Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Ribbon Communications Inc. (NASDAQ:RBBN) presented its second quarter 2025 results on July 23, showcasing a significant rebound from a disappointing first quarter. The company reported substantial growth in revenue and profitability, driven primarily by strong performance in its Cloud & Edge segment. Following the announcement, Ribbon’s stock rose 5.46% in regular trading to close at $4.03, with an additional 3.23% gain to $4.16 in after-hours trading.

Executive Summary

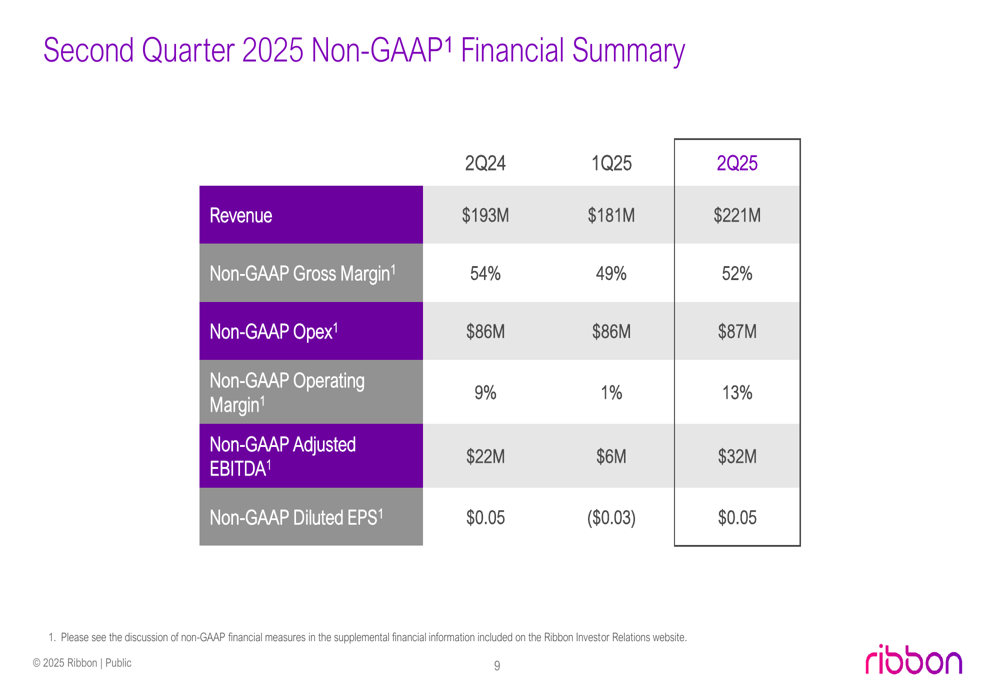

Ribbon Communications reported Q2 2025 revenue of $221 million, representing a 15% increase year-over-year and a substantial 22% sequential improvement from Q1’s $181 million. The company’s adjusted EBITDA reached $32 million, up 47% compared to the same period last year and a dramatic recovery from the $6 million reported in Q1 2025. Non-GAAP earnings per share came in at $0.05, matching the year-ago quarter and recovering from the -$0.03 loss in Q1.

As shown in the following quarterly performance summary:

"We’re pleased with our strong second quarter results, which demonstrate the resilience of our business model and the success of our strategic initiatives," said Bruce McCollin, CEO of Ribbon Communications, during the earnings presentation. "The significant growth in our Cloud & Edge segment reflects increasing demand for network modernization solutions from both service providers and enterprises."

Quarterly Performance Highlights

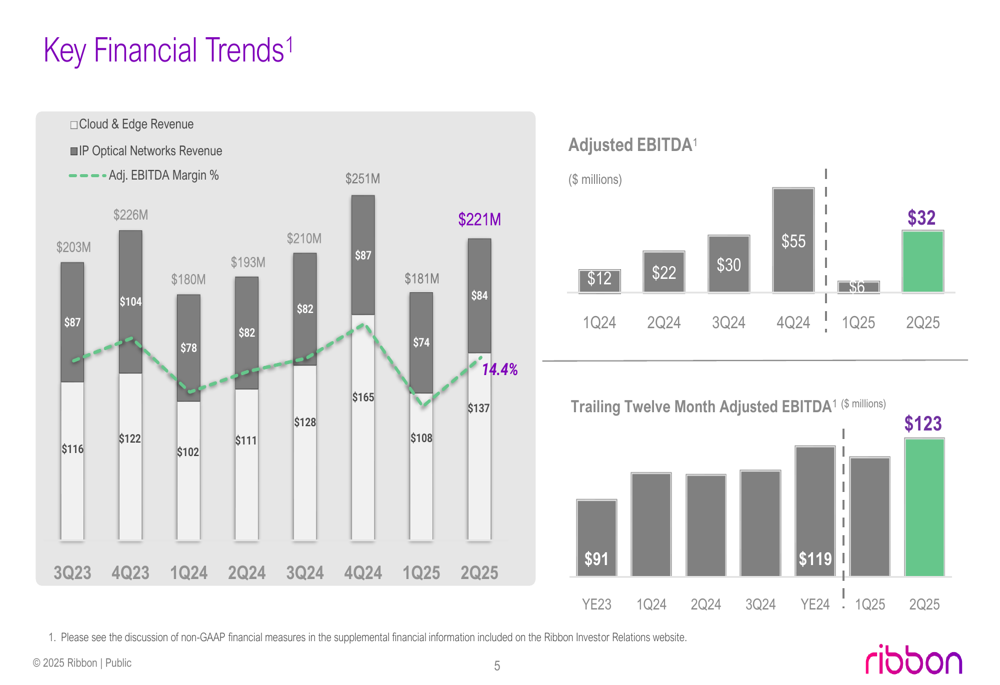

The company’s financial trends show a clear recovery in Q2 after a challenging start to the year. Revenue and adjusted EBITDA have returned to the growth trajectory established in the latter half of 2024, with Q2 2025 representing the second-highest quarterly revenue in the past two years.

The following chart illustrates these key financial trends:

Ribbon’s gross margin for Q2 stood at 52%, an improvement from the 49% reported in Q1 but slightly below the 54% achieved in Q2 2024. Operating expenses remained well-controlled at $87 million, just $1 million higher than the previous quarter despite the significant revenue increase. This disciplined approach to cost management helped drive the non-GAAP operating margin to 13%, up from just 1% in Q1.

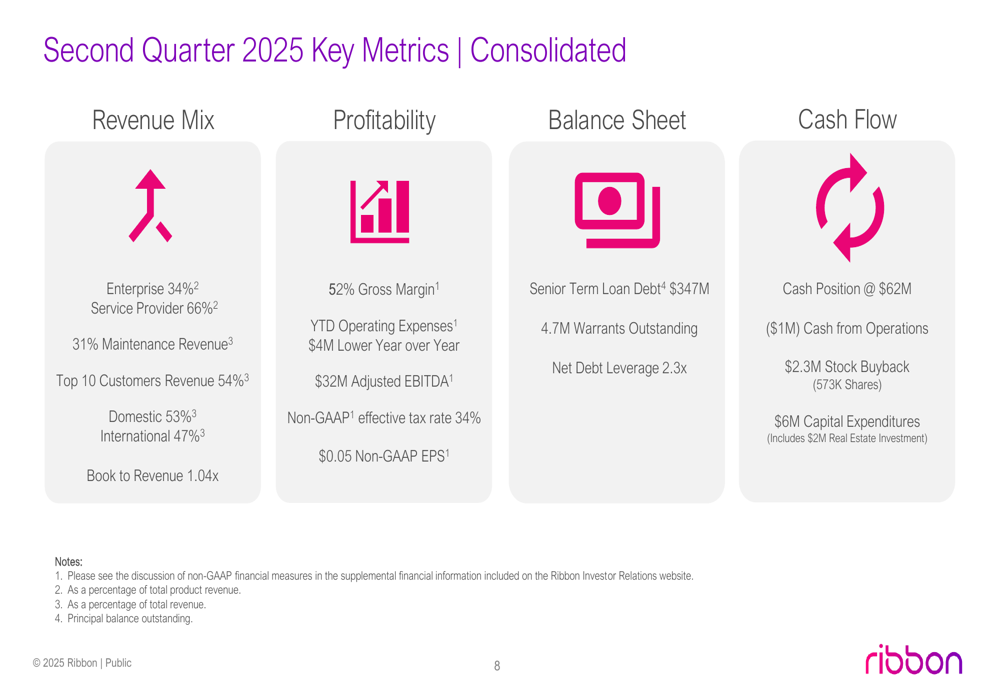

The company’s consolidated metrics reveal a balanced revenue mix, with service providers accounting for 66% of revenue and enterprise customers for 34%. International markets contributed 47% of total revenue, while domestic sales accounted for 53%.

Segment Analysis

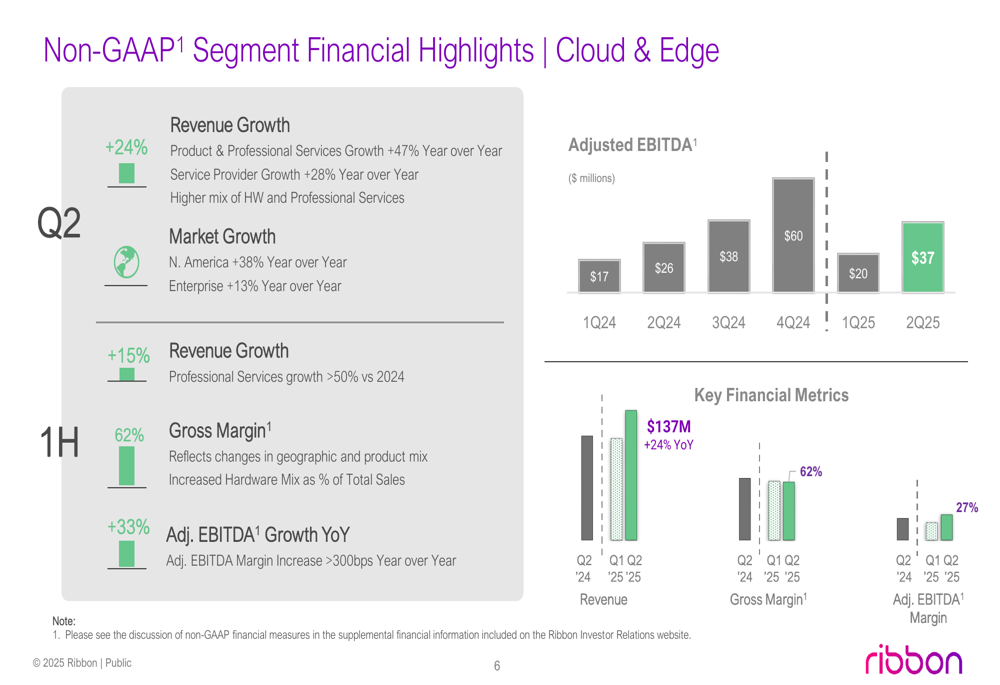

Ribbon’s performance was primarily driven by its Cloud & Edge segment, which reported revenue of $137 million, a robust 24% increase year-over-year. This growth was fueled by a 47% jump in product and professional services revenue and a 28% increase in service provider sales. North American markets were particularly strong, growing 38% compared to the same period last year.

The Cloud & Edge segment also delivered impressive profitability, with a gross margin of 62% and an adjusted EBITDA margin of 27%. Adjusted EBITDA for this segment reached $37 million in Q2, up from $20 million in Q1 and $26 million in Q2 2024.

As illustrated in the segment performance chart:

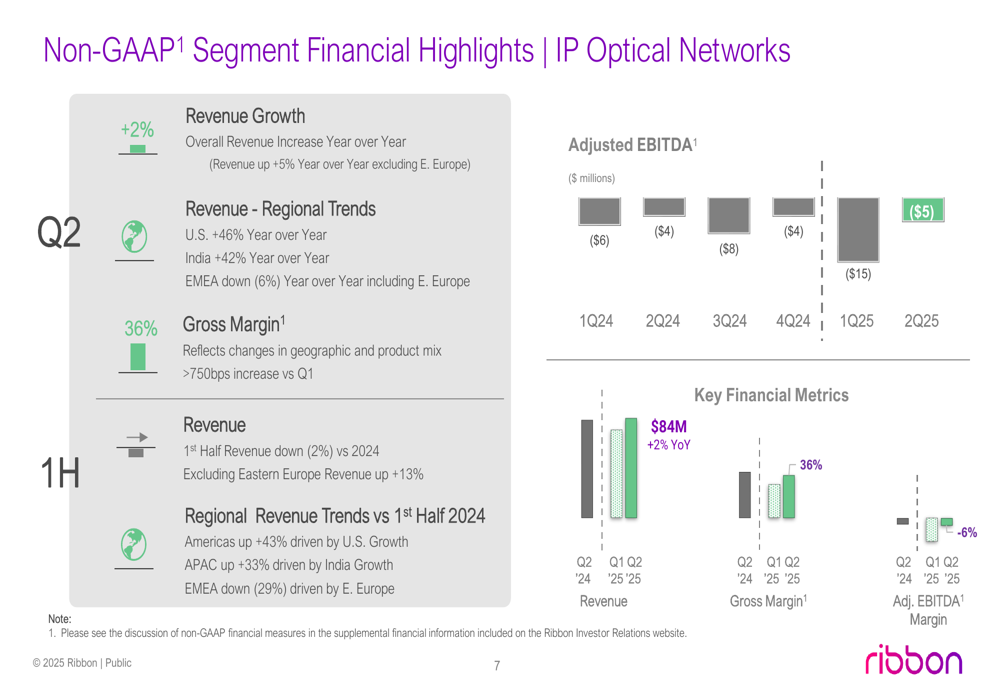

The IP Optical Networks segment showed more modest improvement, with revenue of $84 million representing a 2% year-over-year increase. Performance varied significantly by region, with the U.S. market growing 46% and India up 42%, while EMEA declined 6% due to challenges in Eastern Europe.

Despite the revenue growth, the IP Optical segment continued to operate at a loss, with an adjusted EBITDA margin of -6%. However, this represents an improvement from the -15% margin reported in Q1 2025.

Strategic Initiatives

Ribbon highlighted several strategic focus areas driving its growth, including network modernization projects, federal and defense secure communications, and fiber investment opportunities. The company is particularly well-positioned to benefit from the $42 billion U.S. BEAD (Broadband Equity, Access, and Deployment) program, which aims to expand high-speed internet access across the country.

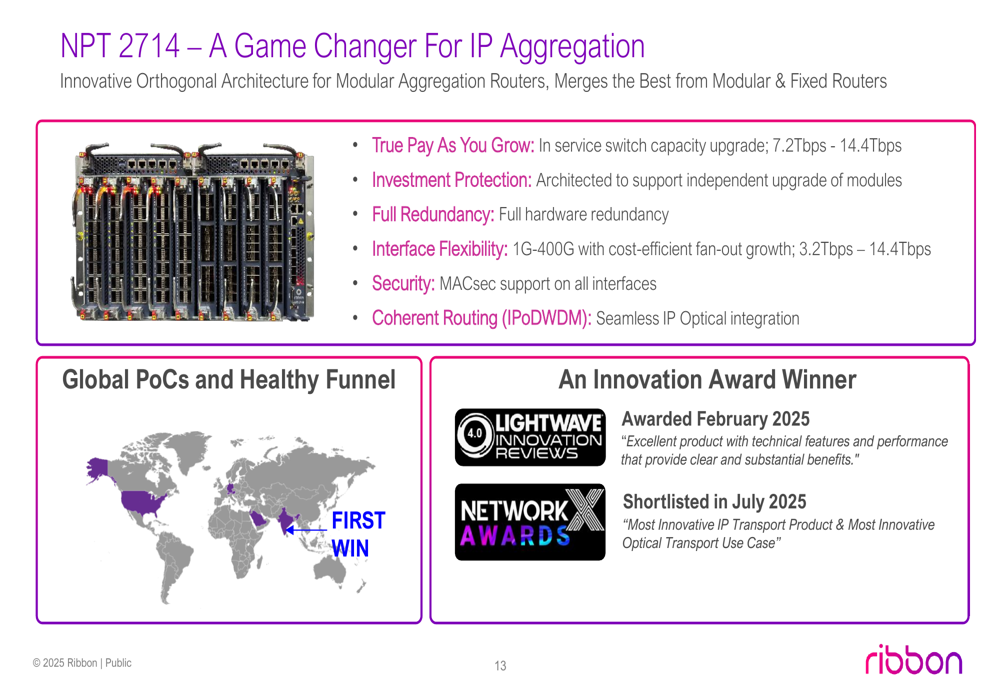

A key product introduction during the quarter was the NPT 2714, which Ribbon describes as a "game changer for IP aggregation." This new offering provides scalable capacity from 7.2Tbps to 14.4Tbps and supports interfaces from 1G to 400G, positioning Ribbon competitively in the high-performance networking market.

The following image showcases the NPT 2714’s capabilities and market reception:

"The NPT 2714 represents a significant advancement in our IP routing portfolio," explained the company’s CTO during the presentation. "Early customer feedback has been extremely positive, and we’re seeing strong interest across multiple regions."

Forward Guidance

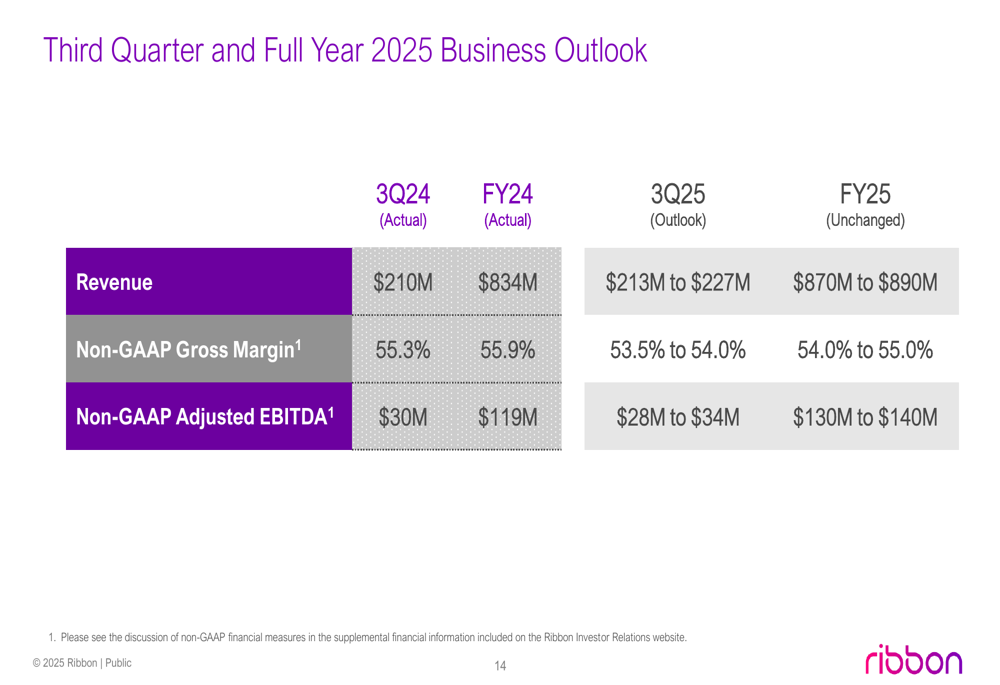

Despite the strong Q2 performance, Ribbon maintained its full-year 2025 guidance, projecting revenue between $870 million and $890 million and adjusted EBITDA between $130 million and $140 million. For the third quarter, the company expects revenue between $213 million and $227 million and adjusted EBITDA between $28 million and $34 million.

The unchanged full-year outlook suggests management may be taking a conservative approach given ongoing economic uncertainties and potential challenges in the second half of the year.

Market Context

Ribbon’s Q2 results represent a significant improvement from its disappointing Q1 performance, when the company missed analyst expectations with an EPS of -$0.03 against a forecast of $0.02. The strong rebound aligns with management’s previous guidance, which had projected Q2 revenue between $210 million and $220 million and adjusted EBITDA between $28 million and $32 million.

The company continues to operate in a competitive but evolving telecommunications infrastructure market, with industry consolidation creating both challenges and opportunities. Ribbon highlighted its positioning in key growth areas, including voice network modernization, cloud adoption, and secure communications for government and defense applications.

With a book-to-revenue ratio of 1.04x and a net debt leverage of 2.3x, Ribbon appears to be maintaining a stable financial position while investing in growth initiatives. The company’s $50 million stock buyback program and ending cash balance of $62 million provide additional financial flexibility as it navigates the competitive landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.