S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Salik Company PJSC (DFM:SALIK), Dubai’s exclusive toll gate operator, reported robust first-quarter 2025 results, showcasing significant growth across all key financial metrics. The company benefited from Dubai’s strong macroeconomic environment, which saw population growth of over 52,000 residents in Q1 2025 and a 3% year-over-year increase in international visitors to 3.82 million.

The toll operator, which has been in operation for over 18 years and holds exclusivity in Dubai until 2071, has successfully leveraged favorable market conditions including a 29% year-over-year increase in real estate transaction value and 33% growth in registered car rental companies.

Quarterly Performance Highlights

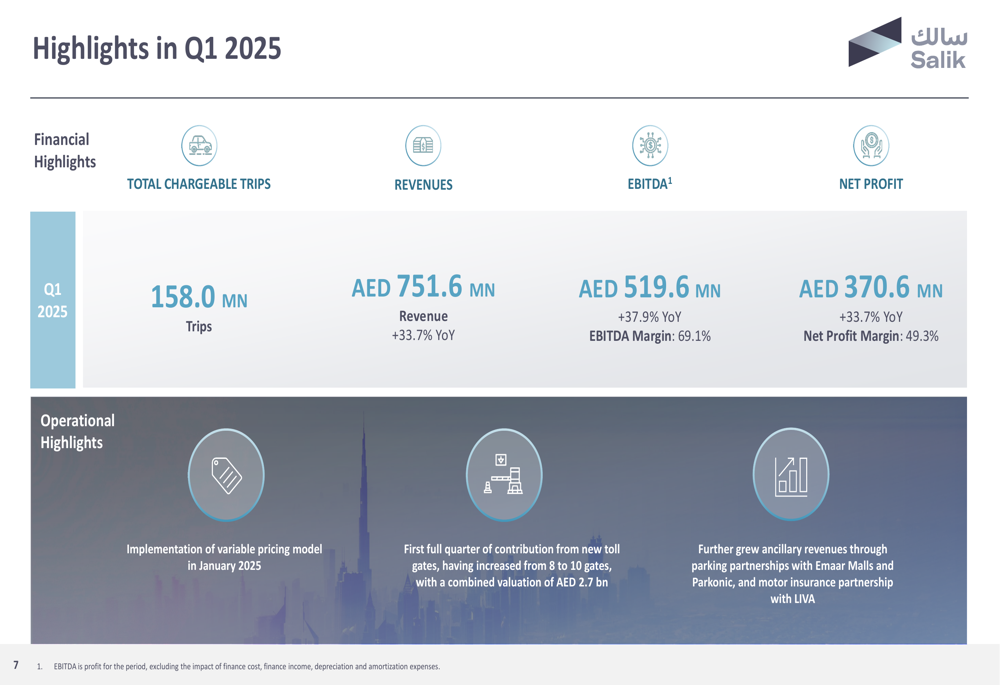

Salik reported impressive financial results for Q1 2025, with revenue reaching AED 751.6 million, representing a 33.7% increase compared to the same period last year. This growth was primarily driven by the implementation of variable pricing in January 2025 and the full quarter contribution from two new toll gates.

As shown in the following chart of key financial metrics:

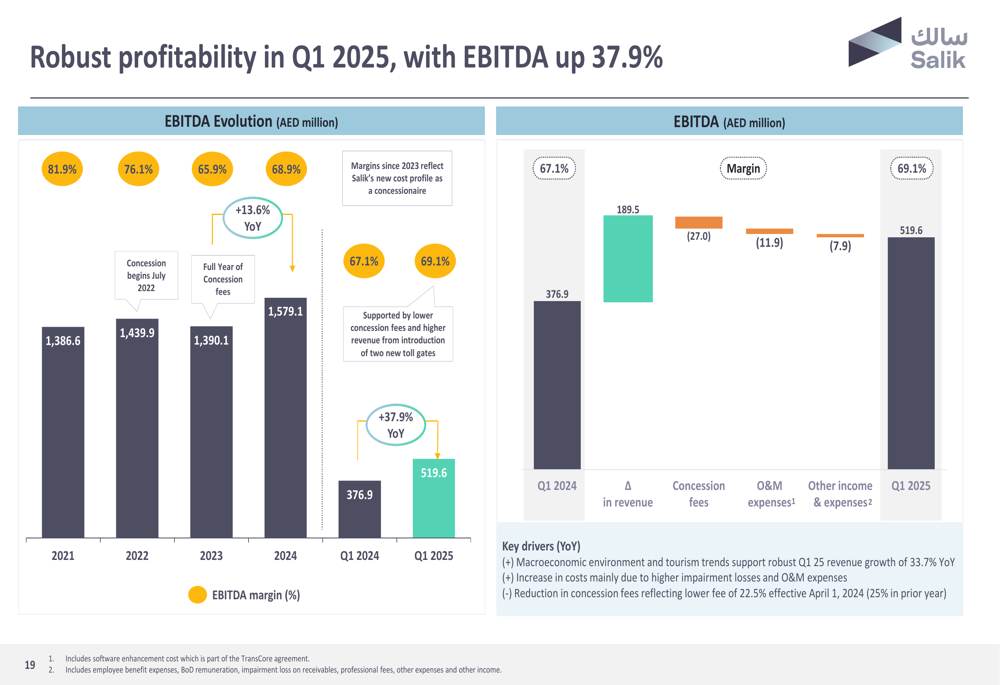

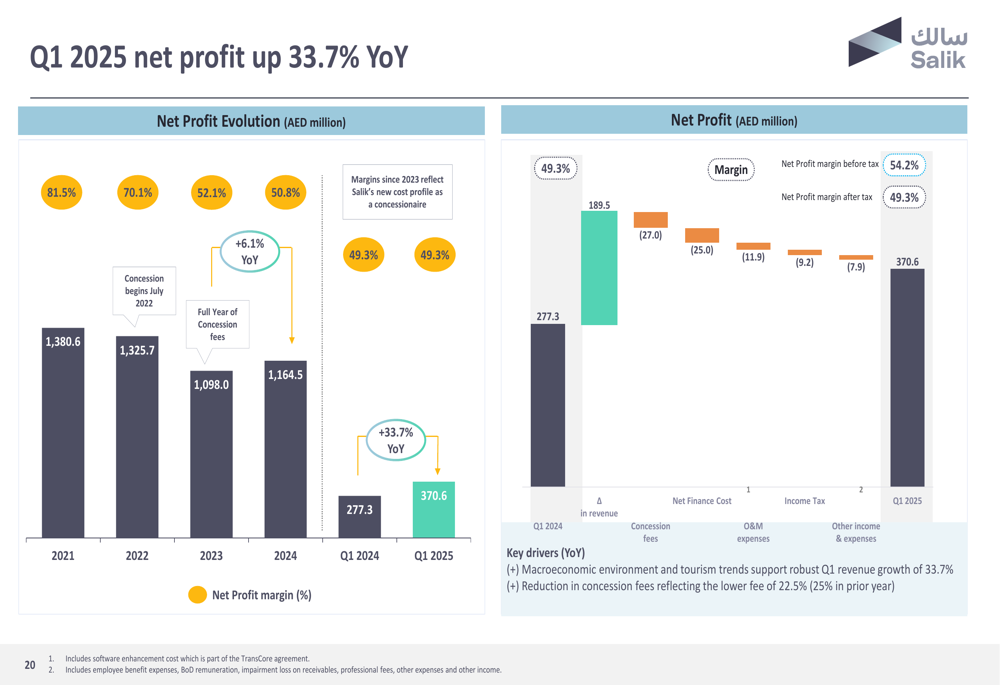

EBITDA grew even more substantially, rising 37.9% year-over-year to AED 519.6 million, with an EBITDA margin of 69.1%. Net profit increased by 33.7% to AED 370.6 million, maintaining a healthy net profit margin of 49.3%.

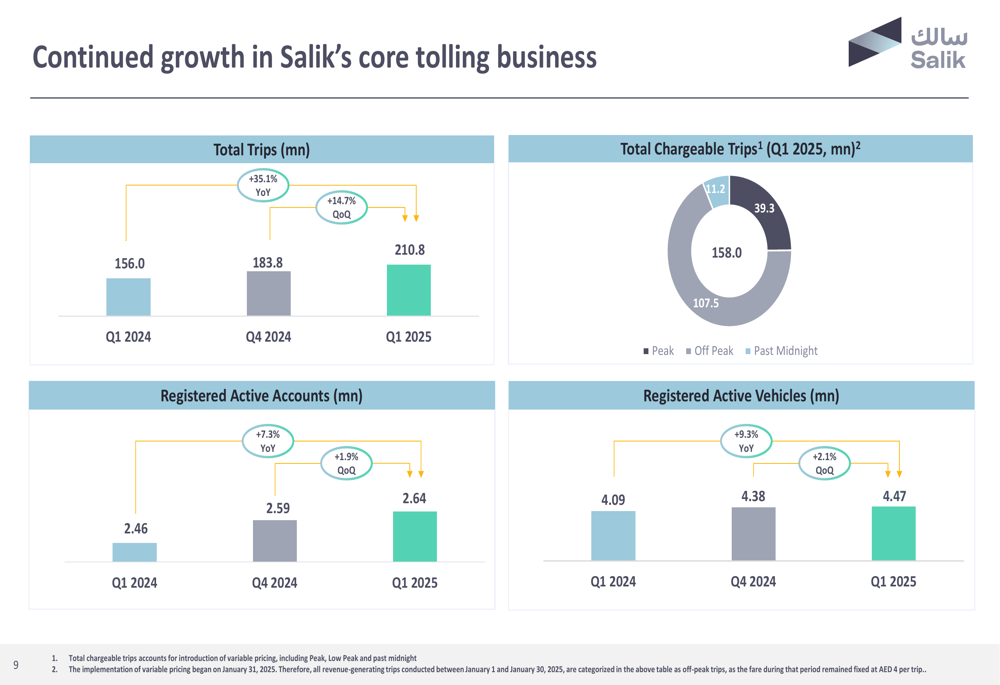

The company’s core tolling business showed strong operational performance with total trips increasing to 210.8 million in Q1 2025, a 35.1% year-over-year growth. Of these, 158.0 million were chargeable trips, with the majority (107.5 million) occurring during peak hours.

The following chart illustrates the growth in Salik’s core tolling business:

Registered active accounts grew to 2.64 million (+7.3% YoY), while registered active vehicles increased to 4.47 million (+9.3% YoY), reflecting broader adoption of Salik’s services.

Strategic Initiatives

A key strategic initiative implemented in Q1 2025 was the introduction of variable pricing, which has already shown positive results. The new pricing model charges AED 6 during peak hours (6:00 AM to 10:00 AM and 4:00 PM to 8:00 PM on weekdays), AED 4 during off-peak hours, and zero fees during past midnight hours (1:00 AM to 6:00 AM).

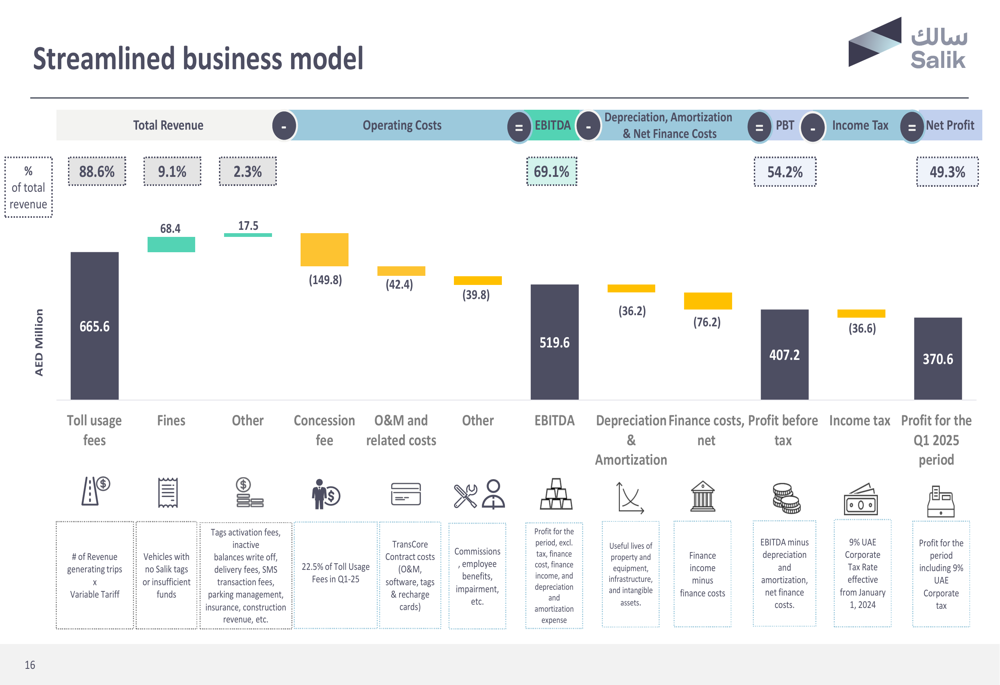

The company’s revenue breakdown demonstrates its streamlined business model, with toll usage fees contributing 88.6% of total revenue, fines accounting for 9.1%, and other sources representing 2.3%.

The following waterfall chart illustrates Salik’s business model and cost structure:

Salik has also made significant progress in diversifying its revenue streams through strategic partnerships. The company’s partnership with EMAAR for Dubai Mall parking generated AED 2.7 million in Q1 2025, while its collaboration with Parkonic is expected to facilitate geographic expansion beyond Dubai with integration across 107+ locations and 135,000+ parking spaces.

The company’s EBITDA has shown consistent improvement over time, as illustrated in the following chart:

Net profit has also maintained a stable trajectory, with margins consistently around 49-50% in recent quarters:

Forward-Looking Statements

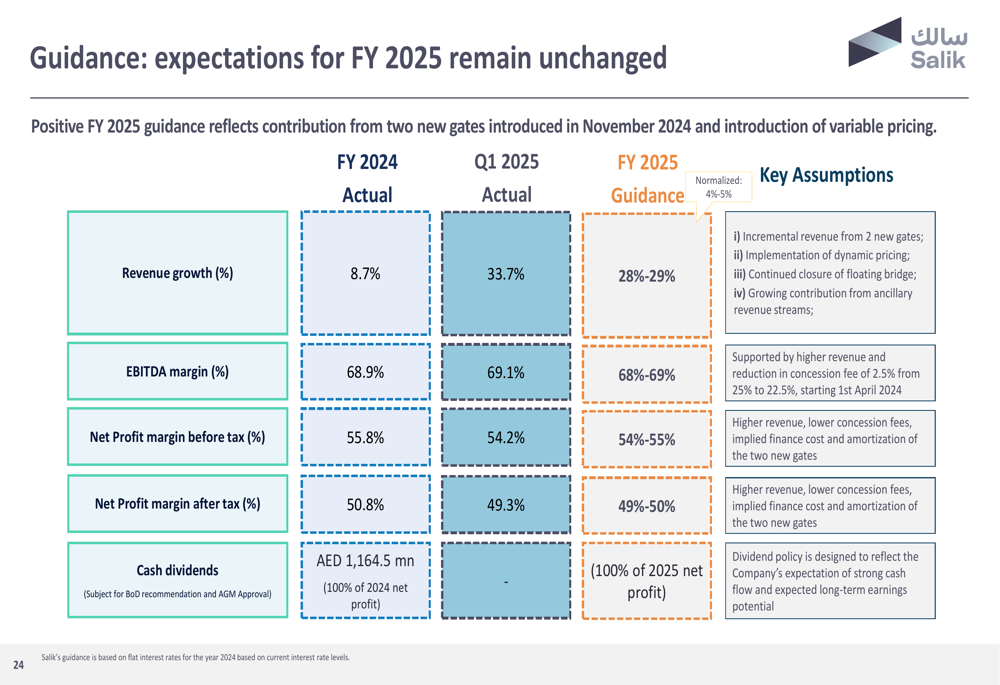

Salik provided positive guidance for FY 2025, projecting revenue growth of 28-29%, an EBITDA margin of 68-69%, and a net profit margin after tax of 49-50%. The company plans to maintain its 100% dividend payout ratio for 2025.

The following slide details the company’s guidance expectations:

For its ancillary revenue streams, Salik has set ambitious medium and long-term targets. By 2026, the company expects parking payment solutions to generate AED 30-50 million annually, data monetization to contribute AED 10-20 million, and other ancillary streams to add AED 2-5 million. These figures are projected to grow substantially by 2030, with parking solutions potentially reaching AED 120-150 million annually.

Salik maintains a healthy balance sheet with AED 6.2 billion in long-term borrowings and related party payable liabilities as of March 31, 2025, offset by AED 1.5 billion in cash and cash equivalents. The company’s net debt-to-T12M EBITDA ratio stands at 2.7x, reflecting conservative leverage. Both Moody’s and Fitch assigned Salik a first-time rating of ’A-’ in December 2024, underscoring its financial stability.

Conclusion

Salik’s Q1 2025 results demonstrate the company’s ability to capitalize on Dubai’s favorable macroeconomic environment while successfully implementing strategic initiatives like variable pricing and expanding its toll gate network. The company’s focus on diversifying revenue streams through partnerships and maintaining strong operational efficiency positions it well for continued growth.

As summarized in the company’s concluding remarks:

With a clear strategy for growth, strong financial performance, and favorable market conditions, Salik appears well-positioned to meet its ambitious targets for 2025 and beyond. The company’s stock (DFM:SALIK) closed at AED 4.94 on May 9, 2025, up 1.53%, reflecting investor confidence in its growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.