AirNet Technology raises $180 million in digital assets offering

Sabre Corporation (NASDAQ:SABR) shares plummeted over 30% in Thursday trading after the travel technology provider’s second-quarter presentation revealed missed targets and significantly reduced full-year guidance. The company reported modest revenue growth but fell short of its own projections across key metrics.

Quarterly Performance Highlights

Sabre reported Q2 2025 revenue of $687 million, representing just 1% year-over-year growth, below the company’s guidance of "low single-digit" growth. Normalized Adjusted EBITDA came in at $127 million, up 6% year-over-year but below the guided ~$140 million. Pro Forma Free Cash Flow was negative at ($2 million), missing the company’s expectation for positive cash flow.

As shown in the following summary of Q2 performance:

The company’s distribution business showed minimal growth, with Air Distribution Bookings up just 1% year-over-year to 76 million and Passengers Boarded increasing 1% to 171 million. Hotel Distribution Bookings performed slightly better at 11 million, up 2% year-over-year with a 100 basis point improvement in attachment rate.

Revised Guidance and Outlook

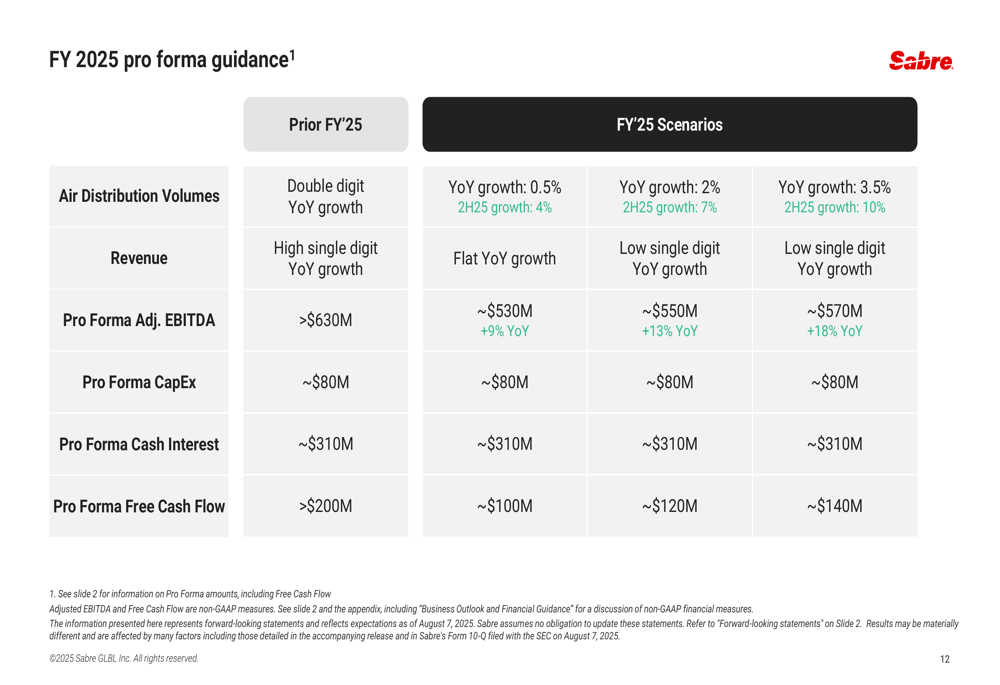

In a significant revision to previous forecasts, Sabre drastically reduced its full-year 2025 guidance. The company now expects Air Distribution Volumes to grow between 4-10%, down from the previous projection of "double-digit" growth. Revenue guidance was cut from "high single-digit" growth to "flat to low single-digit" growth, while Pro Forma Adjusted EBITDA expectations were lowered from over $630 million to a range of $530-$570 million.

The following slide illustrates the company’s revised guidance scenarios:

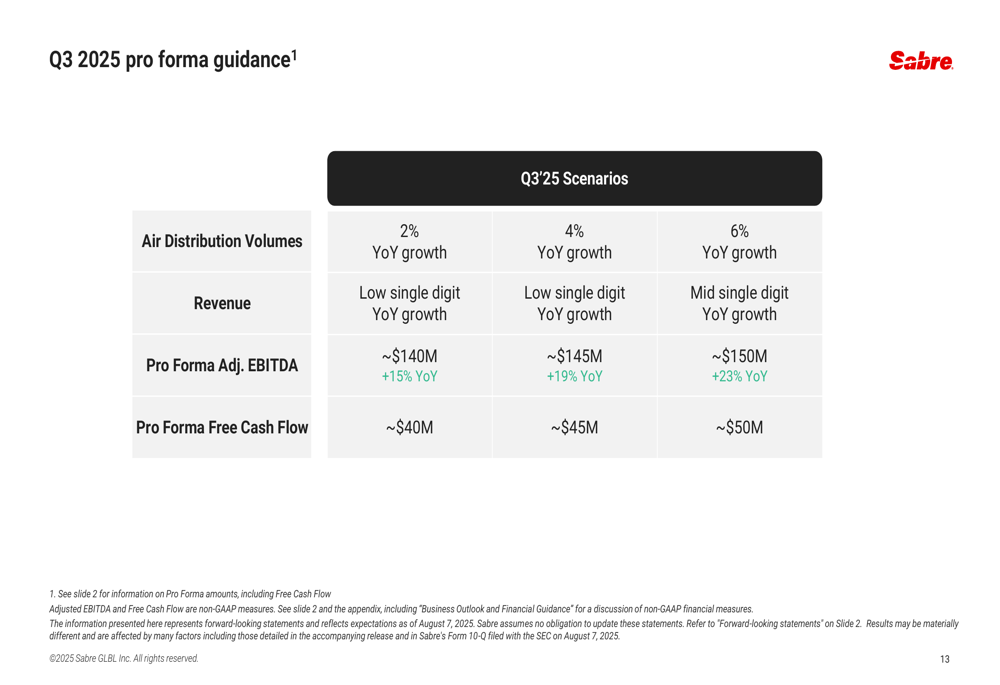

For the third quarter, Sabre provided a range of scenarios based on Air Distribution Volume growth of 2%, 4%, or 6%, with corresponding Pro Forma Adjusted EBITDA projections of $140 million, $145 million, or $150 million, respectively.

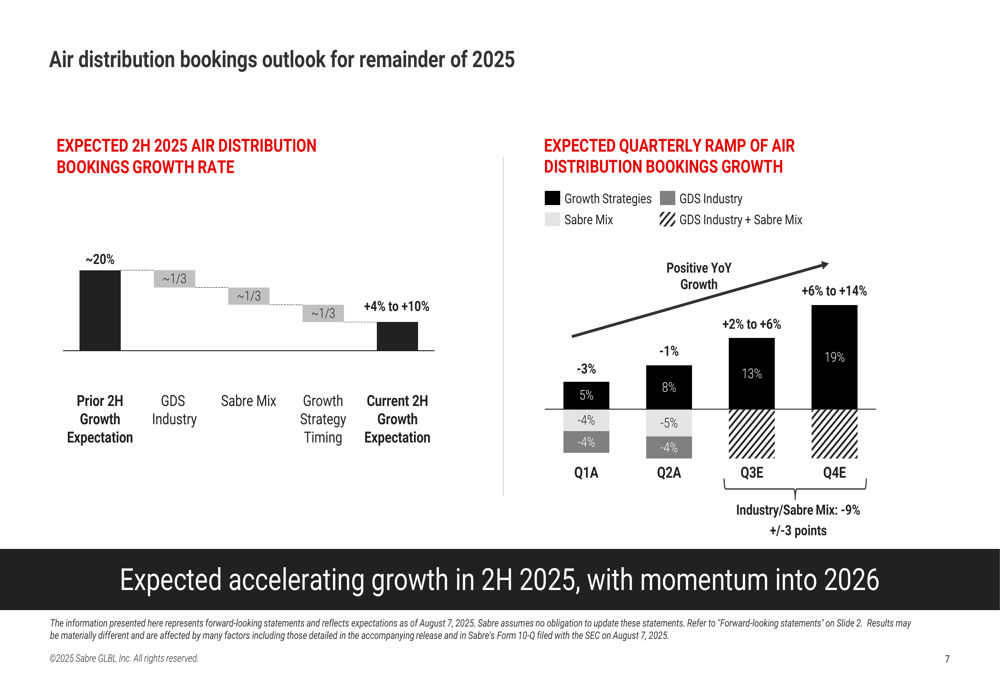

CEO Kurt Ekert explained the company’s expected acceleration in bookings during the second half of 2025, with projected growth of 13% in Q3 and 19% in Q4, following the disappointing first half performance:

Debt Reduction Progress

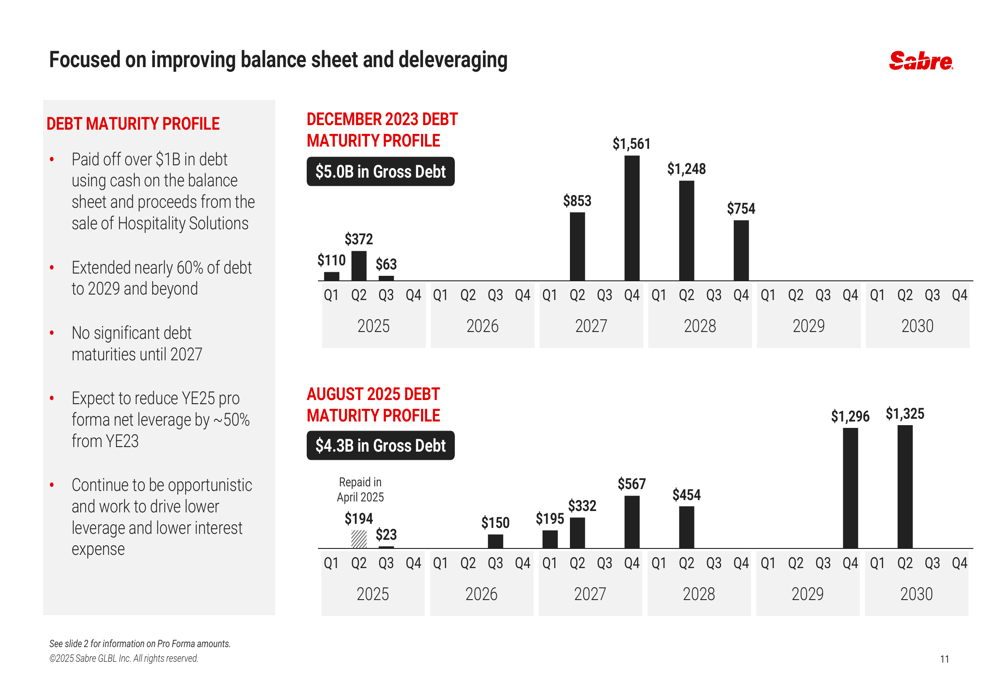

Despite operational challenges, Sabre has made substantial progress in strengthening its balance sheet. The company has paid down over $1 billion in debt, reducing its total debt to approximately $4.3 billion, with net debt of approximately $3.7 billion as of July 31, 2025. Management highlighted that they have successfully extended nearly 60% of debt maturities to 2029 and beyond, with no significant maturities until 2027.

The following chart illustrates the improvement in Sabre’s debt maturity profile:

"We expect to reduce year-end 2025 pro forma net leverage by approximately 50% from year-end 2023," stated Mike Randolfi, EVP & CFO, during the presentation. The company indicated it would continue to be opportunistic in its approach to further reduce leverage and interest expense.

Growth Initiatives

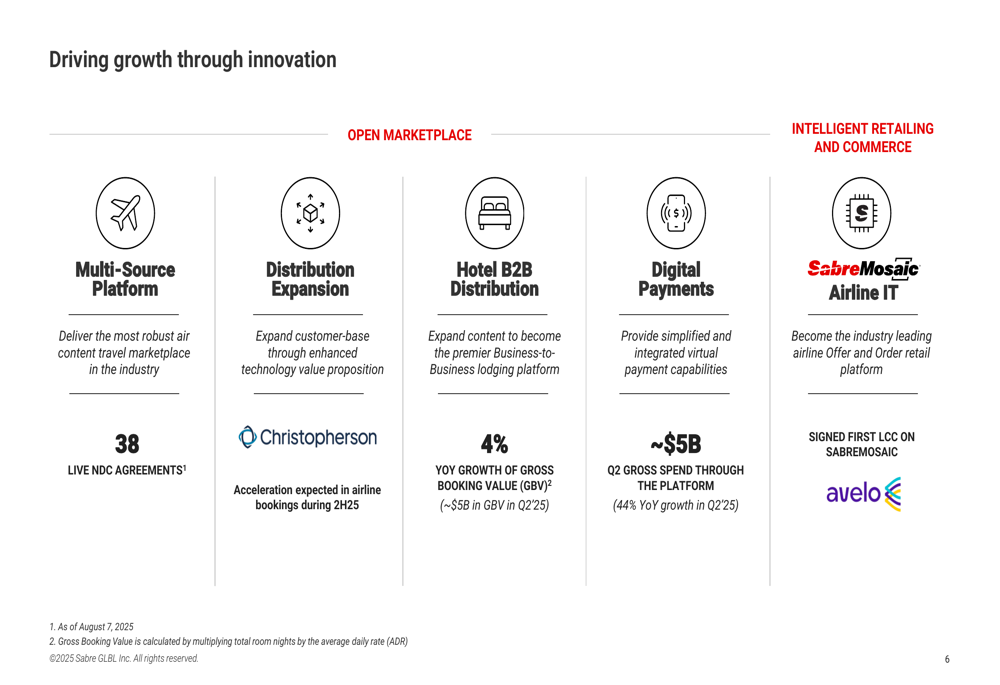

Despite the disappointing quarterly results, Sabre highlighted several growth initiatives that it believes will drive future performance. The company is expanding its distribution capabilities, with 38 live NDC (New Distribution Capability) integrations, positioning it as a leader in this area.

The company’s strategic growth priorities include:

Digital Payments has emerged as a bright spot, with gross spend up 44% year-over-year in Q2 to approximately $5 billion. Hotel B2B Distribution also showed promise with 4% year-over-year growth in Gross Booking (NASDAQ:BKNG) Value, reaching approximately $5 billion in Q2.

Sabre also announced new customer wins, including Christopherson choosing Sabre as its primary distribution technology provider, and SabreMosaic Airline IT agreements with Aeromexico, Alaska Airlines, Avelo, and GOL Linhas Aereas.

Market Reaction

The market responded severely to Sabre’s disappointing results and lowered guidance, with the stock plunging 30.83% to $2.08 in regular trading. In pre-market activity, shares had already fallen 26.34% to $2.21, indicating investors’ immediate negative reaction to the presentation.

This decline continues a challenging period for Sabre’s stock, which has traded between $1.93 and $4.63 over the past 52 weeks. The Q2 results follow a similarly disappointing Q1, where the company reported flat revenue of $777 million and missed earnings expectations.

The substantial guidance reduction suggests that the recovery in travel technology spending is occurring more slowly than Sabre had anticipated, despite the broader travel industry’s continued post-pandemic normalization. The company now faces significant challenges in regaining investor confidence while executing on its growth initiatives and continuing its deleveraging efforts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.