Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

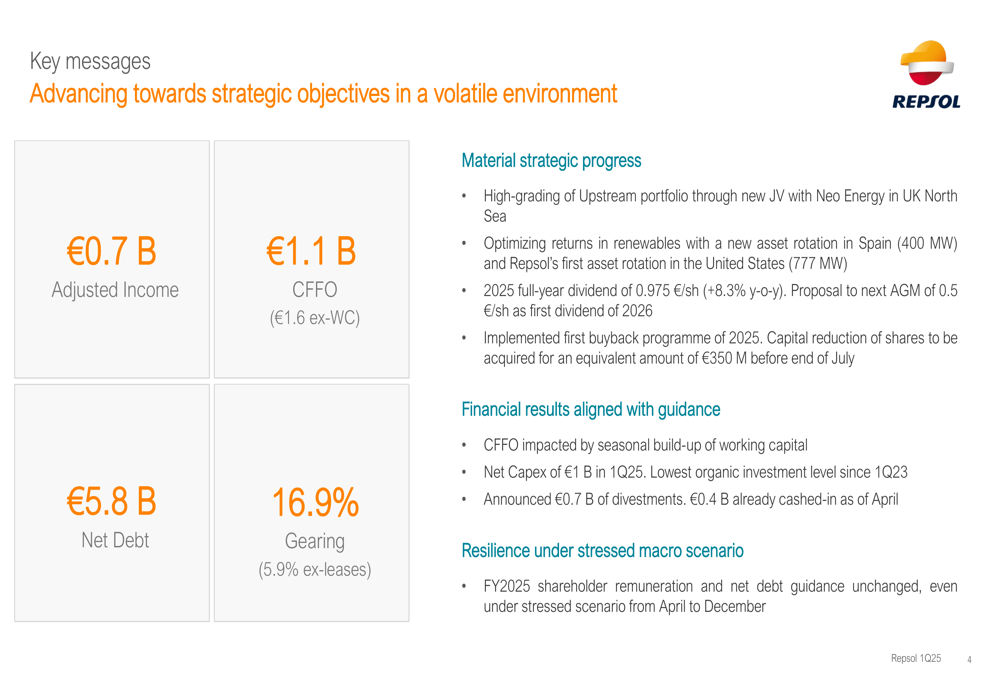

Repsol SA (BME:REP) presented its first quarter 2025 results on April 30, revealing an adjusted income of €651 million, significantly down from €1.27 billion in the same period last year. The Spanish energy company faced a challenging market environment with lower refining margins and reduced production volumes, though it maintained its full-year guidance and shareholder remuneration plans.

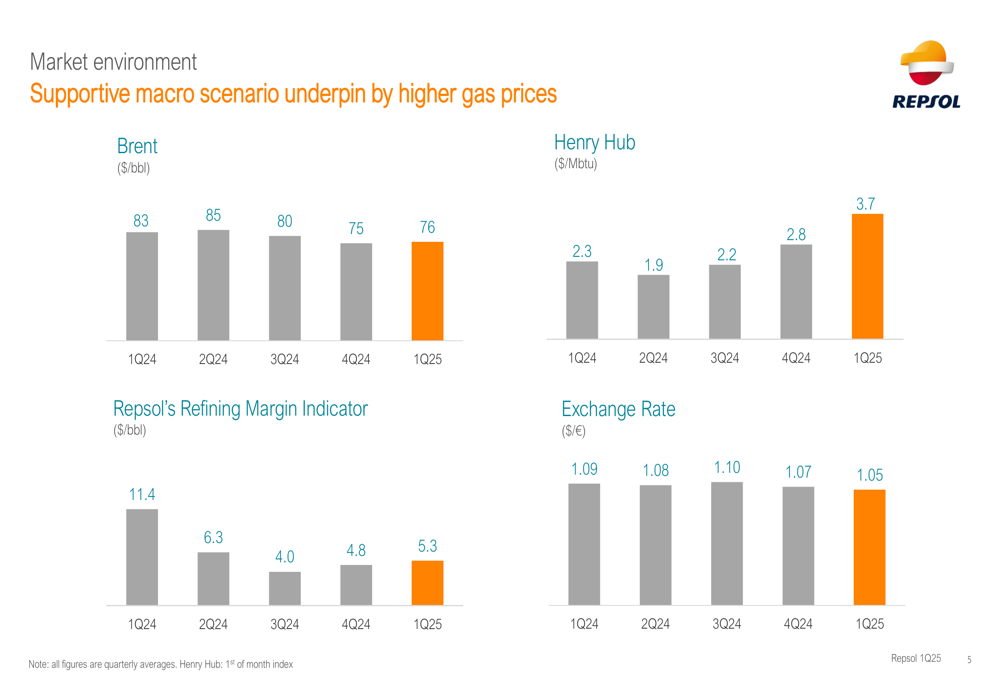

The quarter saw Brent crude prices average $76 per barrel, down from $83 in Q1 2024, while the company’s refining margin indicator stood at $5.3 per barrel, less than half the $11.4 recorded in the first quarter of last year. This market backdrop contributed to the pressure on the company’s industrial segment performance.

Quarterly Performance Highlights

Repsol reported cash flow from operations of €1.1 billion for the quarter, which rises to €1.6 billion when excluding working capital effects. The company’s net debt increased to €5.83 billion, up from €5.01 billion at the end of 2024 and €3.9 billion in Q1 2024. Gearing ratio stood at 16.9%, or 5.9% excluding leases.

The company’s overall adjusted income of €651 million remained relatively stable compared to the previous quarter (€643 million in Q4 2024), but represented a substantial 48.6% decline from the €1.27 billion reported in Q1 2024. This decline was primarily driven by the industrial segment’s performance.

Segment Analysis

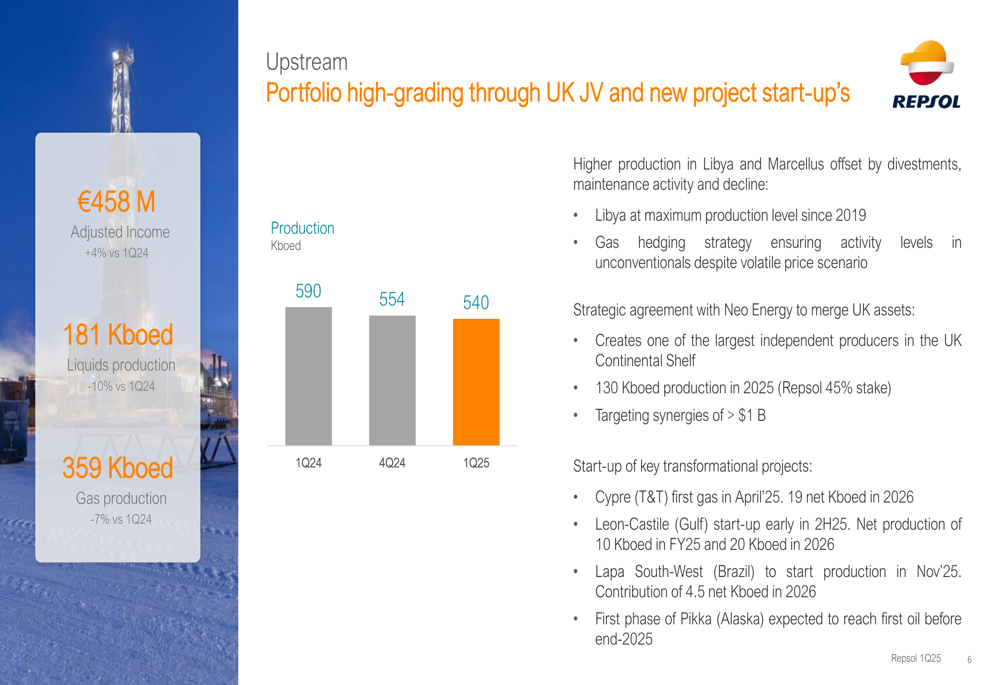

The Upstream segment delivered an adjusted income of €458 million, a modest 4% increase compared to Q1 2024, despite a 8.5% reduction in production to 540 thousand barrels of oil equivalent per day (kboed). The segment benefited from higher production in Libya and Marcellus, which partially offset the impact of divestments and natural field decline.

The Industrial segment saw the most significant decline, with adjusted income plummeting 82% year-over-year to €131 million. This sharp decrease reflects the substantially lower refining margins compared to the exceptional levels seen in early 2024. Processed crude volumes fell 7% to 10.2 million tons, affected by planned maintenance at the Bilbao, Tarragona, and Puertollano refineries.

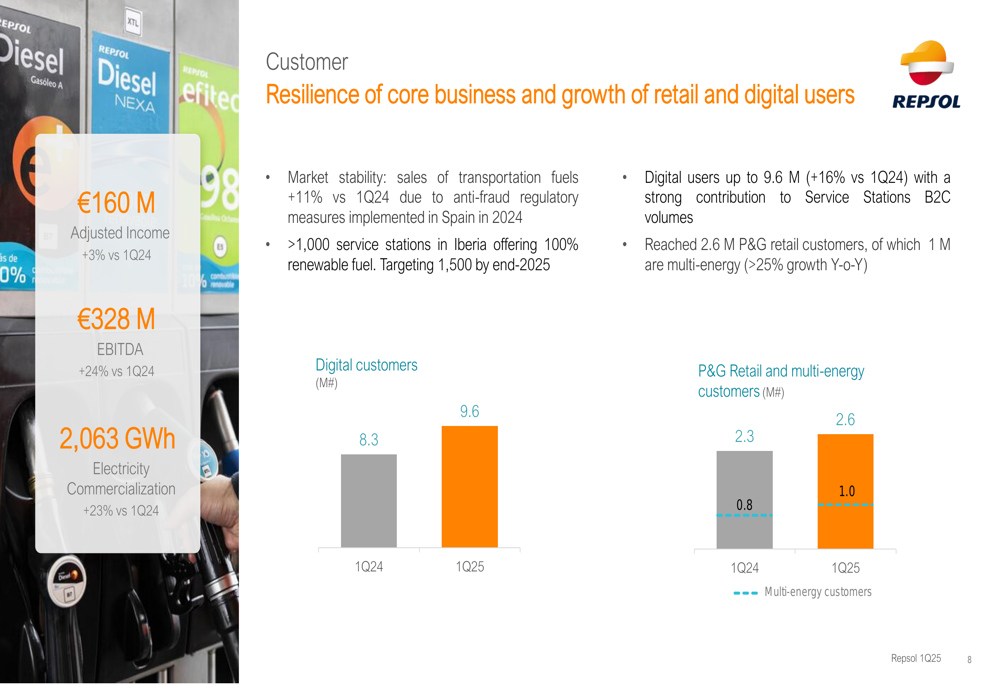

The Customer segment showed resilience with adjusted income of €160 million, up 3% from Q1 2024, and EBITDA growth of 24% to €328 million. Sales of transportation fuels increased 11% year-over-year, attributed to anti-fraud regulatory measures implemented in Spain. Digital users grew 16% to 9.6 million, while the company reached 2.6 million retail customers, with 1 million being multi-energy customers.

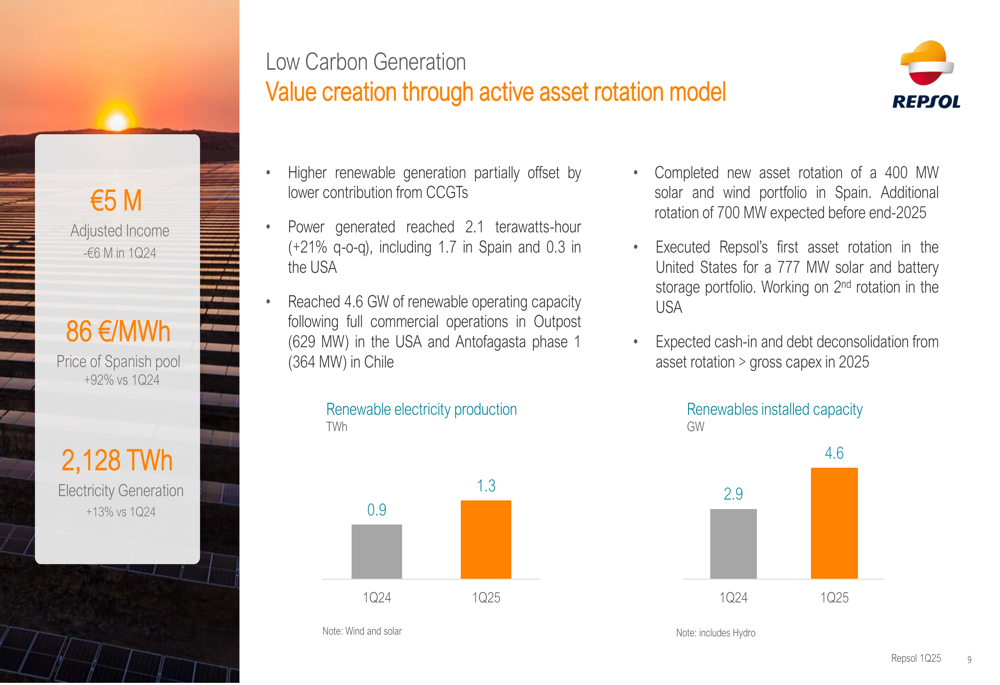

The Low Carbon Generation segment turned profitable with an adjusted income of €5 million, compared to a €6 million loss in Q1 2024. This improvement came despite challenging market conditions, supported by a 92% increase in Spanish electricity pool prices to 86 €/MWh. Renewable electricity generation increased 44% year-over-year to 1.3 TWh, while installed capacity grew to 4.6 GW from 2.9 GW a year earlier.

Strategic Initiatives

Repsol continued to advance its strategic portfolio optimization during the quarter. Key developments included:

1. A new joint venture with Neo Energy in the UK North Sea, creating one of the largest independent producers in the UK Continental Shelf with expected production of 130 kboed in 2025 (Repsol holds a 45% stake).

2. Asset rotation in renewables, including the completion of a 400 MW solar and wind portfolio sale in Spain and the company’s first asset rotation in the United States for a 777 MW solar and battery storage portfolio.

3. Progress on transformational upstream projects, including first gas at Cypre (Trinidad & Tobago) in April 2025, with Leon-Castile (Gulf of Mexico), Lapa South-West (Brazil), and the first phase of Pikka (Alaska) expected to come online later this year.

4. Expansion of renewable fuel offerings to over 1,000 service stations in Iberia, with a target of 1,500 by the end of 2025.

Outlook & Guidance

Despite the challenging start to the year, Repsol maintained its full-year 2025 guidance, projecting cash flow from operations of €6-6.5 billion and net capital expenditure of €3.5-4 billion. The company also confirmed its upstream production target of 530-550 kboed.

Shareholder remuneration plans remain unchanged, with a full-year dividend of 0.975 €/share (an 8.3% increase from 2024) and the implementation of a €350 million share buyback program to be completed before the end of July 2025. The company has also proposed a first dividend of 0.5 €/share for 2026 to be approved at the next Annual General Meeting.

Notably, Repsol presented an alternative "stressed scenario" with lower oil prices ($65/bbl Brent from April to December vs. base case of $75/bbl) and refining margins ($4/bbl vs. $6/bbl), under which it still expects to maintain its shareholder remuneration commitments.

The company’s stock closed at €10.84 on April 29, 2025, significantly below its 52-week high of €15.30, suggesting investors remain cautious about the company’s near-term prospects despite its strategic progress and commitment to shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.