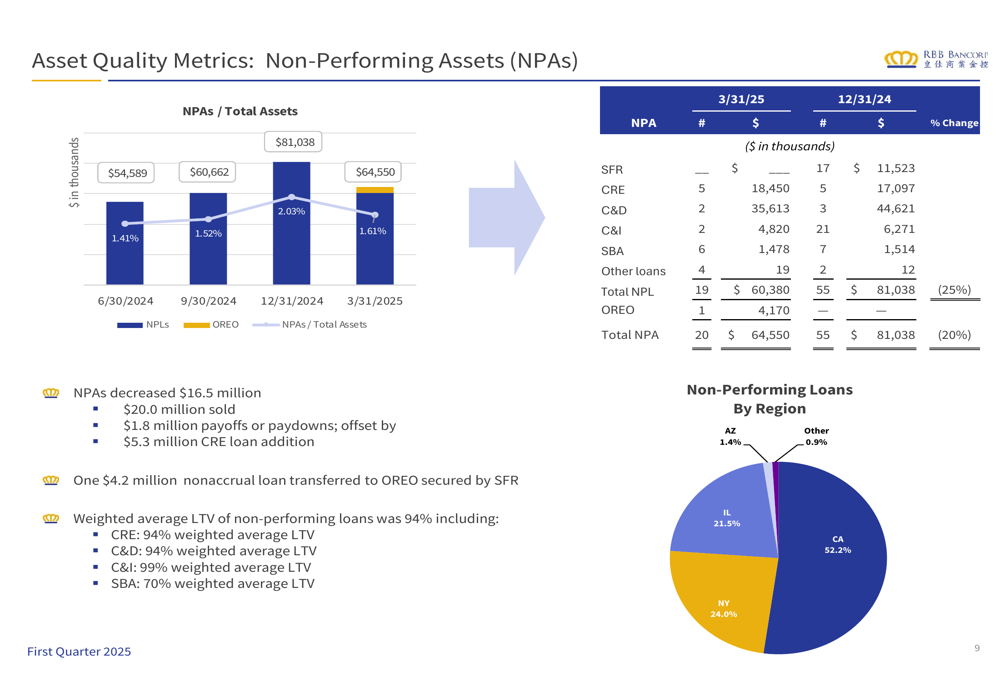

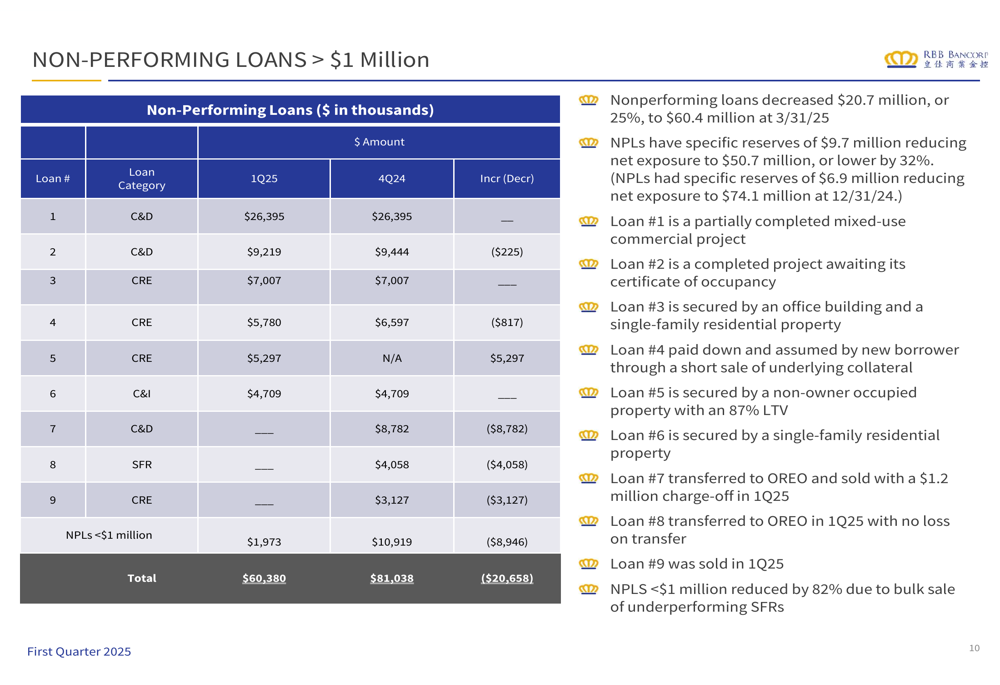

A significant highlight of the quarter was the substantial improvement in asset quality metrics. Non-performing assets (NPAs) decreased by $16.5 million or 20% to $64.6 million, while non-performing loans (NPLs) declined by $20.7 million or 25% to $60.4 million. This reduction represents meaningful progress in the bank’s efforts to address problem assets.

The following chart illustrates the improvement in non-performing assets over recent quarters:

The bank provided detailed information on its largest non-performing loans, showing resolution progress on several significant exposures:

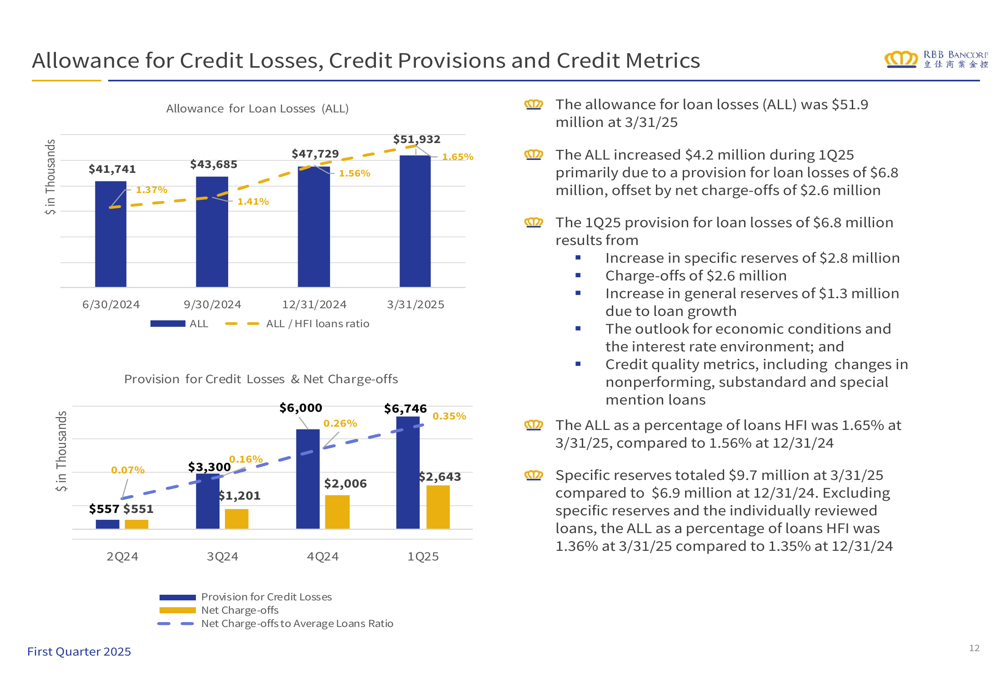

Despite the improvement in non-performing assets, RBB Bancorp increased its allowance for loan losses to $51.9 million, representing 1.65% of loans held for investment. The provision for loan losses in Q1 2025 was $6.8 million, driven by a $2.8 million increase in specific reserves, $2.6 million in charge-offs, and a $1.3 million increase in general reserves due to loan growth.

The following chart shows the trend in allowance for loan losses and related credit metrics:

Capital Position and Outlook

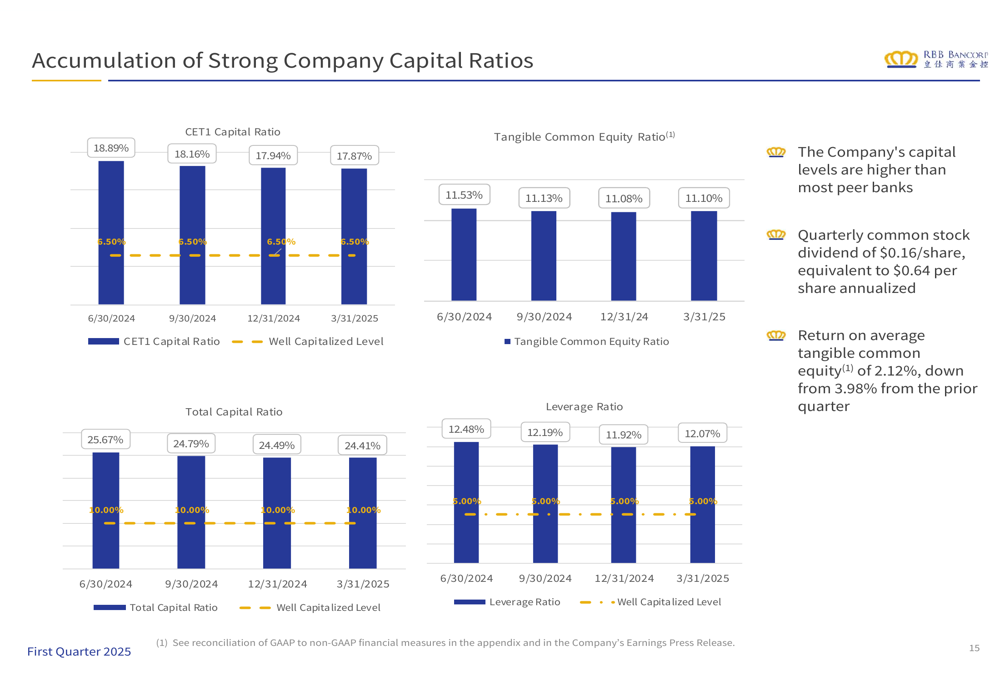

RBB Bancorp maintains strong capital ratios that exceed regulatory requirements and surpass those of most peer banks. As of March 31, 2025, the bank reported a Common Equity Tier 1 (CET1) ratio of 17.87% and a tangible common equity to tangible assets ratio of 11.10%. These robust capital levels provide the bank with significant flexibility to manage through credit challenges while supporting future growth.

The following chart illustrates the bank’s strong capital position over recent quarters:

The bank continues to pay a quarterly common stock dividend of $0.16 per share, equivalent to $0.64 per share annualized. However, the return on average tangible common equity declined to 2.12% in Q1 2025, down from 3.98% in the previous quarter, reflecting the impact of lower earnings on shareholder returns.

Forward-Looking Statements

While RBB Bancorp’s presentation did not provide explicit forward guidance, the bank’s focus on resolving non-performing assets and growing its loan portfolio suggests a strategic emphasis on improving asset quality while maintaining growth. The 20% reduction in non-performing assets during the quarter represents significant progress toward the previously stated goal of resolving problem assets by the end of 2025.

The bank’s loan growth of 12% annualized in Q1 2025 exceeds the "low to mid-single-digit" growth projection mentioned in the previous earnings call, indicating stronger-than-expected lending activity. However, continued elevated provisions for credit losses suggest ongoing challenges in managing loan quality.

RBB Bancorp’s expanded net interest margin of 2.88% represents a positive trend that could support improved profitability if asset quality stabilizes and credit costs normalize. The bank’s strong capital position provides a solid foundation for navigating current challenges while pursuing strategic opportunities, including potential acquisitions of Asian American banks as mentioned in previous communications.

As the bank continues its leadership transition under new CEO Johnny Lee, investors will be watching closely for signs of sustainable improvement in both asset quality and profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.