InvestingPro’s Fair Value model captures 63% gain in Steelcase ahead of acquisition

Salesforce Inc. (NYSE:CRM) presented its first quarter fiscal year 2026 results on May 28, 2025, highlighting strong performance that enabled the company to raise its full-year guidance. The cloud-based software giant reported 8% year-over-year revenue growth while emphasizing its strategic focus on artificial intelligence and the pending acquisition of Informatica.

Quarterly Performance Highlights

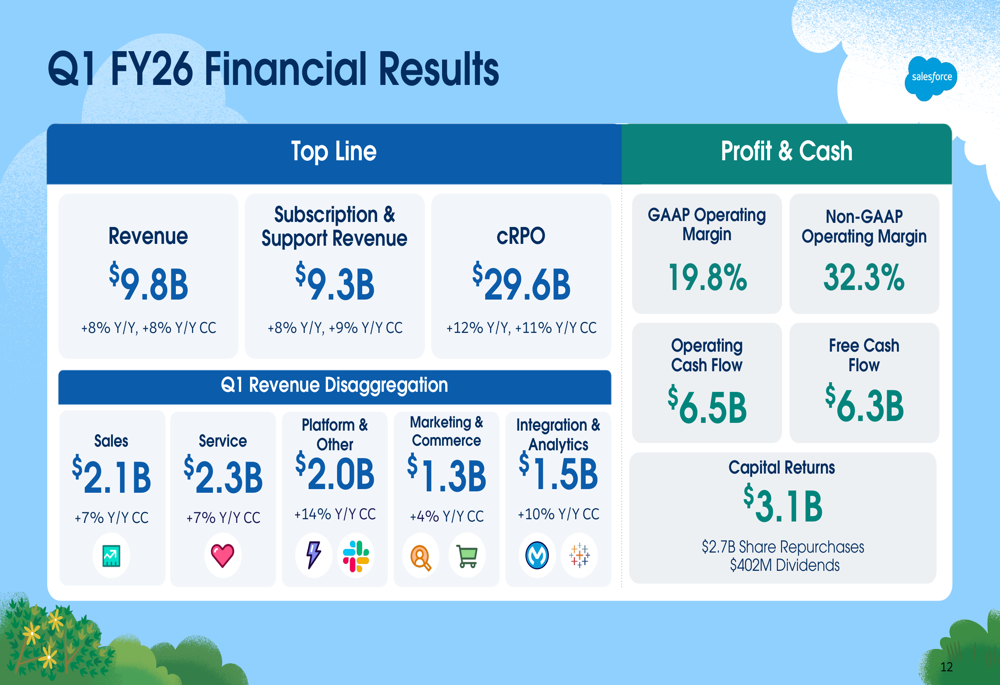

Salesforce reported Q1 FY26 revenue of $9.8 billion, representing 8% growth year-over-year both on a reported and constant currency basis. Subscription and support revenue, which forms the core of the company’s business model, grew to $9.3 billion, up 8% year-over-year (9% in constant currency).

The company’s current remaining performance obligation (CRPO), a key indicator of future revenue, reached $29.6 billion, growing 12% year-over-year (11% in constant currency). This metric suggests continued momentum in Salesforce’s business pipeline.

As shown in the following comprehensive financial breakdown, Salesforce achieved strong performance across all its business segments:

Particularly noteworthy was the performance of the Platform & Other segment, which grew 14% year-over-year in constant currency, reflecting the company’s successful push into AI and data solutions. The Integration & Analytics segment also showed solid growth at 10%.

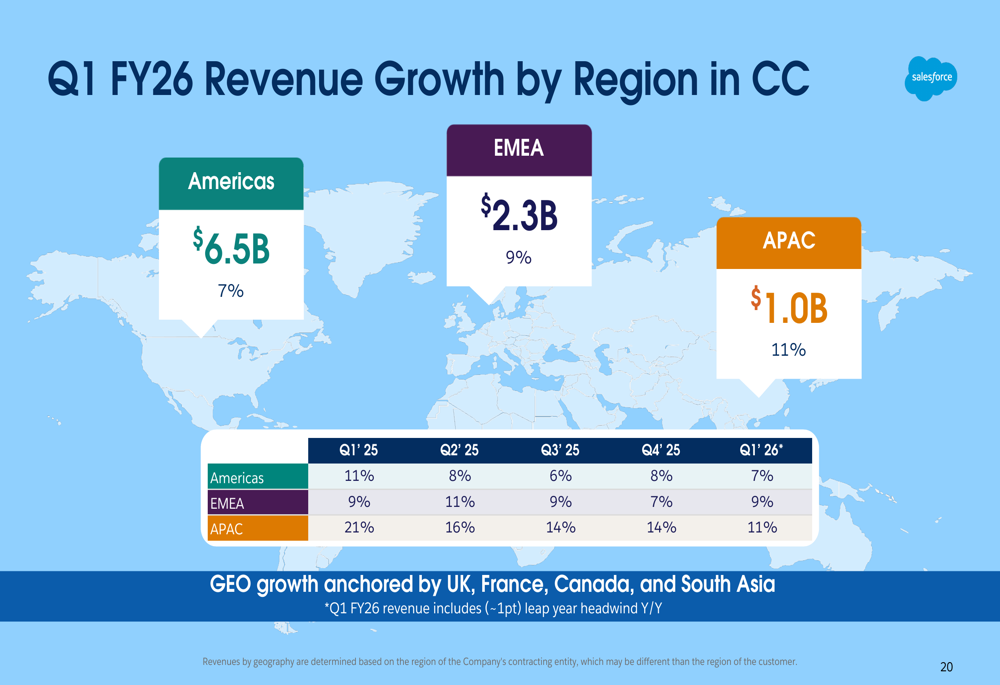

Geographically, Salesforce saw growth across all regions, with APAC leading at 11% year-over-year, followed by EMEA at 9% and Americas at 7%, as illustrated in this regional breakdown:

Strategic Initiatives

A central theme of Salesforce’s presentation was the company’s focus on combining human capabilities with AI agents to drive customer success. The company highlighted its "Agentforce" strategy, which builds on its existing Customer 360 platform.

The following slide illustrates Salesforce’s vision for integrating AI throughout its ecosystem:

Salesforce reported that its Data Cloud and AI annual recurring revenue (ARR) exceeded $1 billion, growing more than 120% year-over-year, underscoring the company’s successful AI monetization strategy.

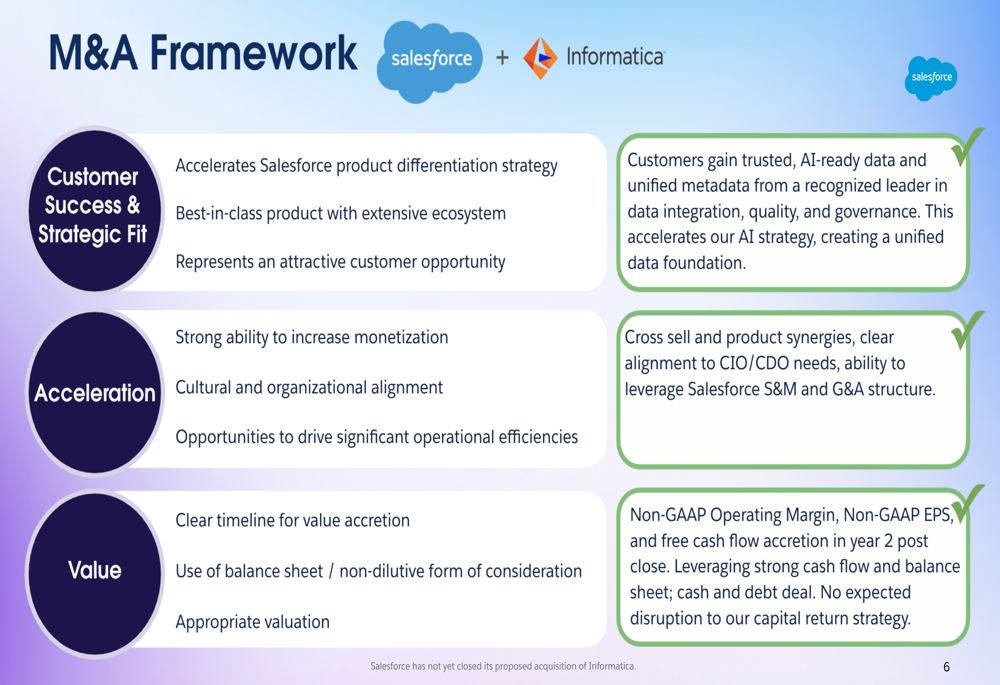

A significant strategic development is Salesforce’s proposed acquisition of Informatica, which the company positions as complementary to its data strategy. The acquisition aims to enhance Salesforce’s ability to help customers understand, govern, and catalog their data—critical capabilities for effective AI implementation.

The strategic rationale for the Informatica acquisition is outlined in this framework:

The company highlighted that the Informatica deal is expected to be accretive to non-GAAP operating margin, EPS, and free cash flow, though it noted that the acquisition has not yet closed.

Detailed Financial Analysis

Salesforce demonstrated strong profitability metrics in Q1 FY26, with a GAAP operating margin of 19.8% and a non-GAAP operating margin of 32.3%. The company generated $6.5 billion in operating cash flow and $6.3 billion in free cash flow during the quarter.

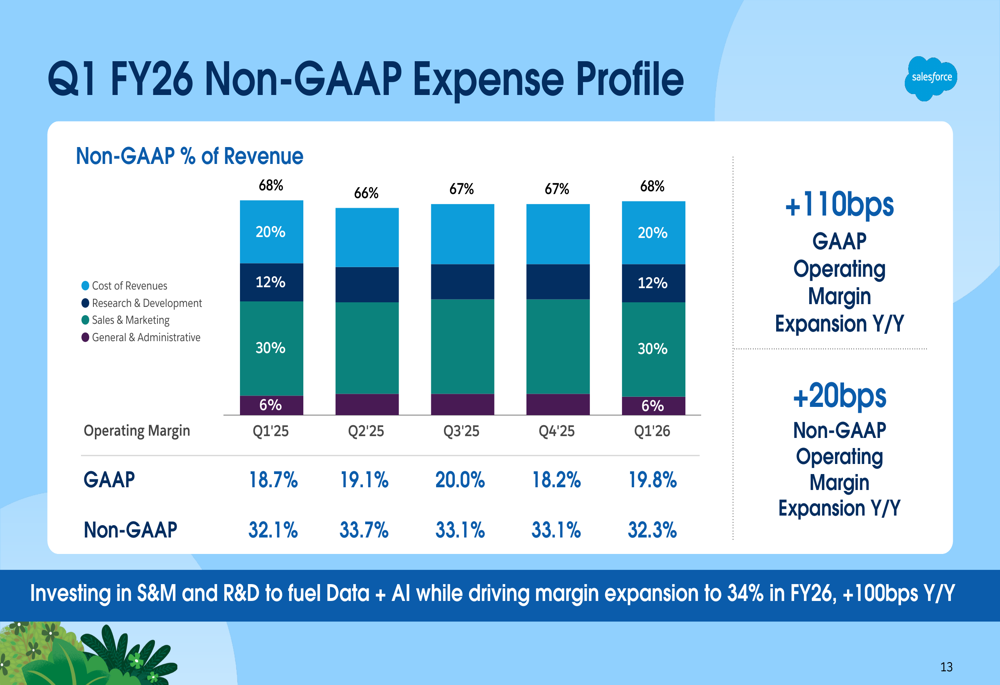

The company’s expense management strategy is reflected in its non-GAAP expense profile:

Salesforce emphasized its continued focus on balancing growth investments with margin expansion, targeting a non-GAAP operating margin of 34% for the full fiscal year 2026, which would represent a 100 basis point improvement year-over-year.

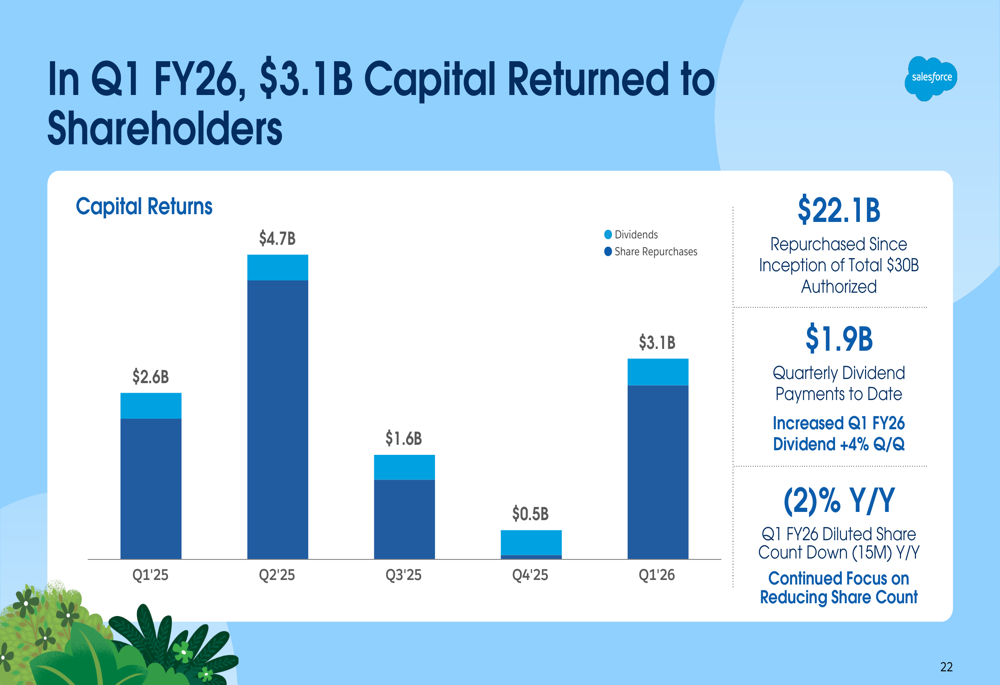

The company also highlighted its commitment to shareholder returns, with $3.1 billion returned to shareholders in Q1 FY26 through a combination of share repurchases ($2.7 billion) and dividends ($402 million). Since the inception of its buyback program, Salesforce has repurchased $22.1 billion of its $30 billion authorized total.

The following chart illustrates Salesforce’s capital return strategy:

Forward-Looking Statements

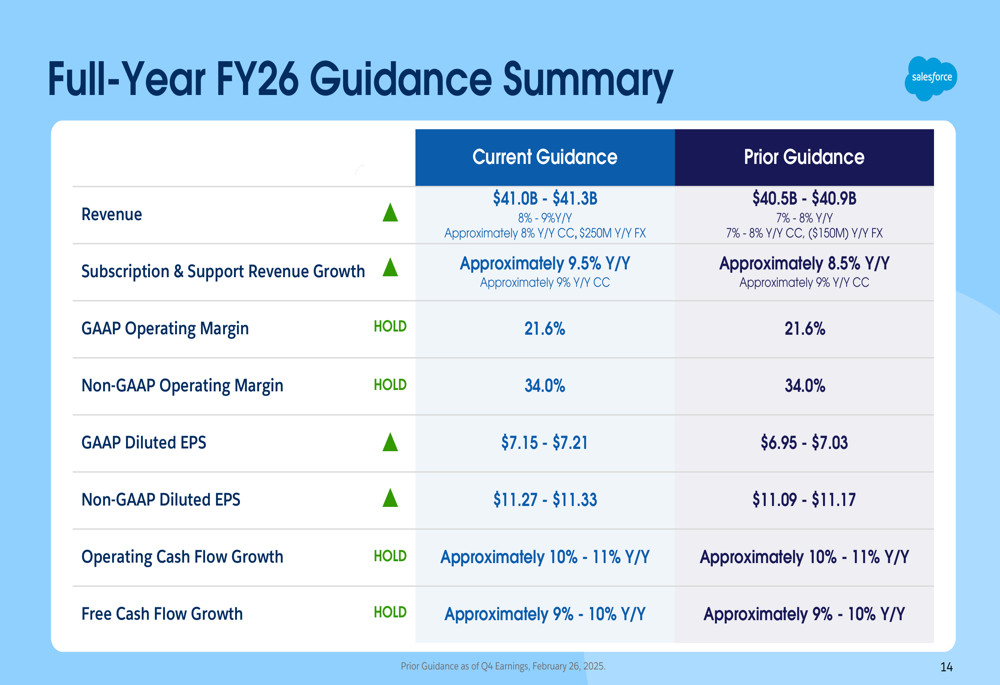

In a positive sign for investors, Salesforce raised its full-year FY26 guidance, now projecting revenue of $41.0 billion to $41.3 billion, up from its previous guidance of $40.5 billion to $40.9 billion. This represents approximately 8% year-over-year growth in constant currency.

The company maintained its non-GAAP operating margin guidance of 34% while raising its EPS projections. The updated guidance is detailed in this comparison:

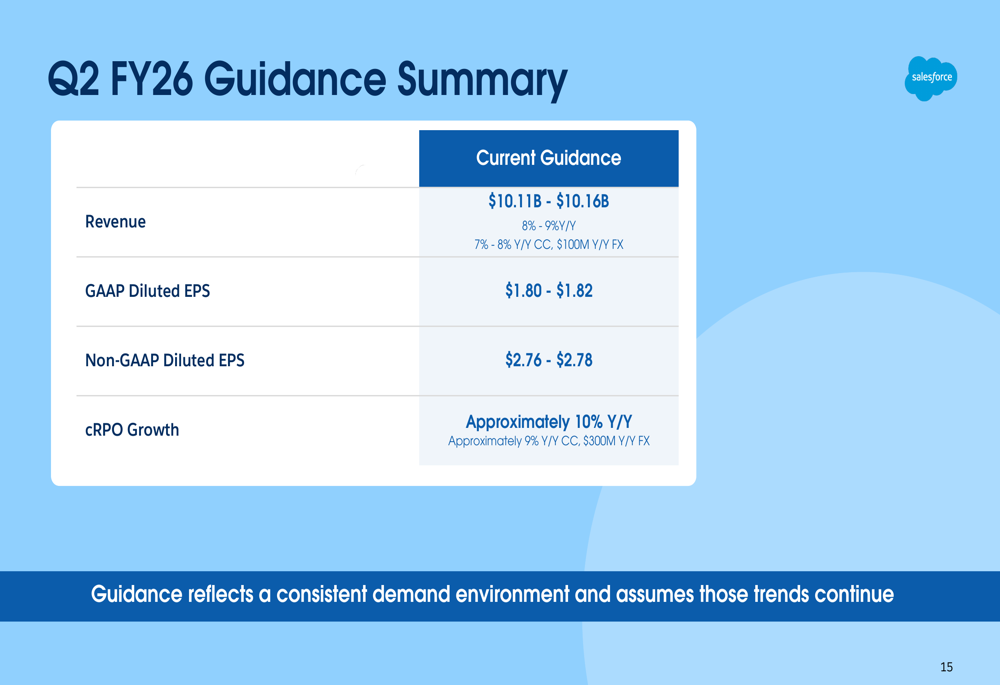

For the second quarter of fiscal year 2026, Salesforce expects revenue between $10.11 billion and $10.16 billion, representing 7-8% year-over-year growth in constant currency. The company projects Q2 non-GAAP diluted EPS of $2.76 to $2.78 and anticipates CRPO growth of approximately 10% year-over-year.

The guidance reflects what management described as a "consistent demand environment" and assumes those trends will continue. This outlook aligns with Salesforce’s previous earnings call from Q4 FY25, where CEO Marc Benioff emphasized the company’s leadership in digital labor and AI-powered solutions.

After the earnings presentation, Salesforce shares rose 1.44% in after-hours trading to $280, according to market data, suggesting a positive reception to the company’s results and raised guidance. The stock had closed the regular session at $277.19, down 0.42% for the day.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.