Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Rockwell Automation (NYSE:ROK) shares jumped nearly 8% in premarket trading after the industrial automation giant released its Q2 fiscal 2025 earnings presentation on May 7, showing improved margins and raised full-year guidance despite ongoing sales challenges.

The company reported a 6% year-over-year sales decline but demonstrated sequential improvement and strong cost management, leading to better-than-expected profitability metrics. This performance comes as Rockwell continues to navigate a challenging industrial environment while positioning itself for future growth.

Quarterly Performance Highlights

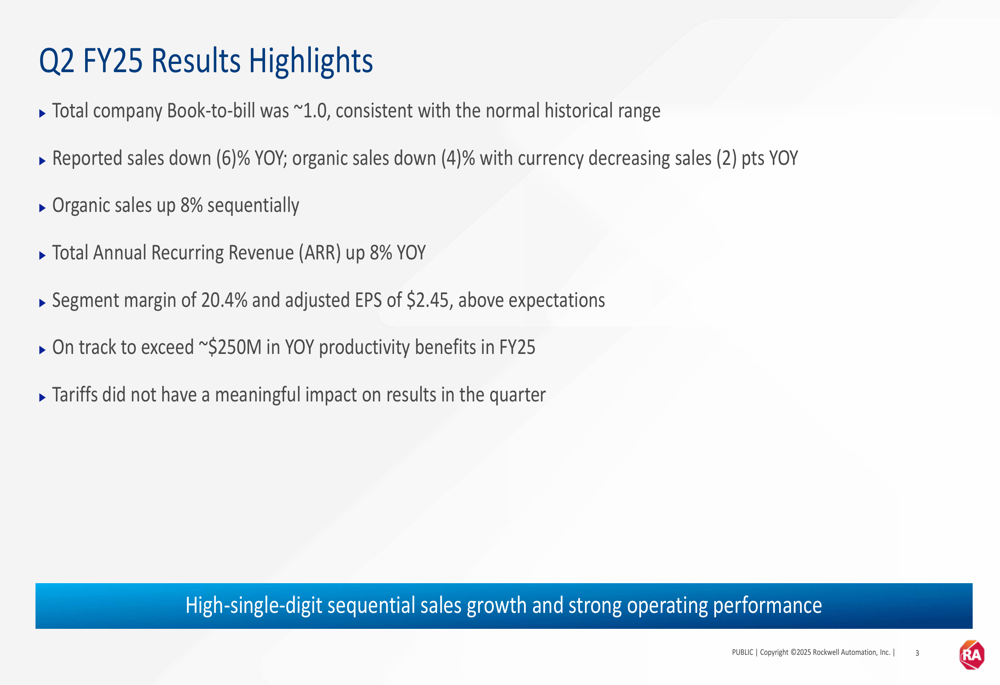

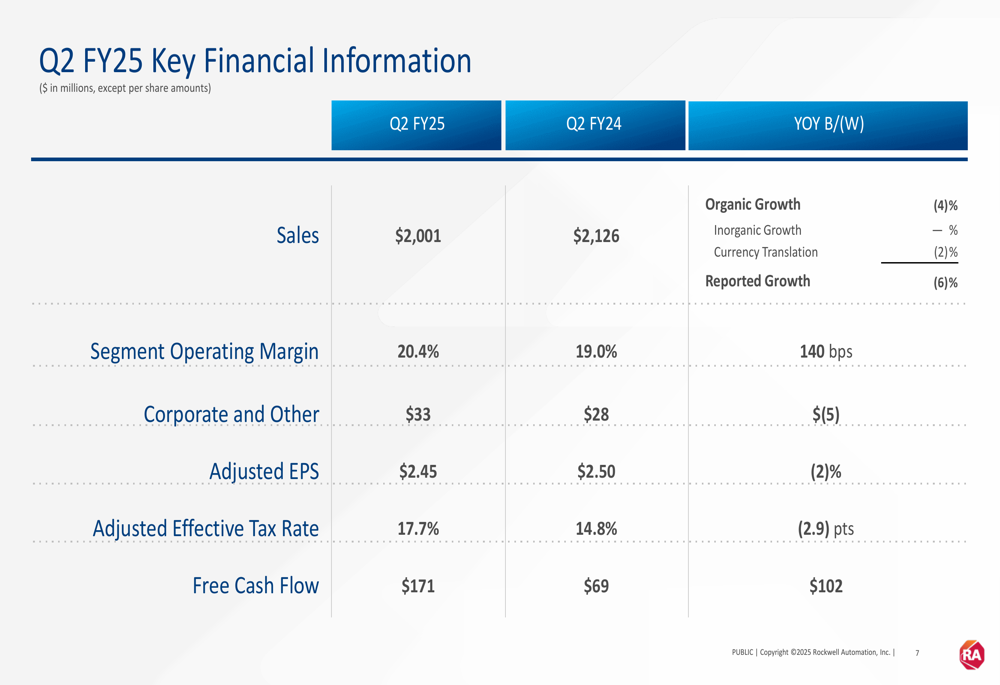

Rockwell reported Q2 fiscal 2025 sales of $2.001 billion, down 6% from $2.126 billion in the same period last year. Organic sales declined 4%, with currency translation reducing reported sales by an additional 2 percentage points. Despite the top-line pressure, the company achieved 8% sequential sales growth compared to Q1.

As shown in the following comprehensive overview of key results:

The company’s segment operating margin improved to 20.4%, up 140 basis points from 19.0% in the prior-year quarter, exceeding expectations. Adjusted earnings per share came in at $2.45, down slightly from $2.50 in Q2 fiscal 2024 but above company projections.

Rockwell’s book-to-bill ratio remained healthy at approximately 1.0, within the normal historical range, suggesting stable order patterns. Total (EPA:TTEF) Annual Recurring Revenue (ARR) grew 8% year-over-year, highlighting the company’s progress in building a more resilient revenue stream.

The detailed financial comparison reveals significant improvement in free cash flow, which reached $171 million compared to $69 million in the prior-year period:

Segment Analysis

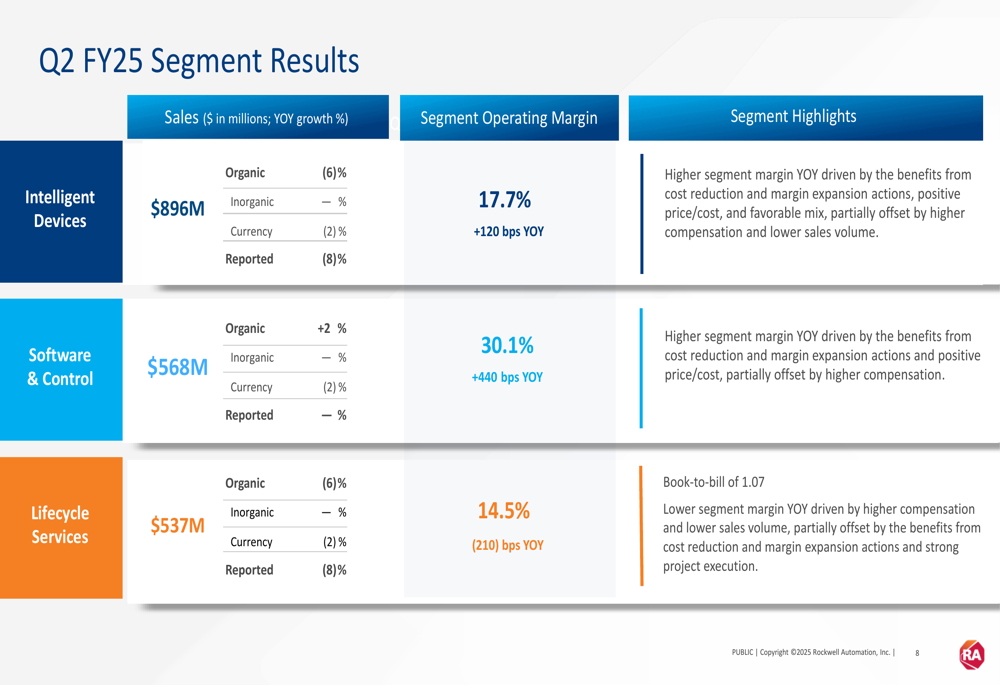

Performance varied significantly across Rockwell’s three business segments, with Software (ETR:SOWGn) & Control emerging as the standout performer:

The Intelligent Devices segment, which accounts for the largest portion of revenue, saw sales decline 8% year-over-year to $896 million. Despite lower volumes, segment operating margin improved by 120 basis points to 17.7%, driven by cost reduction initiatives, positive price/cost dynamics, and favorable mix.

Software & Control was the only segment to achieve organic growth, with sales up 2% organically (flat on a reported basis) to $568 million. The segment delivered exceptional margin performance, with operating margin expanding 440 basis points to 30.1%, reflecting successful cost management and pricing actions.

Lifecycle Services experienced an 8% reported sales decline to $537 million, with organic sales down 6%. Segment operating margin contracted 210 basis points to 14.5%, though the segment maintained a healthy book-to-bill ratio of 1.07.

Industry and Regional Performance

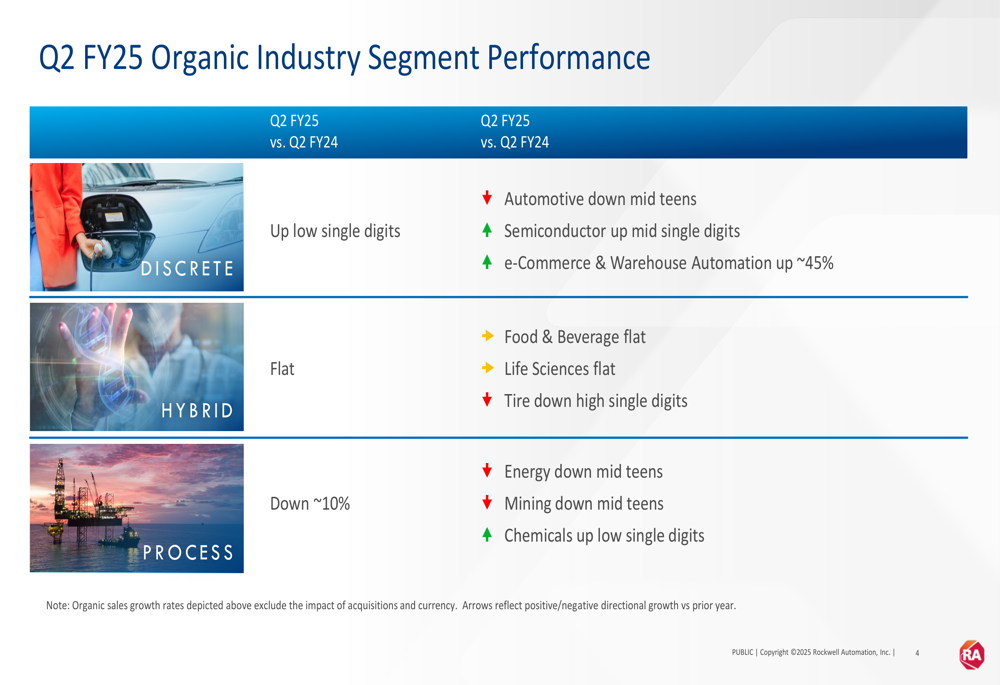

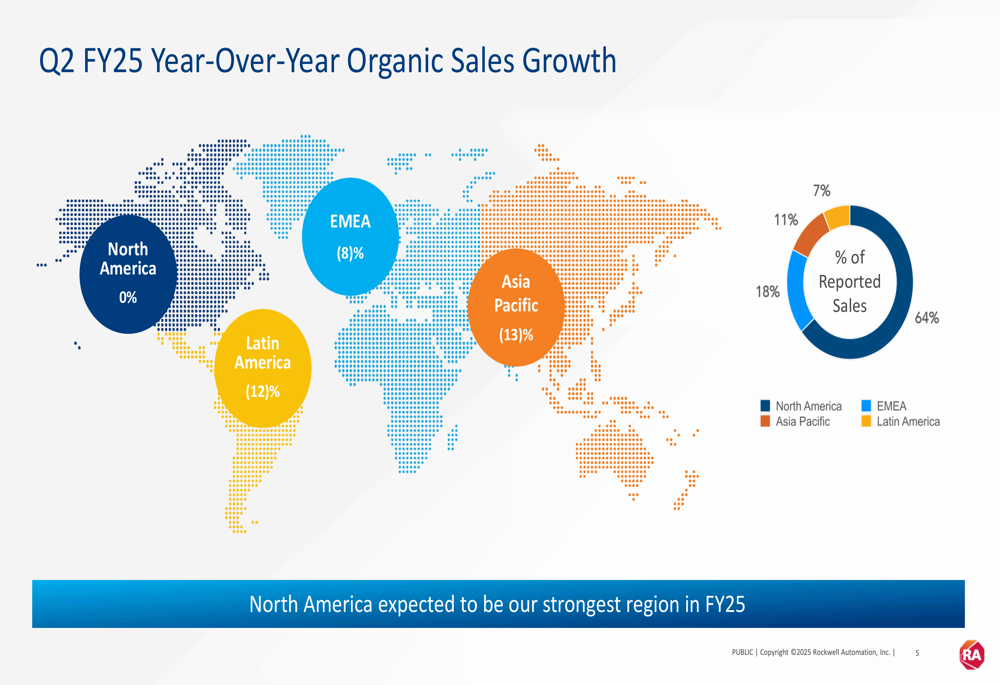

Rockwell’s performance varied significantly across industries and regions, as illustrated in this breakdown:

The discrete automation sector showed low single-digit growth, with semiconductor up mid-single digits and e-commerce & warehouse automation surging approximately 45%, offsetting a mid-teens decline in automotive. Hybrid industries remained flat overall, while process industries declined approximately 10%, with energy and mining both down mid-teens.

Geographically, North America demonstrated resilience with flat organic sales, while other regions experienced significant declines:

North America, which represents 64% of Rockwell’s total sales, is expected to remain the company’s strongest region throughout fiscal 2025. Latin America, EMEA, and Asia Pacific saw organic sales declines of 12%, 8%, and 13%, respectively.

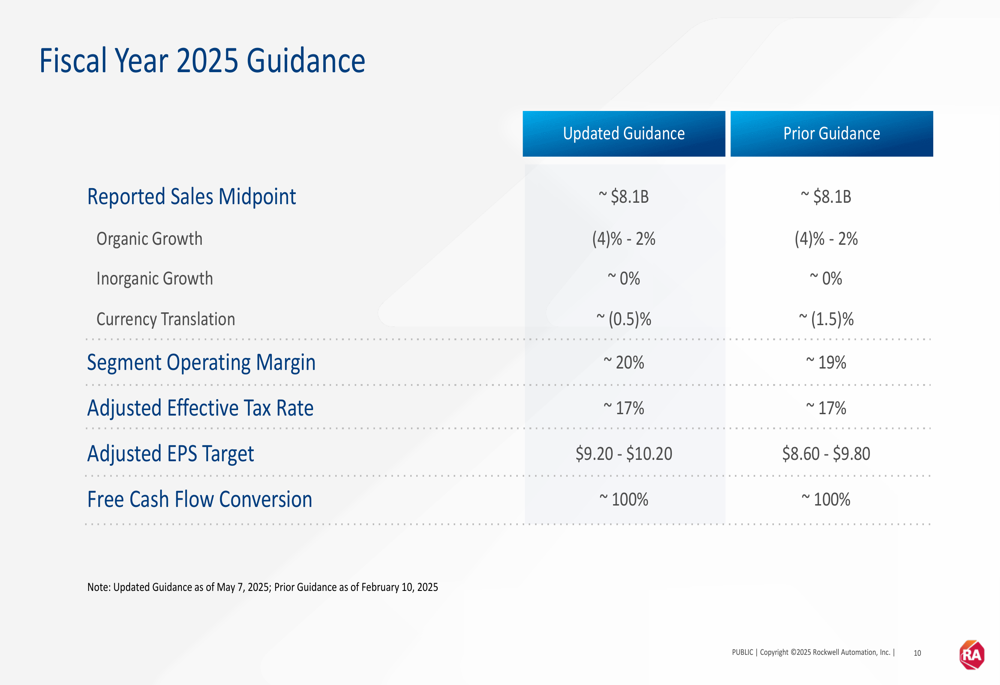

Updated Guidance

Based on its Q2 performance and outlook, Rockwell raised its full-year guidance for fiscal 2025:

While maintaining its organic sales growth range of -4% to 2% year-over-year, the company updated its reported sales growth range to -4.5% to 1.5%, reflecting a less negative currency impact than previously anticipated. Notably, Rockwell raised its segment operating margin guidance to approximately 20%, up from 19% in its prior outlook.

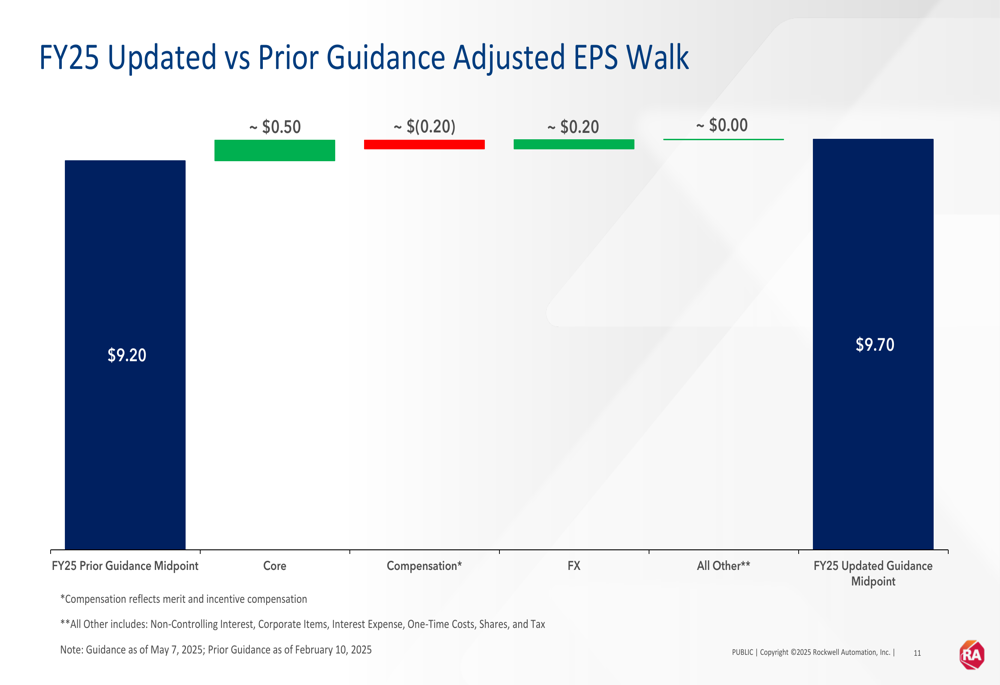

The company also increased its adjusted EPS guidance range to $9.20-$10.20, up from $8.60-$9.80 previously. This improvement is visualized in the following EPS walk:

The guidance upgrade primarily reflects stronger core performance, contributing approximately $0.50 to the EPS midpoint, and favorable foreign exchange impact of approximately $0.20, partially offset by higher compensation costs.

Strategic Initiatives

Rockwell emphasized its progress on cost reduction and margin expansion actions, which are on track to deliver over $250 million in year-over-year productivity benefits in fiscal 2025. These initiatives have helped offset volume declines and support margin improvement.

The company noted strong adoption of recent new product offerings, supporting its strategic focus on innovation. Management indicated that cost impacts from tariffs are expected to be offset through supply chain actions and pricing adjustments.

In its closing remarks, Rockwell highlighted its continued investment in "innovation and resiliency for sustained growth and profitability," signaling its commitment to long-term strategic priorities despite near-term market challenges.

The company’s focus on expanding recurring revenue streams appears to be gaining traction, with total ARR expected to grow approximately 10% year-over-year for the full fiscal year, providing greater stability to its business model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.