Street Calls of the Week

Introduction & Market Context

Repay Holdings Corp (NASDAQ:RPAY) released its Q2 2025 earnings presentation on August 11, 2025, revealing mixed financial results with modest revenue growth but declining profitability metrics. The payment processing company, which specializes in loan repayments and B2B payment solutions, demonstrated significant improvement in free cash flow generation despite ongoing challenges from one-off client losses.

The company’s stock closed at $5.15 on August 11, up 4.08% for the day, but fell 1.75% in after-hours trading following the earnings release. RPAY has traded between $3.59 and $9.75 over the past 52 weeks, indicating continued volatility as the company navigates its growth strategy.

Quarterly Performance Highlights

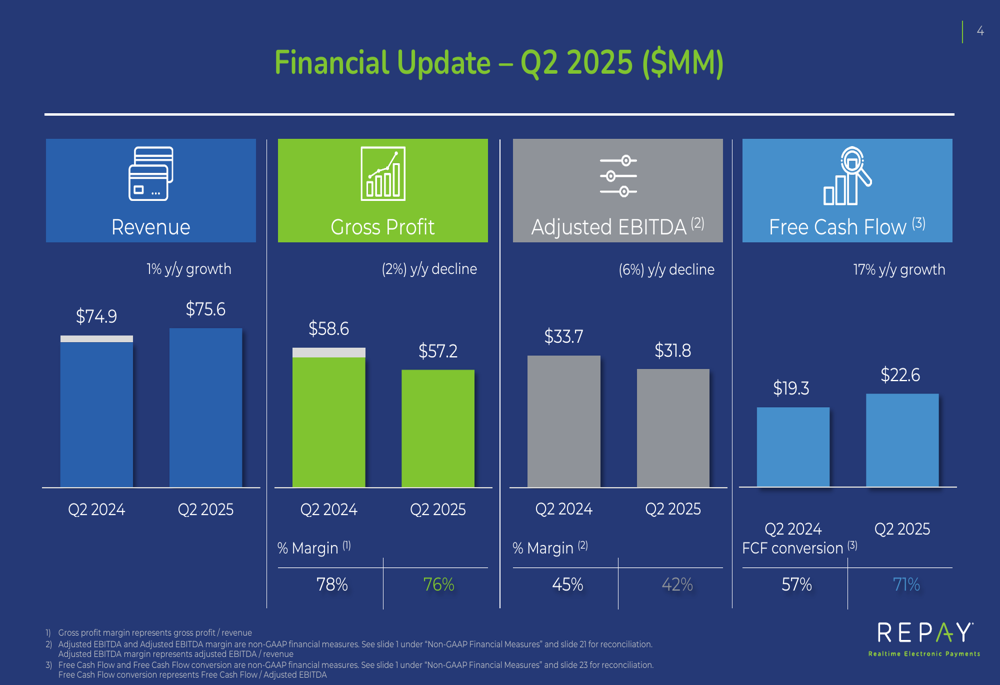

Repay reported Q2 2025 revenue of $75.6 million, representing a modest 1% year-over-year increase from $74.9 million in Q2 2024. However, gross profit declined 2% to $57.2 million, down from $58.6 million in the prior year period. Adjusted EBITDA also decreased by 6% to $31.8 million, compared to $33.7 million in Q2 2024.

The following chart illustrates these key financial metrics:

Despite the profitability challenges, REPAY demonstrated strong cash flow performance, with free cash flow increasing 17% year-over-year to $22.6 million, up from $19.3 million in Q2 2024. The company’s free cash flow conversion rate improved to 71%, indicating efficient capital management.

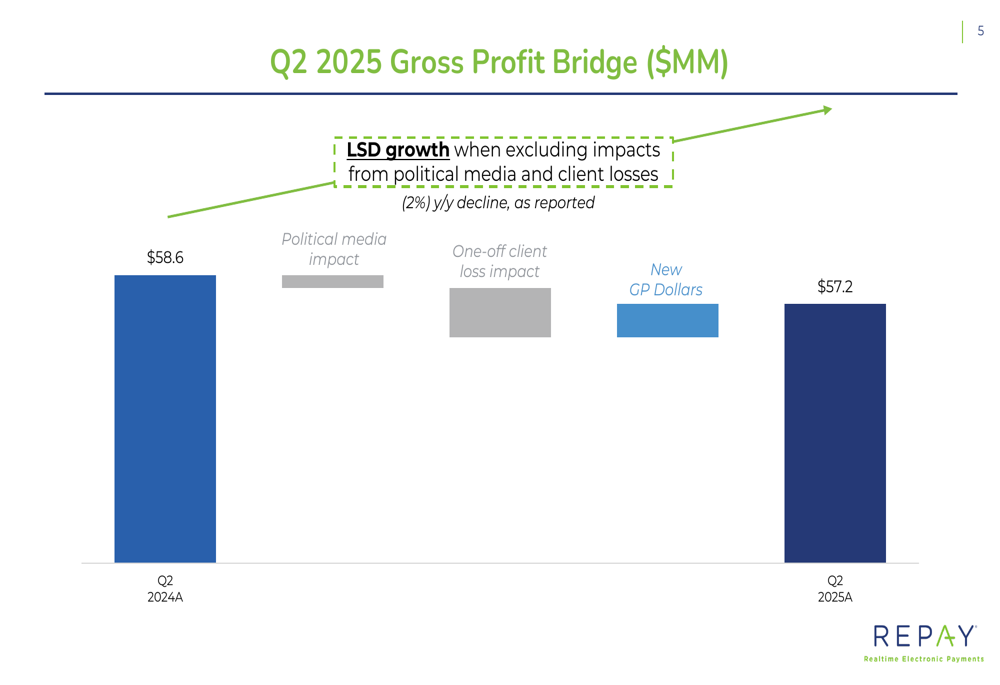

The presentation provided a detailed breakdown of the factors affecting gross profit performance, highlighting that one-off client losses and political media impact were the primary drivers of the year-over-year decline:

This represents a notable improvement from Q1 2025, when the company reported negative free cash flow of $8 million and missed earnings expectations with an EPS of negative $0.09 against a forecast of $0.22.

Segment Performance Analysis

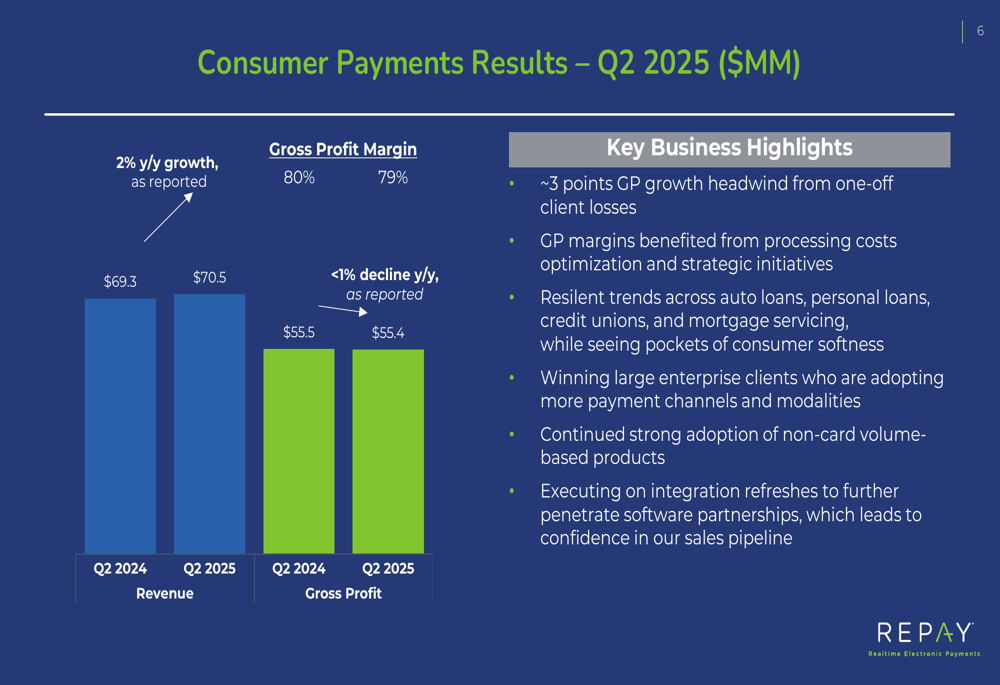

REPAY’s business is divided into two main segments: Consumer Payments and Business Payments. The Consumer Payments segment, which accounts for approximately 93% of total revenue, grew 2% year-over-year to $70.5 million in Q2 2025. However, gross profit remained essentially flat at $55.4 million compared to $55.5 million in the prior year period.

The company noted that Consumer Payments faced approximately 3 percentage points of gross profit growth headwind from one-off client losses, but benefited from processing cost optimization and strategic initiatives:

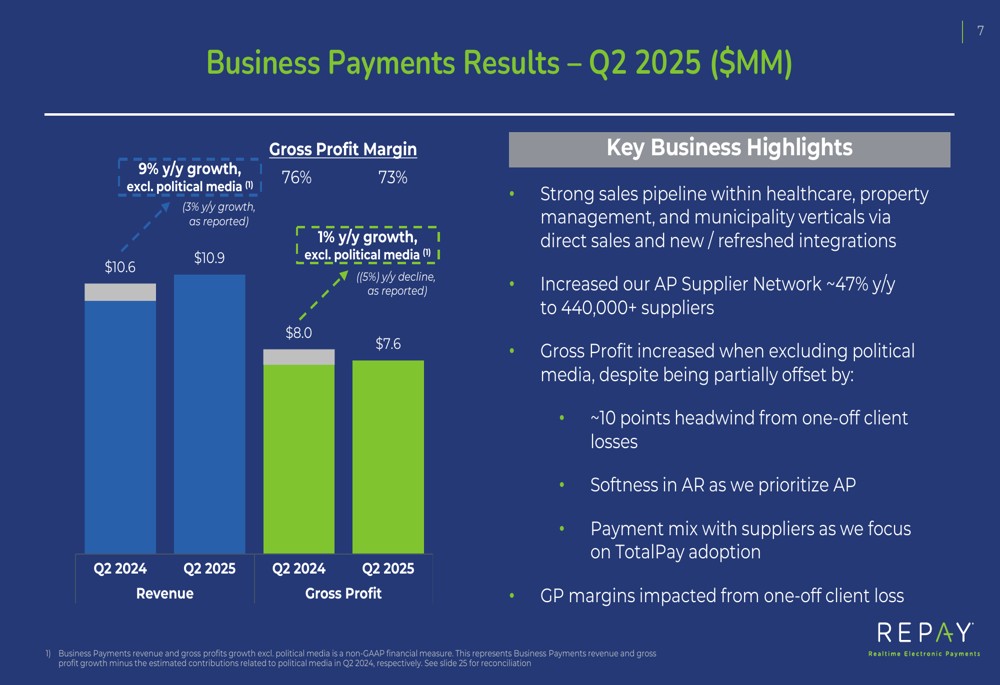

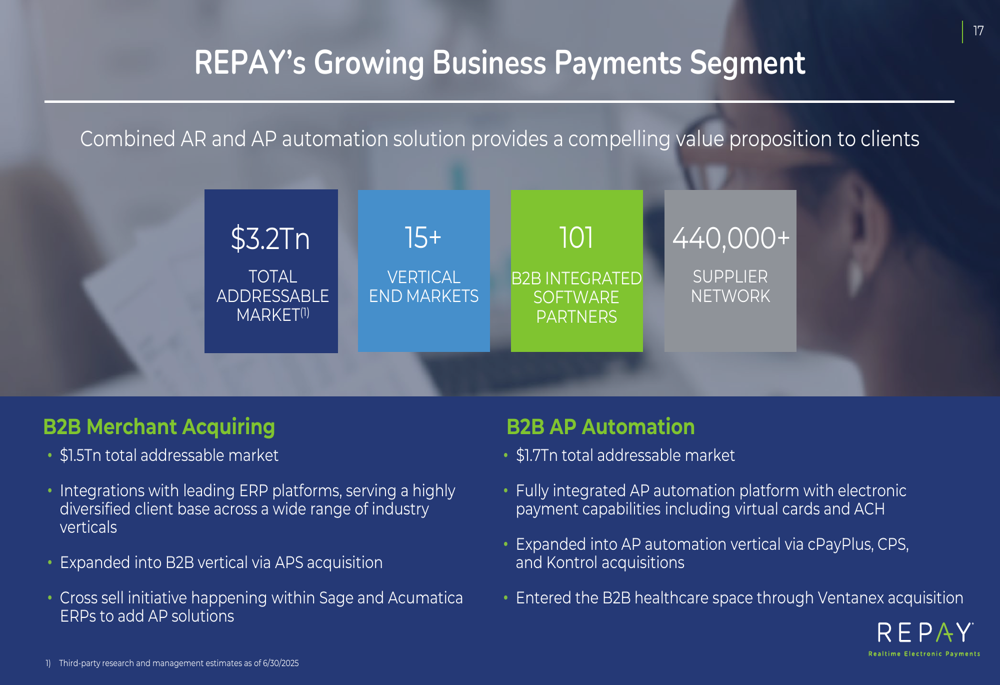

The Business Payments segment showed revenue growth of 3% year-over-year to $10.9 million, but when excluding political media impact, growth was more robust at 9%. Gross profit for this segment decreased to $7.6 million from $8.0 million in Q2 2024, though it increased when excluding political media effects:

A key highlight for the Business Payments segment was the 47% year-over-year expansion of REPAY’s AP Supplier Network to over 440,000 suppliers, demonstrating the company’s continued focus on scaling its B2B payment infrastructure.

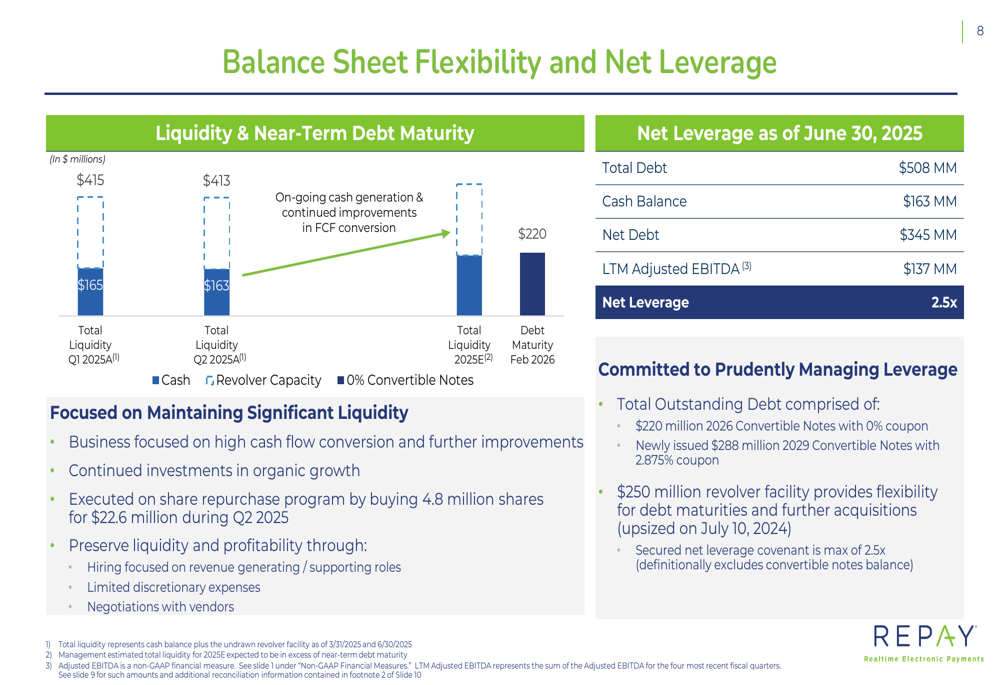

Balance Sheet and Liquidity Position

As of June 30, 2025, REPAY maintained a strong liquidity position with $413 million in total liquidity, including cash and revolver capacity. This represents a slight decrease from the $415 million reported at the end of Q1 2025. The company’s total debt stood at $508 million, with a cash balance of $163 million, resulting in net debt of $345 million and a net leverage ratio of 2.5x.

The following chart details the company’s balance sheet flexibility and leverage position:

During Q2 2025, REPAY executed on its share repurchase program, using $22.6 million to buy back 4.8 million shares. The company’s debt structure includes $220 million in 2026 Convertible Notes with 0% coupon, newly issued $288 million in 2029 Convertible Notes with 2.875% coupon, and a $250 million revolver facility.

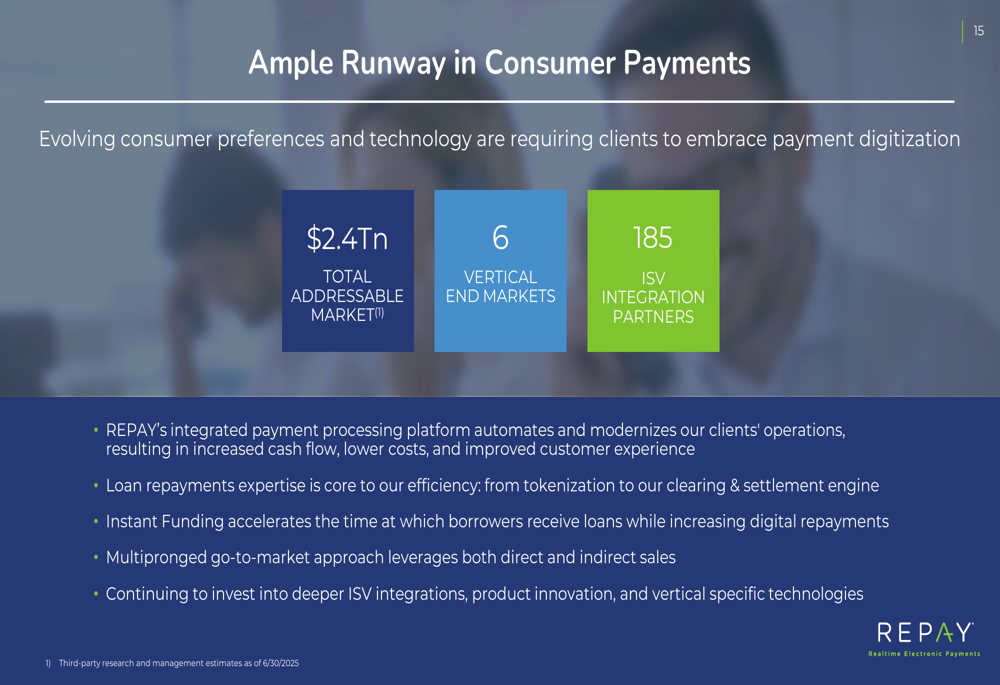

Strategic Initiatives and Outlook

REPAY reaffirmed its previously provided outlook for FY 2025, which includes sequential quarterly acceleration in normalized gross profit growth year-over-year, with Q4 normalized growth expected to reach high single digits to low double digits. The company also anticipates free cash flow conversion to accelerate above 60% by the end of 2025.

The company highlighted its multiple growth levers, focusing on both executing its existing business and broadening its addressable market:

REPAY continues to expand its payment capabilities across multiple channels and modalities, offering a comprehensive suite of solutions for both consumer and business payments:

For its Business Payments segment, which addresses a $3.2 trillion total addressable market across more than 15 vertical end markets, REPAY is positioning itself as a one-stop-shop B2B payments solutions provider:

In the earnings presentation, REPAY emphasized its commitment to "executing towards profitable growth, with a continued focus on optimizing payment flows and enhancing operational efficiency." The company also noted that it will "continue to take advantage of the many secular trends towards frictionless digital payments that have been, and will continue to be, a tailwind driving our business."

With its extensive network of 286 software partner relationships, 353 credit union clients, and expanding supplier network, REPAY appears positioned to leverage its integrated payment infrastructure to drive future growth, despite the near-term challenges from client losses and political media impacts that affected Q2 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.