Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Ringkjøbing Landbobank (CPH:RILBA) presented its H1/Q2 2025 results on August 6, revealing continued growth momentum and an improved profit outlook for the full year. The Danish bank’s shares closed at DKK 1,452 on August 5, down slightly by 0.21% ahead of the results announcement.

The presentation highlighted the bank’s continued success in expanding its loan and deposit base while maintaining strong credit quality, despite operating in a challenging interest rate environment that has put pressure on deposit margins.

Executive Summary

Ringkjøbing Landbobank reported a net profit after tax of DKK 1,191 million for the first half of 2025, slightly exceeding its performance from the same period in 2024. This translated to earnings per share of DKK 47.9, representing a 6% year-over-year increase.

Based on these results, management has revised its full-year profit expectations upward to a range of DKK 2,000-2,350 million, signaling confidence in the bank’s ability to maintain its growth trajectory through the second half of the year.

The bank’s return on equity remained steady at 21.4%, while its cost-to-income ratio increased slightly to 25.6% from 24.8% in the first half of 2024, still maintaining its position as one of Denmark’s most efficient banks.

Quarterly Performance Highlights

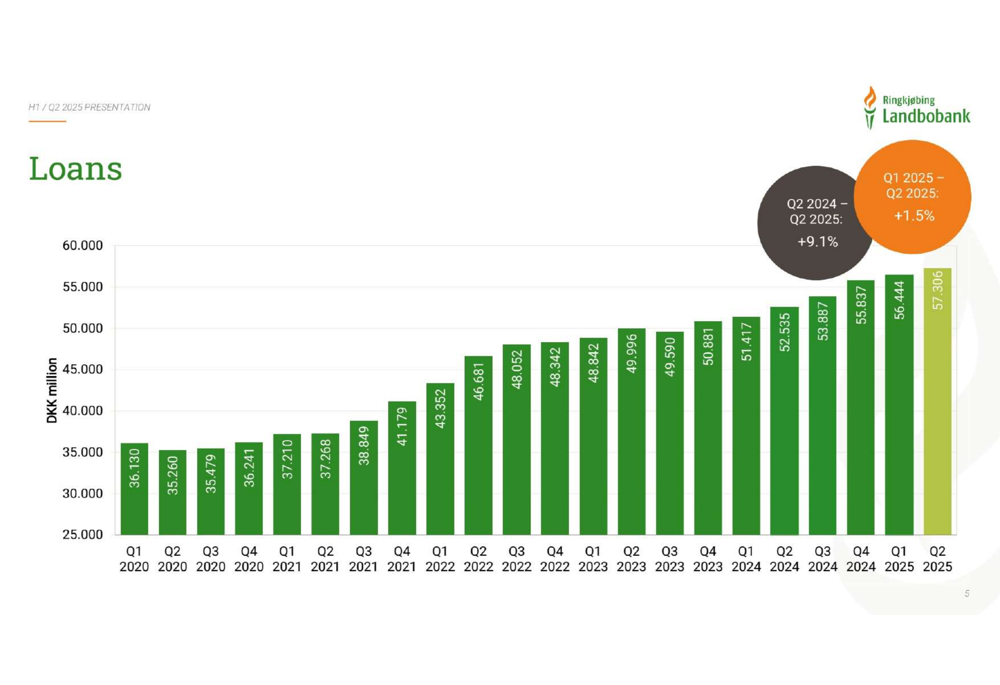

Ringkjøbing Landbobank’s loan book expanded by 1.5% during the second quarter of 2025 and 9.1% year-over-year, reaching DKK 57.3 billion. This growth demonstrates the bank’s continued ability to attract new business despite competitive market conditions.

As shown in the following chart of quarterly loan growth:

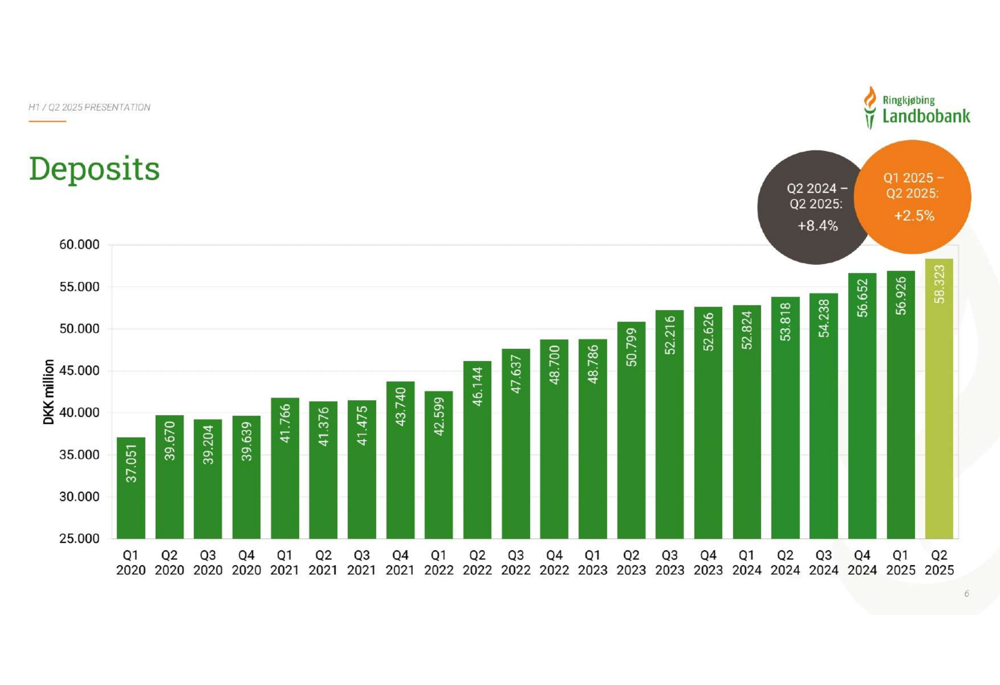

Deposit growth has similarly been robust, with a 2.5% increase in Q2 2025 and an 8.4% rise year-over-year, bringing total deposits to DKK 58.3 billion.

The deposit growth trend is illustrated in this chart:

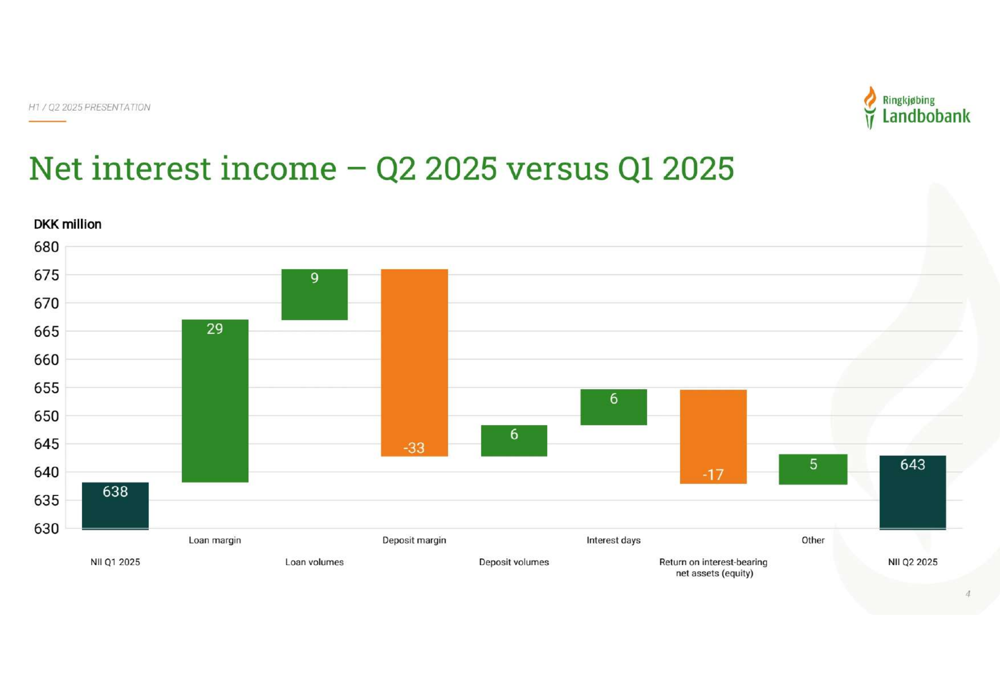

The bank’s net interest income increased slightly to DKK 643 million in Q2 2025 from DKK 638 million in Q1 2025. This modest growth was achieved despite pressure on deposit margins, as shown in the following waterfall chart:

Credit quality remains exceptionally strong, with DKK 24 million in impairment reversals in Q1 and no impairments required in Q2 2025, highlighting the bank’s prudent risk management and the overall health of its loan portfolio.

Detailed Financial Analysis

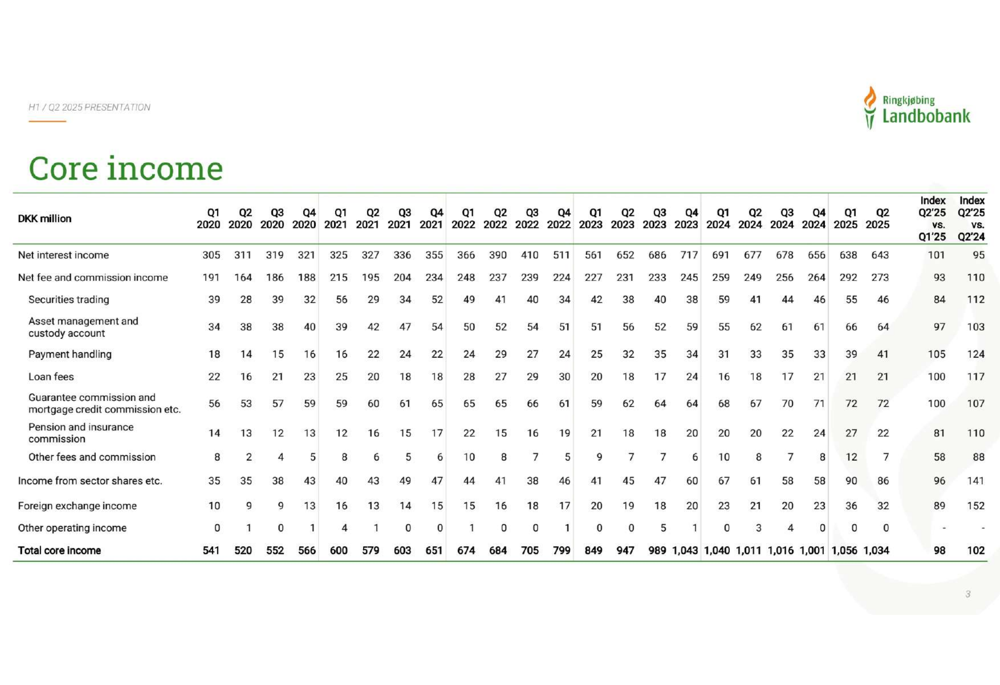

Core income for Q2 2025 totaled DKK 1,034 million, representing a 2% increase compared to Q2 2024 but a 2% decrease from Q1 2025. The detailed breakdown of core income components provides insight into the bank’s revenue streams:

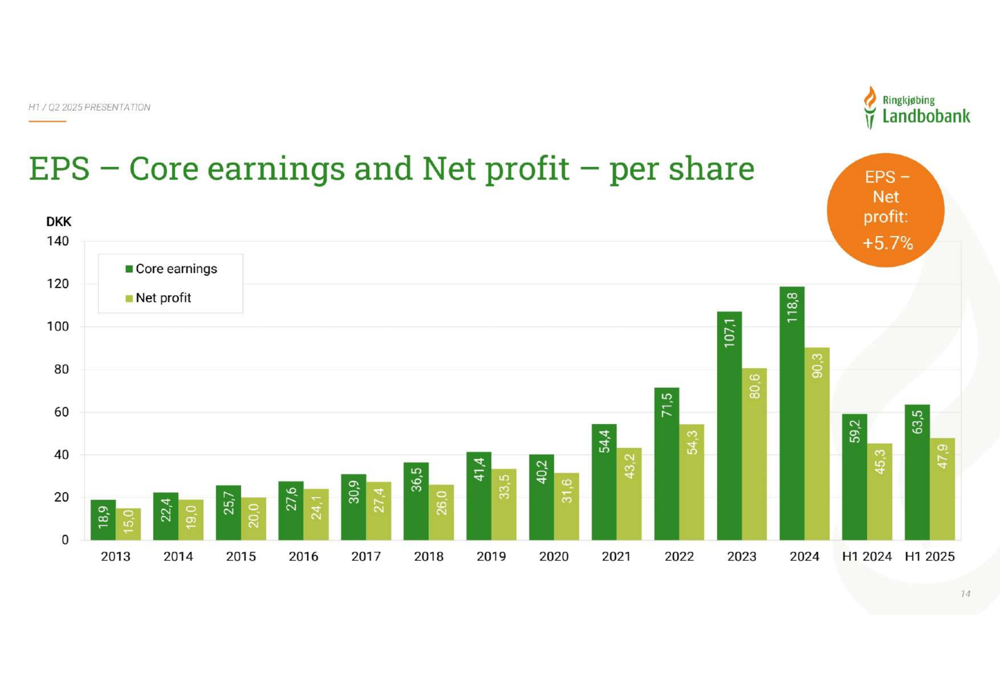

Earnings per share continued its upward trajectory, with EPS from net profit reaching DKK 47.9 for H1 2025, a 5.7% increase from DKK 45.3 in H1 2024. Core earnings per share showed even stronger growth, rising to DKK 63.5 from DKK 59.2 in the prior year period.

The following chart illustrates the EPS trend:

Total (EPA:TTEF) expenses increased by 5.2% year-over-year to DKK 275 million in Q2 2025, primarily driven by higher staff and administration costs. This expense growth outpacing revenue growth contributed to the slight deterioration in the cost-to-income ratio to 25.6%.

The bank maintains a strong capital position with an adjusted CET1 capital ratio of 17.7 in Q2 2025, well above regulatory requirements. This robust capital base supports the bank’s ongoing share buyback program, which is expected to reduce the number of outstanding shares to approximately 24.3 million by January 2026.

Competitive Industry Position

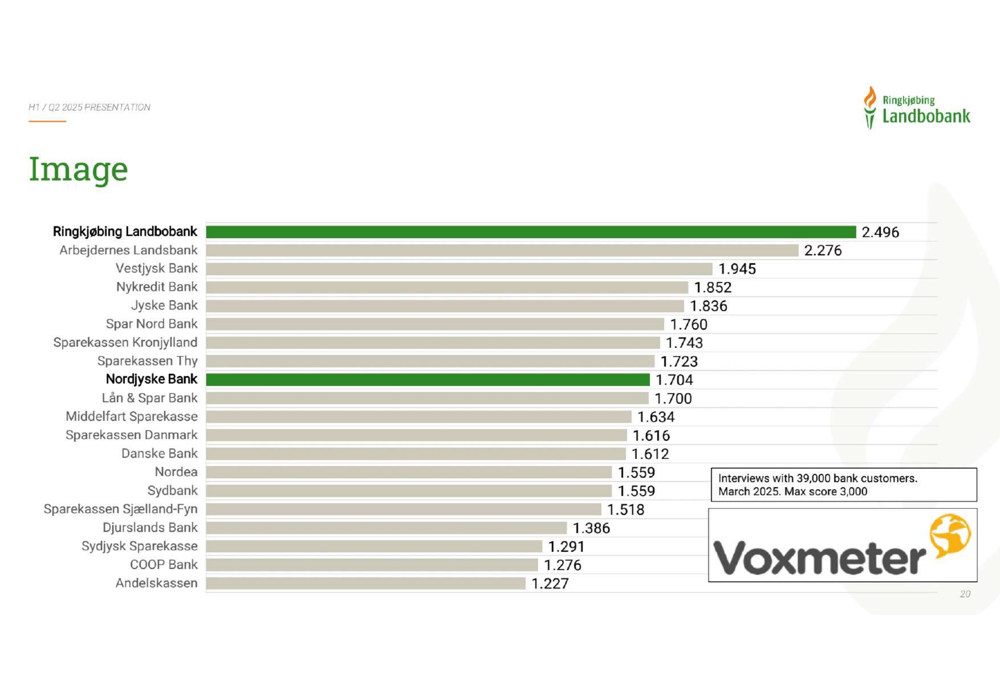

Ringkjøbing Landbobank continues to enjoy a strong competitive position in the Danish banking sector. The bank ranked highest in customer satisfaction with a score of 2,496 out of 3,000 in a survey of 39,000 bank customers conducted in March 2025.

The bank’s competitive standing is illustrated in this customer satisfaction ranking:

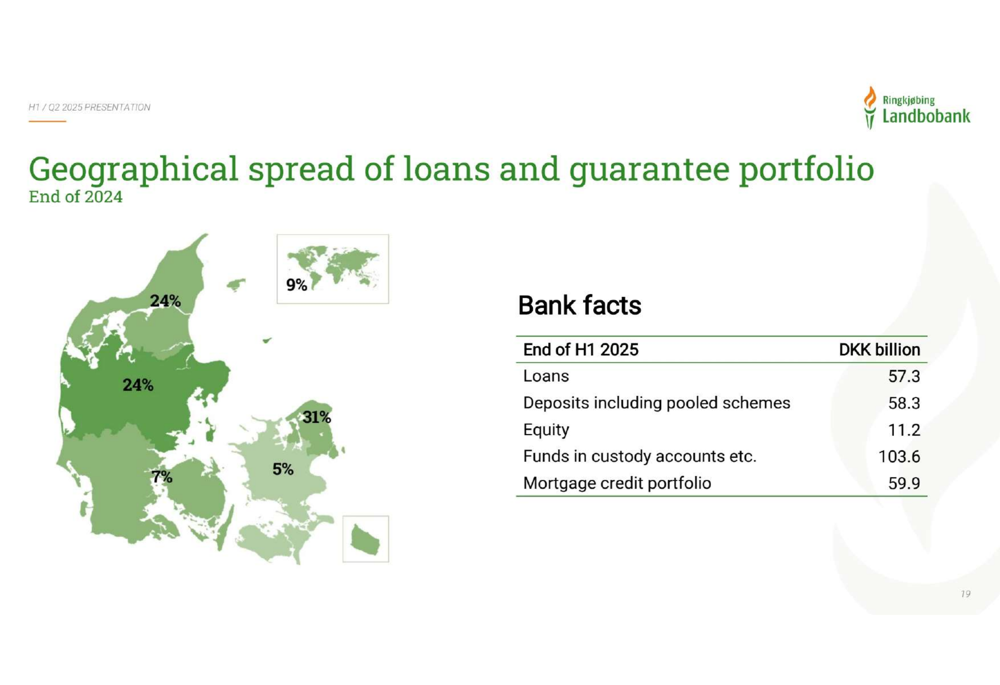

The bank’s business model combines traditional retail banking with specialized niche banking, allowing it to maintain the lowest cost-to-income ratio in Denmark. Its loan portfolio is geographically diversified across Denmark with 9% international exposure.

This geographical diversification is shown in the following map:

Moody’s has assigned strong credit ratings to Ringkjøbing Landbobank, including Aa3 ratings for bank deposits, issuer rating, and counterparty risk rating, all with a stable outlook. These ratings were last reviewed on June 18, 2025, and reflect the bank’s solid financial position and risk management practices.

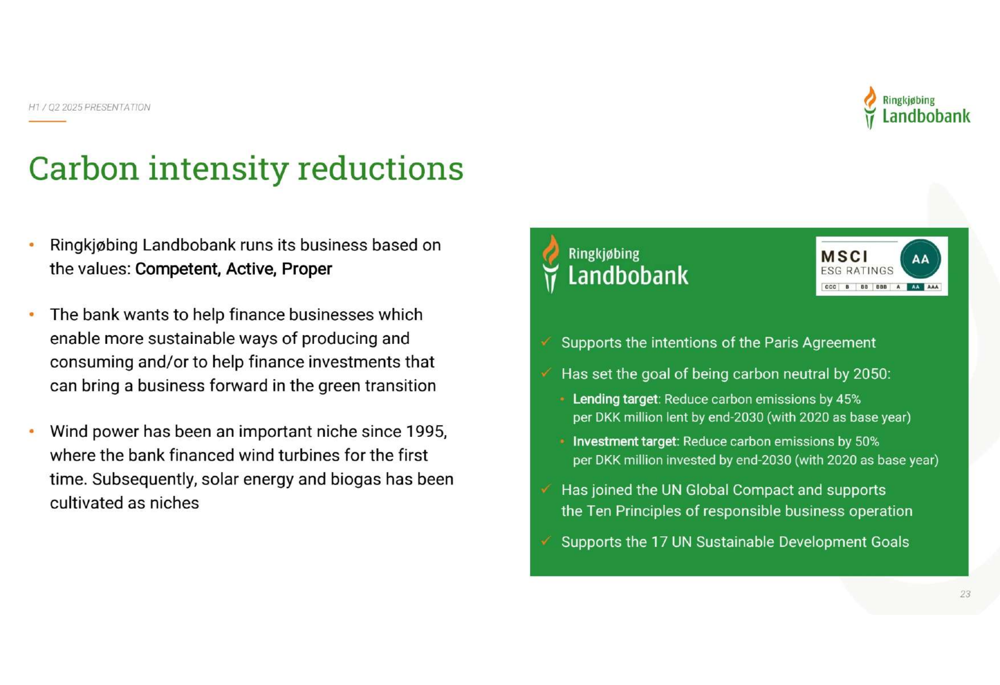

The bank has also strengthened its ESG profile, supporting the Paris Agreement with a goal of becoming carbon neutral by 2050. It has joined the UN Global Compact and supports the 17 UN Sustainable Development Goals.

The bank’s ESG initiatives and ratings are summarized here:

Forward-Looking Statements

Based on its strong first-half performance, Ringkjøbing Landbobank has adjusted its full-year 2025 net profit expectations upward to a range of DKK 2,000-2,350 million.

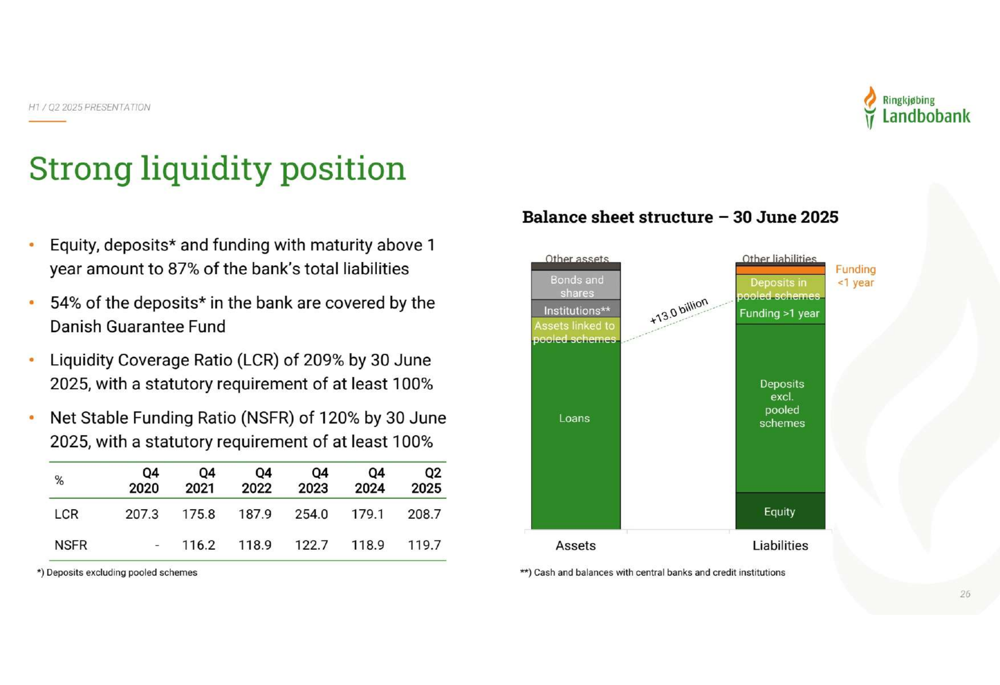

The bank’s strong liquidity position, with a liquidity coverage ratio of 209% and 87% of liabilities consisting of equity, deposits, and funding with maturity above one year, provides a solid foundation for continued growth.

Management expects to continue its share buyback program, further enhancing shareholder returns through reduced share count alongside direct dividend payments.

While the bank faces challenges from competitive pressures on deposit margins and slightly rising costs, its diversified business model, strong credit quality, and efficient operations position it well to navigate the evolving financial landscape through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.