China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Introduction & Market Context

Resolute Mining Ltd (ASX:RSG) released its Q3 2025 Activities Report on October 28, 2025, highlighting steady gold production despite cost pressures from higher royalties. The gold miner's stock fell 12.23% following the presentation, despite reporting a strong net cash position and progress on key growth projects across its West African operations.

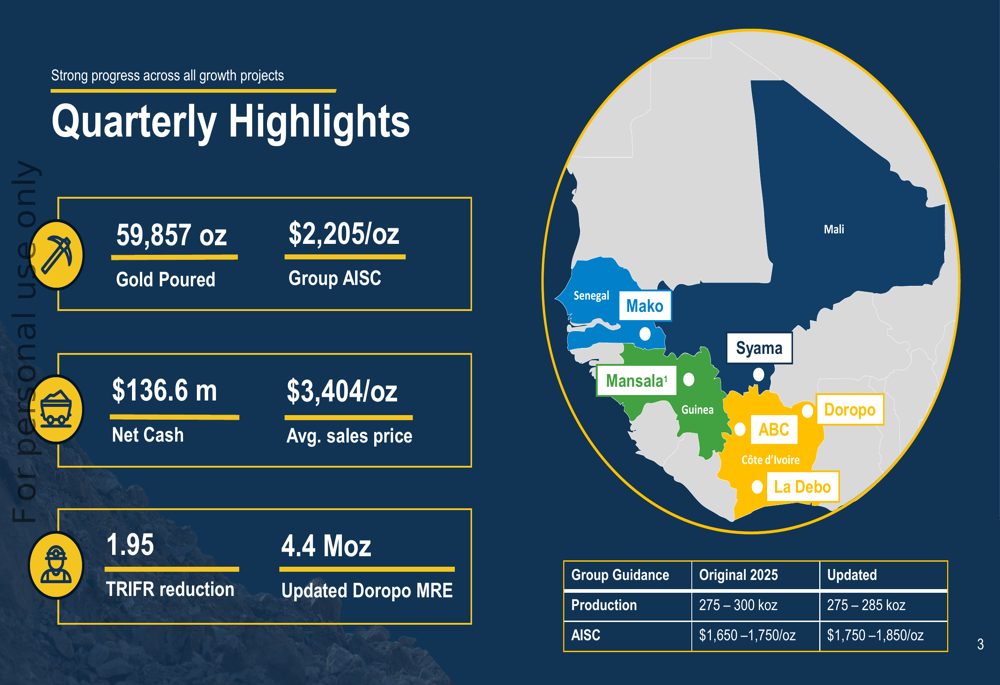

The company's presentation comes amid a period of elevated gold prices, with Resolute reporting an average sales price of $3,404/oz during the quarter. This favorable pricing environment has helped offset some of the cost increases experienced across its operations in Mali, Senegal, and Côte d'Ivoire.

Quarterly Performance Highlights

Resolute produced 59,857 ounces of gold during Q3 2025, bringing year-to-date production to 211,000 ounces. The company maintained its full-year production guidance of 275-285 koz but revised its All-In Sustaining Cost (AISC) guidance upward to $1,750-1,850/oz from the original $1,650-1,750/oz, primarily due to higher royalty expenses resulting from increased gold prices.

As shown in the following quarterly highlights:

The company's operations span multiple countries in West Africa, with its Syama mine in Mali contributing 39,918 ounces at an AISC of $2,358/oz during the quarter, while the Mako operation in Senegal delivered 19,939 ounces at a more favorable AISC of $1,415/oz. The group's overall AISC for Q3 was $2,205/oz, higher than the year-to-date average of $1,834/oz.

Financial Analysis

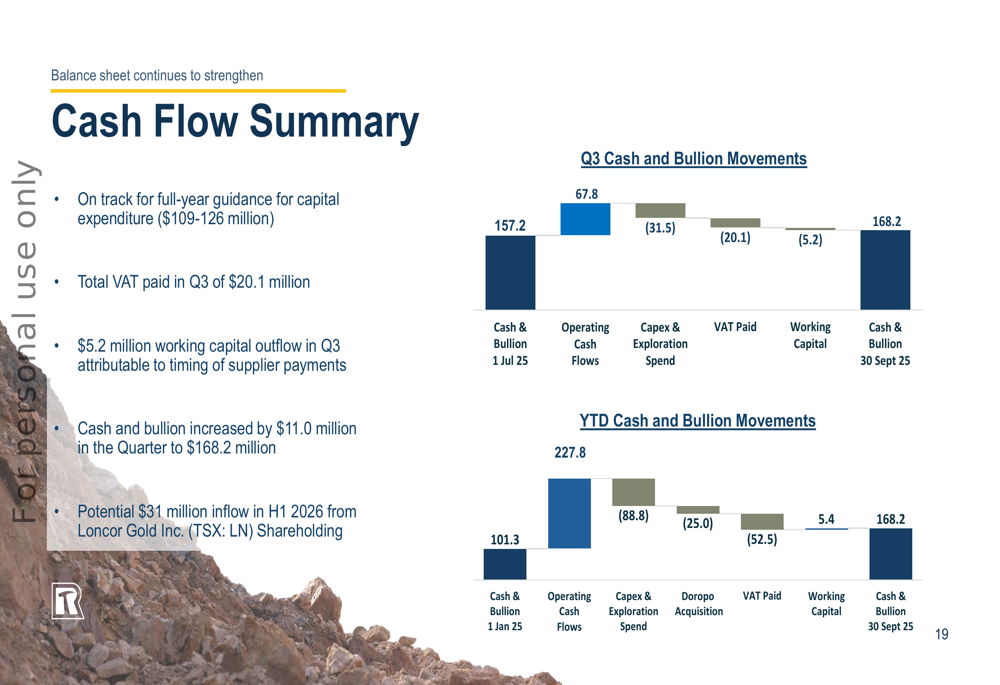

Resolute reported strong financial metrics for the quarter, with year-to-date revenue of $664.1 million and EBITDA of $292.8 million. The company generated operating cash flows of $227.8 million year-to-date, strengthening its balance sheet with a net cash position of $136.6 million as of quarter-end.

The following financial highlights illustrate the company's performance:

Cash and bullion increased by $11.0 million during the quarter to reach $168.2 million, despite significant capital expenditure and working capital outflows. The company paid $20.1 million in VAT during Q3 and experienced a $5.2 million working capital outflow.

The cash flow waterfall chart below demonstrates these movements:

Resolute remains on track for its full-year capital expenditure guidance of $109-126 million, with significant investments directed toward growth projects, particularly the Syama Sulphide Conversion Project in Mali. The company also noted a potential $31 million inflow in H1 2026 from its shareholding in Loncor Gold Inc. (TSX:LN).

Strategic Growth Initiatives

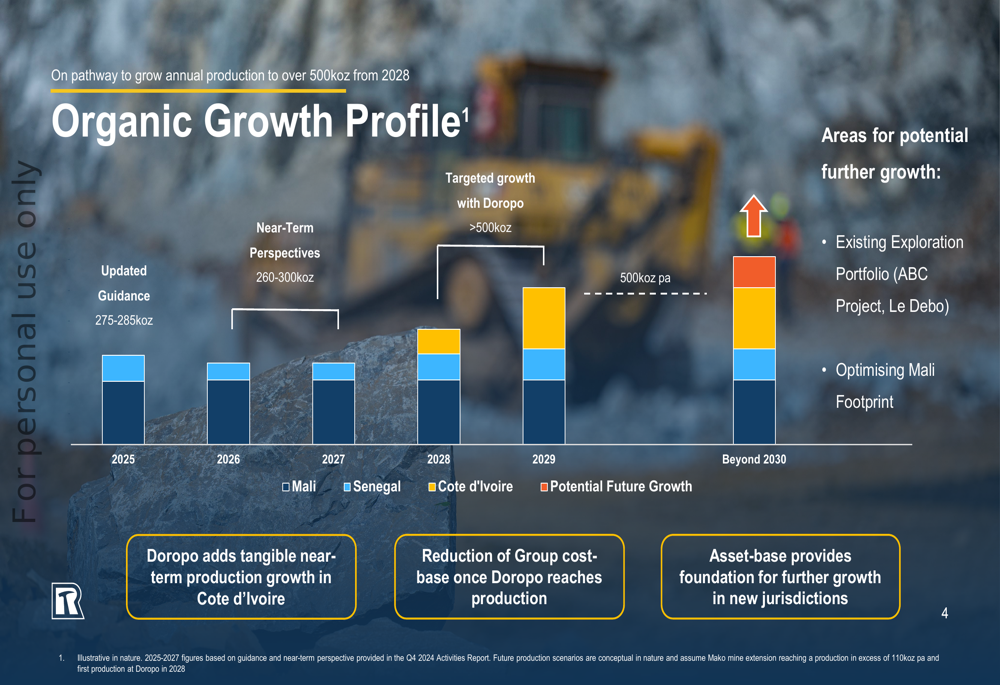

Resolute's presentation emphasized its organic growth strategy, outlining a clear pathway to increase annual gold production to over 500,000 ounces by 2028. This growth trajectory is built on several key projects across its portfolio.

The company's growth profile is illustrated in the following chart:

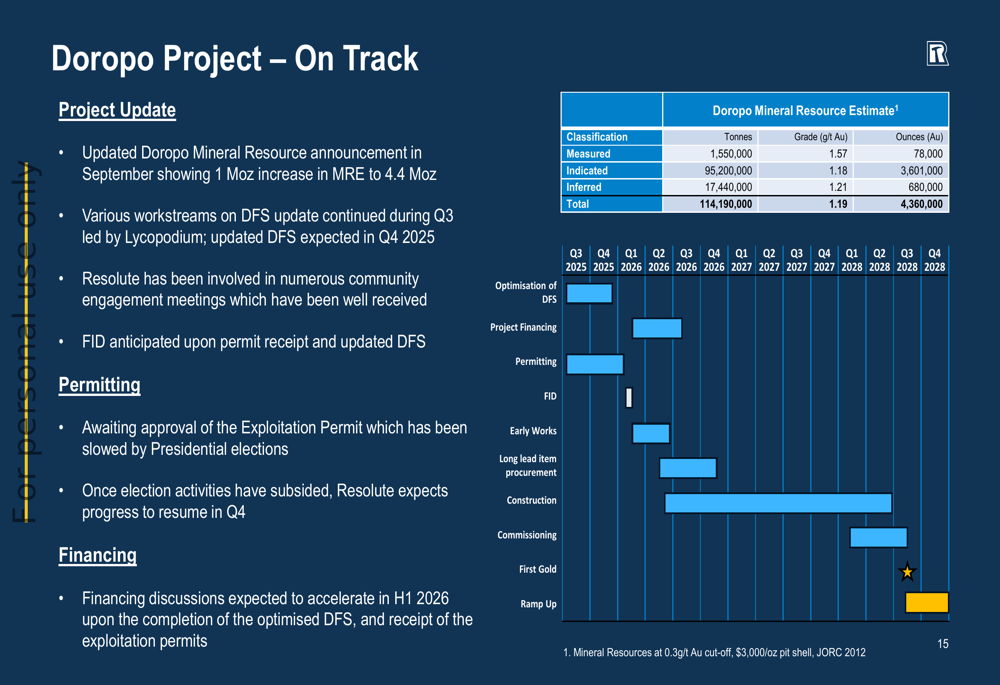

A cornerstone of this growth strategy is the Doropo Project in Côte d'Ivoire, which recently saw its Mineral Resource Estimate increase by 1 million ounces to 4.4 million ounces. The updated Definitive Feasibility Study for Doropo is expected in Q4 2025, with financing discussions anticipated to accelerate in H1 2026.

The Doropo Project timeline and resource estimate are shown below:

In Mali, the Syama Sulphide Conversion Project is progressing on time and budget, with year-to-date capital expenditure of $20.7 million. The project is expected to start treating sulphide ore at half throughput in Q1 2026, with full ramp-up from Q3 2026. Resolute anticipates that annual gold production will exceed original guidance once the project is fully operational.

In Senegal, the company is advancing the Mako Life Extension Project, which includes the Tomboronkoto and Bantaco Projects. With a current Mineral Resource Estimate of over 600,000 ounces, Resolute believes this initiative has the potential to extend mining activities in Senegal by an additional five to ten years.

Forward-Looking Statements

Resolute's management expressed confidence in meeting its revised 2025 production guidance while continuing to advance its strategic growth initiatives. The company summarized its position and outlook as follows:

CEO Chris Eger emphasized during the earnings call that Resolute is "very much on a pathway to deliver targeted annual production of over 500,000 ounces from 2028," highlighting the company's commitment to long-term growth despite near-term cost pressures.

The company faces several challenges, including supply chain disruptions affecting explosive supplies at the Syama site in Mali and VAT receivables issues that could impact cash flow. However, management remains focused on geographical diversification and establishing additional operating mines in new jurisdictions to mitigate country-specific risks.

With a strong cash position, advancing growth projects, and a clear strategic vision, Resolute appears well-positioned to execute its growth strategy while navigating the current cost environment. Investors will be closely watching the progress of key projects, particularly the Syama Sulphide Conversion Project and the Doropo development, as critical indicators of the company's ability to achieve its ambitious production targets for 2028 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.