Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Steel Authority of India Limited (BSE:NSE:SAIL) presented its Q4 and full-year FY’25 results on May 29, 2025, showing quarterly improvements despite facing global steel market headwinds. The company’s stock closed at Rs. 128.96, up 0.94% on the day of the presentation.

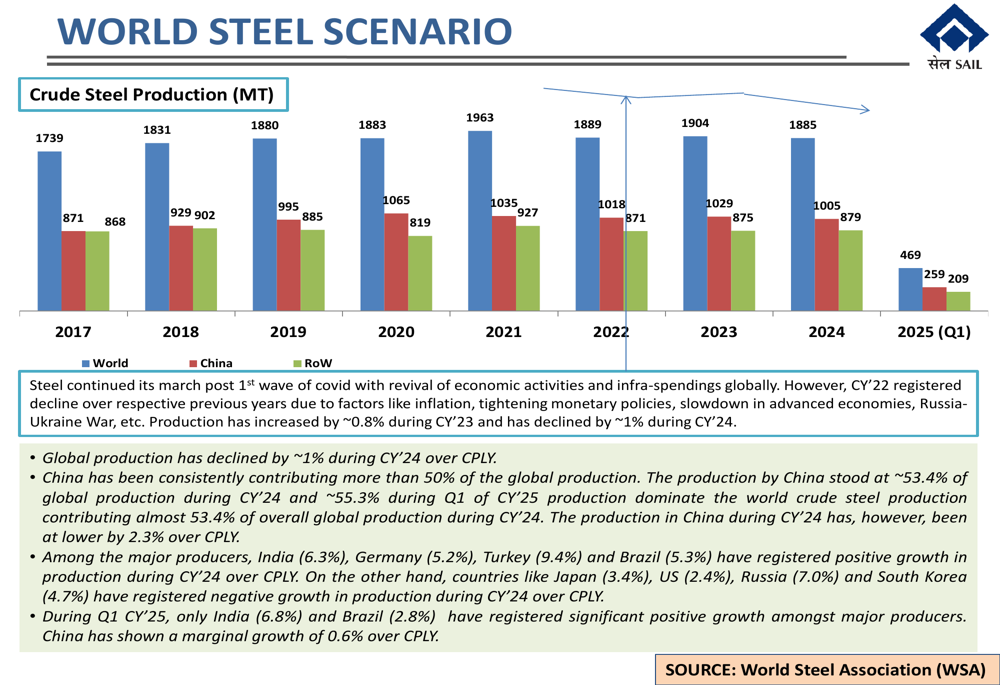

The results come amid a challenging global steel scenario, with worldwide steel demand expected to decrease by 0.9% in 2024 before rebounding with a 1.2% increase in 2025, according to the World Steel Association. While China’s demand is projected to decline by 3% in 2024 and 1% in 2025, India remains a bright spot with expected demand growth of 8.5% in CY2025.

As shown in the following chart of global steel production, China continues to dominate with over 50% of worldwide output, though its production declined by 2.3% in CY’24 compared to the previous year:

Quarterly Performance Highlights

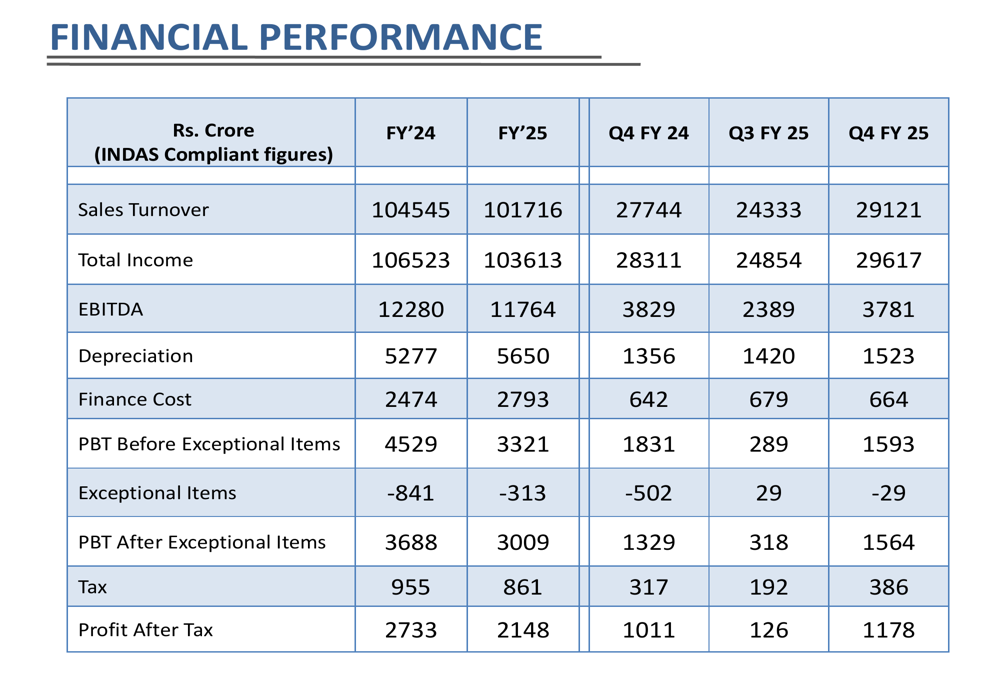

SAIL reported a strong fourth quarter with sales volume of 5.3 million tonnes, up from 4.6 million tonnes in Q4 FY’24. This volume growth helped drive quarterly sales turnover to Rs. 29,121 crore, an increase from Rs. 27,744 crore in the same quarter last year.

The company’s Q4 FY’25 EBITDA remained relatively stable at Rs. 3,781 crore compared to Rs. 3,829 crore in Q4 FY’24, while profit after tax (PAT) improved to Rs. 1,178 crore from Rs. 1,011 crore in the year-ago quarter.

The detailed financial performance for the quarter and full year is illustrated in the following table:

The quarterly improvement was particularly notable compared to Q3 FY’25, when SAIL reported an EBITDA of Rs. 2,389 crore and PAT of just Rs. 126 crore. This sequential improvement was driven by higher sales volumes, improved raw material usage, and favorable price adjustments.

Detailed Financial Analysis

For the full fiscal year 2025, SAIL reported a turnover of Rs. 101,716 crore, down from Rs. 104,545 crore in FY’24. Annual EBITDA declined slightly to Rs. 11,764 crore from Rs. 12,280 crore, while PAT decreased to Rs. 2,148 crore from Rs. 2,733 crore in the previous year.

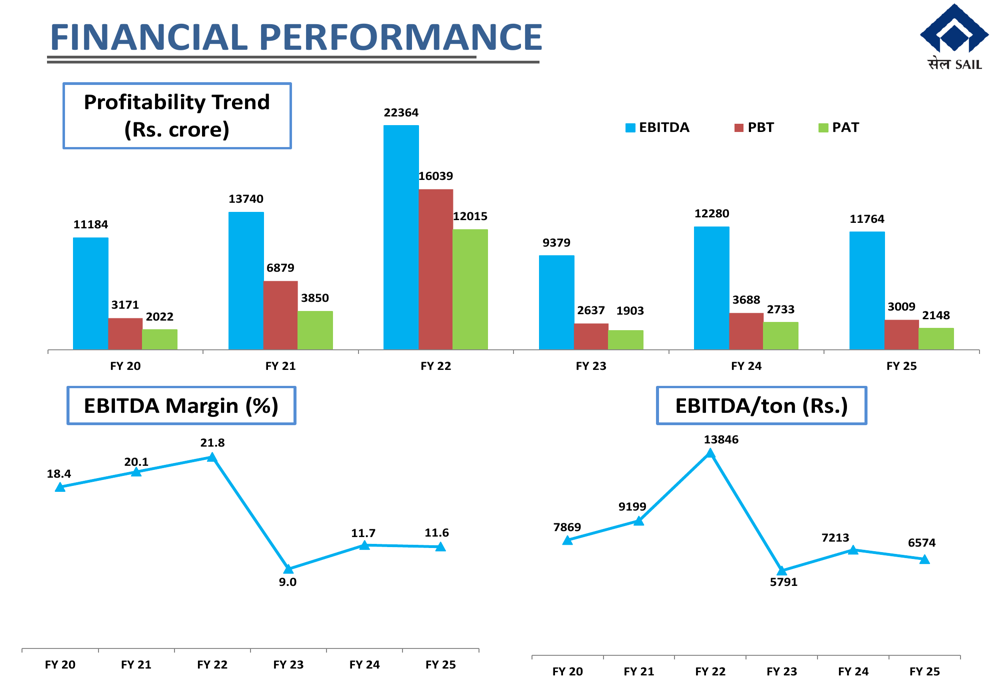

The company’s EBITDA margin remained relatively stable at 11.6% in FY’25 compared to 11.7% in FY’24, though significantly below the peak of 21.8% achieved in FY’22 during exceptional market conditions. EBITDA per tonne stood at Rs. 6,574 in FY’25, down from Rs. 7,213 in FY’24.

The following chart illustrates SAIL’s profitability trends over the past six fiscal years:

SAIL maintained a stable financial position with a debt-equity ratio of 0.66 as of March 2025, unchanged from March 2024. The company’s net worth increased to Rs. 55,656 crore as of March 2025, up from Rs. 54,131 crore a year earlier.

Operational Improvements

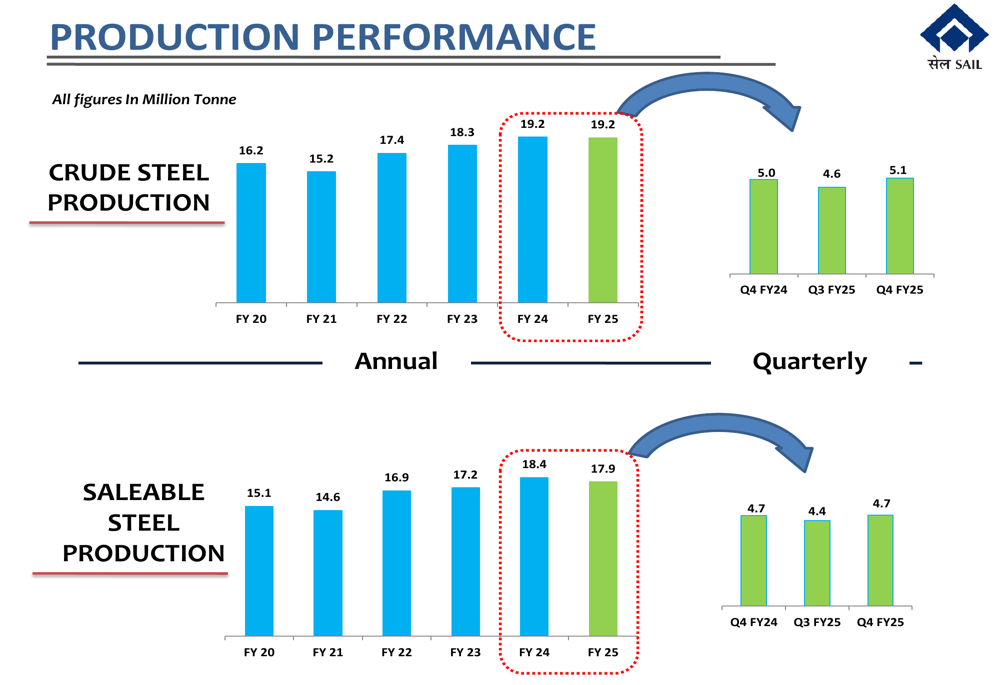

SAIL’s crude steel production remained flat at 19.2 million tonnes in FY’25 compared to FY’24, while saleable steel production decreased slightly to 17.9 million tonnes from 18.4 million tonnes. However, total sales volume increased to 17.9 million tonnes in FY’25 from 17.0 million tonnes in FY’24.

The company’s production performance is illustrated in the following chart:

SAIL continued to improve its operational efficiency metrics during FY’25. The coke rate improved to 421 kg/thm from 440 kg/thm in FY’24, while the coal dust injection (CDI) rate increased to 113 kg/thm from 106 kg/thm. Specific energy consumption decreased to 6.26 GCal/tcs from 6.30 GCal/tcs, and blast furnace productivity improved significantly to 2.02 T/m3/day from 1.88 T/m3/day.

The company’s product mix comprised 50.6% flat products, 35.6% long products, and 13.7% semi-finished products. Value-added steel accounted for 55.3% of total saleable steel production, highlighting SAIL’s focus on higher-margin products.

Sustainability Initiatives

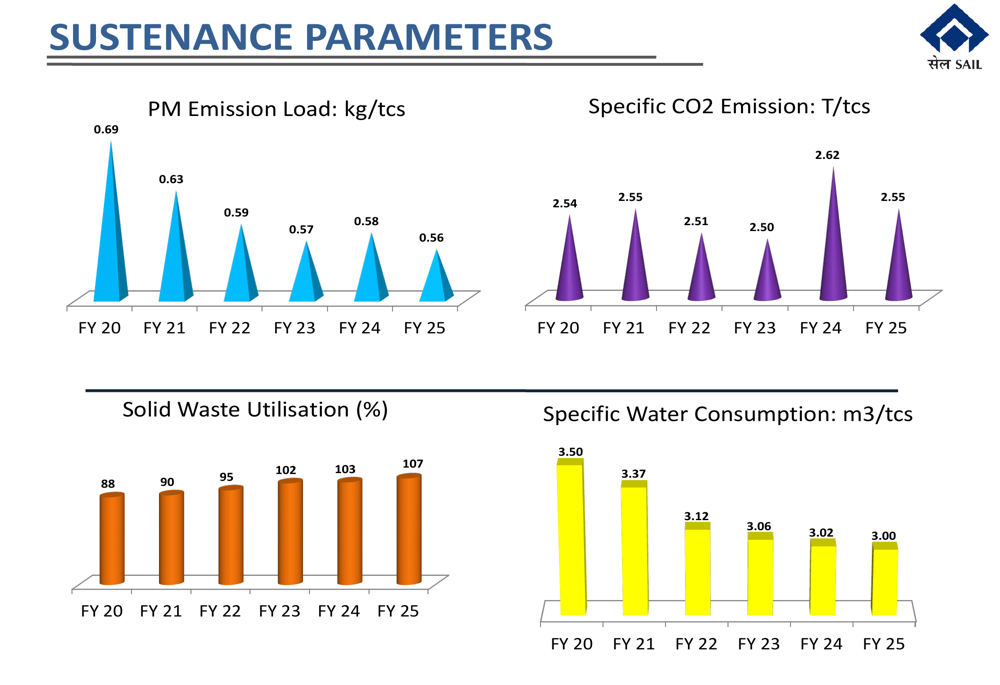

SAIL demonstrated continued improvement in its sustainability parameters during FY’25. Particulate matter emission load decreased to 0.56 kg/tcs from 0.58 kg/tcs in FY’24, while specific CO2 emissions improved to 2.55 T/tcs from 2.62 T/tcs. Solid waste utilization increased to 107% from 103%, and specific water consumption reduced to 3.00 m3/tcs from 3.02 m3/tcs.

The following chart illustrates SAIL’s progress on key sustainability metrics:

The company also reported significant improvements in labor productivity, which increased to 615 tcs/man/year in FY’25 from 579 tcs/man/year in FY’24. This improvement was partly driven by a reduction in manpower, which decreased by 2,830 during the year to 53,159 as of April 1, 2024.

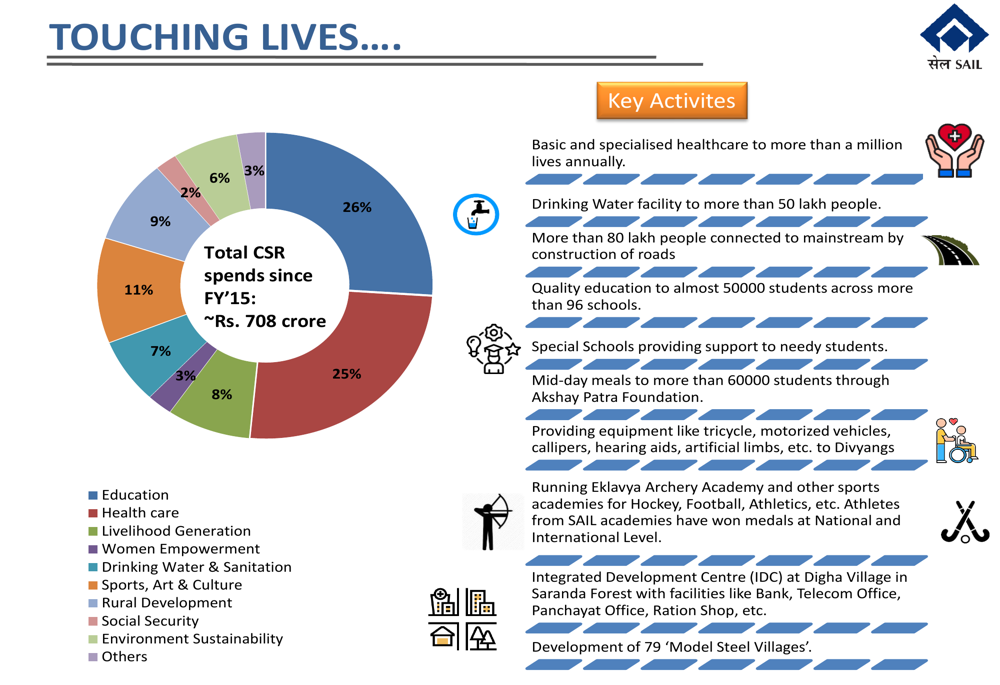

SAIL has invested approximately Rs. 708 crore in CSR activities since FY’15, with 26% allocated to education, 11% to healthcare, and 9% to livelihood generation programs, as shown in the following breakdown:

Forward-Looking Statements

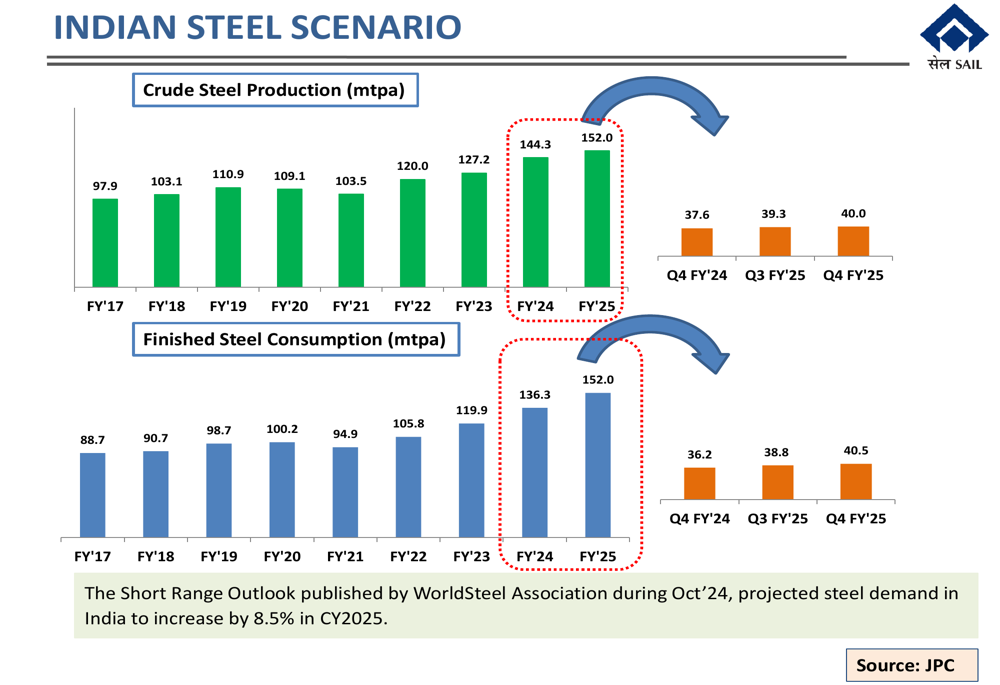

Looking ahead, SAIL is positioned to benefit from India’s robust steel demand growth, which is expected to outpace global trends. The Indian economy is projected to grow at 6.5% in FY’25, providing a supportive environment for domestic steel consumption.

As illustrated in the following chart, India’s crude steel production and finished steel consumption have shown consistent growth over the years, with FY’25 consumption reaching 152 million tonnes:

While international steel prices have shown a declining trend, SAIL’s focus on operational efficiency, sustainability, and value-added products should help the company navigate market challenges. The company’s improved quarterly performance in Q4 FY’25 provides a positive momentum heading into the new fiscal year.

The management did not provide specific guidance for FY’26, but the ongoing improvements in operational parameters and India’s favorable demand outlook suggest potential for growth in the coming year, despite global market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.