AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

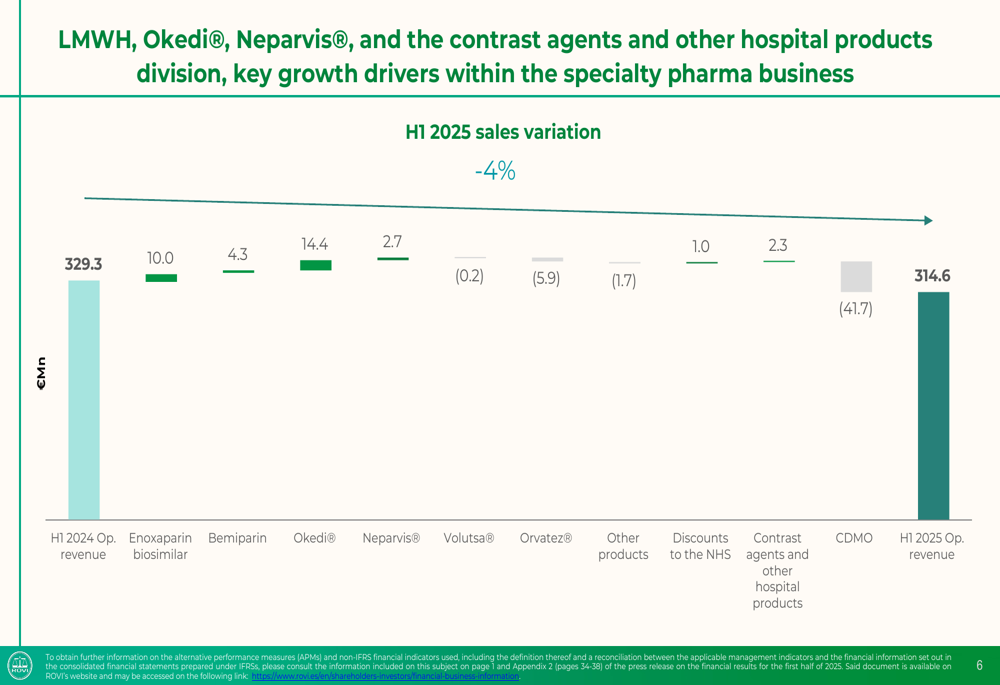

Laboratorios Farmacéuticos ROVI, S.A. (BME:ROVI) presented its first half 2025 financial results on July 24, 2025, revealing a 4% decline in operating revenue to €314.6 million, primarily driven by weakness in its contract development and manufacturing organization (CDMO) business. Despite the overall revenue decline, the company’s specialty pharmaceutical segment showed strong growth, increasing 13% to €237.4 million.

ROVI shares responded positively to the results, trading up 2.84% to €55.80 on the day of the announcement. The stock has been trading near its 52-week low of €45.52, significantly below its 52-week high of €89.50, suggesting investors may be finding value after recent declines.

Quarterly Performance Highlights

ROVI’s first half results revealed divergent performance across business segments. While the specialty pharma business demonstrated robust growth, the CDMO segment experienced a significant decline, impacting overall results.

As shown in the following chart breaking down sales variation by division:

The 4% decrease in operating revenue was primarily attributed to a €41.7 million decline in CDMO business, which overshadowed growth in other segments. The CDMO business decreased by 35% from €118.9 million in H1 2024 to €77.2 million in H1 2025, reflecting challenges in this segment despite ROVI’s continued collaboration with Moderna (NASDAQ:MRNA).

On the positive side, ROVI’s specialty pharma business showed impressive growth, with particularly strong performance from its heparin franchise and Okedi product. The heparin franchise, including both Bemiparin and Enoxaparin biosimilar, grew 12% to €135.2 million.

The following chart illustrates the growth in prescription-based products and the heparin franchise:

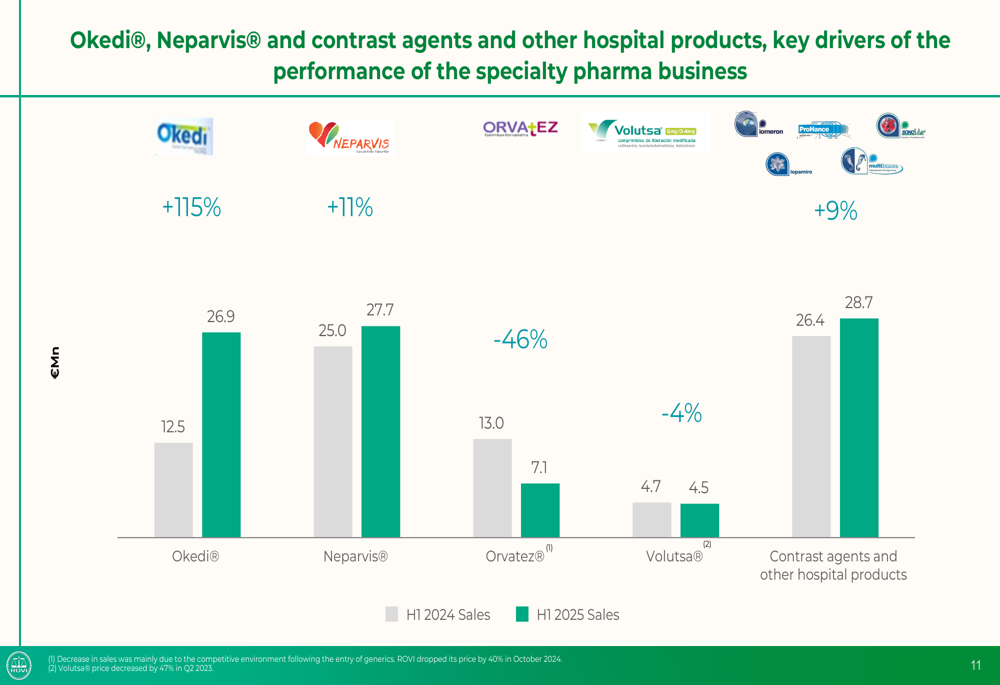

Okedi®, ROVI’s treatment for schizophrenia, was a standout performer with sales surging 115% to €26.9 million compared to H1 2024. Neparvis® also performed well with an 11% increase to €27.7 million. However, Orvatez® sales declined 46% to €7.1 million.

The performance of these key specialty pharma products is illustrated in the following chart:

Detailed Financial Analysis

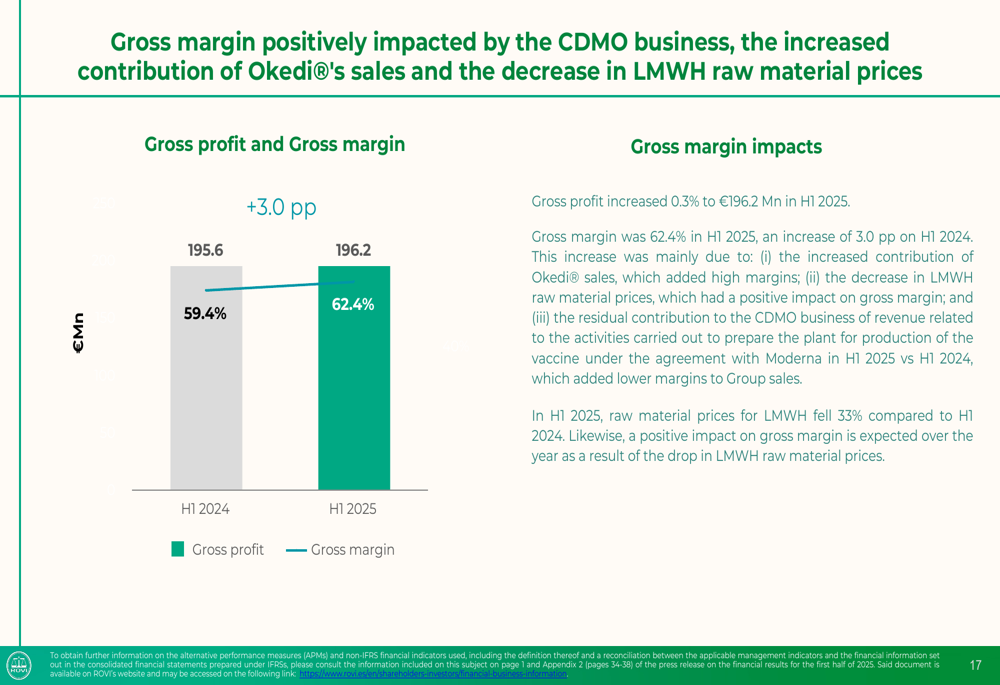

Despite the revenue decline, ROVI managed to improve its gross margin by 3.0 percentage points to 62.4% in H1 2025. This improvement was supported by a 33% decrease in raw material prices for low molecular weight heparins (LMWH) compared to H1 2024.

The gross margin improvement is visualized in the following chart:

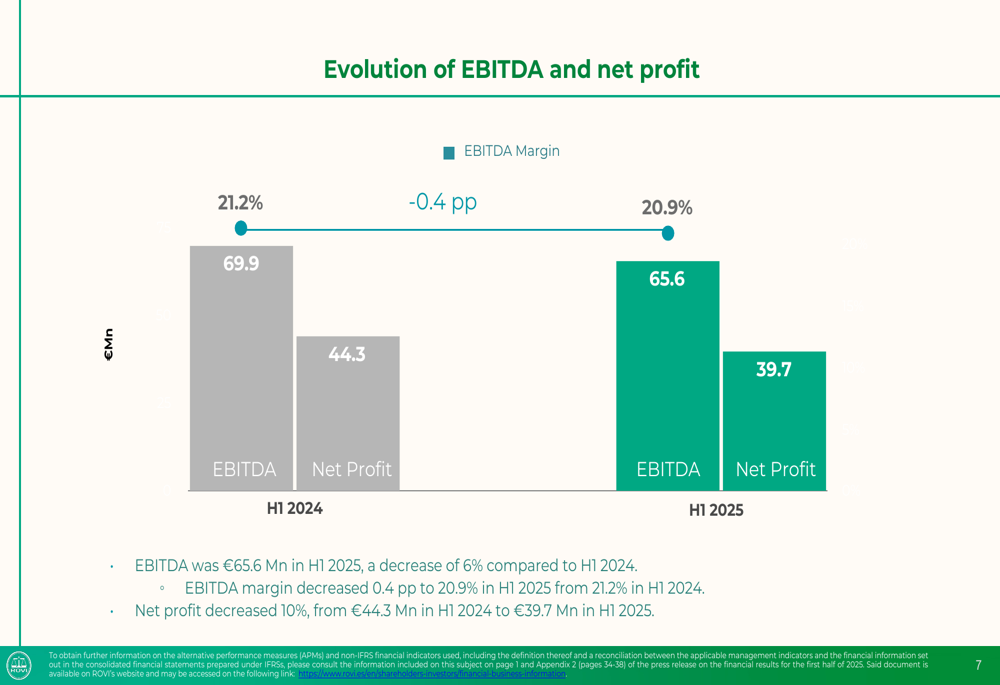

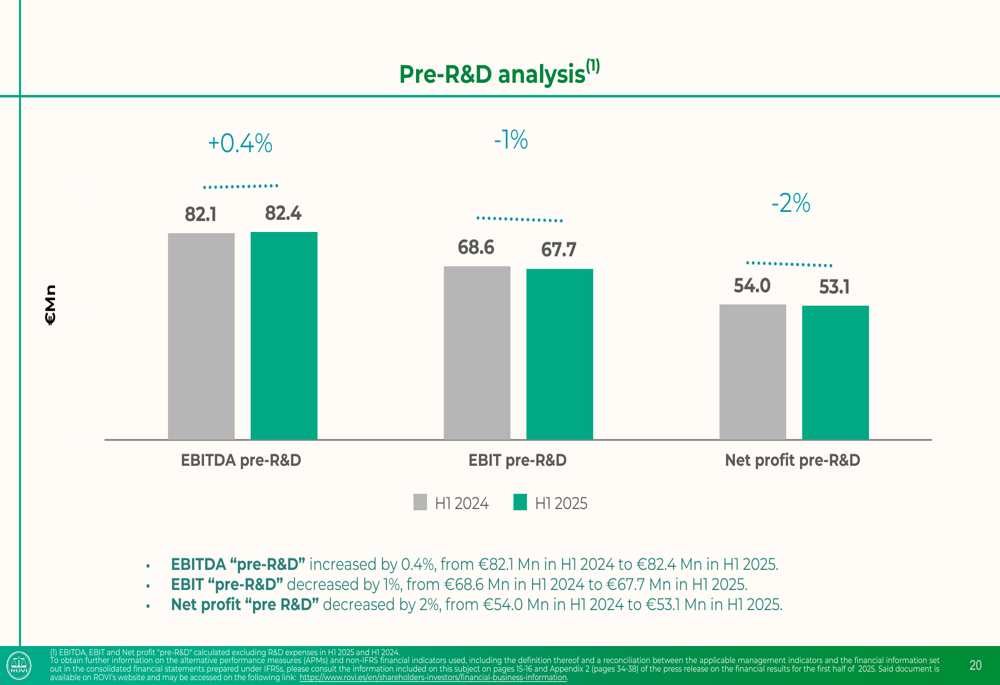

EBITDA decreased 6% to €65.6 million, while net profit fell 10% to €39.7 million. However, the company noted that EBITDA would have increased by 0.5% if R&D expenses had remained at the same level as H1 2024, highlighting the impact of increased investment in research and development.

The following chart shows the evolution of EBITDA and net profit:

R&D expenses increased significantly by 38% to €16.8 million in H1 2025, reflecting ROVI’s commitment to future growth through innovation. Meanwhile, selling, general, and administrative (SG&A) expenses remained stable at €113.7 million.

To provide a clearer picture of underlying performance, ROVI presented "pre-R&D" metrics, which showed more favorable trends:

ROVI maintained a solid financial position with net debt of €79.7 million as of June 30, 2025, an improvement from €85.1 million at the end of December 2024. Capital expenditure increased 12% to €20.8 million, with 55.6% allocated to new filling lines and operations expansion.

Strategic Initiatives

ROVI highlighted several strategic developments during the first half of 2025. The company received a final decision to award aid of €36.3 million for its LAISOLID project, subsidized by the CDTI (Centre for the Development of Industrial Technology). This aid covers the period from January 2023 to August 2026, with ROVI planning to book revenue related to expenses incurred from January 2023 to September 2025.

In a strategic move to diversify its business, ROVI acquired a majority position in Cells IA Technologies, S.L., a company focused on artificial intelligence-assisted diagnosis in pathological anatomy. This acquisition aligns with ROVI’s strategy to expand into new healthcare technologies.

The company continues to expand its international presence, with sales outside Spain representing 55% of operating revenue in H1 2025. However, international sales decreased 8% compared to H1 2024.

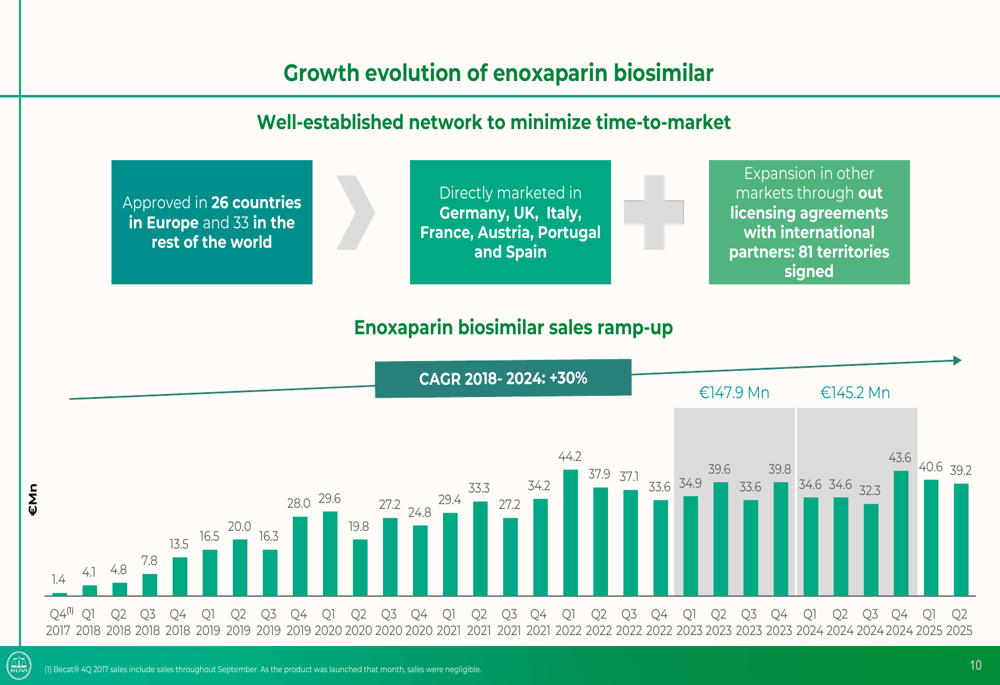

ROVI’s enoxaparin biosimilar has shown impressive long-term growth, with a compound annual growth rate (CAGR) of 30% from 2018 to 2024, as illustrated in the following chart:

The company has established a direct sales network in Germany, UK, Italy, France, Austria, Portugal, and Spain, while expanding into other markets through licensing agreements in 81 territories.

Forward-Looking Statements

Looking ahead, ROVI expects operating revenue to decrease by a mid-single-digit percentage in 2025 compared to 2024, consistent with guidance provided in previous communications. This outlook reflects the continued challenges in the CDMO business while acknowledging growth opportunities in specialty pharma.

Key growth levers for 2025 include:

1. In Specialty Pharma:

- Launch of Risperidone ISM® (Okedi) in new countries

- Continued growth of the LMWH franchise

- Expansion of the existing portfolio of specialty pharmaceuticals

- New product distribution licenses

- New diagnosis solutions powered by artificial intelligence

2. In CDMO:

- Ongoing agreement with Moderna

- Capacity increases

- New formats (cartridges)

The company’s focus on R&D investment, particularly in its ISM® technology platform, underscores its commitment to long-term growth despite near-term revenue challenges. This internally-developed and patented innovative drug-release technology has potential applications in chronic therapeutic areas, including psychiatry and oncology.

ROVI’s first half 2025 results reflect a company in transition, with significant investments being made to support future growth while navigating challenges in its CDMO business. The strong performance of its specialty pharma segment, particularly Okedi, provides a bright spot amid the overall revenue decline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.