Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Richardson Electronics , Ltd. (NASDAQ:RELL) presented its Q4 and full-year FY2025 results on July 24, 2025, highlighting a year of revenue growth and strategic repositioning. The company’s stock showed positive movement, up 2.35% to $10.01 in regular trading and gaining an additional 3.78% in pre-market activity.

The presentation comes after a challenging third quarter when the company missed earnings expectations, resulting in a significant stock drop. However, the full-year results paint a more positive picture, with the company emphasizing its transition toward power management solutions and green energy markets.

Quarterly Performance Highlights

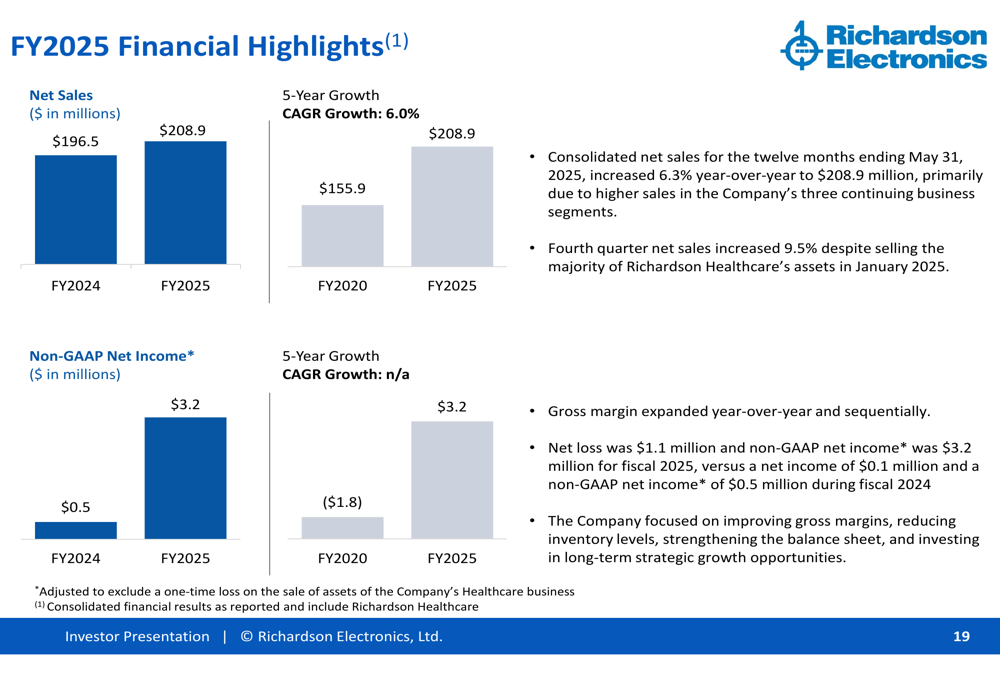

Richardson Electronics reported consolidated net sales of $208.9 million for the fiscal year ending May 31, 2025, representing a 6.3% increase compared to the previous year. Fourth quarter sales showed particularly strong momentum, increasing 9.5% despite the January 2025 sale of the majority of Richardson Healthcare’s assets.

The company’s business is divided into three main segments, with Power & Microwave Technology (PMT) generating the largest portion of revenue at $137.8 million, followed by Canvys at $33.1 million and Green Energy Solutions (GES) at $28.7 million.

As shown in the following financial highlights chart:

Non-GAAP net income improved significantly to $3.2 million in FY2025, up from $0.5 million in FY2024. This represents a substantial turnaround from the $1.8 million loss reported in FY2020, demonstrating the company’s progress in improving profitability over a five-year period.

Strategic Initiatives

A key strategic move during FY2025 was the January sale of most Richardson Healthcare assets to DirectMed Imaging for $8.2 million. Under this arrangement, Richardson retained its CT tube engineering and manufacturing assets through an exclusive supply agreement with DirectMed. The remaining healthcare assets will be consolidated into the PMT segment beginning in Q1 FY2026, with proceeds from the sale being directed toward growth initiatives, primarily within the Green Energy Solutions segment.

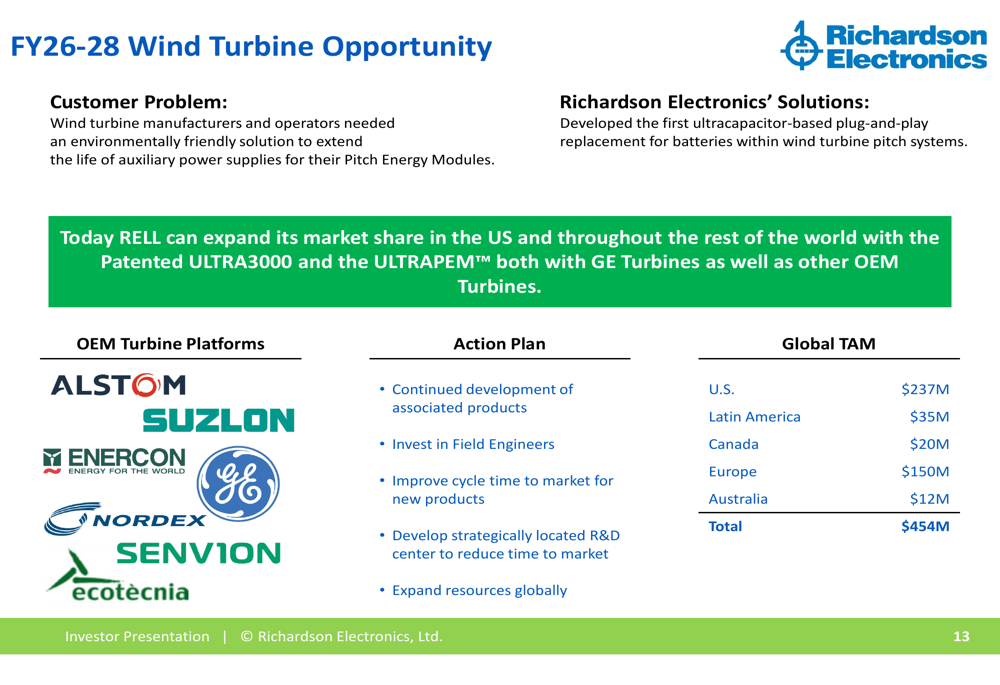

Richardson Electronics is strategically positioning itself in the renewable energy sector, particularly in wind turbine applications. The company has identified a significant market opportunity for its patented ultracapacitor-based solutions that replace batteries in wind turbine pitch energy modules.

The following slide illustrates the substantial market opportunity across various regions:

The company estimates a total addressable market of $454 million globally, with the largest opportunities in the U.S. ($237 million) and Europe ($150 million). Richardson’s patented ULTRA3000 and ULTRAPEM products are designed for both GE turbines and other OEM platforms including ALSTOM, SUZLON, ENERCON, and NORDEX.

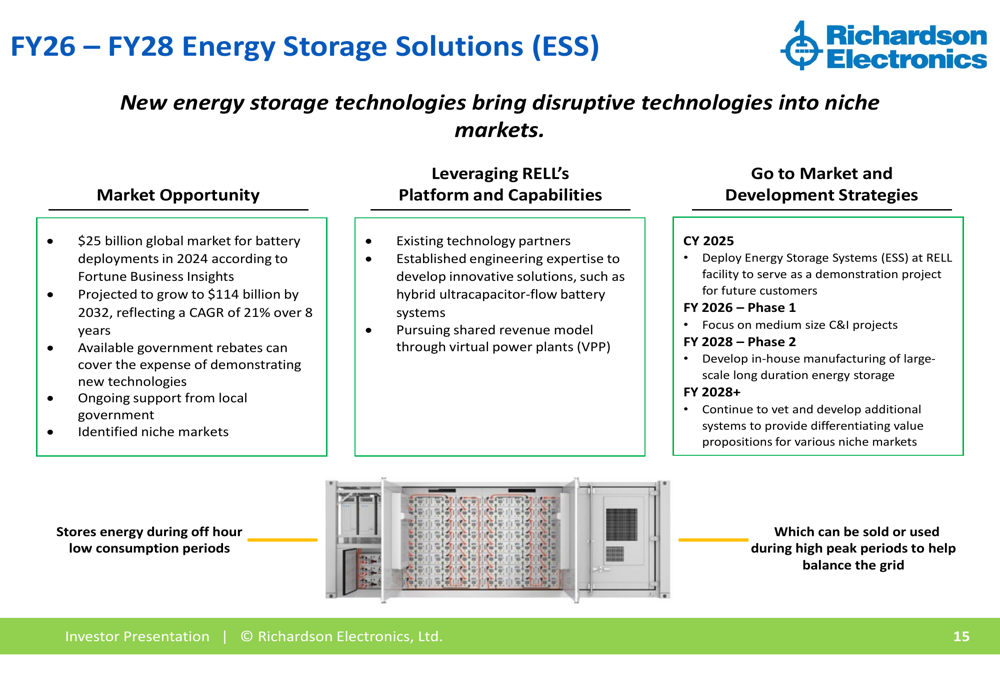

Energy storage represents another significant growth opportunity, with the company outlining a multi-year strategy to enter this rapidly expanding market:

Richardson notes that the global market for battery deployments reached $25 billion in 2024 and is projected to grow to $114 billion by 2032. The company plans to deploy its own Energy Storage Systems in 2025, focus on medium-sized commercial and industrial projects in FY2026, and develop in-house manufacturing of large-scale long-duration energy storage by FY2028.

The company’s strategic repositioning is supported by relationships with major customers across the renewable energy sector, as shown in the following image:

Detailed Financial Analysis

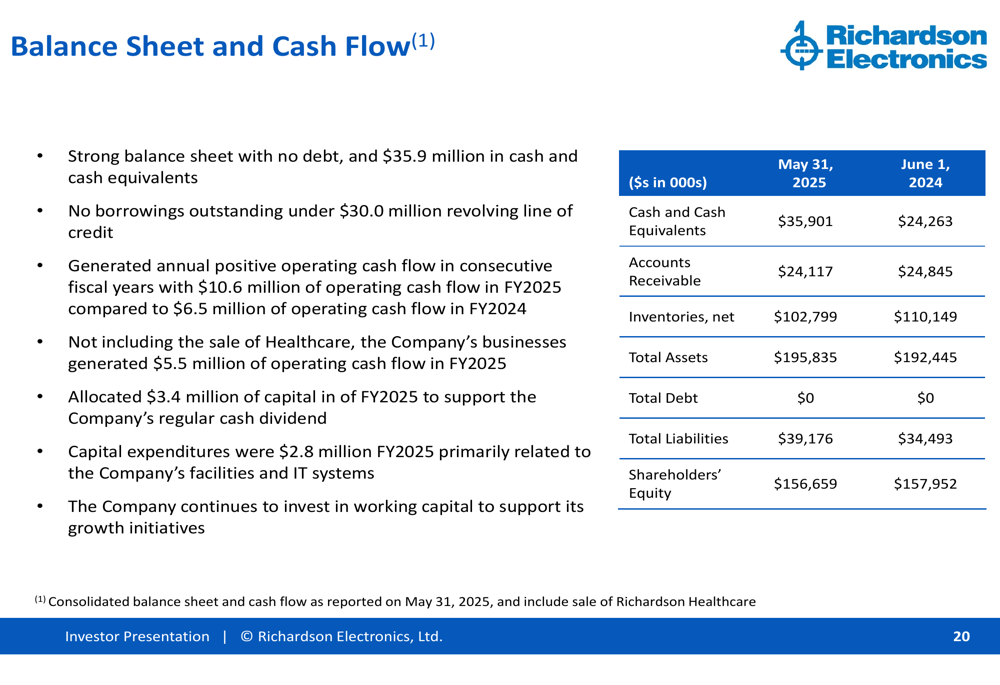

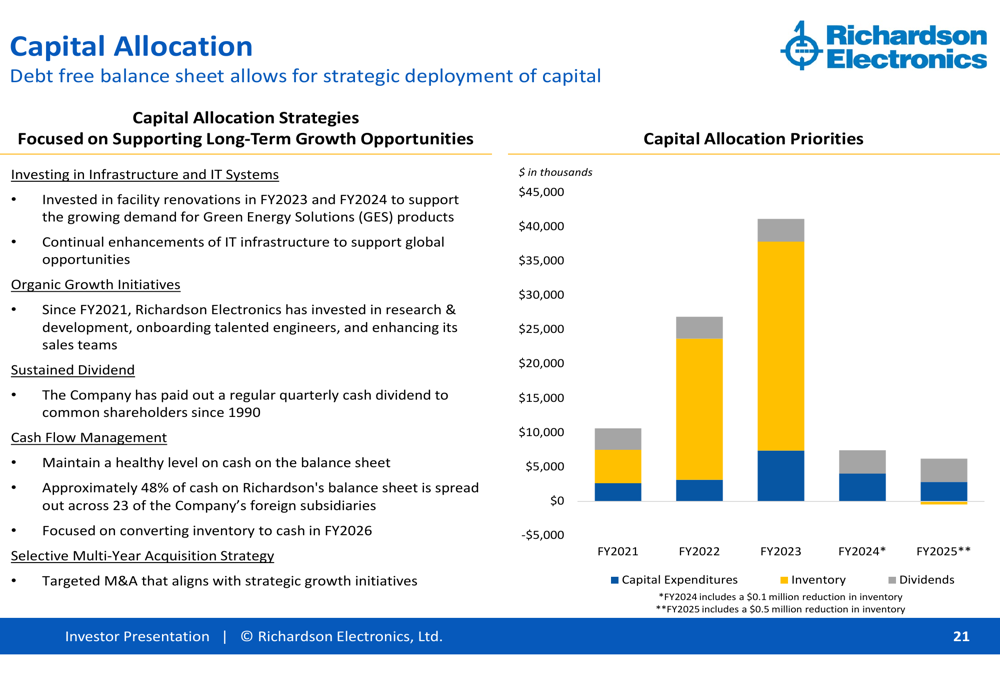

Richardson Electronics maintains a strong balance sheet with no debt and $35.9 million in cash and cash equivalents as of May 31, 2025, up from $24.3 million a year earlier. The company has also reduced its inventory from $110.1 million to $102.8 million year-over-year, improving cash flow.

The following slide details the company’s balance sheet position:

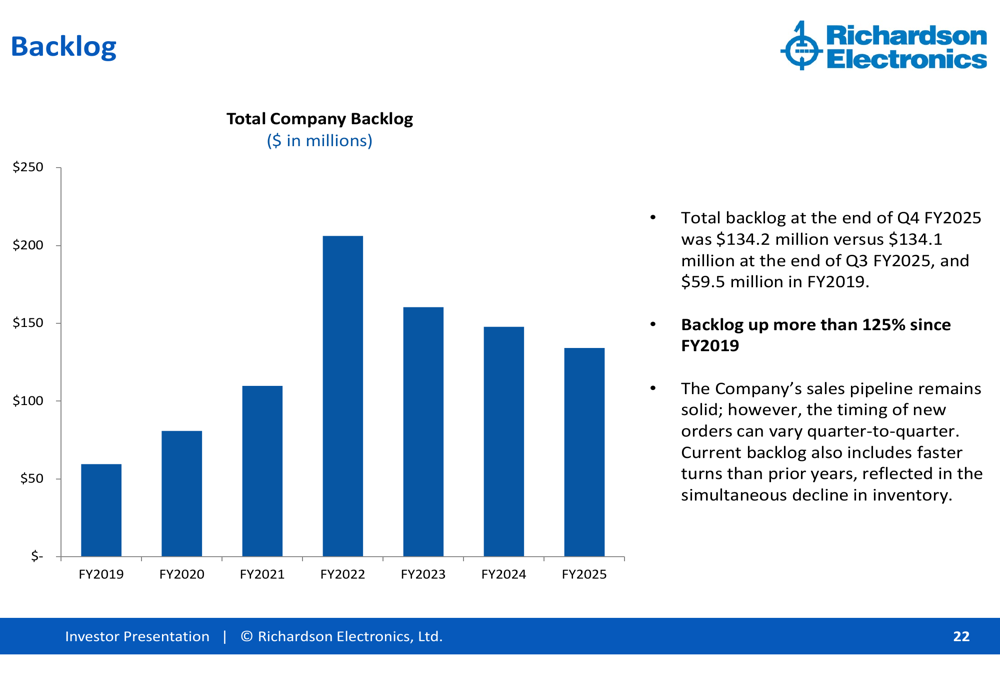

The company’s backlog remains robust at $134.2 million at the end of Q4 FY2025, essentially unchanged from $134.1 million at the end of Q3 but representing more than 125% growth since FY2019. This strong backlog provides visibility into future revenue potential.

Richardson’s capital allocation strategy focuses on supporting long-term growth opportunities through investments in capital expenditures, inventory, and consistent dividend payments:

Forward-Looking Statements

Looking ahead to FY2026, Richardson Electronics expects some volatility due to global trade policies but is positioning itself to capitalize on policies driving manufacturing back to the U.S. The company anticipates steady or increasing sales of wind turbine modules and is preparing for the launch of StartSaver by Wabtec in the EV rail segment.

The semiconductor wafer fab market is showing positive trends, which should benefit the company’s PMT segment. Management expects continued growth in the Green Energy Solutions segment, driven by increasing adoption of its wind turbine solutions and the development of new energy storage products.

These forward-looking statements align with comments made during the Q3 earnings call, where CEO Ed Richardson emphasized the company’s strategic repositioning as "a leader in power management" and COO Wendy Dedell expressed optimism about future opportunities in large power management applications.

While the company faces challenges including tariff concerns and execution risks in its transition to power management and green energy solutions, its strong balance sheet, growing backlog, and strategic focus on high-growth markets position Richardson Electronics for potential growth in FY2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.