AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Laboratorios Farmaceuticos ROVI (BME:ROVI) reported its first quarter 2025 financial results on May 8, showing improved profitability despite modest revenue growth. The Spanish pharmaceutical company’s stock is currently trading at €52.30, down 0.66% today and significantly below its 52-week high of €94.80, reflecting ongoing investor caution about the company’s near-term growth prospects.

The Q1 results follow a challenging fourth quarter of 2024, when ROVI experienced a 7.9% revenue decline. The company continues to navigate what management previously described as "transition years" in 2024 and 2025, with significant investments being made to support future growth while facing headwinds in its contract development and manufacturing organization (CDMO) business.

Quarterly Performance Highlights

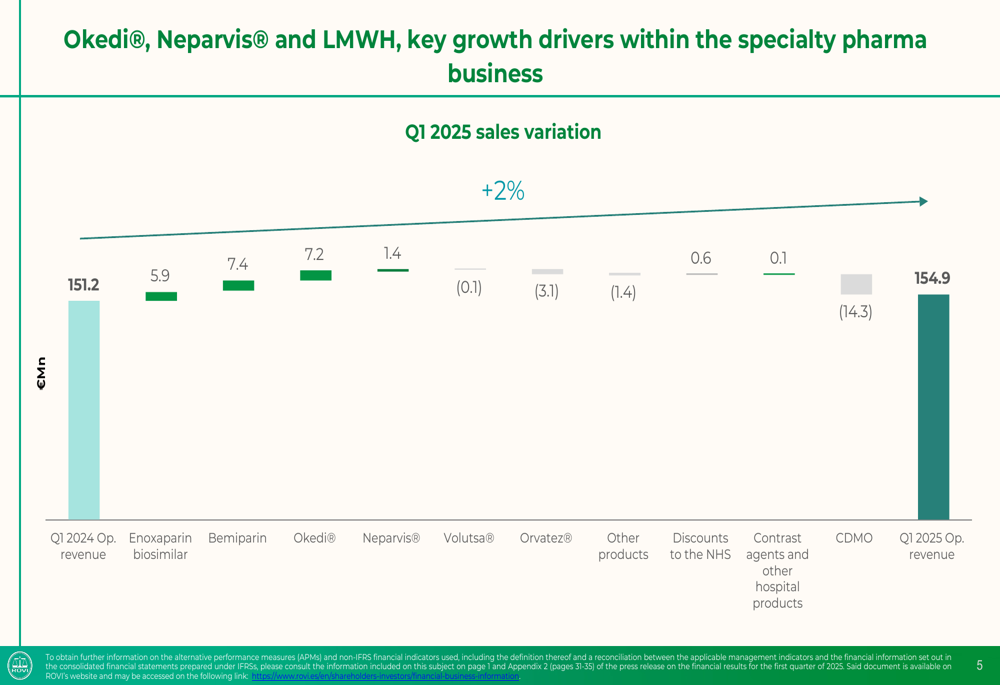

ROVI reported operating revenue of €154.9 million in Q1 2025, representing a 2% increase compared to the same period in 2024. This growth was primarily driven by the specialty pharmaceutical business, which increased 18% to €119.1 million.

The standout performer was Okedi® (Risperidone ISM®), ROVI’s treatment for schizophrenia, which saw sales surge 133% year-over-year to €12.6 million. This impressive growth demonstrates the successful commercialization of this product, which also showed sequential growth of 48% compared to Q4 2024.

As shown in the following chart detailing the company’s sales variation:

The heparin franchise also delivered strong results, with sales increasing 24% to €69.6 million. Within this segment, bemiparin sales rose 38% to €27.1 million, while enoxaparin sales increased 17% to €40.6 million. The company noted that the growth was partly due to greater concentration of orders in the quarter.

Meanwhile, ROVI’s CDMO business continued to face challenges, with sales decreasing 29% to €35.8 million, creating a significant drag on overall performance.

Detailed Financial Analysis

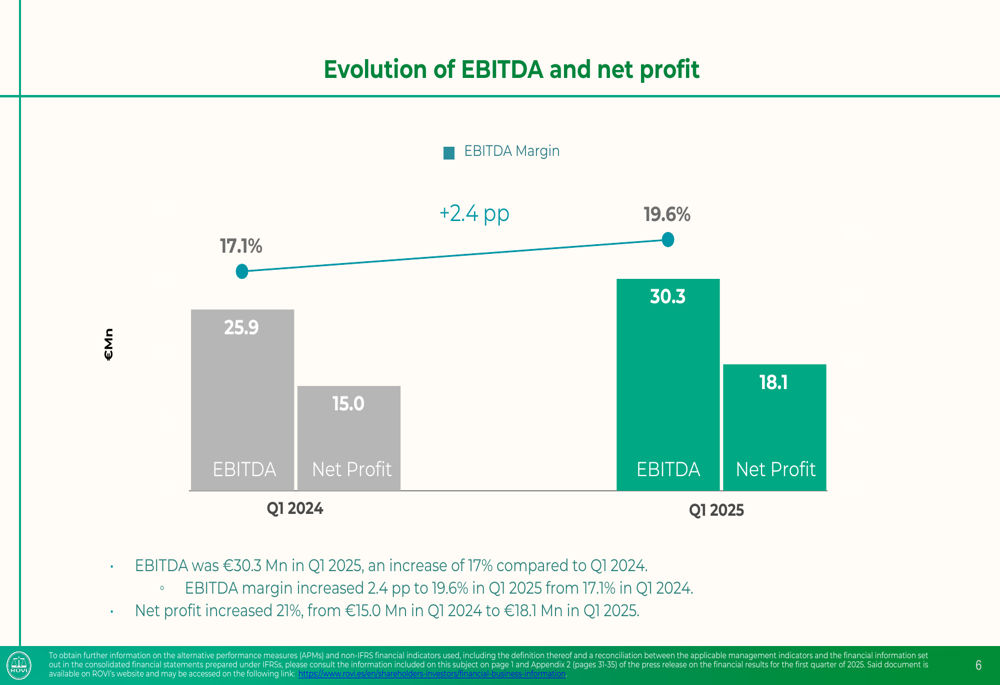

ROVI’s profitability metrics showed substantial improvement in Q1 2025. EBITDA increased 17% to €30.3 million, with the EBITDA margin expanding by 2.4 percentage points to 19.6%. Net profit rose 21% to €18.1 million compared to Q1 2024.

The following chart illustrates this positive trend in EBITDA and net profit:

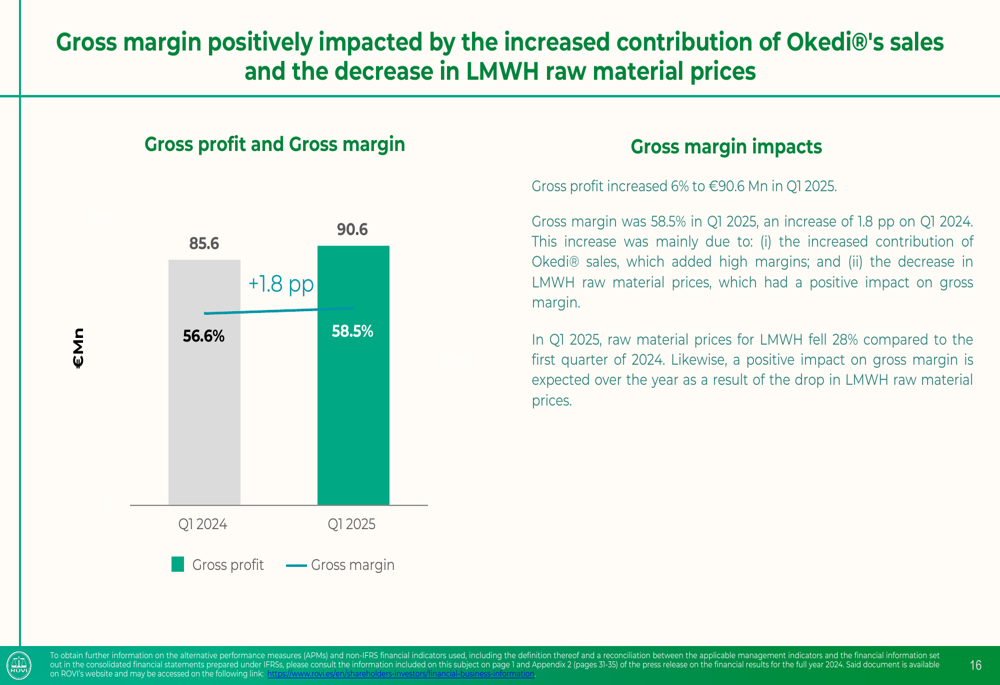

Gross margin improved to 58.5%, up 1.8 percentage points from 56.6% in Q1 2024. This margin expansion was attributed to Okedi’s high-margin contribution and lower low molecular weight heparin (LMWH) raw material prices, which fell 28% compared to Q1 2024.

As shown in the gross margin analysis below:

Operating expenses remained well controlled, with SG&A expenses increasing just 1% to €54.0 million, while R&D expenses rose 2% to €6.2 million. The SG&A to operating revenue ratio improved slightly to 34.9% from 35.5% in Q1 2024.

ROVI’s financial position remains solid, with the company reporting net debt of €77.1 million as of March 31, 2025. Capital expenditure decreased by 8% to €8.3 million, while cash flow from operating activities increased by 21%.

Strategic Initiatives

ROVI continues to advance its internationalization strategy, with international sales now representing 55.1% of total operating revenue, up from 53.4% in Q1 2024. Sales outside Spain increased 6% during the quarter.

The following chart shows the increasing importance of international markets to ROVI’s business:

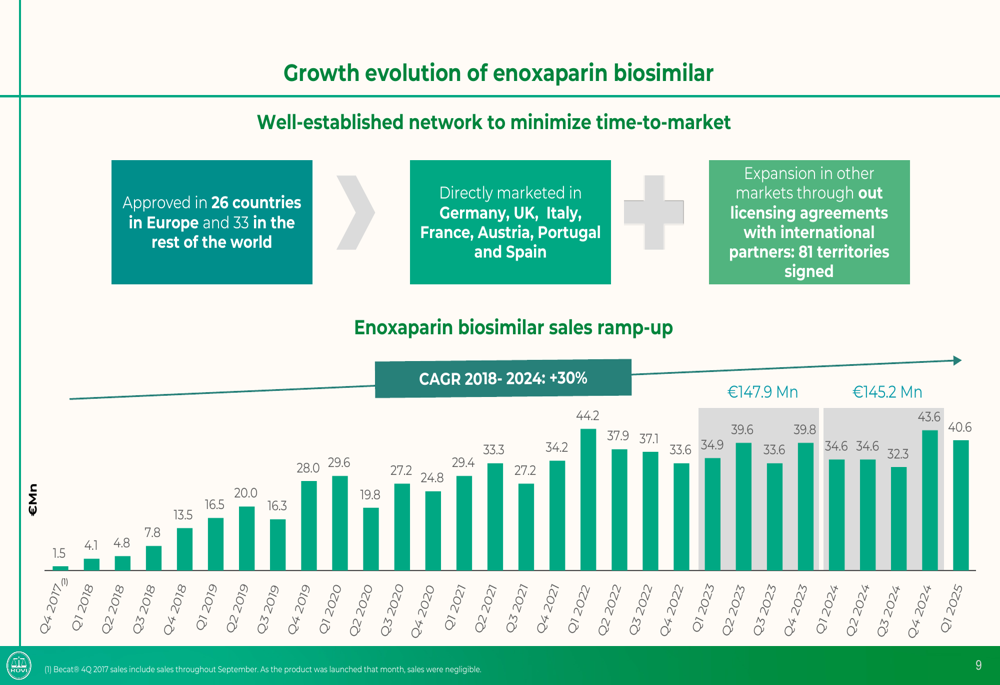

The company’s enoxaparin biosimilar has been a key driver of international growth, with the product now approved in 26 countries in Europe and 33 countries in the rest of the world. ROVI directly markets the product in seven European countries and has signed out-licensing agreements covering 81 territories.

The growth trajectory of the enoxaparin biosimilar is illustrated in this chart:

ROVI’s ISM® technology platform remains a strategic focus for long-term growth. The company is advancing several products based on this platform, including Risperidone ISM® (monthly) for schizophrenia, which is already approved, and other products in clinical development such as Letrozole ISM® for breast cancer.

In the CDMO business, despite current challenges, ROVI maintains its 10-year agreement with Moderna (NASDAQ:MRNA) for seasonal COVID and RSV vaccines. The company’s facilities in Madrid received FDA approval in Q3 2023 and Q2 2024, while its Granada plant was approved in 2024, positioning ROVI for potential future growth in this segment.

Forward-Looking Statements

Despite the positive Q1 results, ROVI maintained its cautious outlook for 2025, expecting operating revenue to decrease by a mid-single-digit percentage compared to 2024. This guidance aligns with management’s previous characterization of 2024 and 2025 as "transition years."

The company identified several growth levers for its specialty pharmaceutical business, including:

- Further launches of Risperidone ISM® in new countries

- Continued growth of the LMWH franchise

- Expansion of the existing portfolio of specialty pharmaceuticals

- New product distribution licenses

- New diagnosis solutions powered by artificial intelligence

For the CDMO segment, ROVI is focusing on:

- Acquiring new business

- Leveraging its agreement with Moderna

- Increasing capacity

- Developing new formats (cartridges)

The expected news flow for 2025 includes potential marketing authorizations for enoxaparin biosimilar outside Europe, progress in Moderna’s product manufacturing, announcements of new contracts, and further marketing of Okedi® in Europe and the rest of the world.

While ROVI faces near-term challenges, particularly in its CDMO business, the strong performance of its specialty pharmaceutical segment and improving profitability metrics suggest the company’s strategic investments may be positioning it for stronger growth beyond 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.