Trading Nvidia earnings report? These are the entry and exit levels to watch for

Russel Metals Inc . (TSX:RUS) presented its Q1 2025 results during an investor conference call on May 7, 2025, highlighting a significant recovery from the previous quarter’s disappointing performance. The company reported record quarterly shipments, improved margins, and continued strategic investments in value-added capabilities and U.S. expansion.

Quarterly Performance Highlights

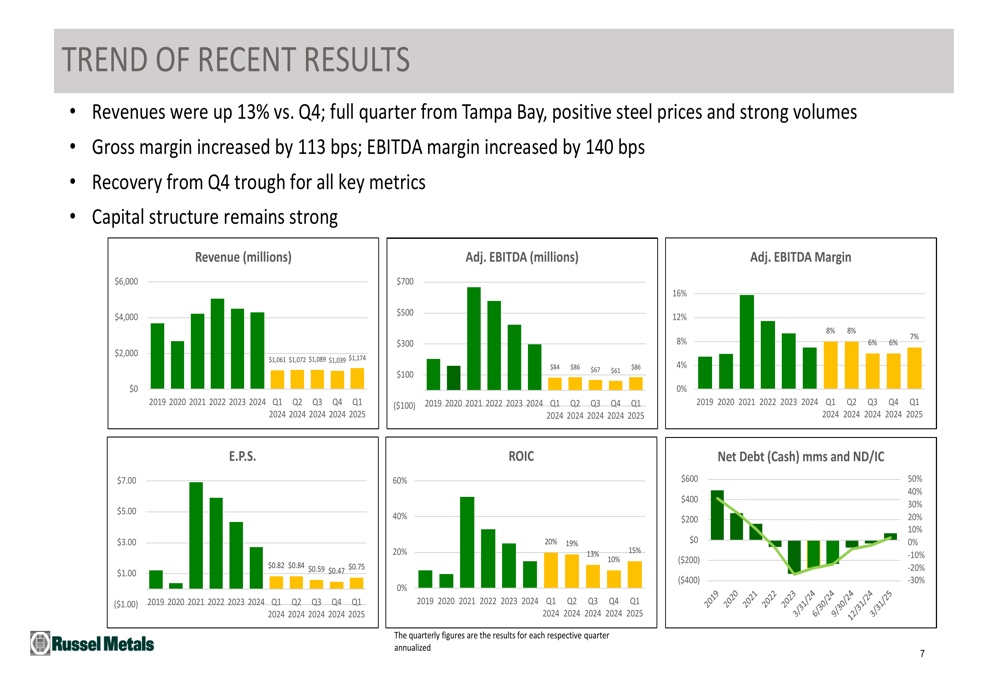

Russel Metals delivered a strong financial rebound in Q1 2025, with revenues reaching $1.17 billion, representing a 13% increase from Q4 2024’s $1.04 billion. This growth was driven by record quarterly shipments, positive steel prices, and a full quarter contribution from the Tampa Bay acquisition.

"We generated strong results across all key metrics, with record quarterly shipments and improved margins," the company noted in its presentation. EBITDA rose to $86 million, up from $61 million in Q4 2024, while earnings per share increased to $0.75 from $0.47 in the previous quarter.

As shown in the following chart of recent financial trends, the company has recovered from its Q4 trough across all key performance indicators:

The company’s gross margin improved to 22% (up 113 basis points from Q4), while EBITDA margin increased to 7% (up 140 basis points). This recovery follows Russel Metals’ disappointing Q4 2024 results, which had missed analyst expectations with EPS falling short by 25%.

Detailed Financial Analysis

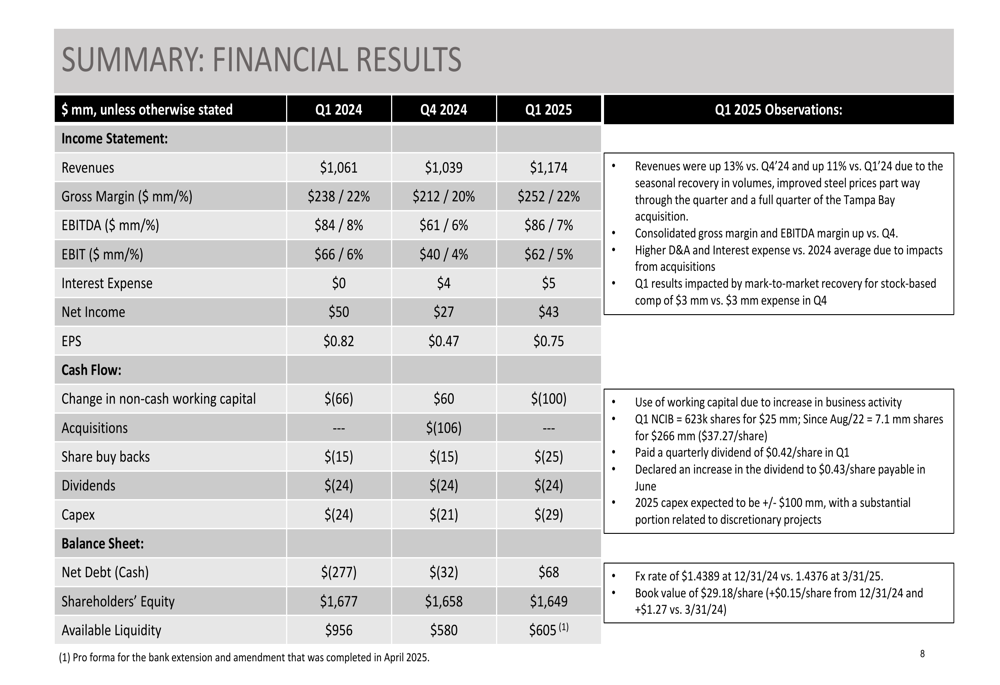

The Q1 2025 financial results show improvements across all segments, with particularly strong performance in the Metal Service Centers division. This segment benefited from a full quarter of contribution from the Tampa Bay acquisition and a strong market environment, resulting in significant increases in prices, margins, and EBIT compared to Q4.

The following financial summary provides a detailed comparison of key metrics across recent quarters:

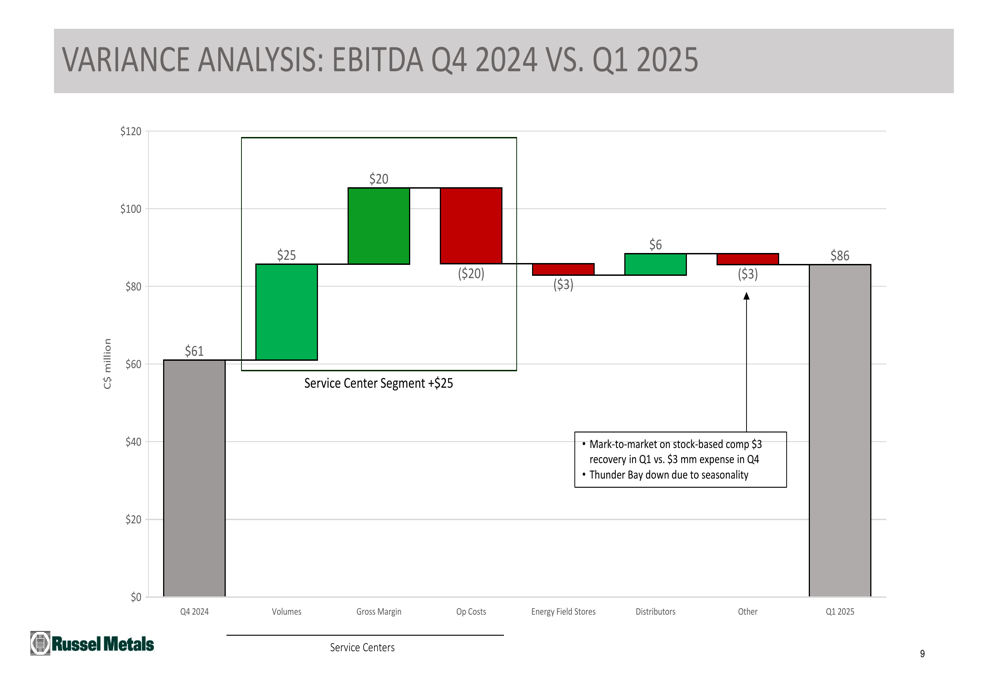

An EBITDA variance analysis reveals that the $25 million improvement from Q4 2024 to Q1 2025 was primarily driven by increased volumes ($25 million positive impact) and improved gross margins ($20 million positive impact), partially offset by higher operating costs ($20 million negative impact).

The company’s Metal Service Centers achieved record quarterly tons shipped, up 14% versus Q4 and 11% on a same-store basis. Price realizations per ton increased while cost of goods sold per ton decreased, resulting in a gross margin per ton of $430, up $62 per ton from Q4.

Strategic Initiatives

Russel Metals continues to execute its strategic priorities, focusing on U.S. expansion and increasing its specialty and value-added product offerings. The U.S. now represents 44% of total revenues, up from 39% in 2024 and 30% in 2019. Similarly, stainless steel and aluminum products have grown to 11% of revenues in Q1 2025, compared to 9% in 2024.

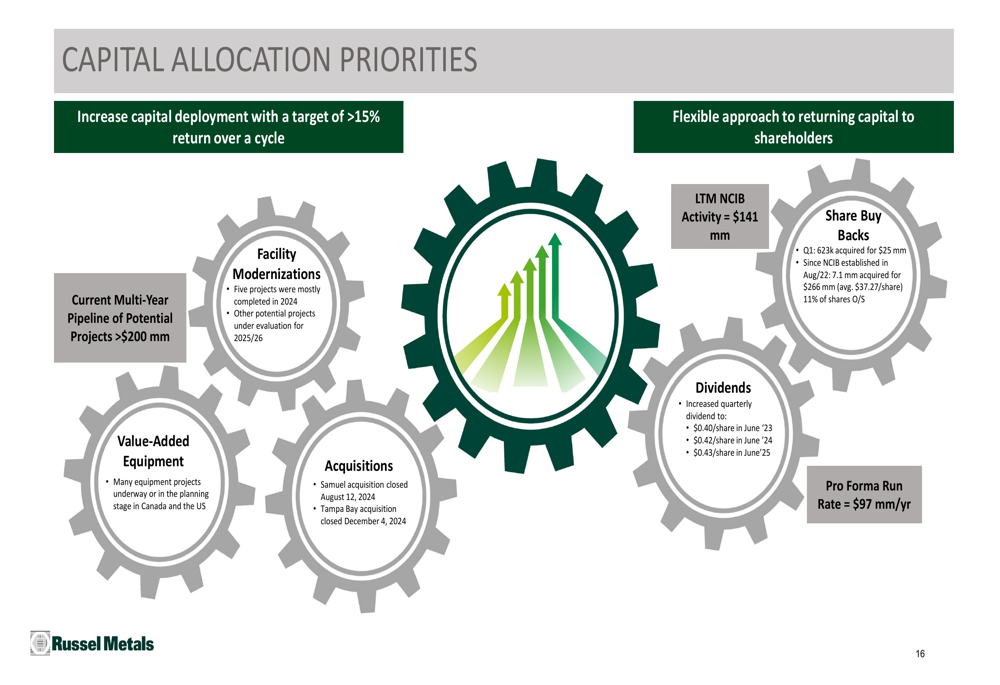

The company’s capital allocation priorities reflect this strategic direction, with investments targeted at facility modernizations, value-added equipment, and acquisitions, while maintaining shareholder returns through dividends and share buybacks.

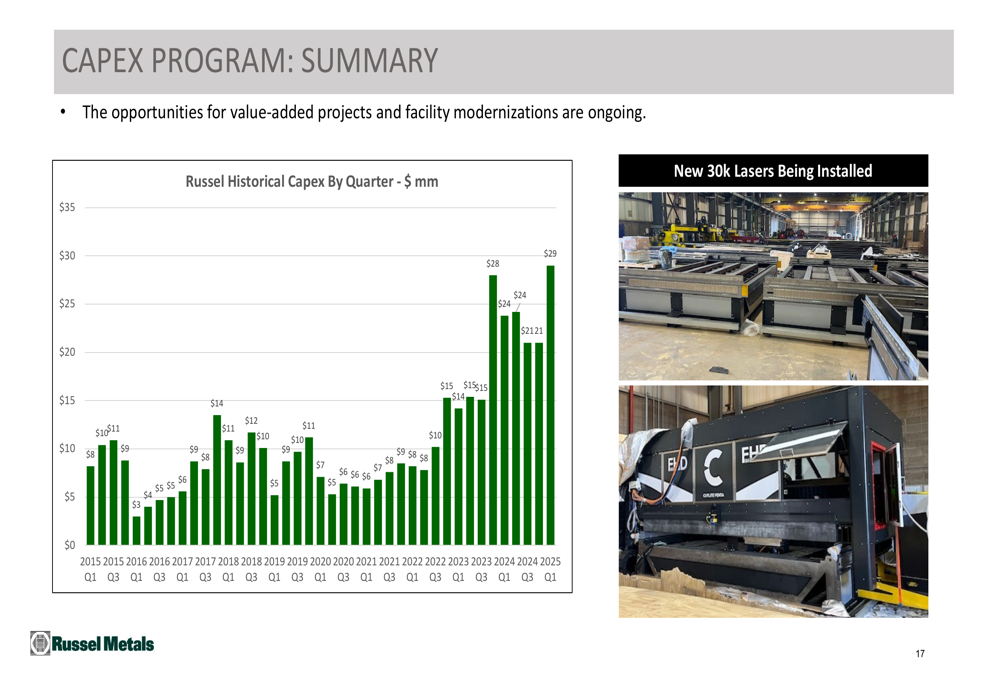

Capital expenditures reached a record quarterly high of $29 million in Q1 2025, with the company on track to invest approximately $100 million throughout 2025. These investments include new equipment installations, such as 30k lasers, aimed at enhancing value-added capabilities.

"The opportunities for value-added projects and facility modernizations are ongoing," the company stated, highlighting its commitment to long-term growth and operational improvements.

Financial Position and Shareholder Returns

Russel Metals maintained a strong financial position while balancing growth investments with shareholder returns. The company completed an inaugural investment grade term debt offering of $300 million at 4.423% due in 2030, while extending and amending its credit facility to April 2029.

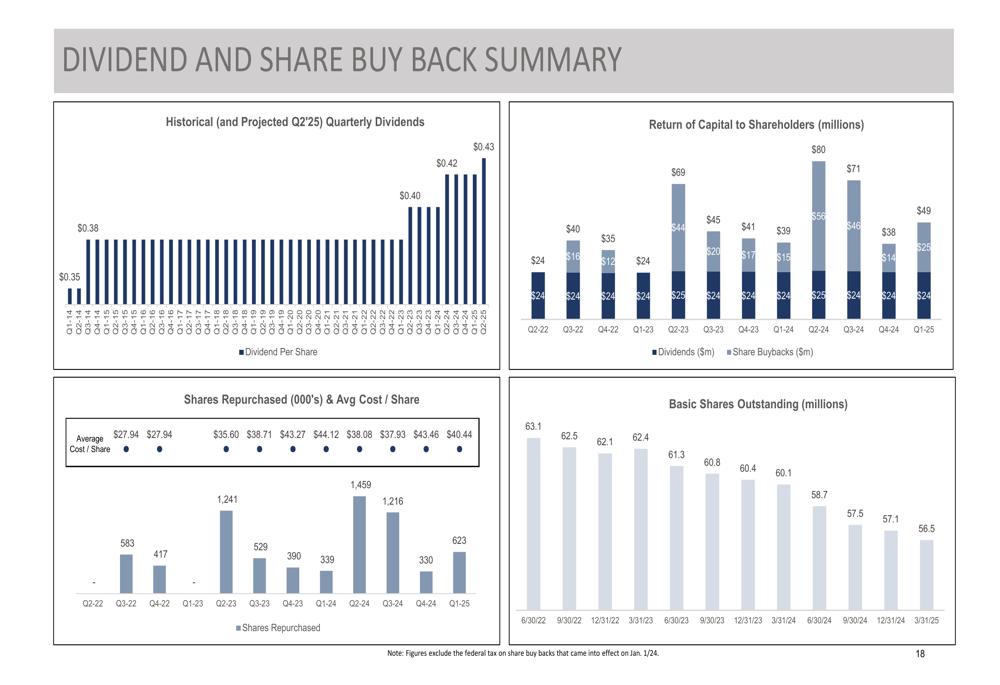

Despite these investments, the company returned significant capital to shareholders, with $25 million allocated to share buybacks and $24 million to dividends during Q1 2025. The company has consistently maintained its dividend payments, with a current run rate of $97 million per year.

The following chart illustrates the company’s dividend and share buyback activity:

Forward-Looking Statements

Looking ahead, Russel Metals appears well-positioned to continue its growth trajectory, with a strong focus on expanding its U.S. presence and value-added capabilities. The company’s return on invested capital improved to 15% in Q1 2025, up from 10% in Q4 2024, though still below its three-year average of 24%.

The company’s strong balance sheet, with liquidity of $605 million as of March 31, 2025, provides flexibility for future growth opportunities and potential acquisitions. Management emphasized that its capital deployment is targeted to achieve returns exceeding 15% over a business cycle.

Market conditions remain favorable, with positive trends in carbon and specialty metals pricing. However, investors should monitor seasonal patterns in the energy field stores segment, which experienced a slow start to 2025 before picking up in March.

Russel Metals shares closed at $40.52 on May 6, 2025, down 0.76% ahead of the earnings presentation. The stock has traded between $34.62 and $46.87 over the past 52 weeks, suggesting potential upside if the company continues to deliver on its recovery and growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.