Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

RE/MAX Holdings, Inc. (NYSE:RMAX) released its first quarter 2025 earnings presentation on May 2, showing declining revenue but improved profitability metrics amid continued divergence between international growth and domestic agent count challenges.

Quarterly Performance Highlights

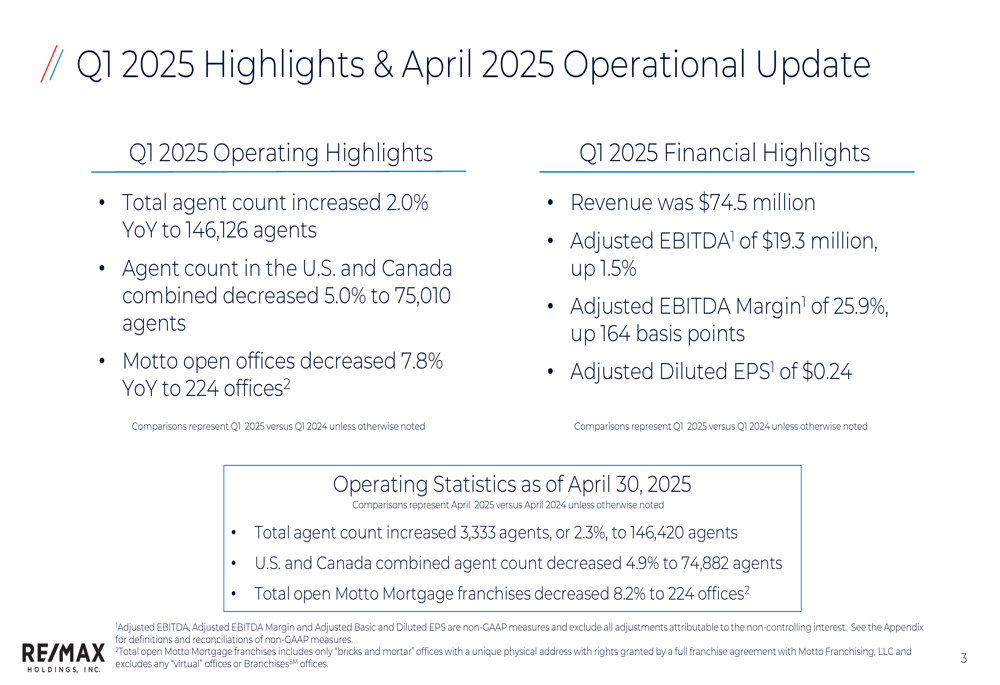

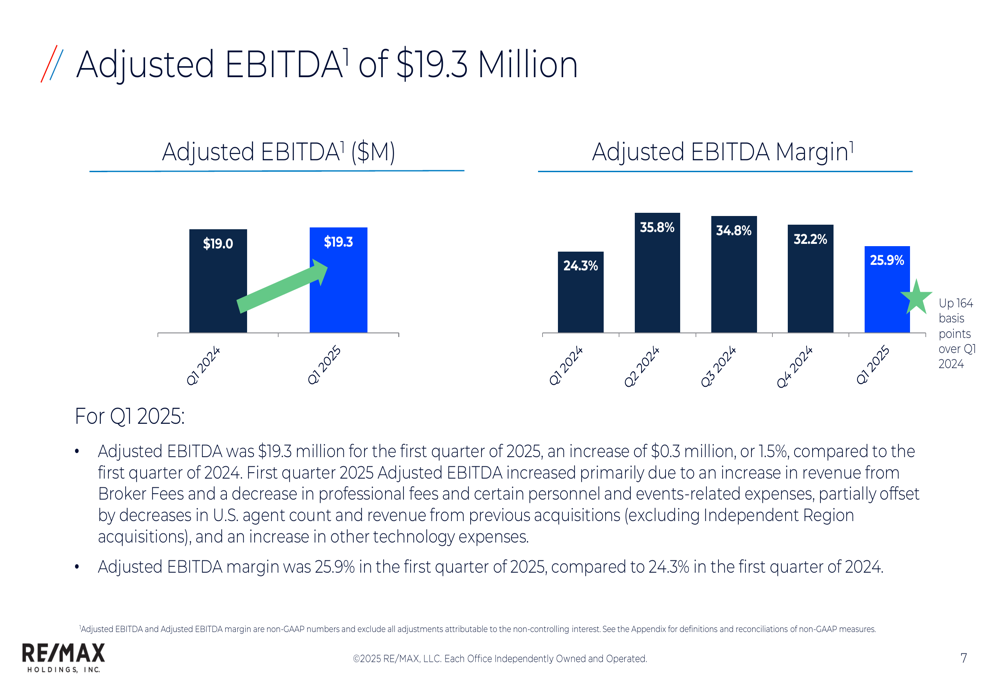

RE/MAX reported total revenue of $74.5 million for Q1 2025, representing a 4.9% decrease compared to $78.3 million in Q1 2024. Despite the revenue decline, the company achieved Adjusted EBITDA of $19.3 million, up 1.5% year-over-year, with an expanded Adjusted EBITDA margin of 25.9%, an improvement of 164 basis points.

As shown in the following summary of key Q1 2025 metrics:

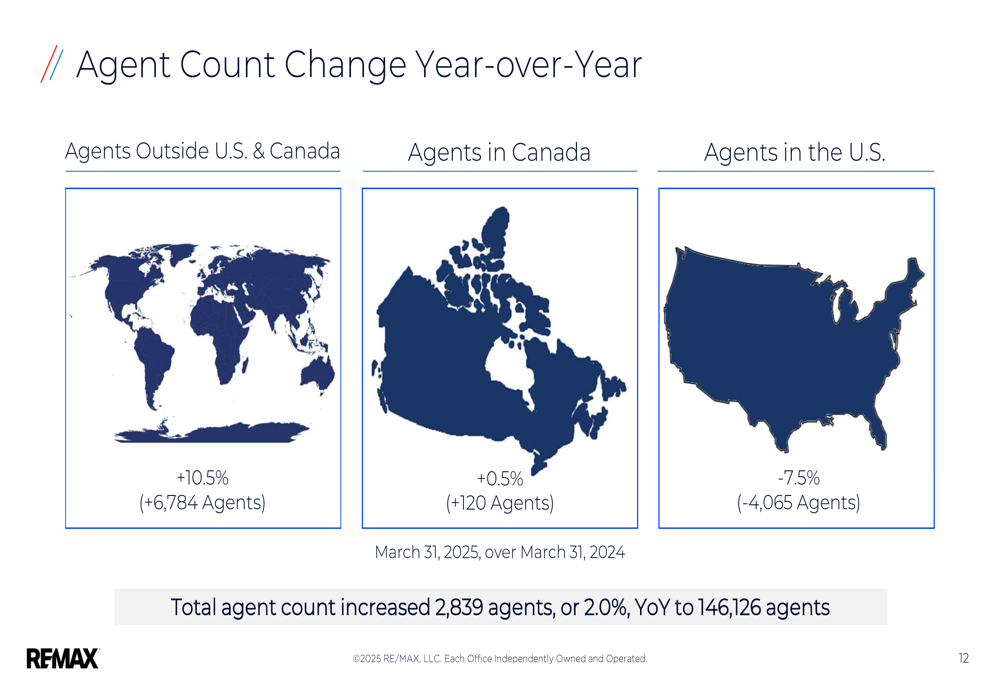

The company’s total agent count increased by 2.0% year-over-year to 146,126 agents, driven by strong international growth that offset continued weakness in the U.S. market. Agent count in the U.S. and Canada combined decreased by 5.0% to 75,010 agents, while agent count outside the U.S. and Canada grew by 10.5% to a record 71,116 agents.

The geographical breakdown of agent count changes reveals the stark contrast between RE/MAX’s domestic and international performance:

Detailed Financial Analysis

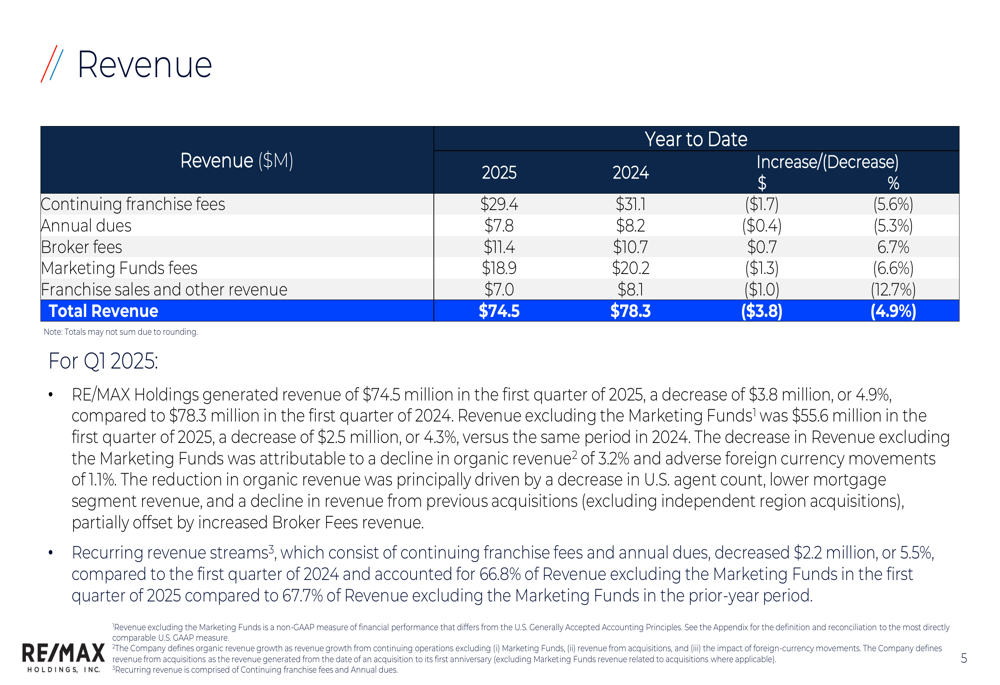

RE/MAX’s revenue decline was primarily driven by lower continuing franchise fees, annual dues, and Marketing Funds fees. Continuing franchise fees decreased by 5.6% to $29.4 million, while annual dues fell by 5.3% to $7.8 million. These declines reflect the company’s challenges in the U.S. market, where agent count decreased by 7.5%.

The following chart details the revenue breakdown for Q1 2025:

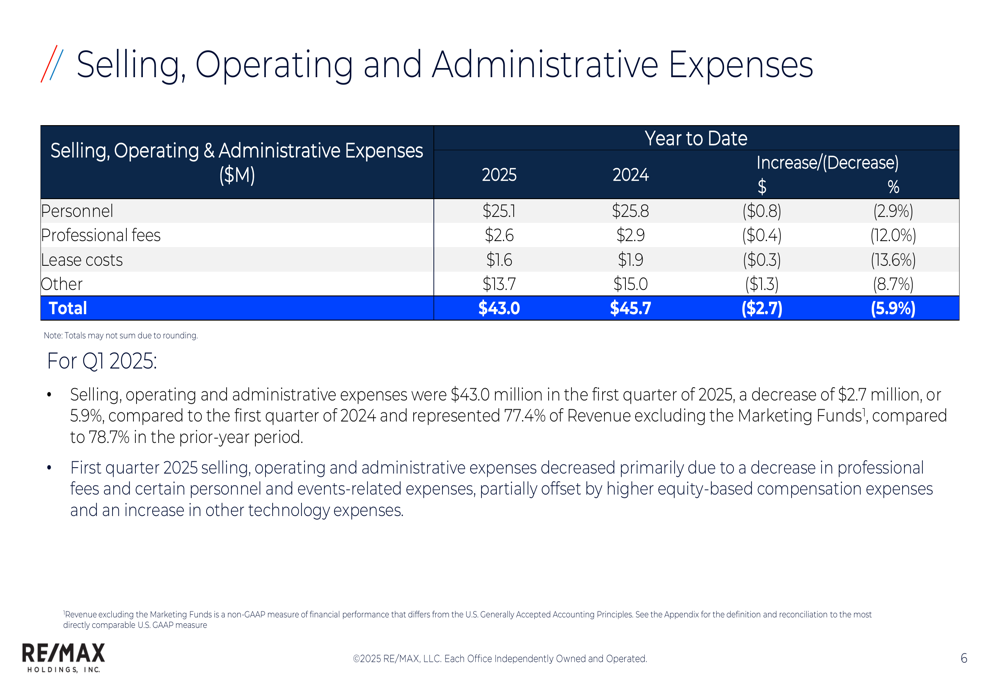

On the positive side, broker fees increased by 6.7% to $11.4 million, providing a partial offset to the revenue declines in other categories. The company also demonstrated effective cost control, with selling, operating, and administrative expenses decreasing by 5.9% to $43.0 million, compared to $45.7 million in Q1 2024.

As illustrated in the expense breakdown:

The combination of cost reductions and revenue mix shifts contributed to the improvement in Adjusted EBITDA and margin expansion, despite the overall revenue decline:

RE/MAX maintained a solid financial position with a cash balance of $89.1 million as of March 31, 2025, though this was down $7.5 million from December 31, 2024. The company reported $439.9 million in outstanding debt with no revolving loans outstanding, resulting in a Total (EPA:TTEF) Debt / TTM Adjusted EBITDA ratio of 4.5:1 and a Net Debt / TTM Adjusted EBITDA ratio of 3.6:1.

Strategic Initiatives

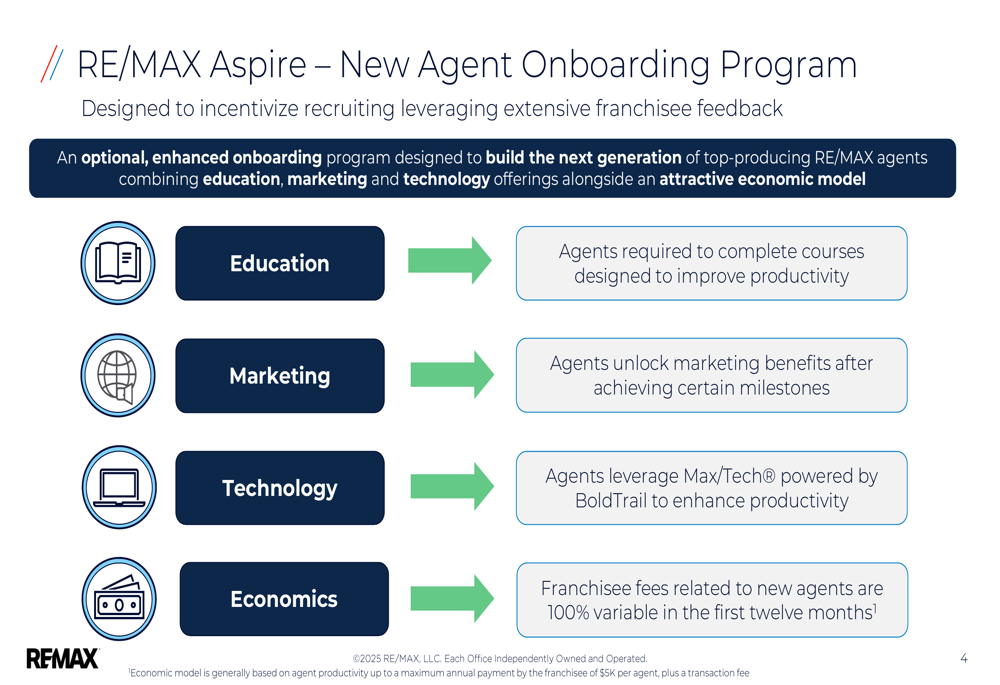

In response to agent recruitment and retention challenges in the U.S. market, RE/MAX introduced the "RE/MAX Aspire" program, which combines education, marketing, and technology offerings with an attractive economic model designed to build the next generation of top-producing agents.

The program’s key components are outlined below:

The company continues to position itself as a leading dual-brand franchisor with RE/MAX and Motto Mortgage, emphasizing its global footprint and brand strength:

However, Motto Mortgage also faced challenges, with open offices decreasing by 7.8% year-over-year to 224 offices as of March 31, 2025.

Forward-Looking Statements

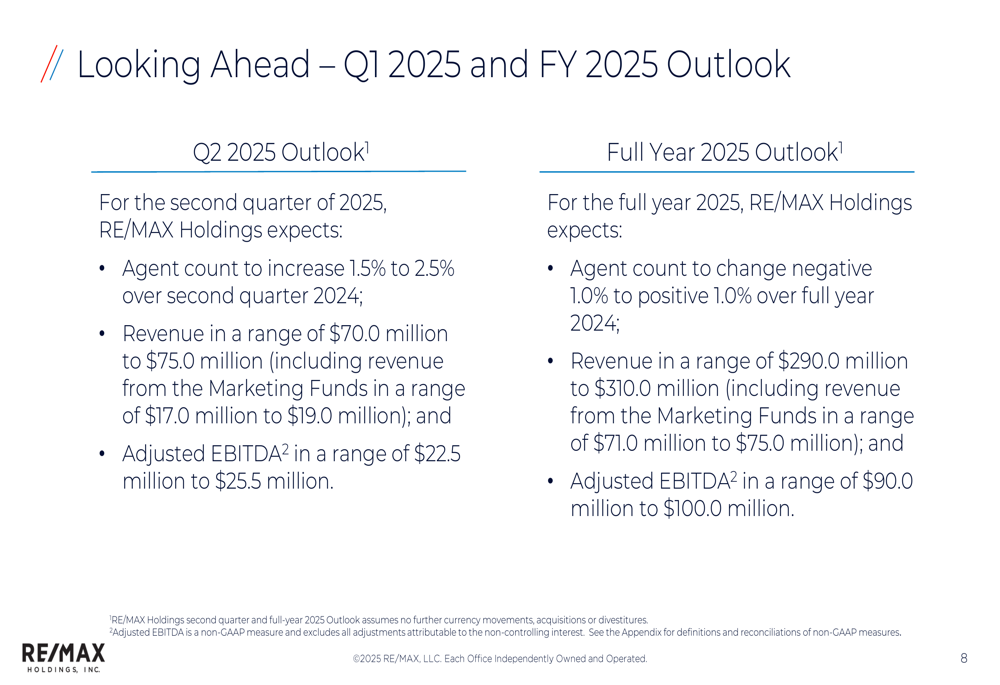

For Q2 2025, RE/MAX expects agent count to increase by 1.5% to 2.5% over Q2 2024, with revenue projected between $70.0 million and $75.0 million. Adjusted EBITDA is expected to range from $22.5 million to $25.5 million.

For the full year 2025, the company provided the following outlook:

The full-year guidance reflects cautious optimism, with agent count expected to range from a 1.0% decrease to a 1.0% increase compared to FY 2024. Revenue is projected between $290.0 million and $310.0 million, with Adjusted EBITDA between $90.0 million and $100.0 million.

These projections come against a backdrop of industry forecasts showing gradual improvement in housing market conditions, with existing home sales expected to increase from approximately 4.07 million in 2024 to 4.24 million in 2025 and 4.5 million in 2026, according to forecasts from Fannie Mae (OTC:FNMA) and the Mortgage Bankers Association.

The Q1 2025 results represent a slight sequential decline from Q4 2024, when the company reported Adjusted EBITDA of $23.3 million with a 32.2% margin. However, the Q1 2025 revenue of $74.5 million falls within the guidance range of $71-76 million provided during the Q4 2024 earnings call, while the 2.0% year-over-year agent count growth is at the high end of the previously guided 1-2% range.

RE/MAX shares closed at $7.79 on May 1, 2025, and gained 1.83% during the regular trading session before the earnings release. The stock is trading significantly below its 52-week high of $14.31, reflecting ongoing investor concerns about the company’s growth trajectory amid challenging housing market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.