Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Regional Management Corp (NYSE:RM) reported mixed financial results for the first quarter of 2025, with strong revenue growth and portfolio expansion offset by a significant decline in net income. The consumer finance company released its earnings presentation on April 30, with shares closing down 2.89% at $32.96.

Quarterly Performance Highlights

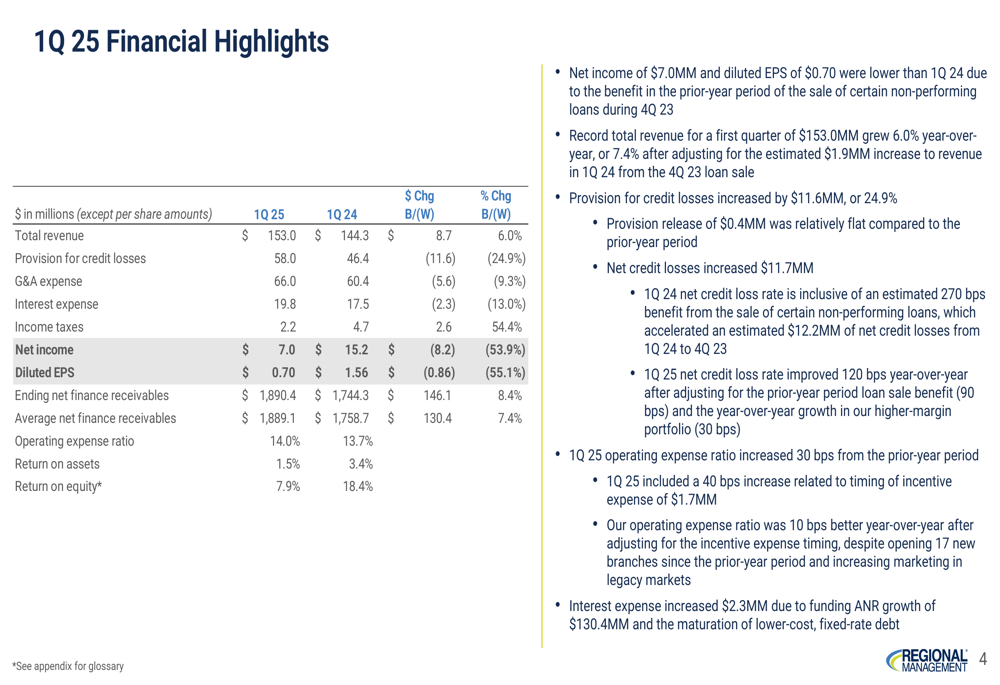

Regional Management achieved record first-quarter revenue of $153.0 million, up 6.0% year-over-year, driven by portfolio growth and strategic shifts in its product mix. However, net income fell 53.9% to $7.0 million, with diluted earnings per share of $0.70, down from $1.56 in the same period last year.

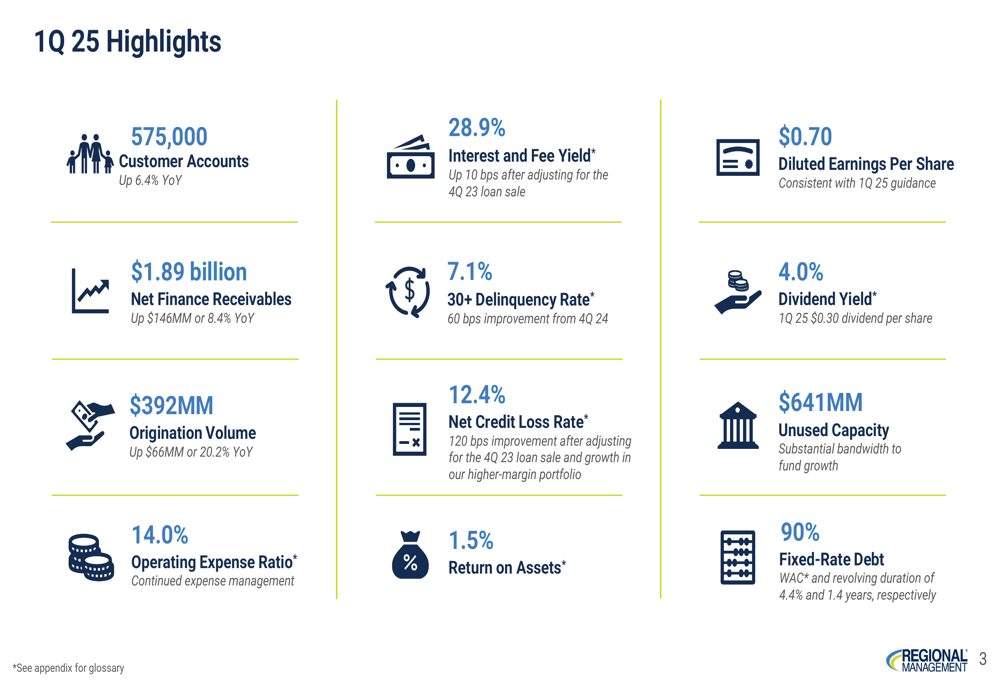

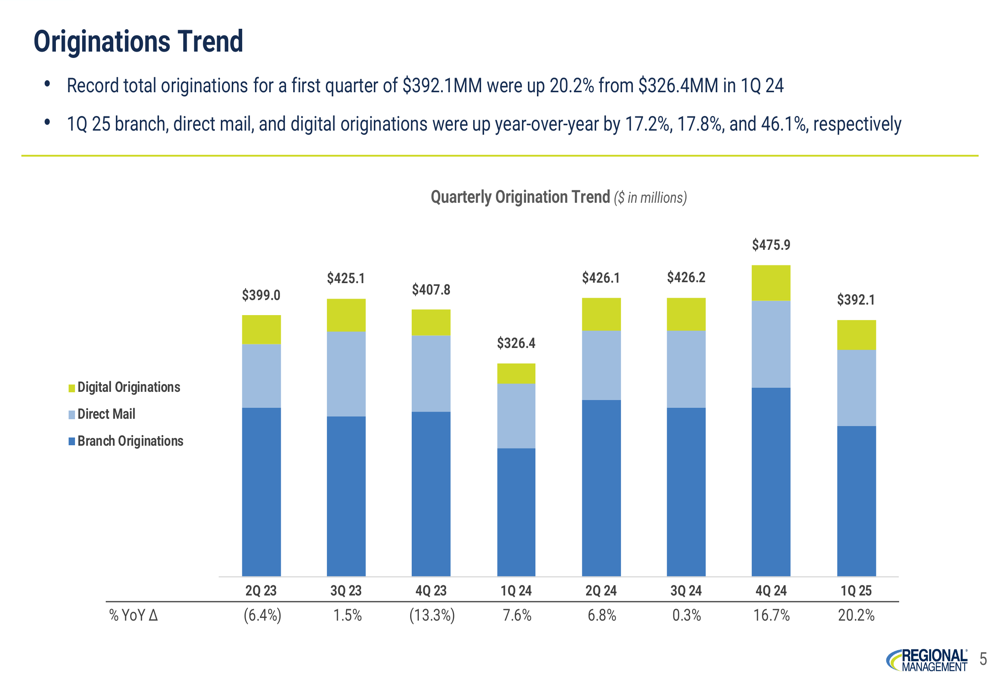

The company reported its customer base grew to 575,000 accounts, a 6.4% increase from the prior year, while net finance receivables reached $1.89 billion, up 8.4% year-over-year. The growth was supported by record first-quarter originations of $392.1 million, representing a 20.2% increase from Q1 2024.

As shown in the following comprehensive overview of key metrics:

Detailed Financial Analysis

Regional Management’s financial performance reflected both positive growth trends and profitability challenges. While total revenue increased by 6.0%, the company faced higher costs across multiple areas. Provision for credit losses rose 24.9% to $58.0 million, general and administrative expenses increased 9.3% to $66.0 million, and interest expense grew 13.0% to $19.8 million.

The detailed financial summary below highlights these trends:

The company’s origination channels all showed strong growth, with digital originations leading the way at 46.1% year-over-year growth. Branch and direct mail originations also performed well, increasing by 17.2% and 17.8% respectively.

As illustrated in the quarterly origination trend chart:

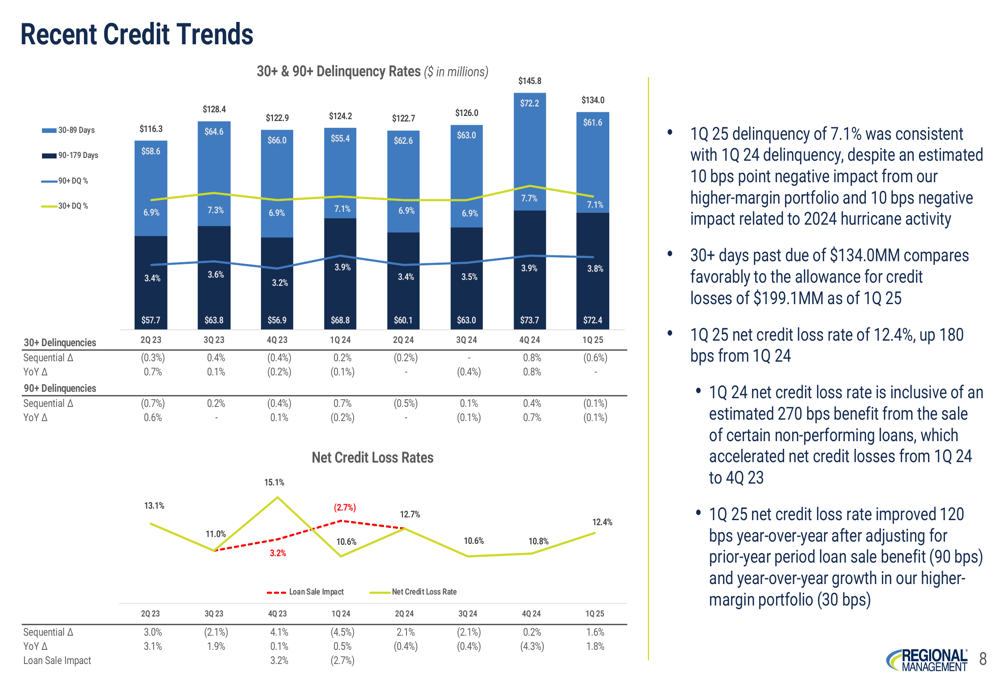

Credit performance showed signs of stabilization, with the 30+ day delinquency rate at 7.1%, consistent with Q1 2024 but improved by 60 basis points from Q4 2024. The net credit loss rate was 12.4%, up 180 basis points from Q1 2024, though the company noted a 120 basis point improvement after adjusting for a prior-year loan sale benefit and growth in higher-margin products.

The following chart demonstrates recent credit trends:

Strategic Initiatives

Regional Management continues to execute on several strategic initiatives aimed at driving growth and operational efficiency. The company is shifting its portfolio mix toward higher-margin products, with the percentage of loans at or below 36% APR declining from 86.1% in Q2 2023 to 81.7% in Q1 2025.

Digital originations have become an increasingly important part of the company’s growth strategy, representing 24.9% of total new borrower volume in Q1 2025. Large loans made up 75.3% of new borrower digitally sourced loans booked during the quarter.

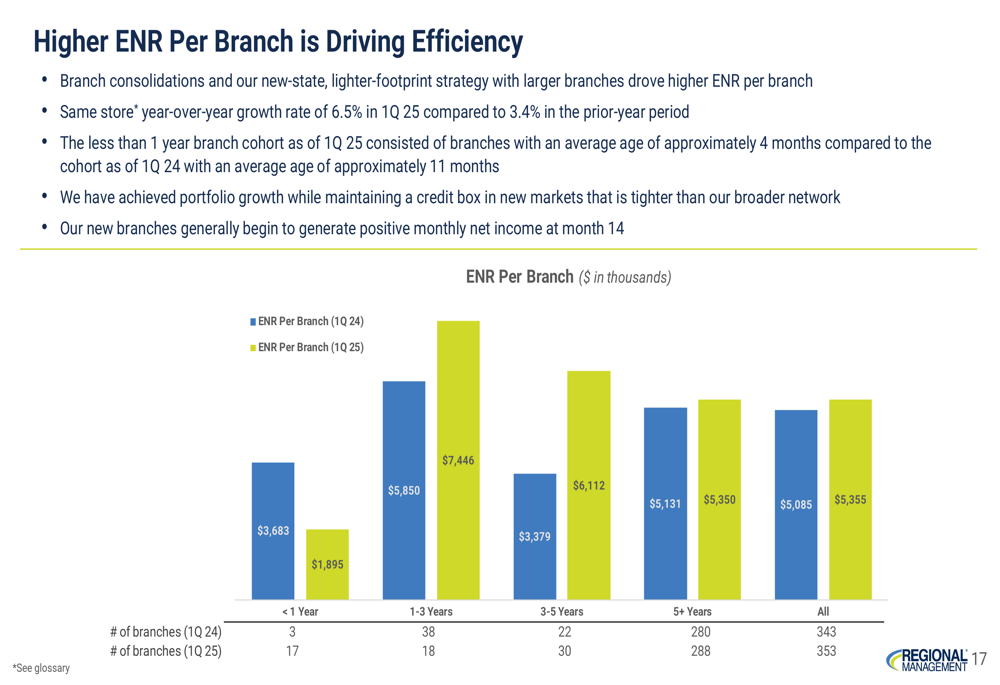

Branch efficiency has also improved significantly, with higher ending net receivables (ENR) per branch driven by branch consolidations and the company’s new-state, lighter-footprint strategy. Same-store year-over-year growth increased to 6.5% in Q1 2025, compared to 3.4% in the prior-year period.

As shown in the following chart demonstrating improved branch efficiency:

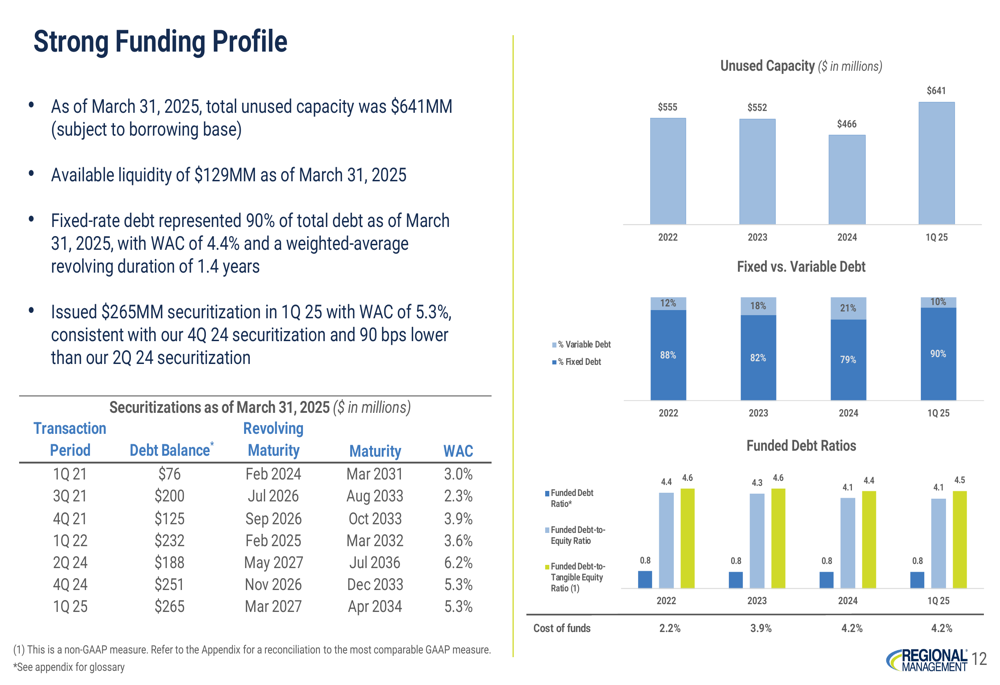

The company maintains a strong funding profile with $641 million in total unused capacity as of March 31, 2025, and available liquidity of $129 million. Fixed-rate debt represented 90% of total debt, providing stability in the current interest rate environment.

The following chart illustrates the company’s funding position:

Forward-Looking Statements

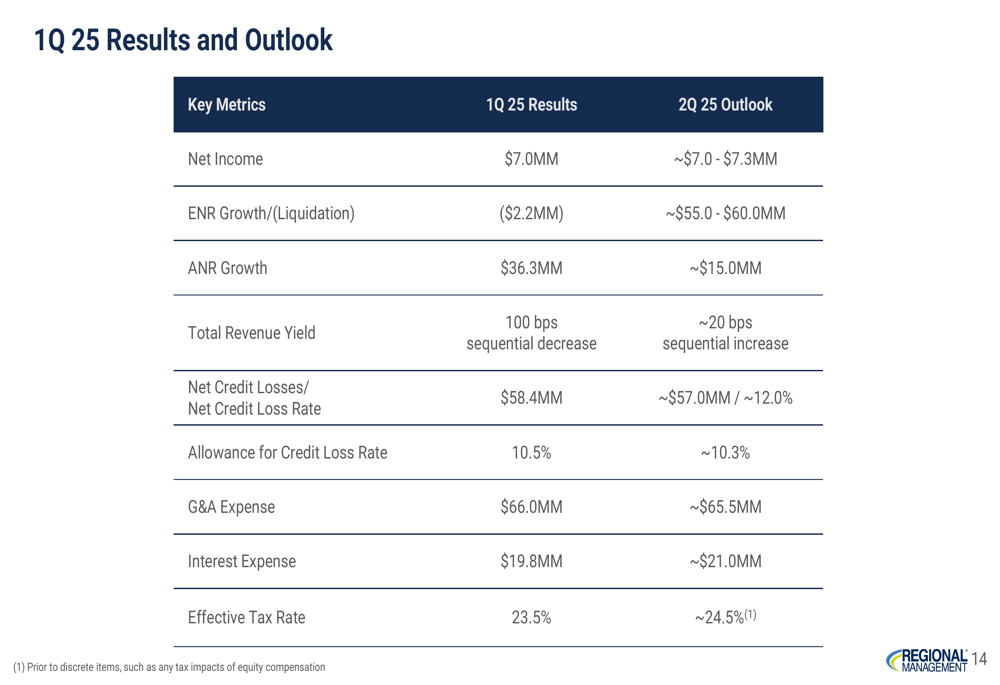

Looking ahead to the second quarter of 2025, Regional Management expects net income of approximately $7.0-7.3 million, with ending net receivables growth of $55-60 million. The company anticipates a slight improvement in the net credit loss rate to approximately 12.0%, down from 12.4% in Q1.

Total (EPA:TTEF) revenue yield is expected to increase by approximately 20 basis points sequentially, while the allowance for credit loss rate is projected to decline slightly to 10.3% from 10.5% in Q1. General and administrative expenses are forecast to decrease marginally to $65.5 million.

The company’s detailed outlook is presented in the following summary:

Regional Management’s focus on controlled growth, expense management, and digital transformation appears to be continuing the trends observed in previous quarters. While the company faces profitability challenges, its revenue growth and portfolio expansion demonstrate resilience in a competitive consumer finance landscape.

The company’s strategic shift toward higher-margin products and digital originations aligns with its long-term goals of improving operational efficiency and enhancing returns on assets and equity. However, investors will likely be watching closely to see if these initiatives can reverse the decline in net income in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.