BOJ keeps interest rates flat, but flags rate hikes on rising inflation, GDP

Introduction & Market Context

Saia Inc. (NASDAQ:SAIA), the sixth-largest Less-Than-Truckload (LTL) carrier in the United States, recently presented its Q1 2025 investor results, revealing a company at a crossroads. Despite achieving record first-quarter revenue of $787.6 million, Saia’s earnings fell significantly short of analyst expectations, triggering a 26.85% stock price drop following the announcement.

The company operates in the domestic LTL market, estimated at $53 billion annually, where the top 10 carriers control 76% of market share. Saia’s position in this competitive landscape is highlighted in their industry overview:

Quarterly Performance Highlights

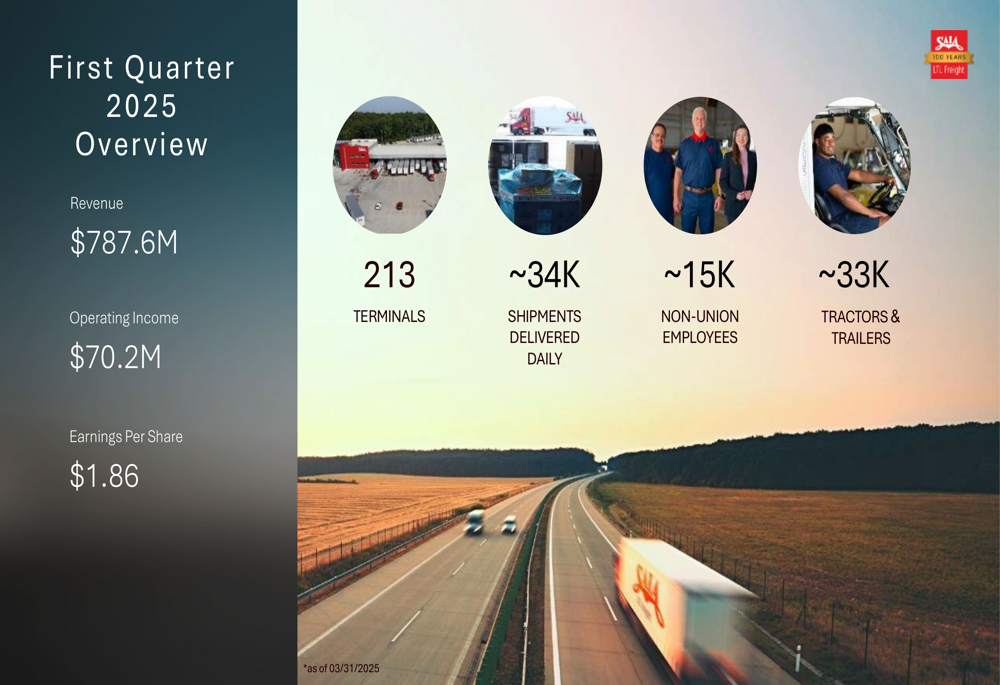

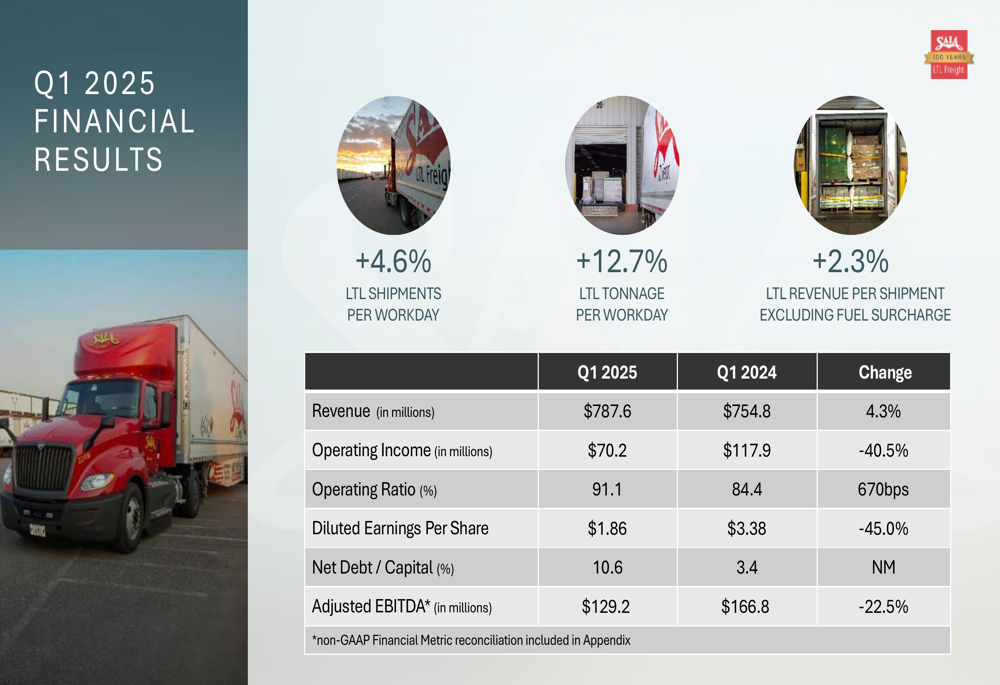

Saia’s Q1 2025 financial results painted a mixed picture. While revenue increased 4.3% year-over-year to $787.6 million, operating income plummeted to $70.2 million from $117.9 million in Q1 2024. Earnings per share fell to $1.86, well below the analyst forecast of $2.77, representing a 32.9% miss.

The company’s key operational metrics for the quarter included handling approximately 34,000 shipments daily across 213 terminals with a workforce of about 15,000 non-union employees:

The detailed financial comparison between Q1 2025 and Q1 2024 reveals significant challenges in maintaining profitability despite revenue growth. Most concerning was the deterioration in operating ratio (a measure of operational efficiency where lower is better) from 84.4% to 91.1%, representing a 670 basis point decline:

On a positive note, Saia reported improvements in service quality metrics, with the claims ratio dropping to 0.50% in Q1 2025 from around 0.60% in previous years:

Strategic Initiatives and Network Expansion

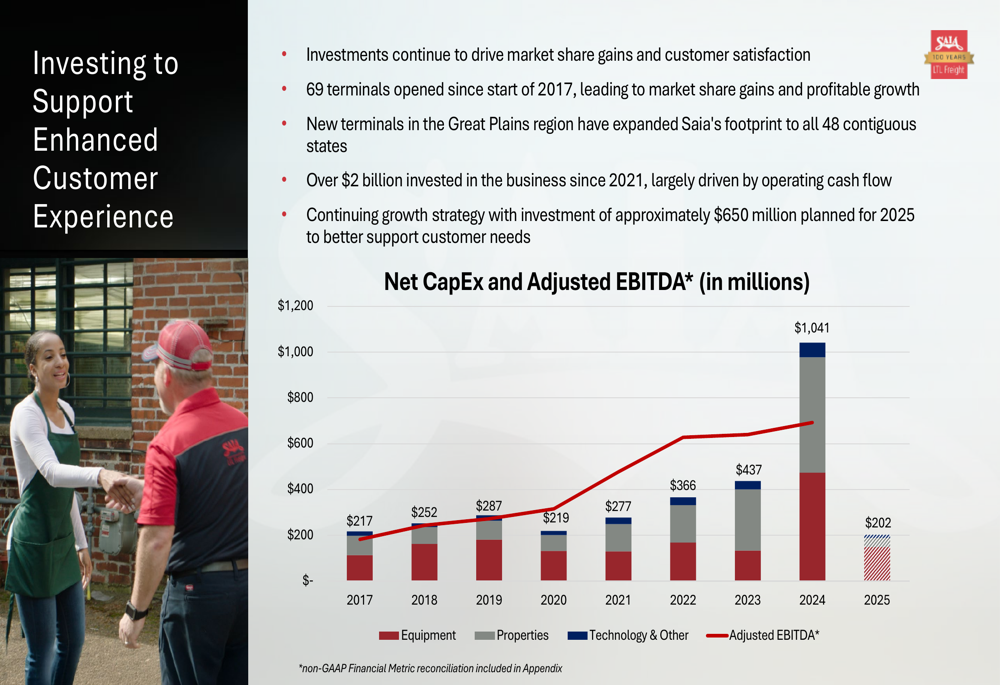

Despite the earnings disappointment, Saia continues to execute its long-term growth strategy focused on network expansion. In 2024, the company deployed over $1 billion in capital, opened 21 new terminals, and relocated 9 others, achieving direct presence in all 48 contiguous states:

This expansion strategy has been ongoing since 2017, with the company opening 69 terminals and investing over $2 billion in the business since 2021. Saia plans to invest approximately $650 million in 2025 to further enhance customer support and network capabilities:

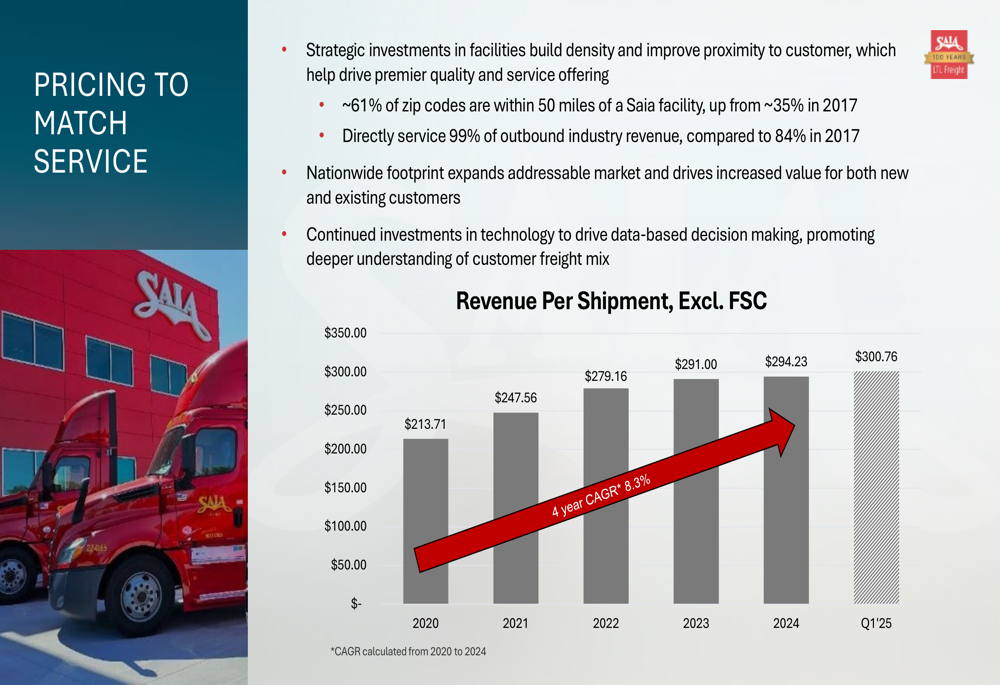

The company’s strategic investments have yielded some positive results in terms of market coverage. Approximately 61% of zip codes are now within 50 miles of a Saia facility, compared to roughly 35% in 2017. Additionally, Saia directly services approximately 99% of outbound industry revenue, up from approximately 84% in 2017.

Financial Position and Challenges

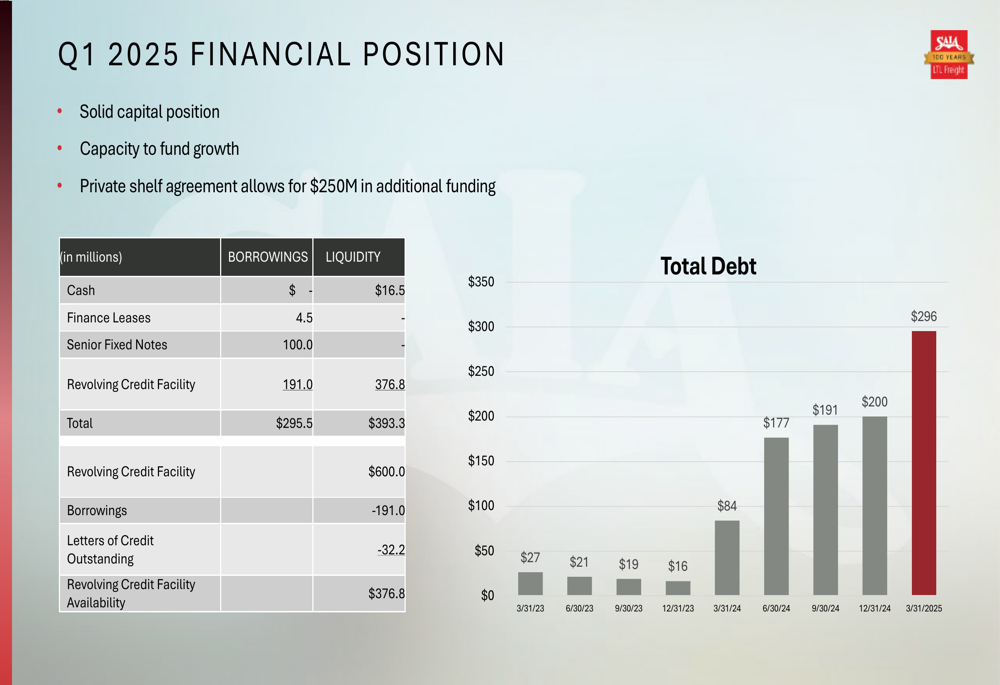

While Saia maintains a solid capital position with the capacity to fund growth, its financial metrics reflect increasing pressure. The company’s debt has been rising, with total debt growing from $27 million in March 2023 to $296 million in March 2025:

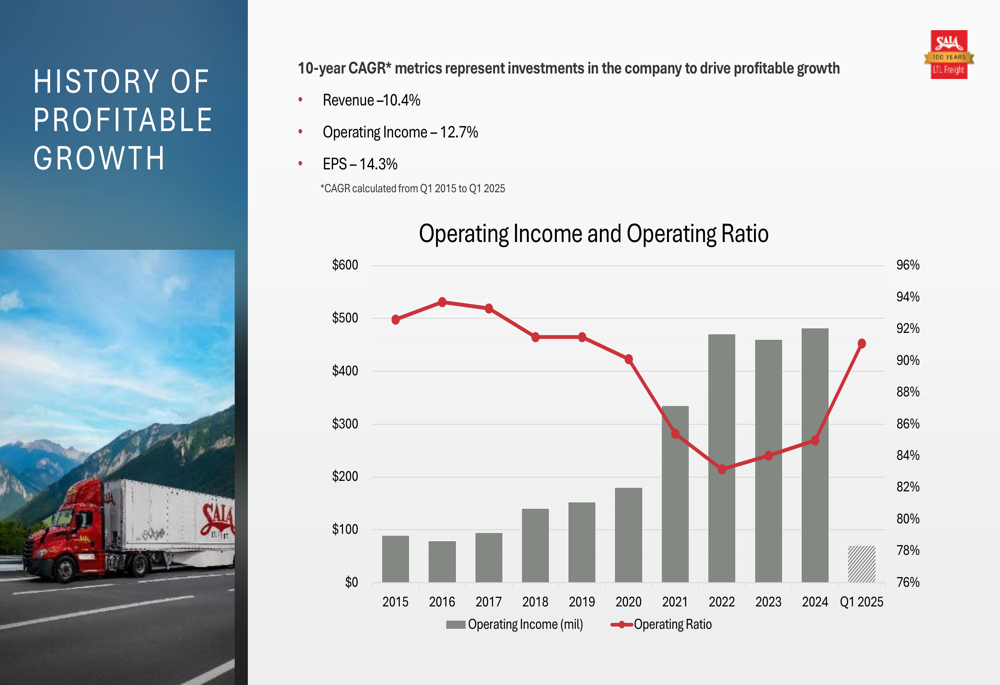

Despite these challenges, Saia has demonstrated a history of profitable growth over the past decade. The 10-year Compound Annual Growth Rate (CAGR) shows revenue growth of 10.4%, operating income growth of 12.7%, and earnings per share growth of 14.3%:

However, the recent operating ratio trend suggests mounting cost pressures that are eroding profitability. The company’s pricing strategy aims to address this by matching pricing to service quality, with revenue per shipment excluding fuel surcharge increasing from approximately $213 in 2020 to around $300 in Q1 2025:

Forward-Looking Statements

Saia’s management remains committed to its long-term growth strategy despite the near-term challenges. CEO Fritz Holzgren emphasized during the earnings call, "We remain very, very committed to the long-term value proposition that Saia can provide to our customers and to our shareholders."

The company’s investment summary highlights its unique position as a 100+ year-old company with above-market growth potential. Management believes Saia is well-positioned for volume growth and market share gains through its expanded network, with significant revenue growth opportunities including ongoing pricing improvements, market penetration in legacy geography, and leveraging partnerships in Canada and Mexico.

Saia also emphasizes its core values as driving its customer-first approach, actively recruiting top talent, engaging in continuous improvement, and investing in the communities where they operate:

However, investors appear concerned about rising operational costs, including salaries and transportation expenses, uncertainty in the macroeconomic environment, increased competition, and potential impacts of weather disruptions on operations. The significant stock price decline following the earnings announcement reflects these concerns and suggests that the market may require more evidence that Saia’s long-term strategy will translate to improved near-term financial performance.

As Saia navigates these challenges, the company’s ability to balance network expansion with operational efficiency will be crucial for regaining investor confidence and returning to its historical trajectory of profitable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.