EU and US could reach trade deal this weekend - Reuters

Introduction & Market Context

Revolve Group (NYSE:RVLV) released its Q1 2025 financial results on May 6, showing solid growth across key metrics, though investors responded with caution. The fashion e-commerce company reported a 10% year-over-year increase in net sales to $296.7 million, alongside improved profitability metrics. Despite these positive results, Revolve’s stock fell 8.13% to $17.40 in after-hours trading, continuing a pattern seen in previous quarters where strong results failed to impress investors.

The company’s current stock price sits significantly closer to its 52-week low of $14.87 than its high of $39.58, reflecting ongoing market skepticism despite Revolve’s consistent financial improvements.

Quarterly Performance Highlights

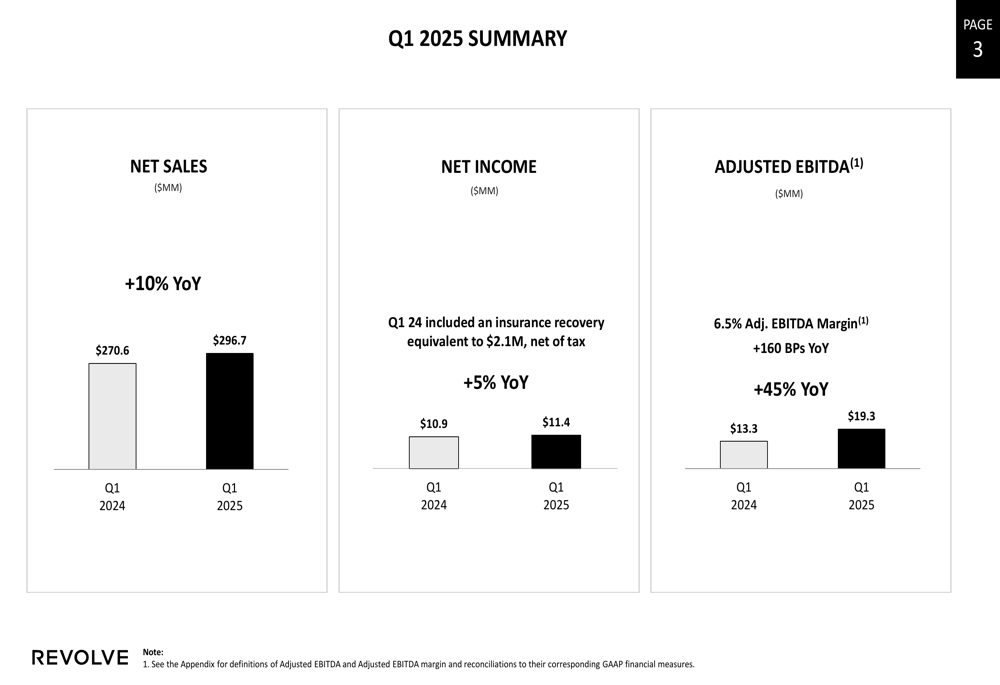

Revolve reported net sales of $296.7 million for Q1 2025, representing a 10% increase from $270.6 million in the same period last year. Net income grew 5% year-over-year to $11.4 million, while Adjusted EBITDA reached $19.3 million with a margin of 6.5%, marking a significant 160 basis point improvement from Q1 2024.

As shown in the following summary of Q1 2025 financial results:

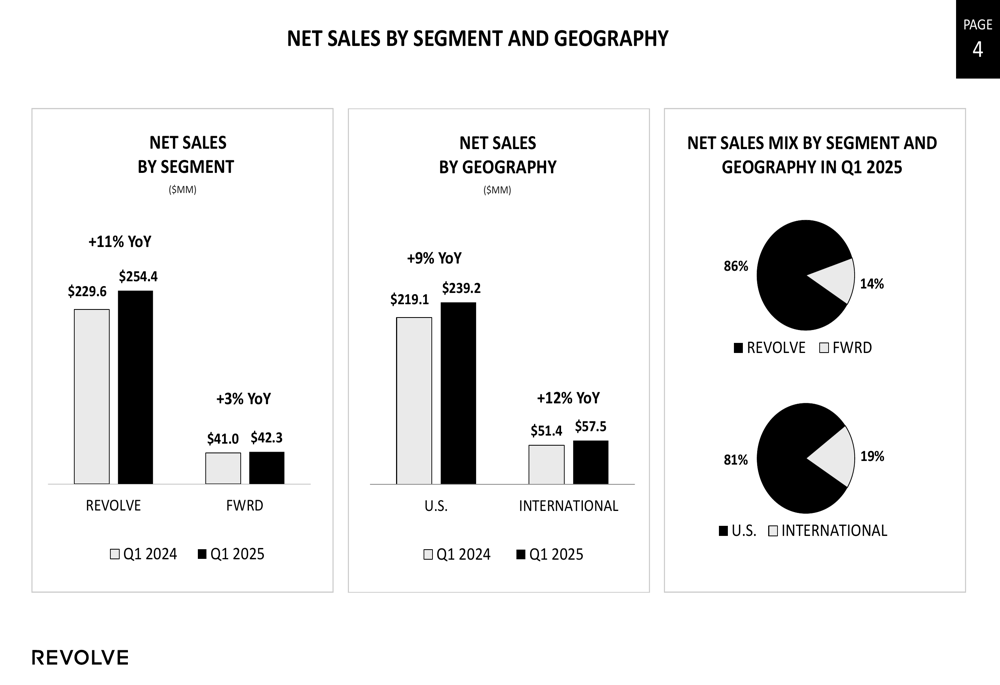

The company’s performance was driven by growth across both of its primary segments. The core REVOLVE segment generated $254.4 million in net sales, an 11% year-over-year increase, while the luxury-focused FWRD segment contributed $42.3 million, up 3% from Q1 2024. Notably, international sales grew at a faster rate than domestic, increasing 12% year-over-year to $57.5 million, compared to 9% growth in U.S. sales, which reached $239.2 million.

The following breakdown illustrates Revolve’s sales distribution by segment and geography:

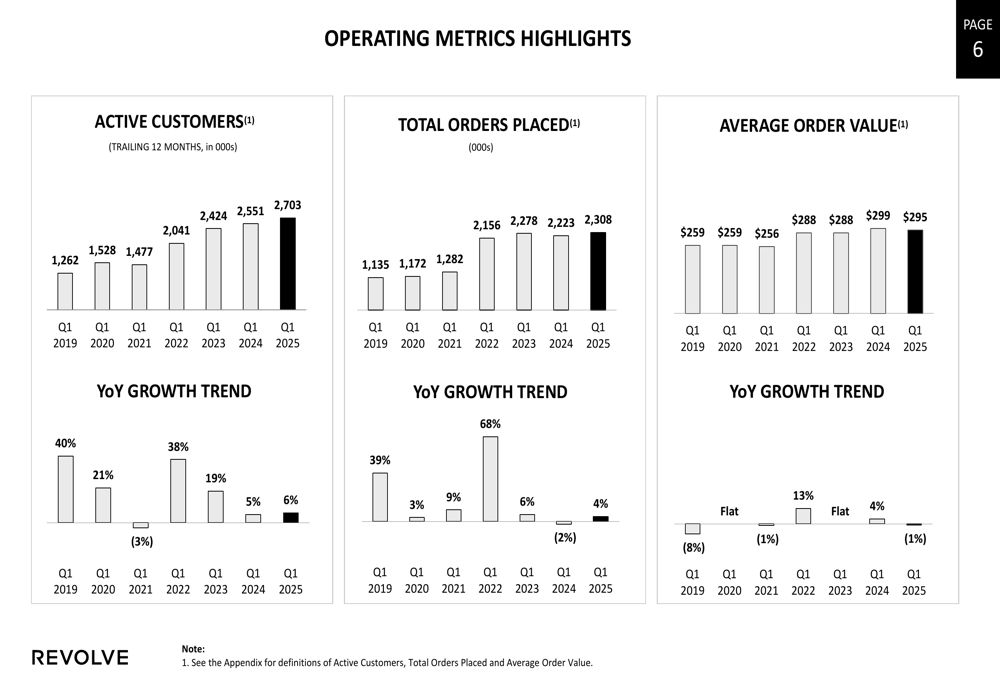

Customer metrics also showed positive momentum, with active customers (measured on a trailing 12-month basis) increasing 6% year-over-year to 2.7 million. Total (EPA:TTEF) orders placed grew 4% to 2.3 million, though average order value declined slightly by 1% to $295.

The following chart details these key operating metrics:

Detailed Financial Analysis

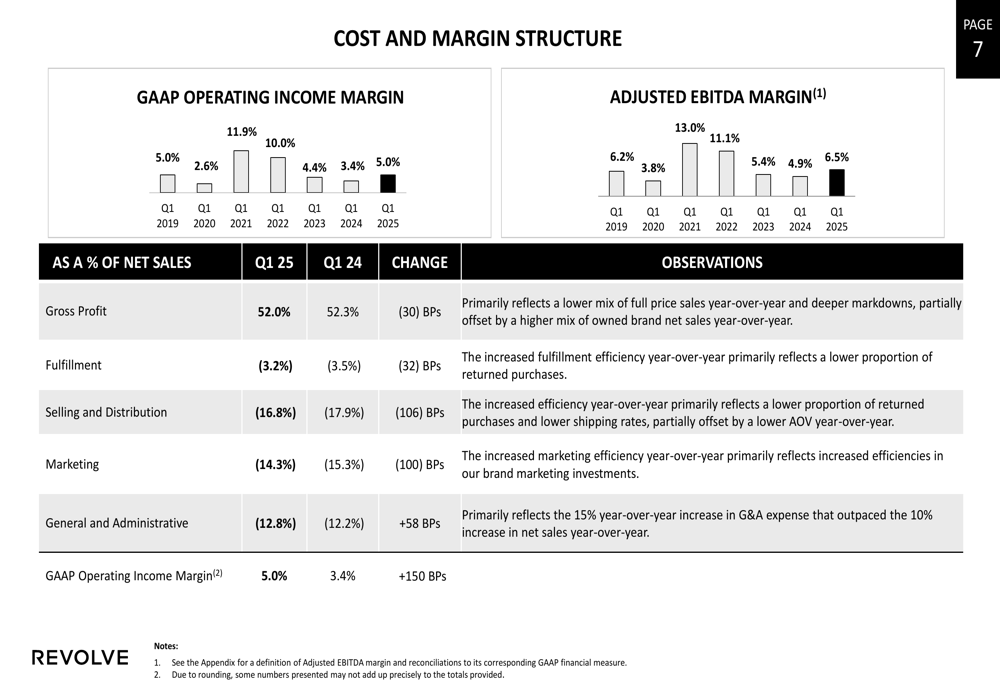

Revolve demonstrated significant margin improvement in Q1 2025. The company’s GAAP operating income margin expanded to 5.0% from 3.4% in Q1 2024, while Adjusted EBITDA margin increased to 6.5% from 4.9% in the prior year period.

The following chart shows Revolve’s margin progression:

Earnings per share reached $0.16 on a diluted basis, representing a 7% increase from $0.15 in Q1 2024. It’s worth noting that the Q1 2024 figure included an insurance recovery equivalent to $0.03 per share, making the underlying improvement even more substantial.

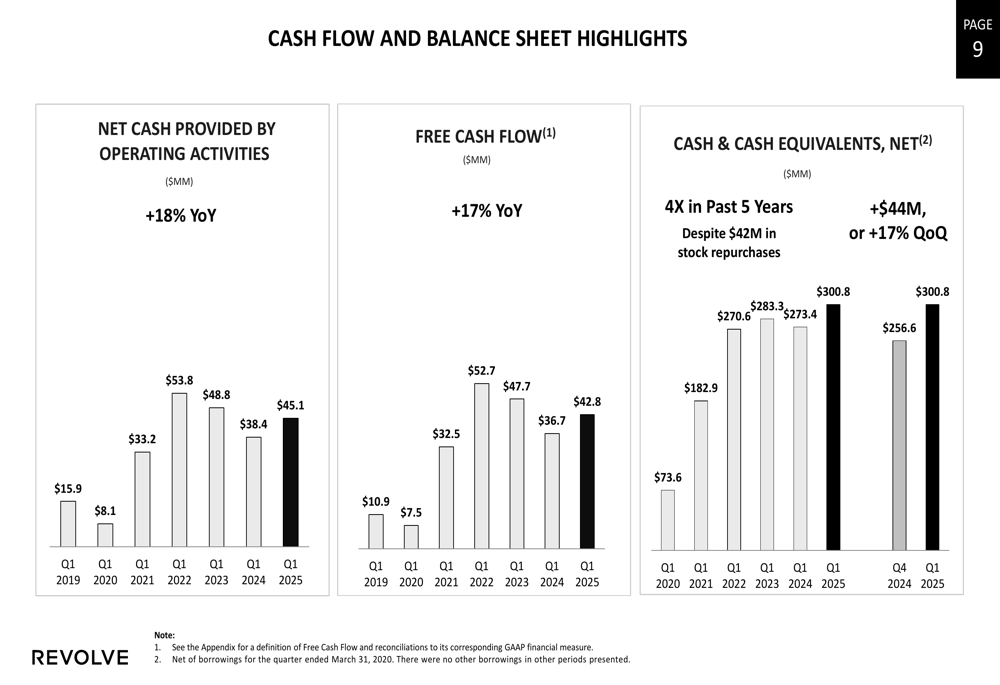

Cash flow generation remained a particular strength for Revolve. Net cash provided by operating activities increased 18% year-over-year to $45.1 million, while free cash flow grew 17% to $42.8 million. The company’s cash position strengthened considerably, with cash and cash equivalents reaching $300.8 million, up $44 million or 17% quarter-over-quarter.

The following chart highlights Revolve’s impressive cash generation:

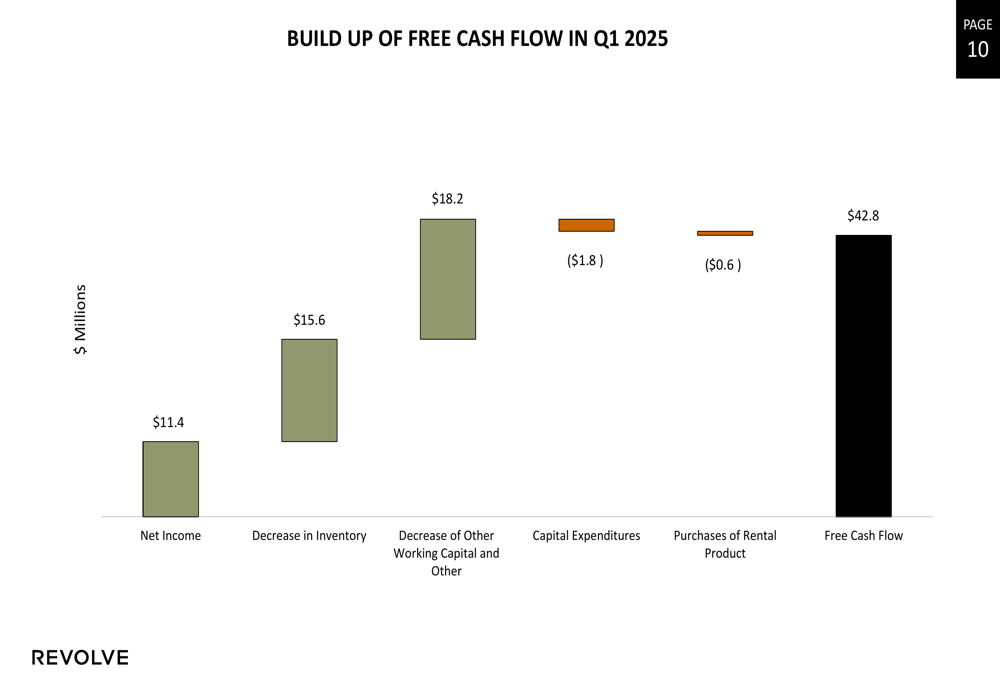

This cash flow growth was primarily driven by improved net income, inventory management, and working capital efficiency. The build-up of free cash flow demonstrates how the company converted its earnings into available cash:

Inventory management showed discipline, with inventory levels decreasing 7% quarter-over-quarter while increasing 6% year-over-year to $214 million. This balanced approach supports Revolve’s growth while maintaining operational efficiency.

Forward-Looking Statements

Looking ahead, Revolve announced its participation in several upcoming investor conferences in June 2025, including the Baird Consumer, Technology and Services Conference, TD Cowen Future of the Consumer Conference, and William Blair Growth Stock Conference. These events will provide further opportunities for the company to articulate its growth strategy and address investor concerns.

The company’s strong cash position of $300.8 million, which has grown fourfold over the past five years, provides significant financial flexibility. Revolve completed $42 million in stock repurchases, demonstrating confidence in its long-term prospects despite the recent stock price performance.

While the presentation did not include specific forward guidance, the company’s consistent revenue growth, expanding margins, and strong cash generation suggest continued operational momentum. However, the market’s reaction indicates investors may be looking for even stronger growth or have concerns about the broader retail environment and consumer spending patterns.

Revolve’s ability to continue growing its active customer base (up 6% year-over-year) while maintaining strong average order values ($295) will be crucial for sustaining its growth trajectory in the competitive e-commerce fashion space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.