Intel stock spikes after report of possible US government stake

Introduction & Market Context

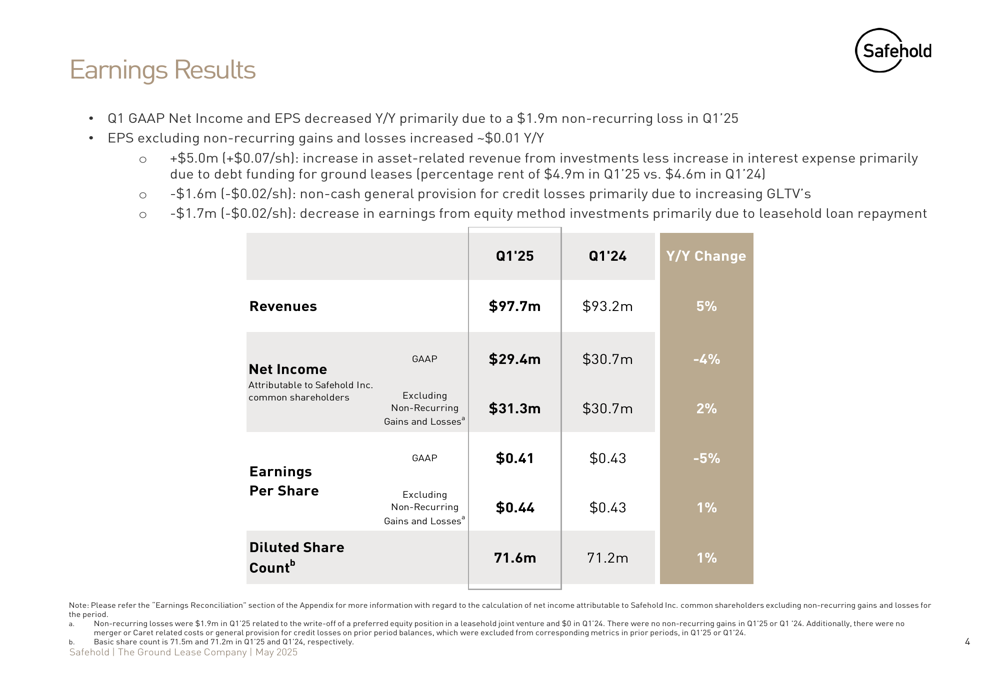

Safehold Inc. (NYSE:SAFE), the ground lease-focused real estate investment trust, reported its first quarter 2025 results, showing modest revenue growth amid its continued strategic shift toward multifamily properties. The company’s presentation, released on May 7, 2025, highlighted a 5% year-over-year increase in revenues to $97.7 million, while GAAP net income declined 4% to $29.4 million.

Trading at $15.33 in after-hours trading, Safehold shares have experienced significant pressure over the past year, currently sitting near their 52-week low of $13.68, and well below their 52-week high of $28.80. This performance comes as the company continues to navigate a challenging commercial real estate environment.

Quarterly Performance Highlights

Safehold’s Q1 2025 financial results showed mixed performance. While revenues increased by 5% year-over-year to $97.7 million, GAAP net income decreased by 4% to $29.4 million, resulting in earnings per share of $0.41, down 5% from $0.43 in Q1 2024.

As shown in the following detailed earnings breakdown, the company attributed the earnings decline primarily to a $1.9 million non-recurring loss in Q1 2025. Excluding this loss, EPS would have increased by approximately 1% year-over-year to $0.44.

The company’s earnings were positively impacted by a $5.0 million increase in asset-related revenue from investments (net of interest expense), contributing approximately $0.07 per share. However, this was partially offset by a $1.6 million non-cash general provision for credit losses due to increasing ground lease-to-value ratios (GLTV) and a $1.7 million decrease in earnings from equity method investments, primarily due to leasehold loan repayment.

Portfolio Growth and Strategic Focus

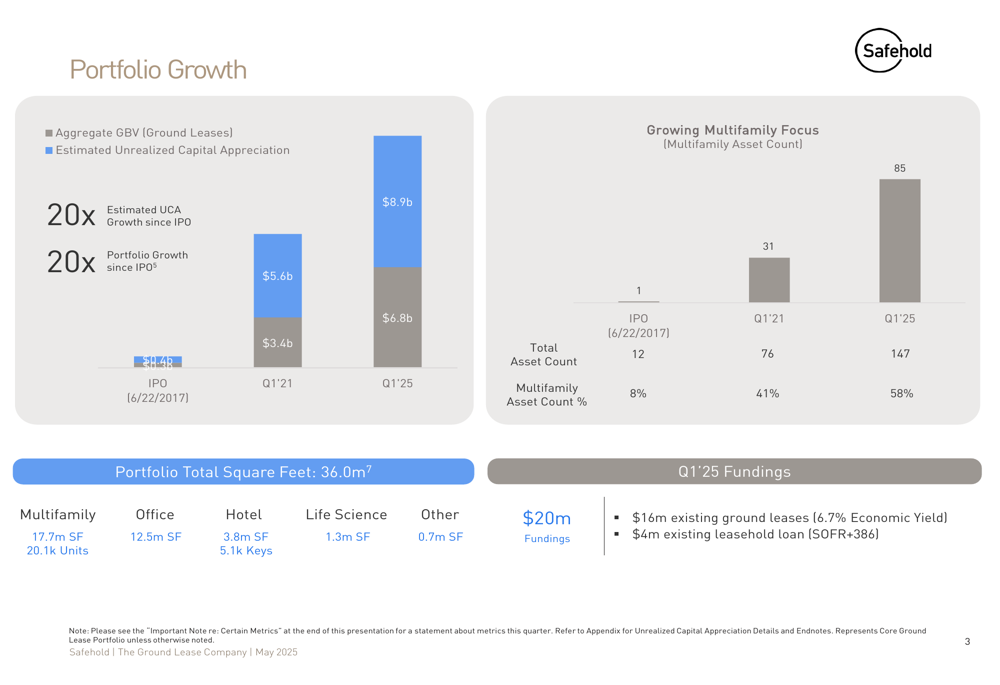

Safehold continues to execute its long-term growth strategy, with significant expansion since its IPO in 2017. The company’s portfolio has grown 20-fold since its public debut, with a particular emphasis on multifamily assets, which now represent 58% of its total asset count, up from just 8% at IPO.

The following chart illustrates this strategic shift toward multifamily properties, which has accelerated in recent years:

In Q1 2025, Safehold reported non-binding letters of intent for 11 ground leases valued at approximately $273 million and 4 leasehold loans worth approximately $113 million. These potential investments span 8 markets and involve 11 different sponsors, with an average ground lease-to-value ratio of 34% and rent coverage of 2.6x.

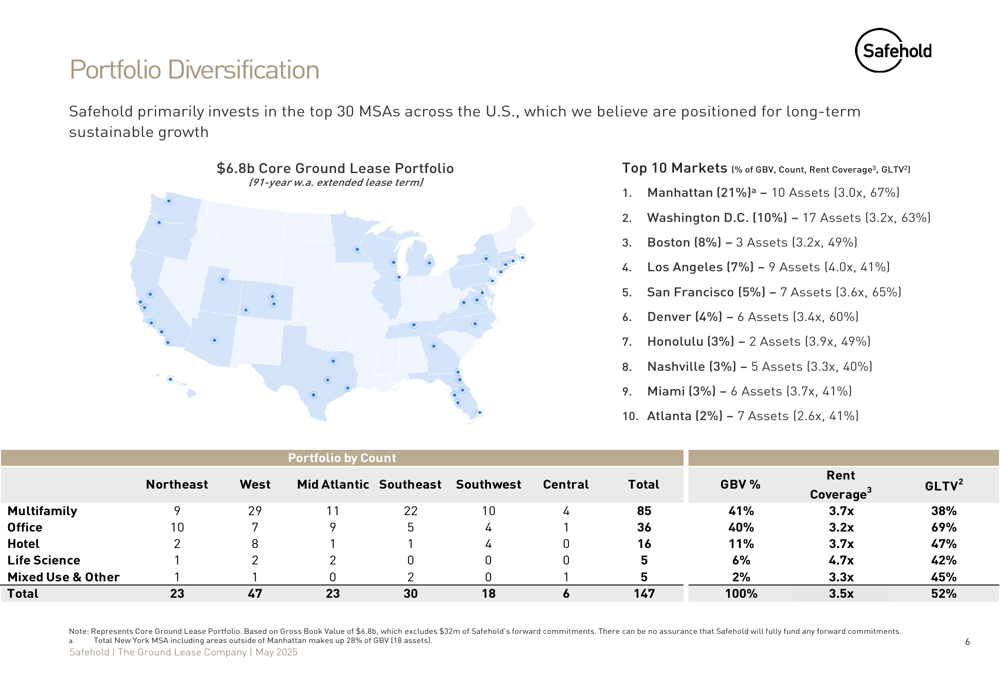

The company’s portfolio diversification across property types and geographic markets provides stability and risk mitigation. As shown in the following breakdown, Safehold maintains a balanced presence across key U.S. markets, with Manhattan representing its largest concentration at 21% of gross book value:

Capital Structure and Liquidity

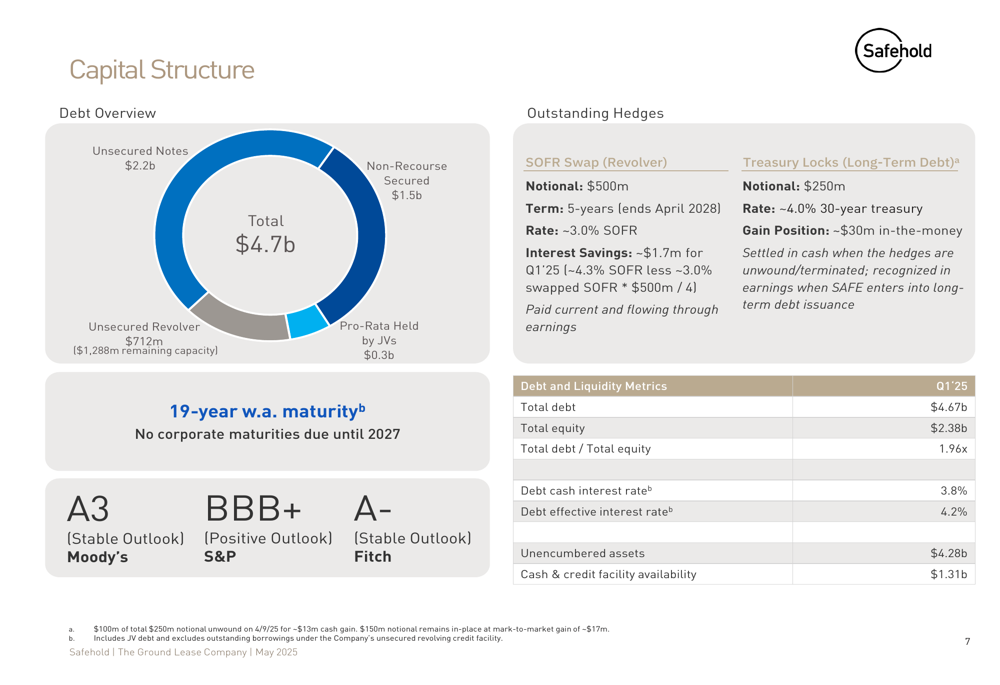

Safehold maintains a strong capital position with $1.3 billion in cash and credit facility availability. The company’s debt structure is well-managed with a 19-year weighted average maturity and no corporate maturities due until 2027.

The following chart illustrates Safehold’s capital structure, highlighting its balanced approach to financing:

The company’s total debt stands at $4.67 billion against total equity of $2.38 billion, resulting in a debt-to-equity ratio of 1.96x. Safehold’s debt carries a cash interest rate of 3.8% and an effective interest rate of 4.2%. The company maintains strong investment-grade ratings, including A3 (Stable) from Moody’s, BBB+ (Positive) from S&P, and A- (Stable) from Fitch.

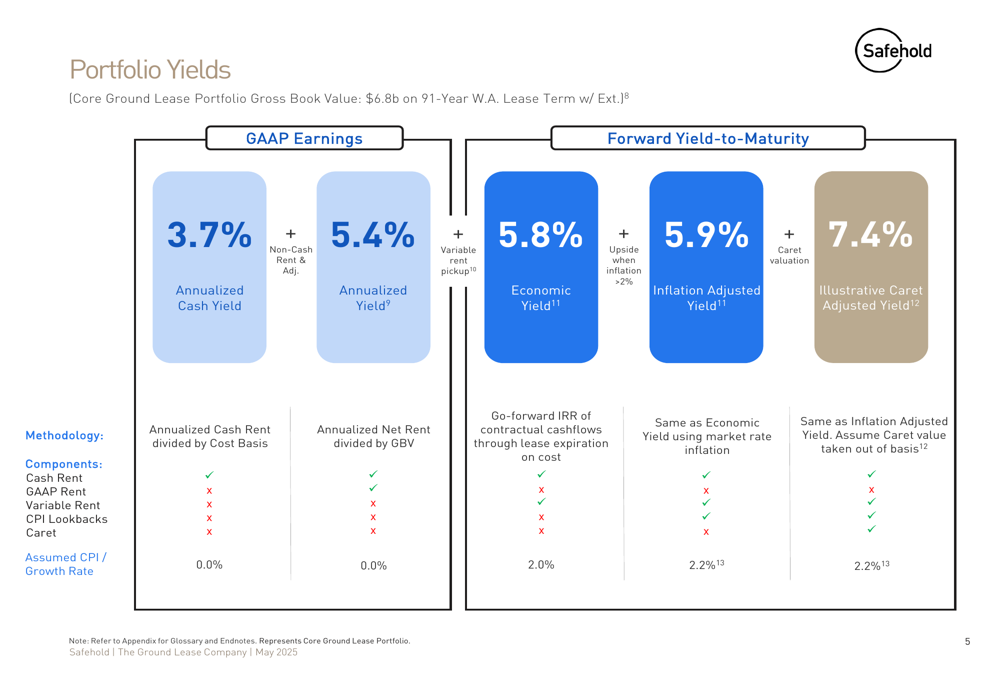

Safehold’s portfolio yields demonstrate the company’s ability to generate consistent returns. The core ground lease portfolio, valued at $6.8 billion with a 91-year weighted average lease term, generates an annualized yield of 5.4% with potential upside from variable rent. The company’s economic yield stands at 5.8%, with an illustrative Caret-adjusted yield of 7.4% when accounting for potential value appreciation.

Forward-Looking Statements

Looking ahead, Safehold appears well-positioned to continue its strategic focus on high-quality ground leases, particularly in the multifamily sector. The company’s strong liquidity position of $1.3 billion provides significant flexibility to capitalize on new investment opportunities as they arise.

Safehold also maintains additional capital through its joint venture with a leading sovereign wealth fund, with $400 million remaining ($220 million from SAFE and $180 million from its partner). This provides additional capacity for investment growth without immediately tapping into debt markets.

The company’s Q1 2025 presentation aligns with statements made in previous earnings calls about focusing on high-quality ground leases in top markets for long-term benefits. As noted in their Q3 2024 earnings call, Safehold has been strategically shifting toward owning properties outright rather than through joint ventures, particularly for smaller multifamily ground leases.

While Safehold faces challenges from market uncertainties and fluctuating interest rates, its diversified portfolio, strong liquidity, and investment-grade ratings position the company to navigate the commercial real estate environment effectively. The continued focus on multifamily assets, which now represent 58% of the portfolio by count and 41% by gross book value, suggests a strategic emphasis on what the company views as a more stable property sector in the current market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.