Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Real Matters Inc (TSX:REAL) presented its second-quarter fiscal 2025 financial results on April 30, 2025, highlighting a mixed performance across its business segments amid ongoing challenges in the U.S. mortgage market. The company reported consolidated net revenue of $10.1 million, down 13% year-over-year, primarily due to declining volumes in the U.S. purchase mortgage origination market.

Despite these headwinds, Real Matters maintained a strong cash position of $46 million with no debt, while continuing to expand its client base and achieve operational efficiencies. The company’s shares closed at $6.02 on April 29, 2025, up 0.67% ahead of the results presentation.

Quarterly Performance Highlights

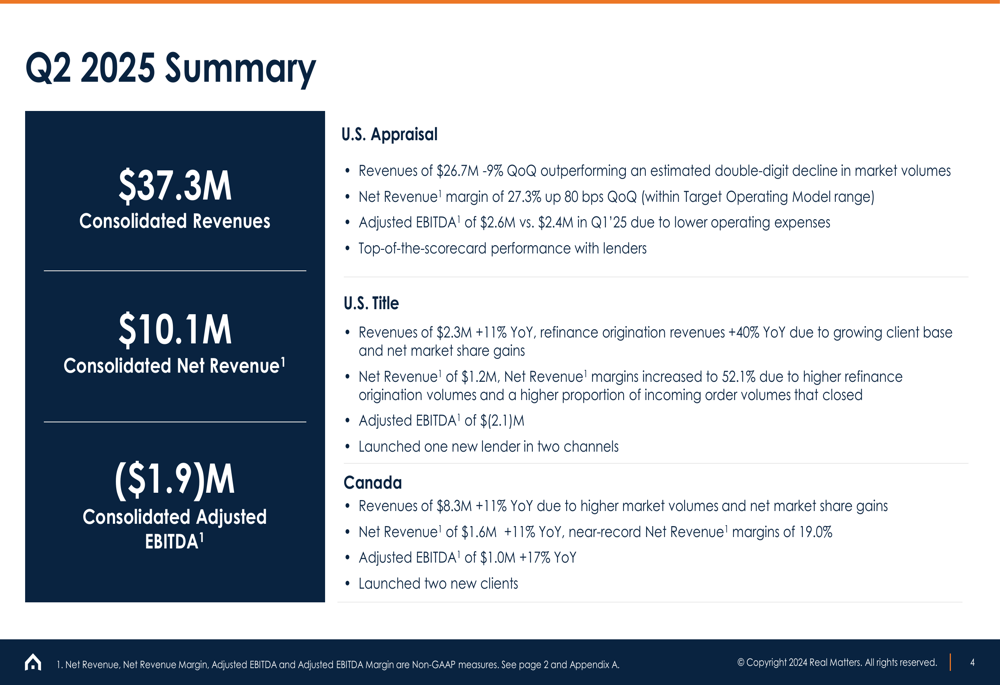

Real Matters reported consolidated revenues of $37.3 million for Q2 2025, representing a 9% decrease quarter-over-quarter and an 11% decline year-over-year. However, the company emphasized that it outperformed the broader market on a sequential basis, while maintaining top-of-the-scorecard performance with its lender clients.

As shown in the following highlights from the company’s presentation:

The company’s net revenue margin remained healthy at 26.9%, though adjusted EBITDA was negative at $(1.9) million for the quarter. Management attributed this performance to disciplined cost management and the flexibility of their network management model, which allowed them to adapt to changing market conditions.

Segment Analysis

Real Matters operates across three key segments: U.S. Appraisal, U.S. Title, and Canada. Each segment showed distinct performance patterns in Q2 2025, as detailed in the following segment breakdown:

U.S. Appraisal

The U.S. Appraisal segment, which represents the largest portion of Real Matters’ business, experienced a 9% quarter-over-quarter revenue decline to $26.7 million. Despite this decrease, the company noted that it outperformed the estimated double-digit decline in market volumes, suggesting market share gains.

Net revenue margin in this segment improved by 80 basis points quarter-over-quarter to 27.3%, which falls within the company’s target operating model range. Adjusted EBITDA increased slightly to $2.6 million from $2.4 million in Q1 2025, driven by lower operating expenses and operational efficiencies.

U.S. Title

In contrast to the Appraisal segment, the U.S. Title business showed strong growth, with revenues increasing 11% year-over-year to $2.3 million. Refinance origination revenues were particularly strong, up 40% compared to the same period last year, reflecting the company’s growing client base and net market share gains.

Net revenue in this segment reached $1.2 million with margins expanding to 52.1%, attributed to higher refinance origination volumes and improved conversion rates of incoming orders. Despite these improvements, the segment still recorded an adjusted EBITDA loss of $(2.1) million, indicating ongoing investments in growth.

Canada

The Canadian segment delivered solid performance with revenues of $8.3 million, up 11% year-over-year. This growth was driven by higher market volumes and net market share gains. Net revenue also increased by 11% to $1.6 million, with near-record margins of 19.0%.

Adjusted EBITDA in Canada grew by 17% year-over-year to $1.0 million, demonstrating the strength and profitability of this segment. The company also successfully launched two new clients in the Canadian market during the quarter.

Financial Position

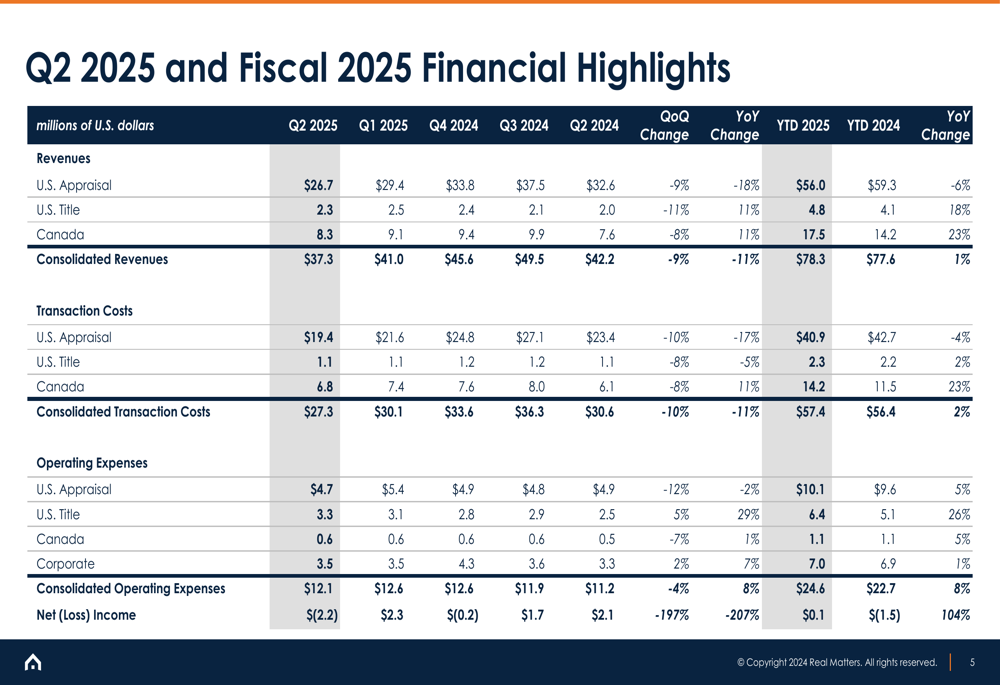

A detailed view of Real Matters’ financial performance across recent quarters shows the trends in revenue, costs, and profitability:

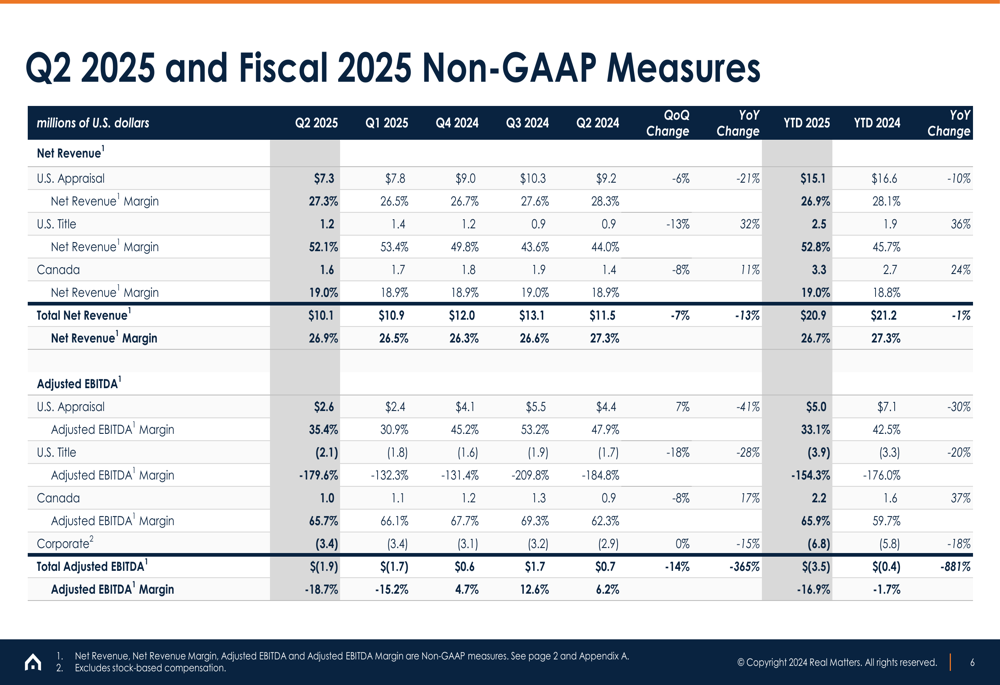

The company’s non-GAAP measures provide additional insight into segment performance and overall profitability:

Real Matters maintained a strong balance sheet with $46 million in cash and no debt at the end of Q2 2025. This financial flexibility positions the company well to weather current market challenges while investing in strategic growth initiatives.

Strategic Initiatives & Outlook

Real Matters continues to execute on its strategy focused on broadening its client base, deepening customer relationships, and maintaining cost discipline. During Q2 2025, the company onboarded three new customers across its business segments and launched one new lender in two channels within its U.S. Title segment.

Looking ahead, management highlighted a growing pool of potential refinance candidates, with approximately 10 million mortgages currently at or above 6% interest rates. This represents a significant opportunity for Real Matters as interest rates potentially moderate in the future, driving refinance activity.

The company believes it is well-positioned to capitalize on mortgage market improvements when they occur, leveraging its network management model and operational efficiencies to drive growth and profitability. In the meantime, Real Matters continues to focus on gaining market share and improving margins within the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.