AI is a game of kings, and OpenAI knows it

Introduction & Market Context

Rogers Communications Inc (NYSE:RCI) presented its Q1 2025 financial results on April 23, 2025, showing modest growth across key metrics while highlighting significant balance sheet improvements through a strategic investment from Blackstone (NYSE:BX). The Canadian telecommunications giant reported a 2% increase in total service revenue and adjusted EBITDA, alongside a 9% rise in net income compared to the same period last year.

The company’s presentation emphasized its continued subscriber growth momentum, network reliability achievements, and a transformative $7 billion minority equity investment from Blackstone that substantially improves Rogers’ debt position following its Shaw acquisition.

Quarterly Performance Highlights

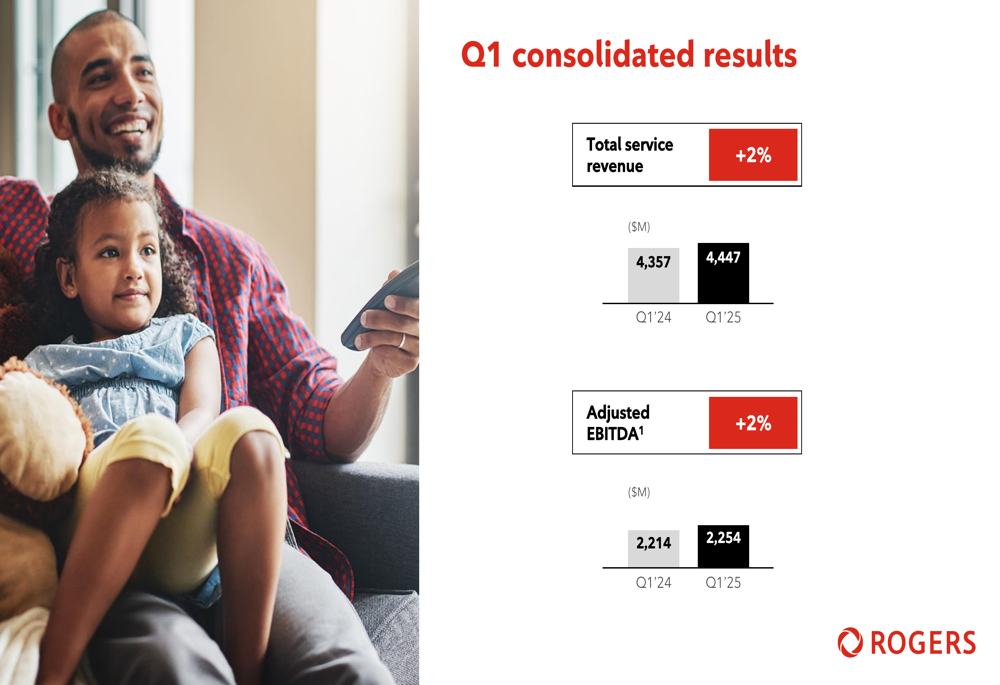

Rogers reported total service revenue of $4,447 million in Q1 2025, representing a 2% year-over-year increase from $4,357 million in Q1 2024. Adjusted EBITDA also grew by 2% to $2,254 million, while net income rose 9% to $280 million.

As shown in the following consolidated results chart:

The company added 57,000 combined mobile phone and retail internet subscribers during the quarter. While this represents continued growth, it marks a slowdown from previous quarters. In Q3 2024, for comparison, Rogers had reported adding 227,000 mobile phone and internet subscribers.

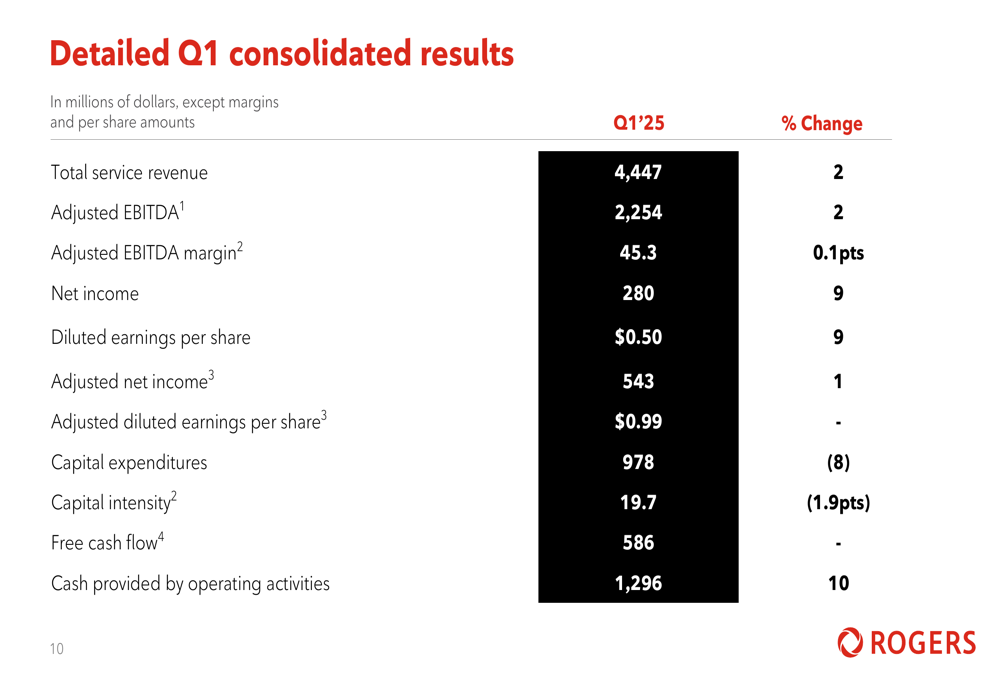

A detailed breakdown of the company’s consolidated financial results shows improvements across multiple metrics:

Particularly notable was the 9% increase in both net income and diluted earnings per share, reaching $280 million and $0.50 respectively. Free cash flow remained stable at $586 million, while cash provided by operating activities increased by 10% to $1,296 million.

Segment Analysis

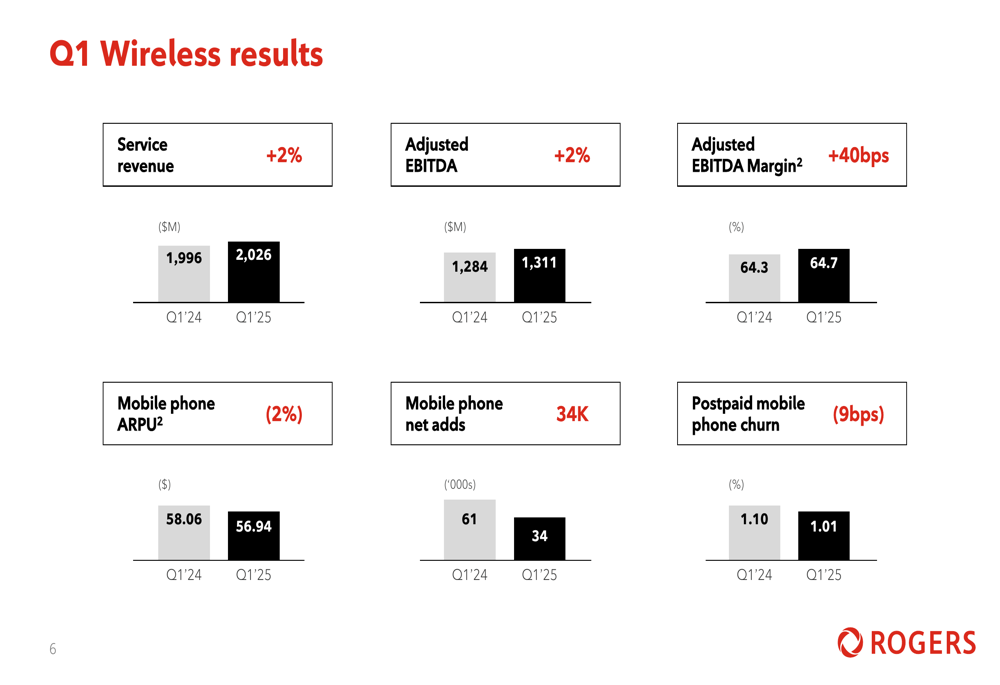

In the wireless segment, Rogers reported service revenue of $2,026 million, up 2% year-over-year, with adjusted EBITDA also increasing by 2% to $1,311 million. The company’s wireless adjusted EBITDA margin improved by 40 basis points to 64.7%.

The wireless results chart illustrates these metrics:

Mobile phone net additions totaled 34,000 for the quarter, down from 61,000 in Q1 2024. However, postpaid mobile phone churn improved by 9 basis points to 1.01%, indicating stronger customer retention. Mobile phone ARPU (average revenue per user) decreased by 2% to $56.94.

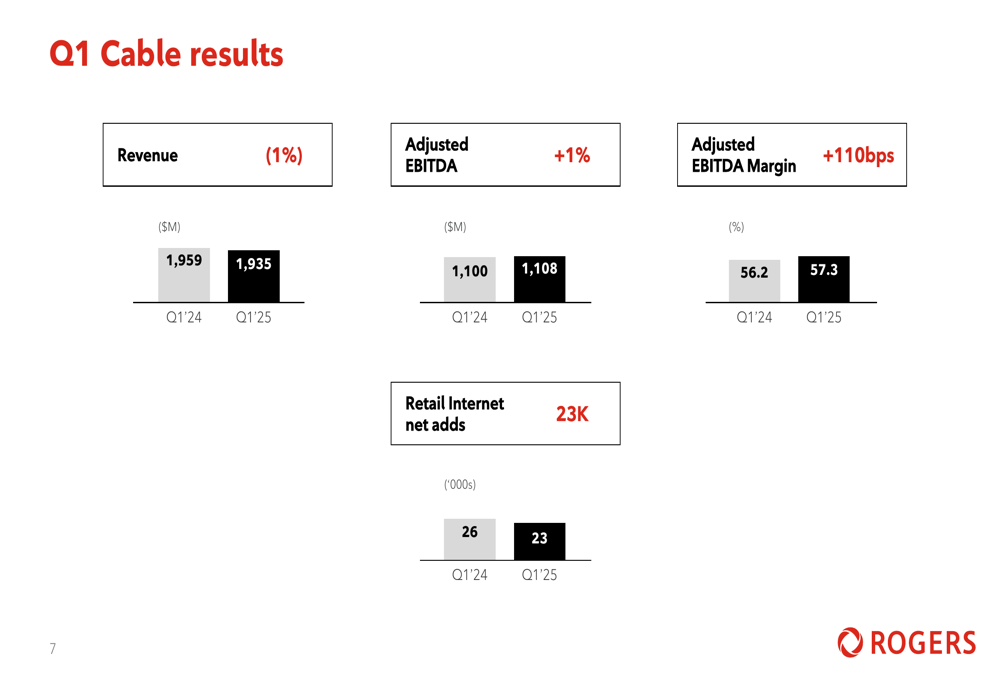

The cable segment saw a 1% decrease in revenue to $1,935 million, but managed to increase adjusted EBITDA by 1% to $1,108 million, with margins improving by 110 basis points to 57.3%. Retail internet net additions were 23,000, slightly down from 26,000 in Q1 2024.

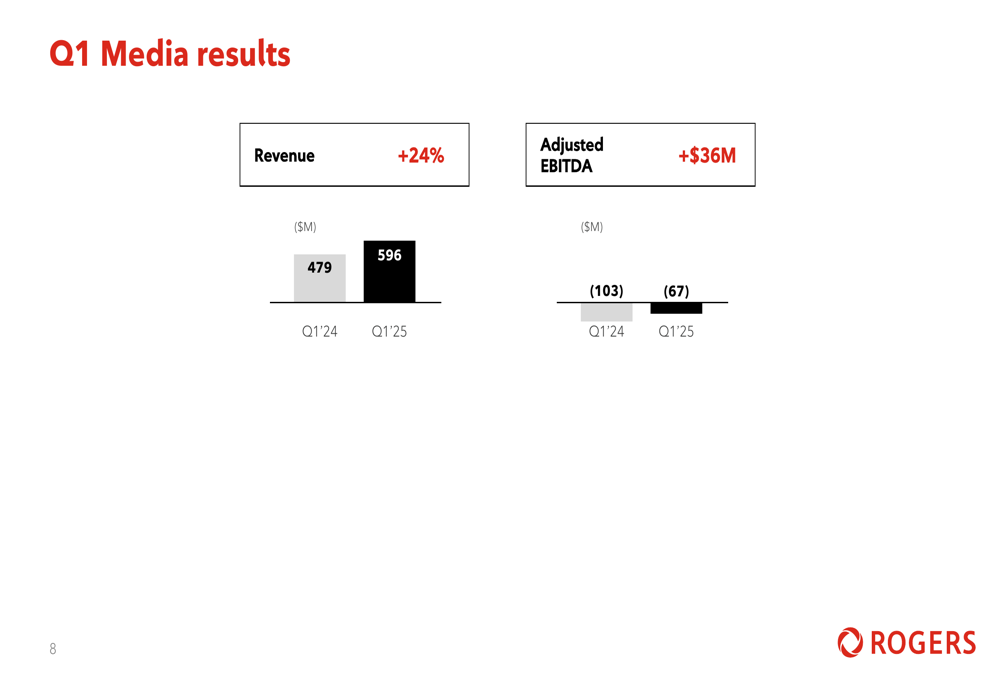

The standout performer was Rogers’ media segment, which delivered exceptional growth with revenue increasing by 24% to $596 million. The segment’s adjusted EBITDA improved by $36 million to -$67 million, continuing the positive trajectory seen in previous quarters.

This strong media performance follows the trend observed in Q3 2024, when the segment reported an 11% revenue increase. The significant acceleration to 24% growth in Q1 2025 likely reflects the impact of Rogers’ strategic content investments, including the newly signed 12-year agreement with the NHL for national media rights.

Capital Expenditures and Financial Position

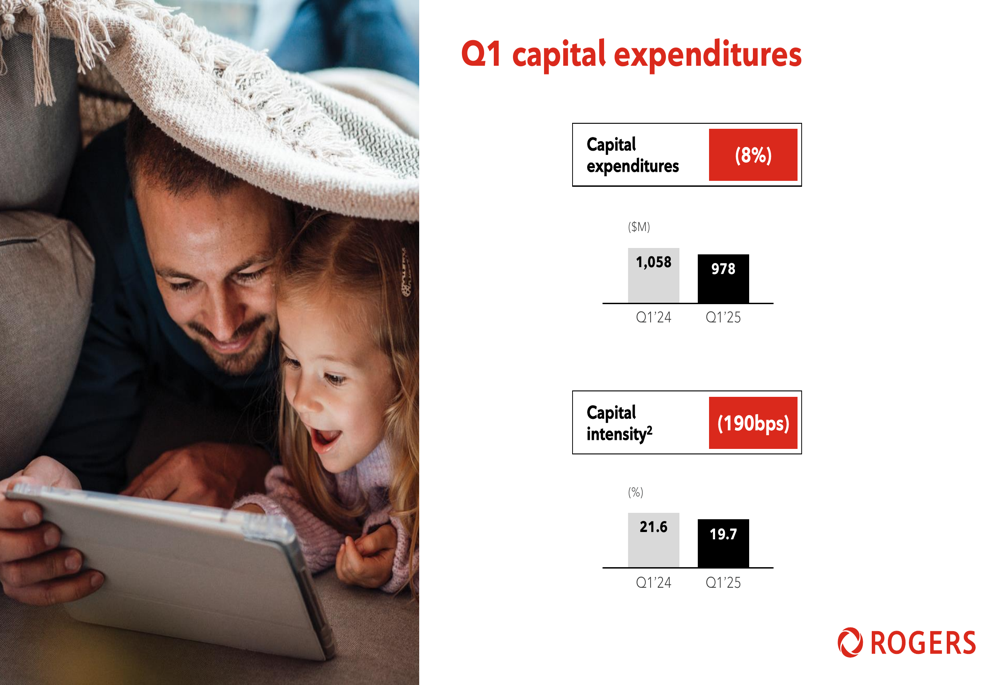

Rogers reported capital expenditures of $978 million for Q1 2025, representing an 8% decrease compared to the same period last year. Capital intensity improved by 190 basis points to 19.7%.

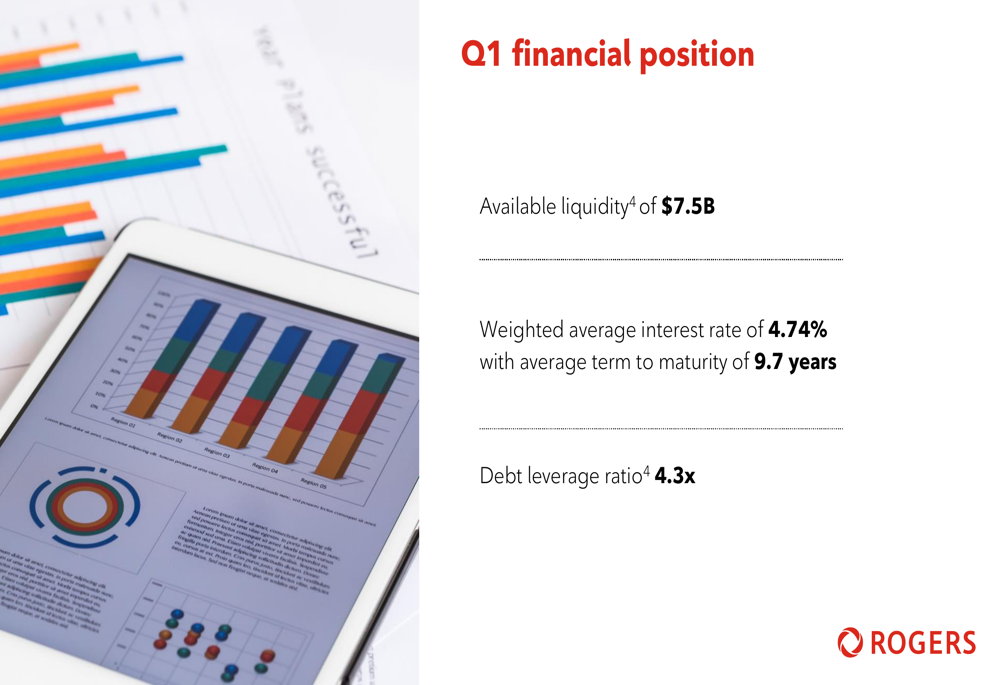

The company’s financial position remains strong, with available liquidity of $7.5 billion and a weighted average interest rate of 4.74% with an average term to maturity of 9.7 years. The debt leverage ratio stood at 4.3x at the end of Q1.

Balance Sheet Improvement

A key highlight of the presentation was the announcement of a $7 billion minority equity investment from Blackstone, which is expected to significantly improve Rogers’ debt position. The company indicated that this investment would reduce its debt leverage ratio to approximately 3.6x, compared to 5.2x following the Shaw acquisition closing.

This development accelerates Rogers’ deleveraging plans and aligns with the company’s previous statements in Q3 2024 about targeting a leverage ratio of around 3.7x by the end of 2024. The removal of the 2% discount on dividend reinvestment plan shares further signals the company’s confidence in its financial position.

Strategic Initiatives

Rogers highlighted several strategic achievements during the quarter, including signing a "monumental" 12-year agreement with the NHL for national media rights across all platforms in Canada. This content acquisition strengthens the company’s media portfolio and supports its position as Canada’s communications and entertainment leader.

The company also emphasized its network leadership, noting that it was recognized as Canada’s most reliable wireless network and most reliable internet by Opensignal. This recognition supports Rogers’ focus on network quality as a key competitive differentiator.

Forward-Looking Statements

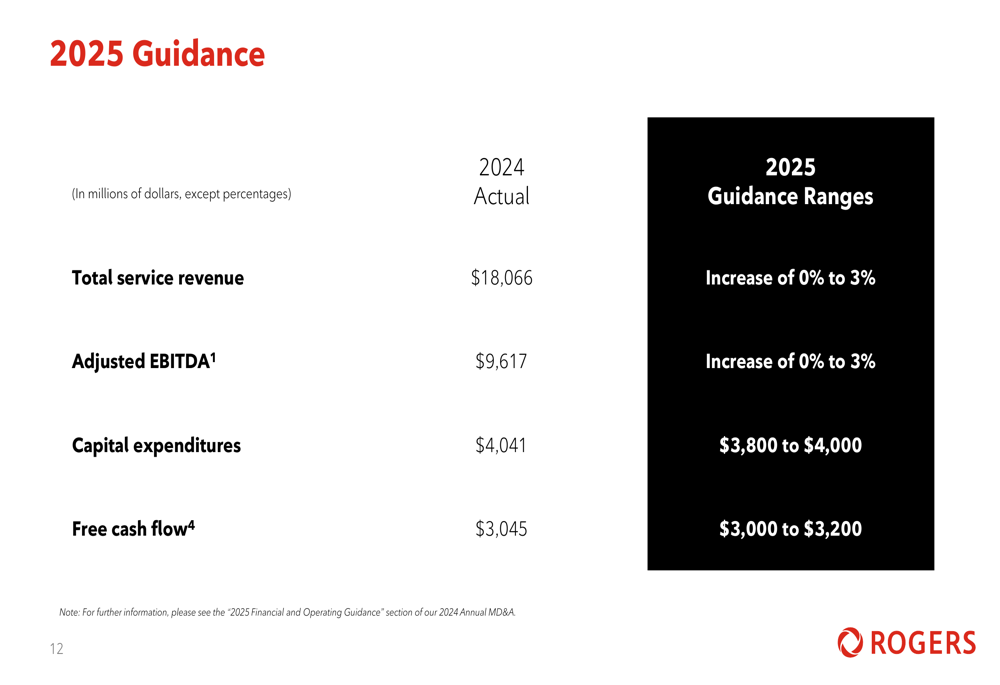

Looking ahead, Rogers provided guidance for 2025, projecting total service revenue growth of 0% to 3% compared to $18,066 million in 2024, and adjusted EBITDA growth of 0% to 3% from $9,617 million in 2024.

Capital expenditures are expected to range between $3,800 million and $4,000 million, down from $4,041 million in 2024. Free cash flow is projected to be between $3,000 million and $3,200 million, compared to $3,045 million in 2024.

These projections suggest Rogers anticipates continued steady performance throughout 2025, maintaining the momentum seen in recent quarters while focusing on operational efficiency and strategic investments in network reliability and content.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.