SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Repay Holdings Corporation (NASDAQ:RPAY) released its Q1 2025 earnings presentation on May 12, 2025, revealing a 4% year-over-year decline in revenue amid mixed segment performance. The payment processing company, which specializes in electronic payment solutions for consumer loans and business payments, reported continued growth in its Business Payments segment while facing headwinds in its larger Consumer Payments division.

The company’s stock traded at $4.09 in after-hours trading, up 1.24% following the earnings release, suggesting investors were somewhat encouraged by the company’s outlook for sequential improvement throughout the remainder of 2025 despite the challenging quarter.

Quarterly Performance Highlights

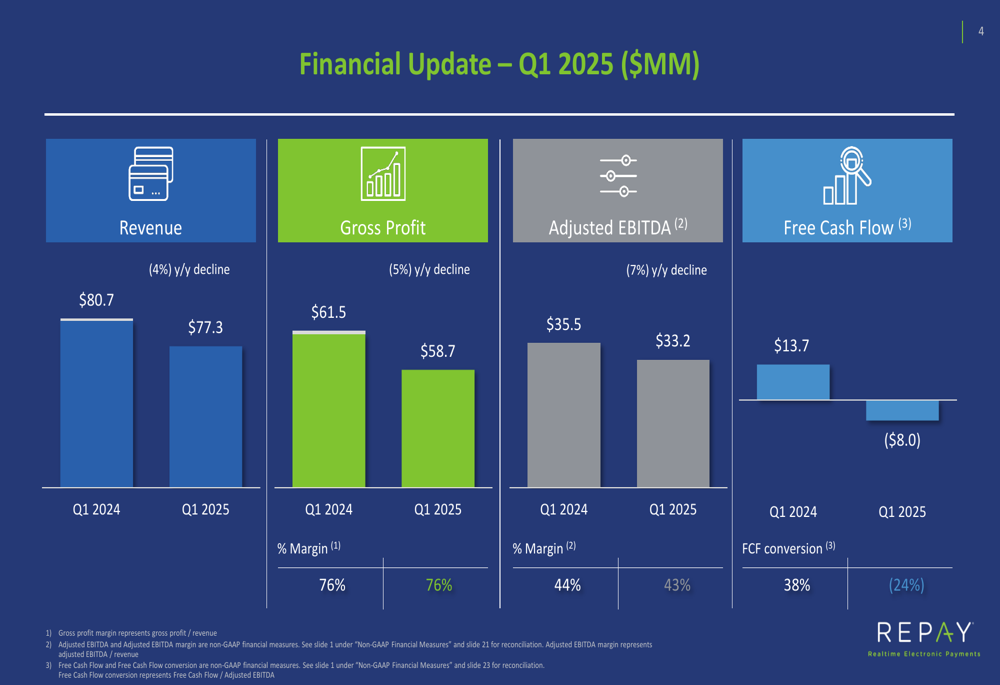

REPAY reported Q1 2025 revenue of $77.3 million, down 4% from $80.7 million in Q1 2024. Gross profit declined 5% to $58.7 million, while maintaining a 76% margin. Adjusted EBITDA fell 7% to $33.2 million with a 43% margin, down slightly from 44% in the prior year period.

As shown in the following chart of REPAY’s Q1 2025 financial results:

The most significant decline was in Free Cash Flow, which turned negative at -$8.0 million compared to positive $13.7 million in Q1 2024. The FCF conversion rate plummeted to -24% from 38% in the prior year period. The company attributed this decline primarily to the reversal of net working capital timing and one-off client losses.

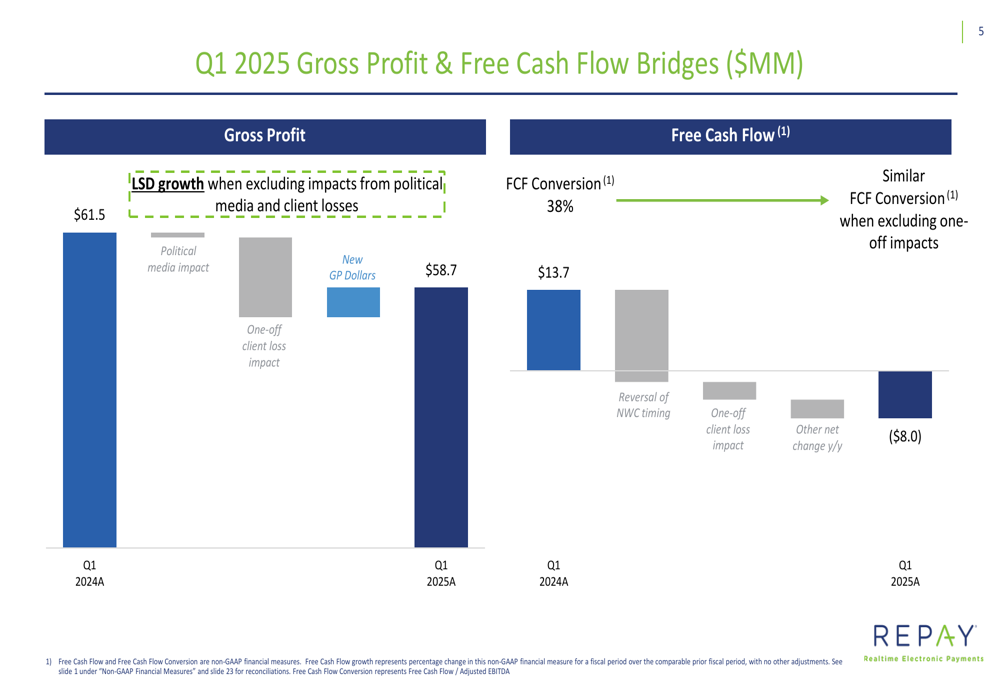

The following bridge chart illustrates the factors affecting Gross Profit and Free Cash Flow:

Segment Performance Analysis

REPAY’s performance varied significantly between its two business segments. The Consumer Payments segment, which represents the majority of the company’s business, experienced a 6% year-over-year revenue decline to $71.9 million, with gross profit falling 5% to $56.7 million. The company cited approximately 6 percentage points of gross profit growth headwind from client losses, though it maintained resilient trends across auto loans, personal loans, credit unions, and mortgage servicing.

The Consumer Payments segment results are detailed in the following chart:

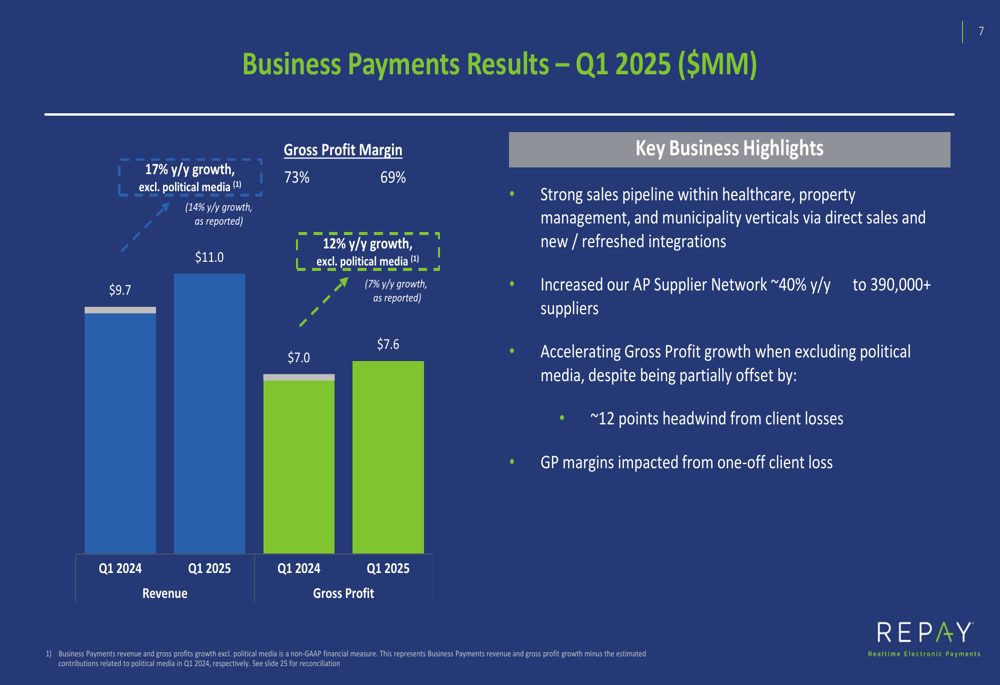

In contrast, the Business Payments segment showed strong growth, with revenue increasing 14% year-over-year (17% excluding political media) to $11.0 million. Gross profit in this segment rose 7% (12% excluding political media) to $7.6 million, though margins contracted from 73% to 69% due to one-off client losses.

The company highlighted the expansion of its AP Supplier Network by approximately 40% year-over-year to over 390,000 suppliers, and noted a strong sales pipeline within healthcare, property management, and municipality verticals.

Balance Sheet and Liquidity

REPAY maintained a solid balance sheet with $165 million in cash as of March 31, 2025, though this represented a decrease from $190 million a year earlier. Total (EPA:TTEF) liquidity stood at $415 million, down from $440 million in Q1 2024.

The company reported total debt of $508 million, resulting in net debt of $343 million and a net leverage ratio of 2.5x based on last twelve months Adjusted EBITDA of $138 million. REPAY’s debt structure includes $220 million in 2026 Convertible Notes with a 0% coupon and $288 million in 2029 Convertible Notes with a 2.875% coupon.

The following chart details REPAY’s balance sheet flexibility and leverage position:

Strategic Initiatives and Growth Outlook

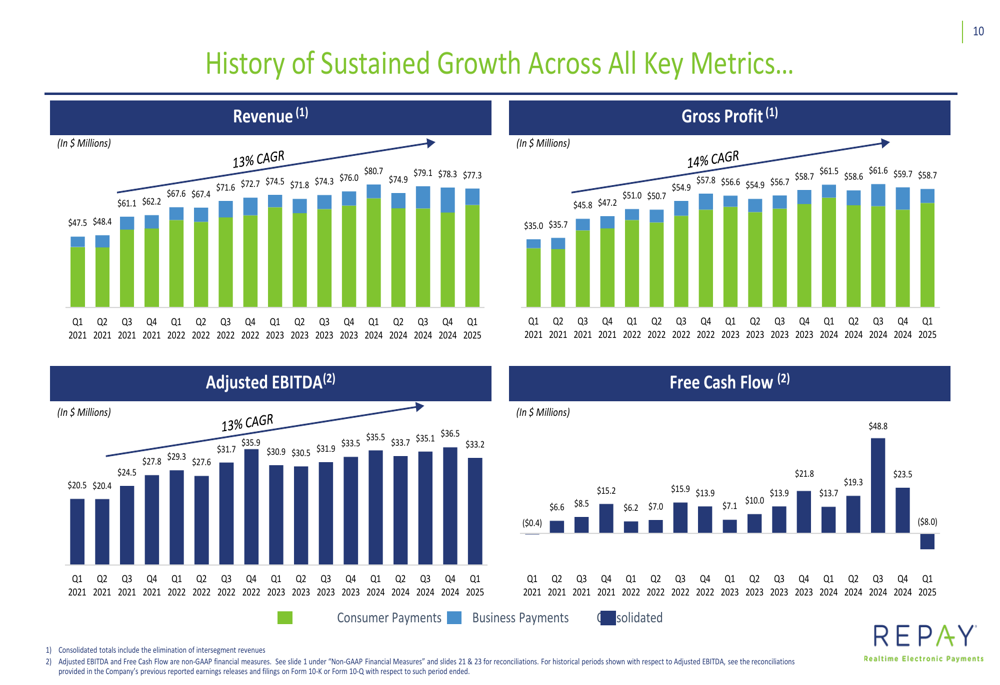

Despite the challenging quarter, REPAY emphasized its long-term growth trajectory, highlighting a 13-14% CAGR across key financial metrics from Q1 2021 to Q1 2025. The company outlined multiple levers to drive future growth, including expanding usage within existing clients, acquiring new clients in current verticals, enhancing software partnerships, and pursuing strategic M&A opportunities.

REPAY’s addressable market remains substantial, with a total opportunity of approximately $5.6 trillion across its Consumer Payments ($2.4 trillion) and Business Payments ($3.2 trillion) segments. The company maintains 283 software partner relationships and serves 343 credit union clients as of Q1 2025.

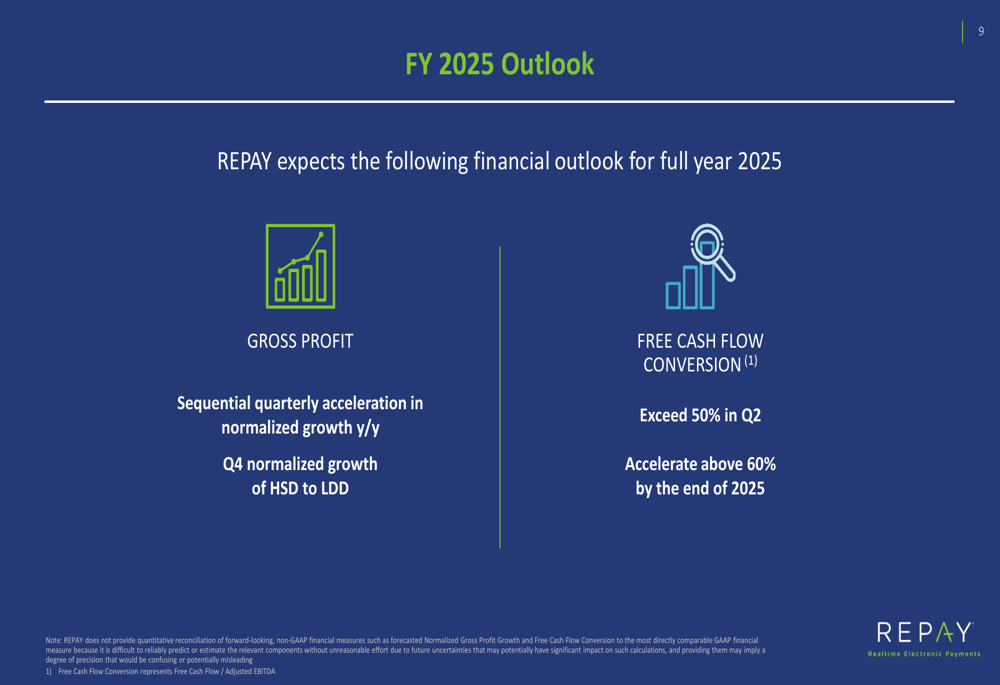

For the full year 2025, REPAY expects sequential quarterly acceleration in normalized gross profit growth year-over-year, with Q4 normalized growth reaching high single digits to low double digits. The company also forecasts Free Cash Flow conversion to exceed 50% in Q2 and accelerate above 60% by the end of 2025, a significant improvement from the -24% reported in Q1.

The following chart illustrates REPAY’s history of sustained growth across key metrics:

Forward-Looking Statements

Looking ahead, REPAY’s management expressed confidence in the company’s ability to return to growth through both execution within its existing business and broadening its addressable market. The company is focusing on operational efficiencies while continuing to invest in expanding its payment capabilities and vertical reach.

"We remain committed to optimizing payment flows and enhancing operational efficiency to drive profitable growth," stated the company in its presentation. "The secular trends towards frictionless digital payments continue to serve as a tailwind for our business."

REPAY’s gross profit margins and free cash flow conversion have shown variability over time, as illustrated in the following chart:

While Q1 2025 presented challenges, particularly in free cash flow conversion, the company’s expectation for sequential improvement throughout the year suggests management believes the current quarter represents a temporary setback rather than a long-term trend. Investors will be watching closely to see if REPAY can deliver on its projections for accelerating growth and improved cash flow conversion in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.