Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Rocket Companies (NYSE:RKT) released its Q2 2025 investor presentation highlighting strategic acquisitions and technology investments aimed at transforming the homeownership experience. Despite reporting adjusted revenue of $1.34 billion in Q2, which missed analyst expectations of $1.67 billion, the company emphasized its long-term strategy of building an integrated homeownership platform powered by artificial intelligence.

The mortgage lender’s stock declined 1.66% in premarket trading following the earnings release, settling at $15.97, as investors weighed the EPS beat of $0.04 (exceeding forecasts by 15.2%) against the revenue shortfall.

Strategic Initiatives

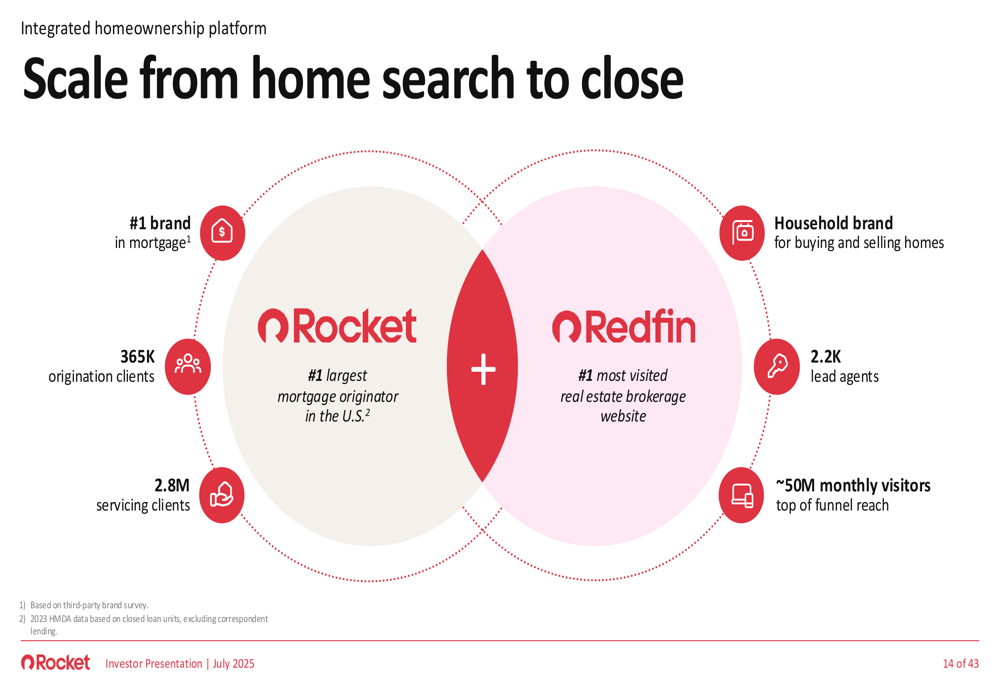

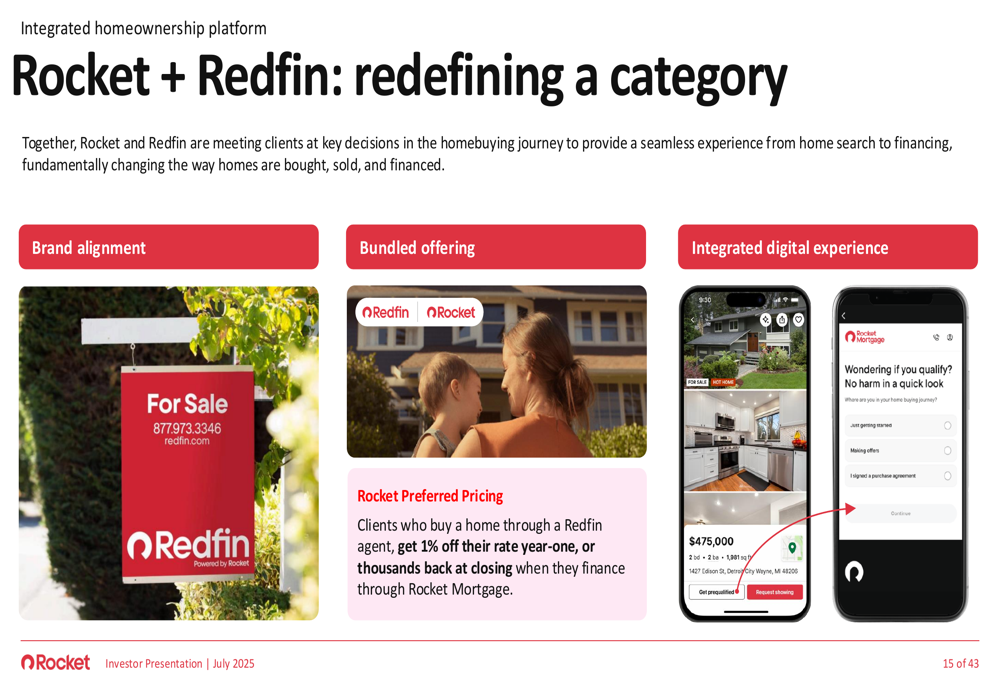

A central theme of Rocket’s presentation was its acquisition strategy, particularly the integration of Redfin to create a comprehensive homeownership platform. The company positioned the combination as transformative for the industry, bringing together Rocket’s mortgage expertise with Redfin’s real estate platform.

As shown in the following slide detailing the scale of the combined entities, Rocket brings its position as the #1 mortgage brand with 365K origination clients and 2.8M servicing clients, while Redfin contributes the #1 most visited real estate brokerage website with approximately 50M monthly visitors:

The strategic rationale for combining the companies focuses on brand alignment, bundled offerings, and an integrated digital experience. Rocket highlighted a "Rocket Preferred Pricing" initiative that offers clients who buy a home through a Redfin agent 1% off their rate in the first year or thousands back at closing when financing through Rocket Mortgage:

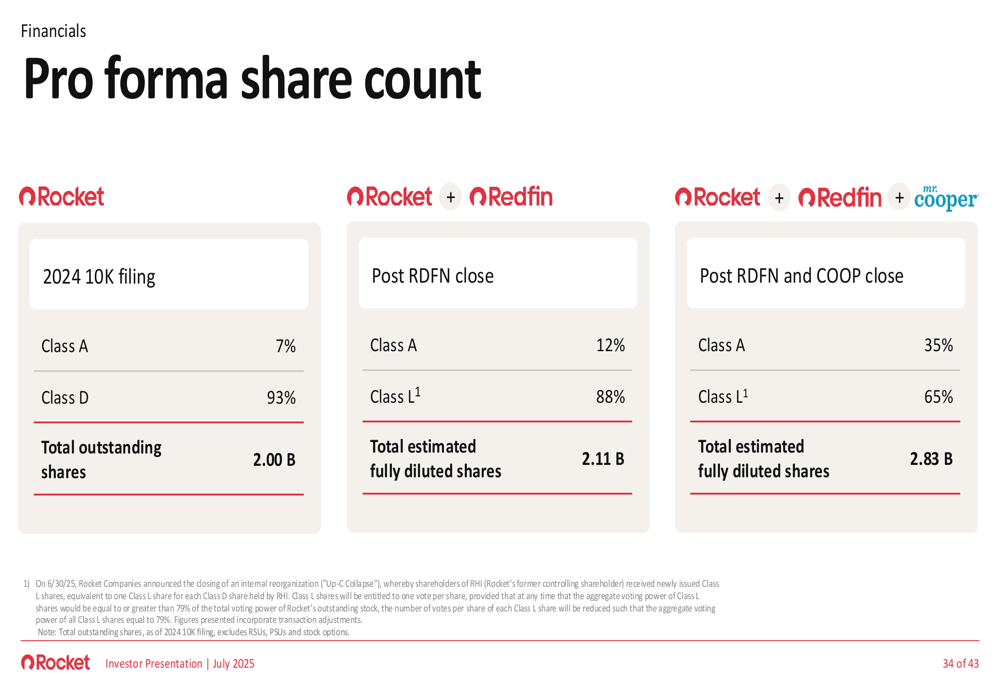

The presentation also referenced plans for the acquisition of Mr. Cooper, though with fewer details. The pro forma share count slide showed the potential ownership structure following both acquisitions, with Class A shares increasing from 7% to 35% of the total:

AI and Technology Investments

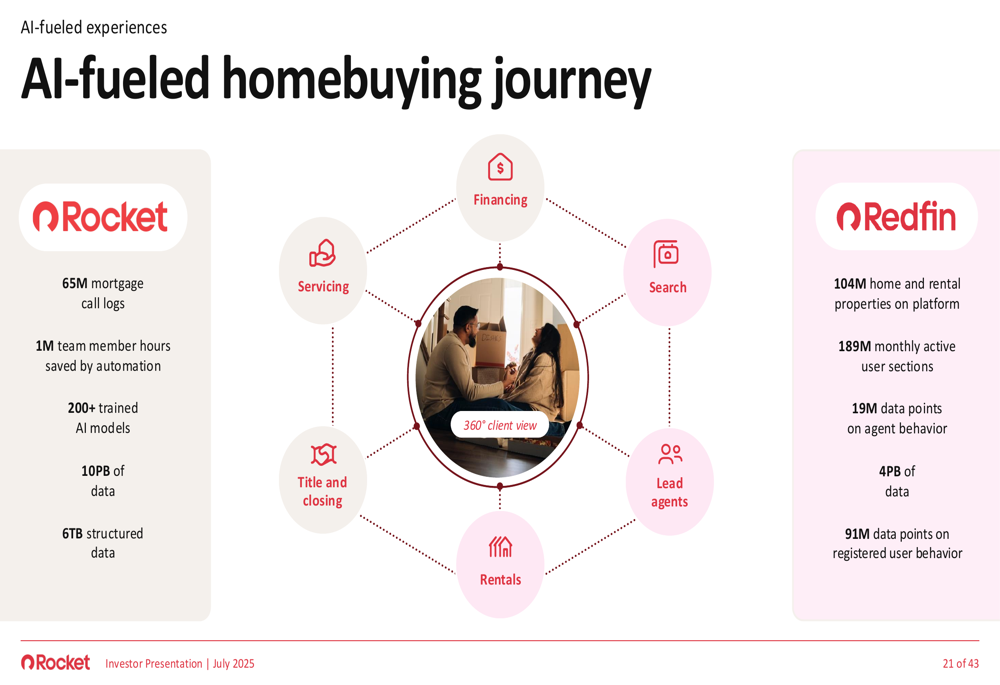

Rocket emphasized its significant investments in artificial intelligence, reporting $500 million invested in AI over the past five years resulting in 200+ proprietary AI models. The company presented AI as a key differentiator and growth driver across its business operations.

The following slide illustrates how AI is being integrated throughout the homebuying journey, leveraging massive datasets from both Rocket and Redfin:

CEO Varun Krishna emphasized during the earnings call that "We are building a homeownership experience that is simpler, faster, and more affordable," with AI playing a central role in that vision. The company highlighted specific applications of AI across its business:

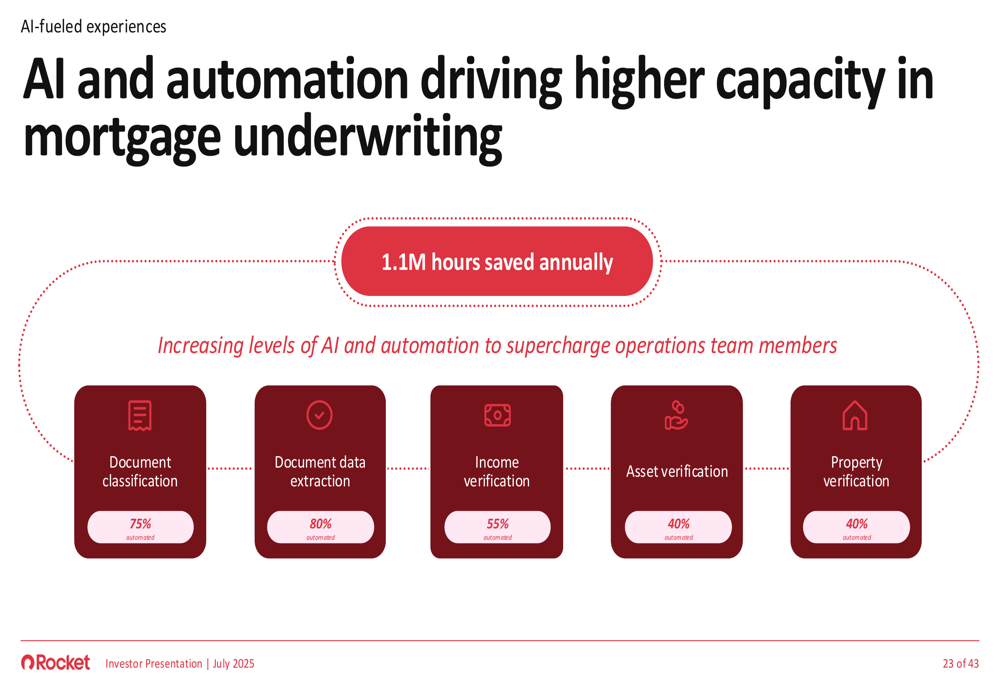

Rocket also detailed how AI and automation are driving higher capacity in mortgage underwriting, with significant portions of document classification (75%), data extraction (80%), and verification processes being automated:

Financial Performance

The presentation showcased Rocket’s financial performance with charts demonstrating growth in adjusted revenue and EBITDA. However, these figures should be viewed in the context of the company missing its Q2 revenue forecast by approximately $330 million.

The following chart shows the company’s adjusted revenue climbing from $1,002M in Q3’23 to $1,340M in Q2’25, while adjusted EBITDA increased from $73M in Q3’23 to $286M in Q3’24:

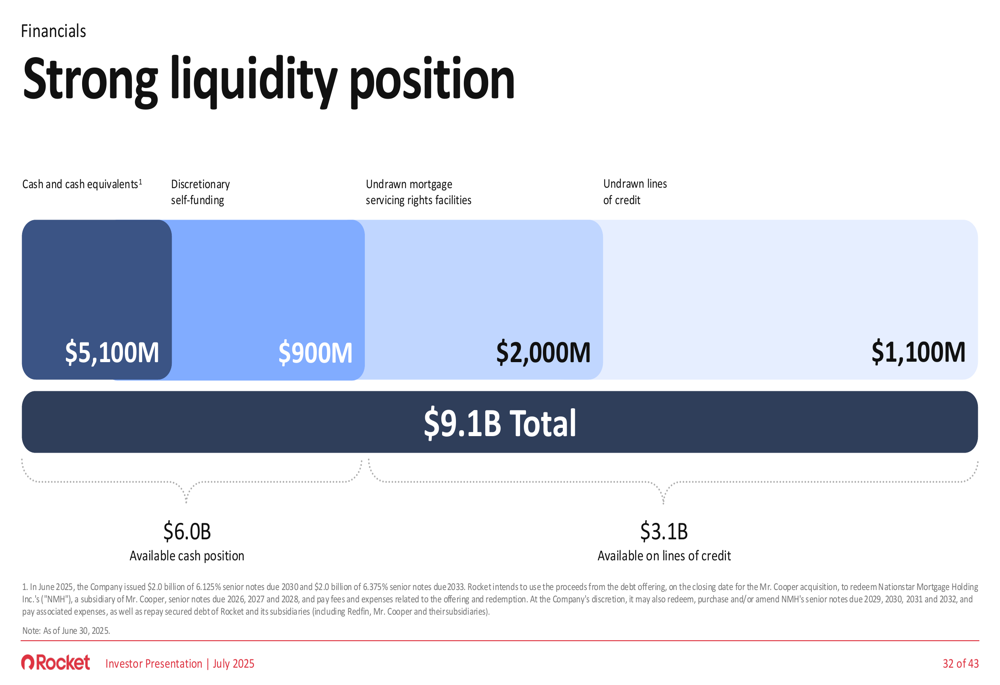

Rocket highlighted its strong liquidity position, totaling $9.1 billion, which provides flexibility for acquisitions and investments:

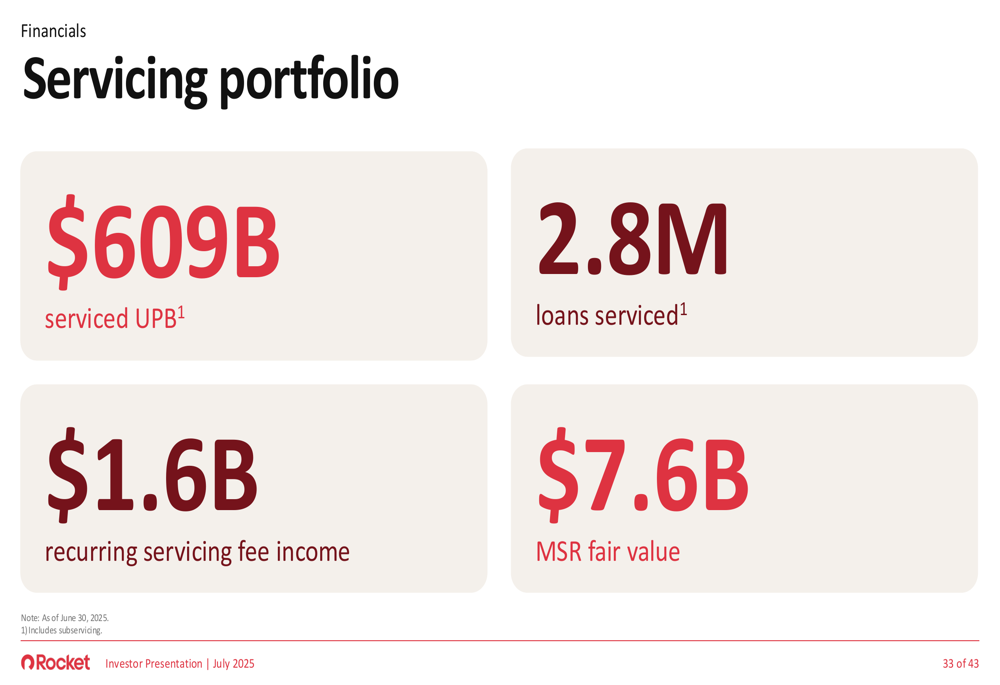

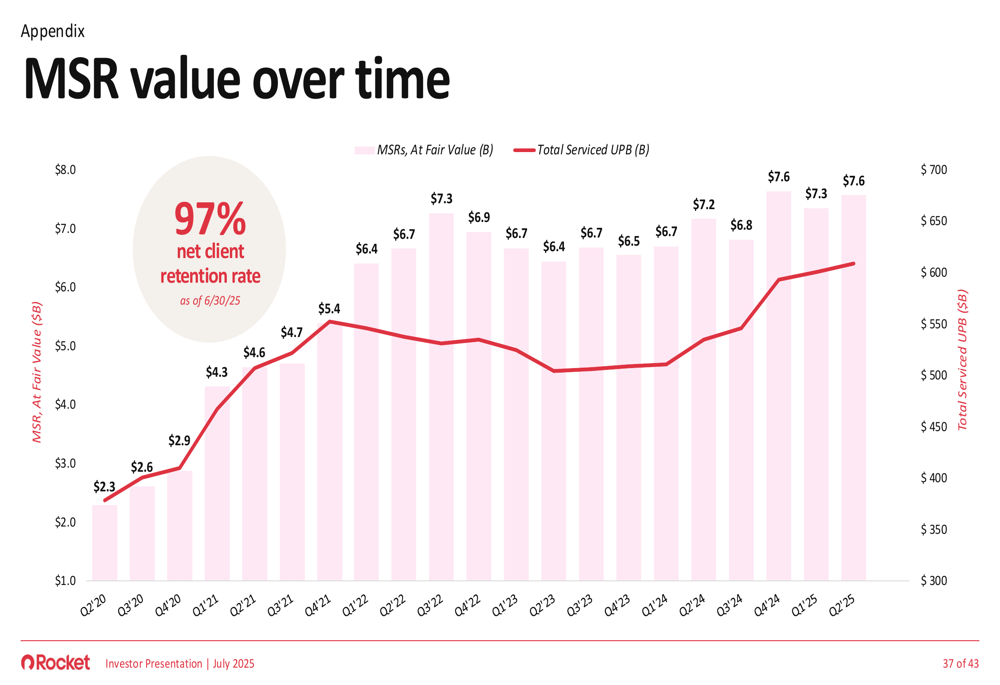

The company also emphasized the value of its mortgage servicing rights (MSR) portfolio, which represents a significant recurring revenue stream:

The MSR portfolio has shown consistent growth over time, with a 97% net client retention rate:

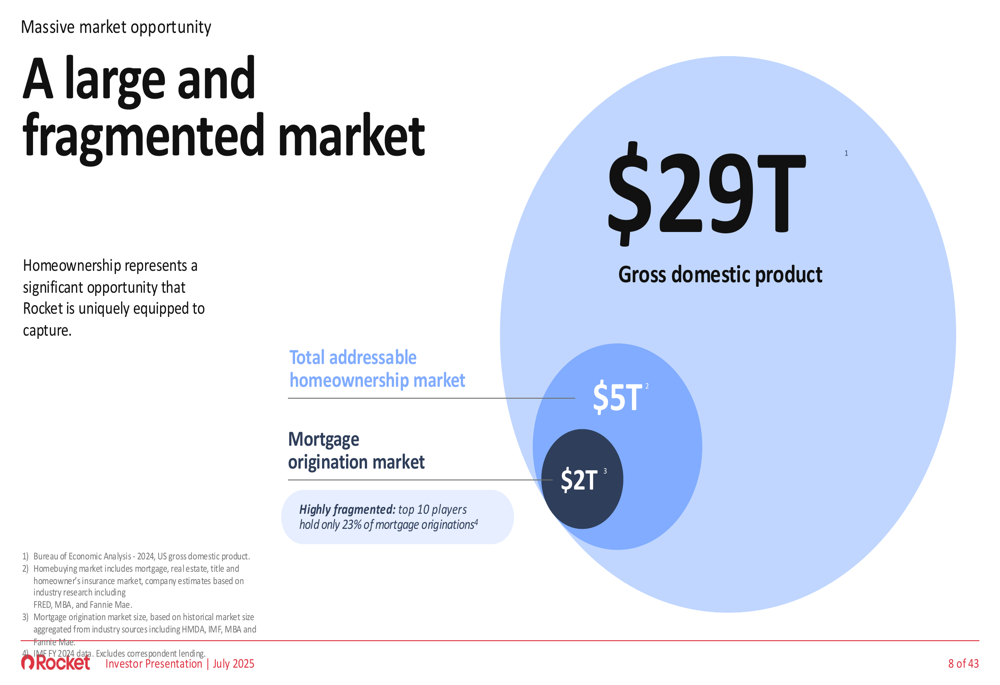

Market Opportunity and Competitive Position

Rocket positioned itself within a large but fragmented market, with the top 10 players holding only 23% of mortgage originations. The company highlighted the total addressable homeownership market at $5 trillion, with the mortgage origination market at $2 trillion:

A key competitive advantage emphasized throughout the presentation was Rocket’s industry-leading recapture rate of 83%, compared to the industry average of 25%:

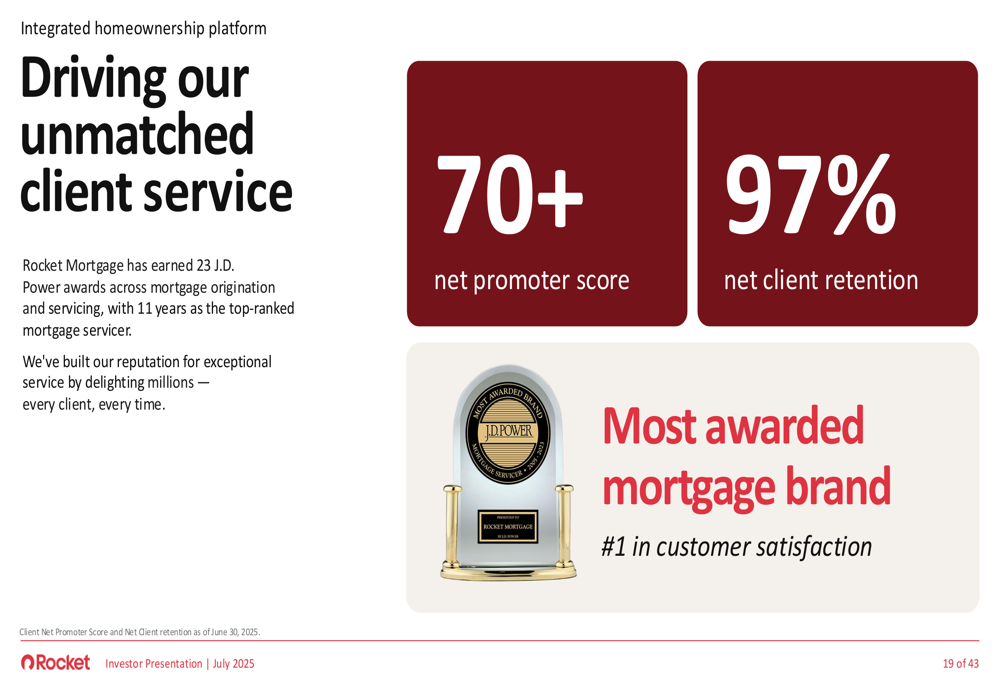

The company also highlighted its strong customer service reputation, noting 23 J.D. Power awards across mortgage origination and servicing:

Forward-Looking Statements

Looking ahead, Rocket projects Q3 adjusted revenue between $1.6 billion and $1.75 billion, anticipating continued momentum in the purchase market. The company remains focused on completing the acquisition of Mr. Cooper by Q4 and fully integrating Redfin into its platform.

While the presentation painted an optimistic picture of Rocket’s strategic direction, investors should note the challenges mentioned in the earnings call, including macroeconomic pressures, slowing home price growth, and operational challenges from restructuring efforts. The company expects its operational restructuring to save approximately $80 million annually.

As CFO Brian Brown noted during the earnings call, "Our combined 14-petabyte data lake enhances our AI capabilities," underscoring the company’s bet on technology-driven growth despite near-term revenue challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.