Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Salmones Camanchaca SA (SALMOCAM) presented its second quarter 2025 results on August 27, showing improved profitability despite revenue challenges. The Chilean seafood producer, which operates fishing, salmon, and mussel farming divisions, demonstrated effective cost management that helped offset price pressures in key product segments.

The company’s stock closed at 3,530.6 on September 16, 2025, having risen 3.27% on the day and currently trading near its 52-week high, suggesting positive market reception to the company’s operational improvements and debt reduction efforts.

Quarterly Performance Highlights

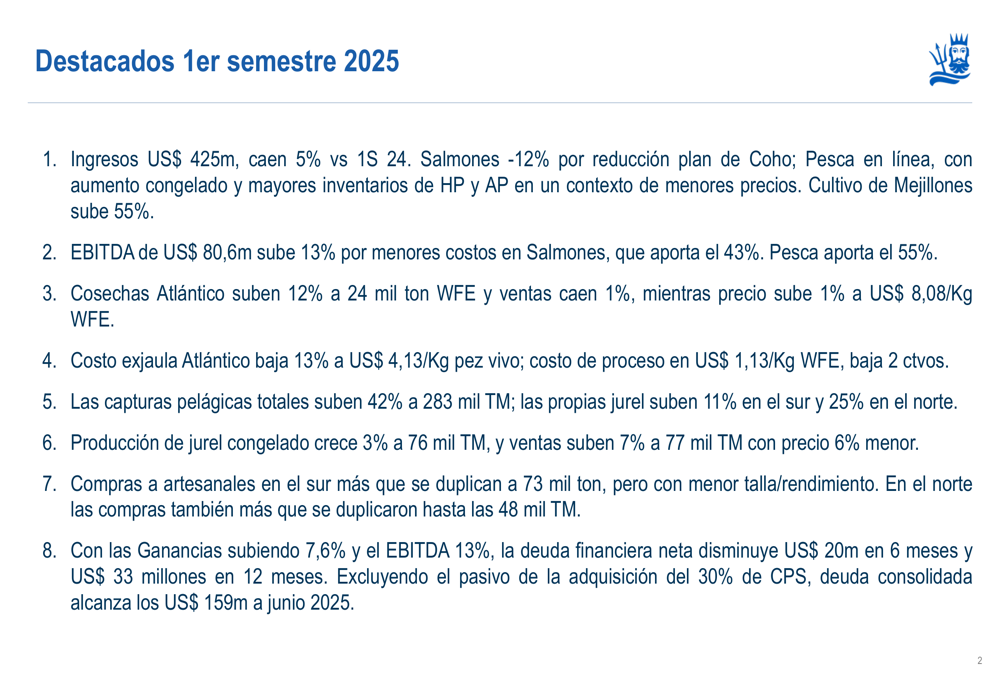

Camanchaca reported revenue of US$425 million for the first half of 2025, representing a 5% decrease compared to the same period in 2024. Despite this revenue decline, the company achieved a 13% increase in EBITDA to US$80.6 million, demonstrating significant operational efficiency improvements.

As shown in the following comprehensive overview of first-half performance:

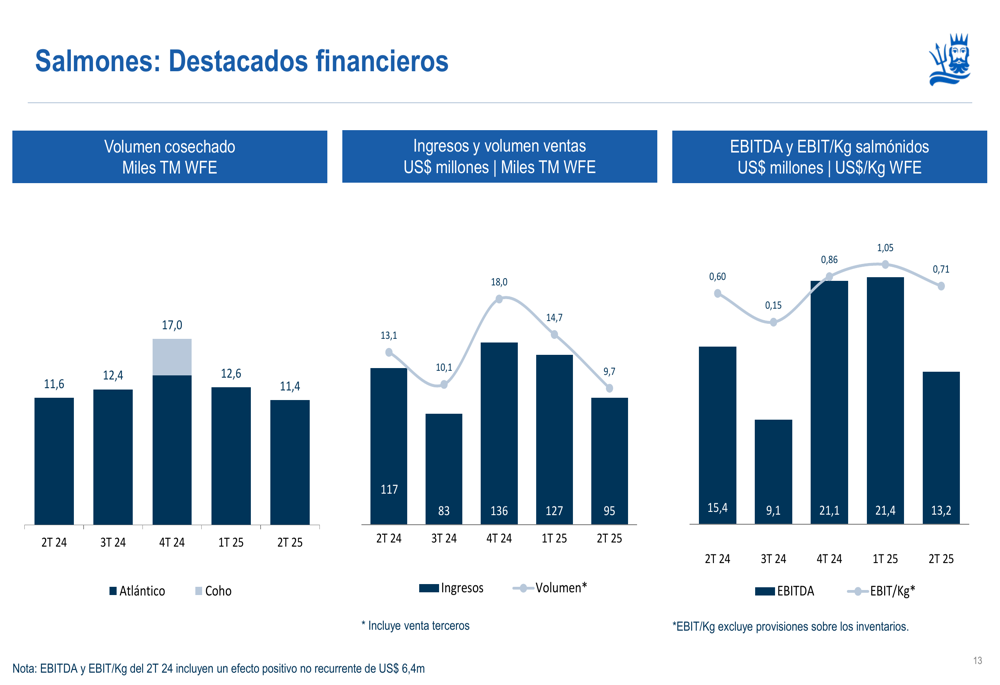

The company’s improved profitability came primarily from lower salmon production costs, with the fishing division contributing 55% of total EBITDA and salmon operations contributing 43%. Atlantic salmon harvests increased by 12% to 24,000 tons WFE (whole fish equivalent), while sales volume decreased slightly by 1%. Salmon prices increased marginally by 1% to US$8.08/kg WFE.

Total pelagic catches rose significantly by 42% to 283,000 tons, with jack mackerel catches increasing by 11% in the south and 25% in the north. This higher production volume helped offset price pressures in the fishing segment.

Fishing Division Performance

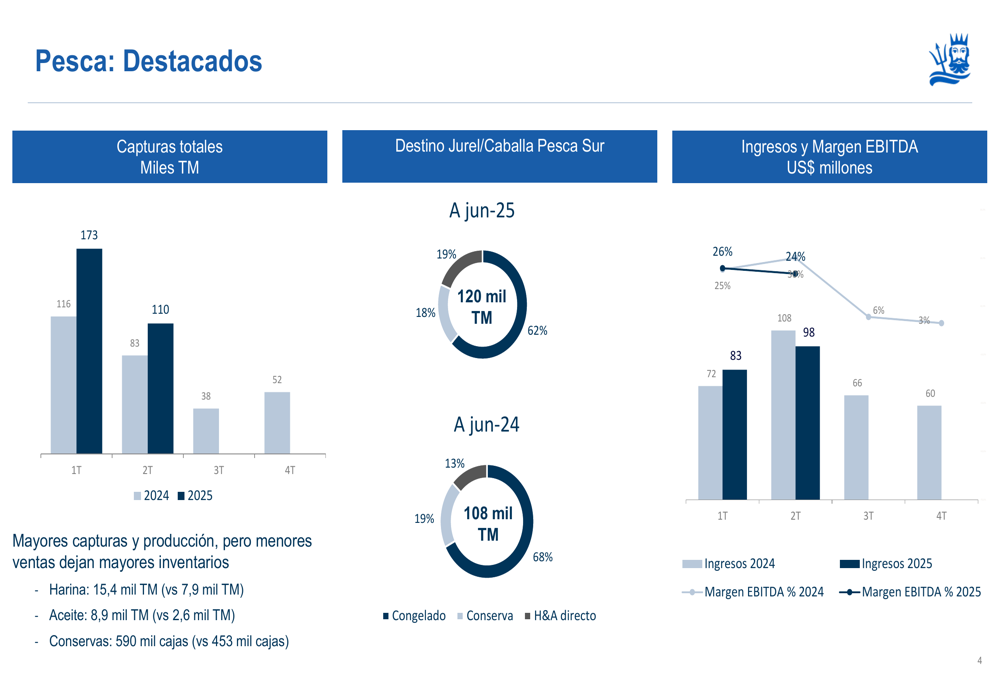

The fishing division faced price pressures but benefited from higher catch volumes. Total catches increased from 199,000 tons in the first half of 2024 to 283,000 tons in the same period of 2025, with particularly strong performance in the second quarter.

The following chart illustrates the division’s catch volumes and revenue trends:

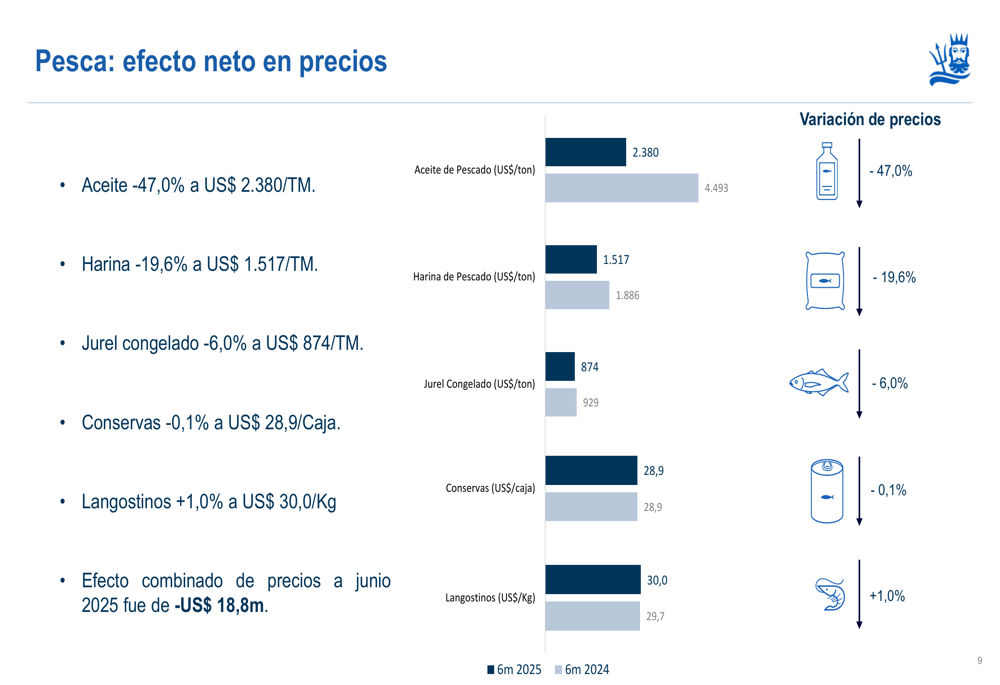

While production volumes increased, the division faced significant price declines across key products. Fish oil prices dropped dramatically by 47% to US$2,380 per ton, while fishmeal prices decreased by 19.6% to US$1,517 per ton. Frozen jack mackerel prices also fell by 6% to US$874 per ton.

The price impacts are clearly visualized in this breakdown:

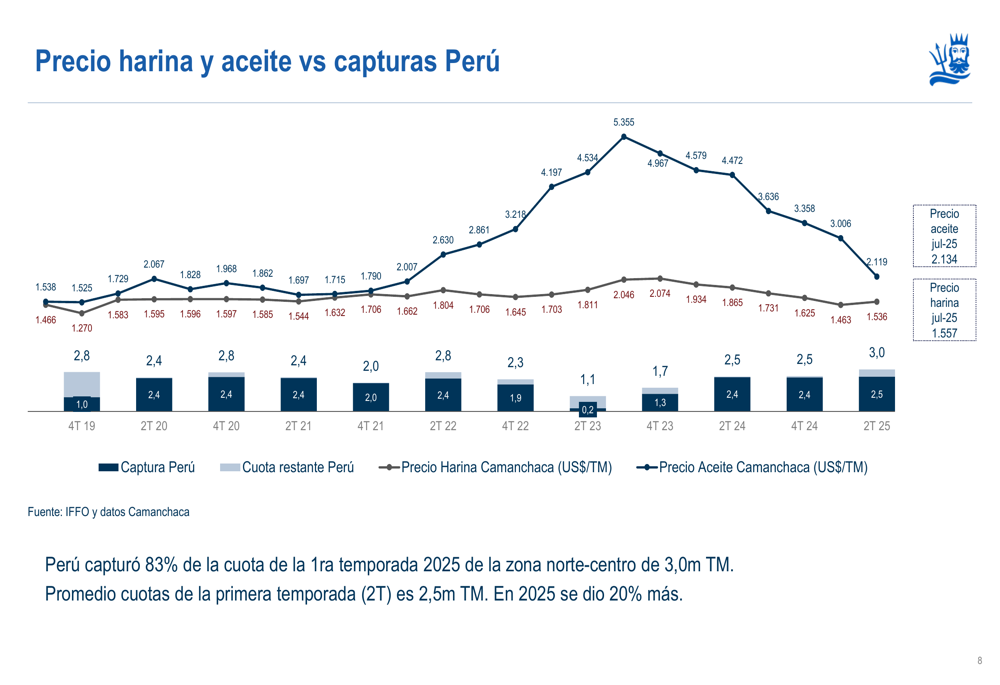

The combined negative price effect amounted to US$18.8 million for the first half of 2025. These price pressures were largely attributed to normalized catches in Peru, as shown in the relationship between Peruvian catches and global prices:

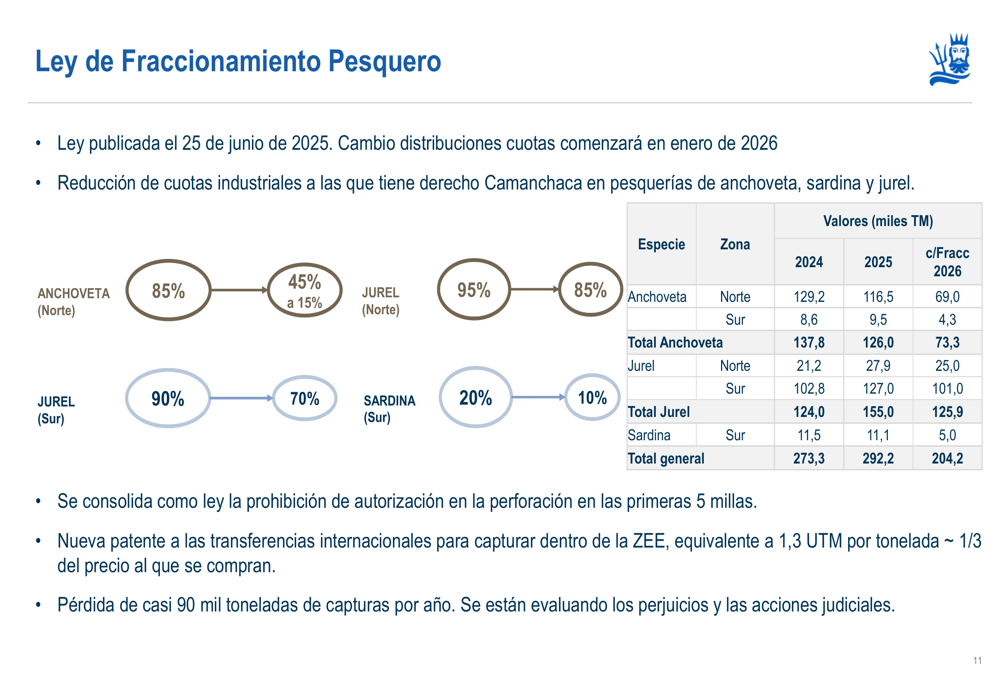

A significant regulatory challenge emerged with the publication of a new fishing law on June 25, 2025. The law will reduce Camanchaca’s industrial fishing quotas starting in January 2026, affecting anchoveta, sardine, and jack mackerel fishing rights. The company estimates it will lose nearly 90,000 tons of annual catches and is evaluating potential legal actions.

The regulatory changes are detailed in this table showing the quota reductions:

Salmon Division Performance

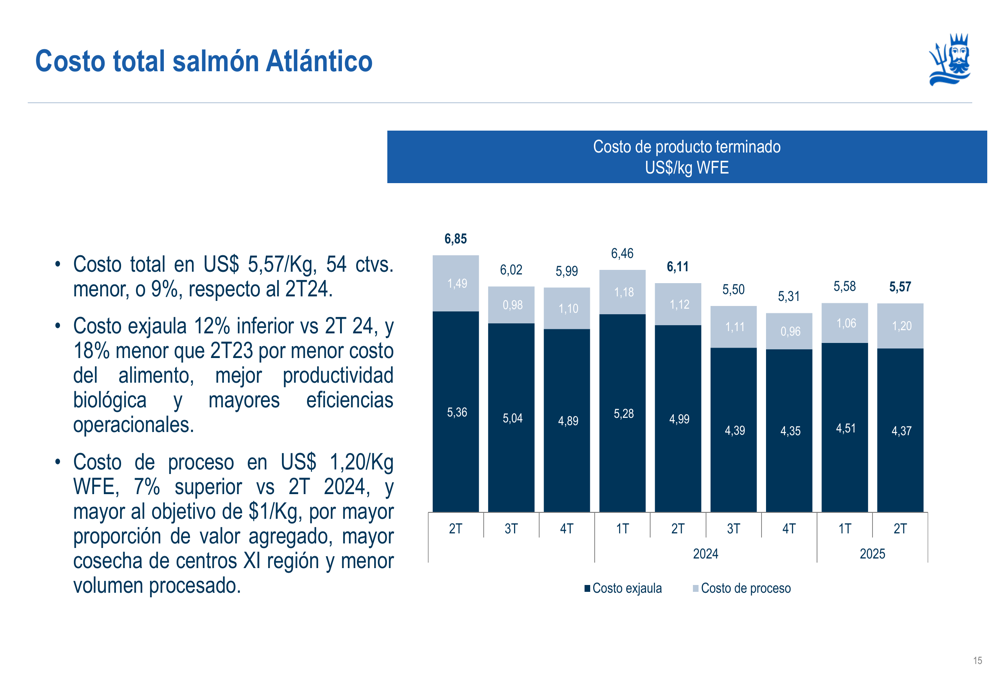

The salmon division showed signs of recovery, primarily driven by significant cost reductions. Atlantic salmon ex-farm costs decreased by 13% to US$4.13/kg live weight, while processing costs declined slightly to US$1.13/kg WFE.

The following chart shows the division’s key financial metrics:

Cost improvements were a key driver of better performance, as illustrated in this breakdown of salmon production costs:

The division’s EBITDA contribution increased to US$20.7 million with an 8% margin, compared to the fishing division’s US$44.5 million with a 25% margin. The southern cultures division (primarily mussels) contributed US$3.6 million with a 15% margin.

Financial Position and Debt Reduction

Camanchaca made significant progress in strengthening its balance sheet during the period. Net financial debt decreased by US$20 million in the first half of 2025 and by US$33 million compared to June 2024.

The company’s financial position is summarized in this table:

The net debt to EBITDA ratio improved substantially to 1.7x from 2.7x in June 2024, reflecting both debt reduction and improved profitability. Excluding the liability from the acquisition of a 30% stake in CPS, consolidated debt reached US$159 million as of June 2025.

The company maintained strong liquidity with approximately US$100 million in cash and available credit lines as of June 2025. The equity to assets ratio stood at 50%, indicating a balanced capital structure.

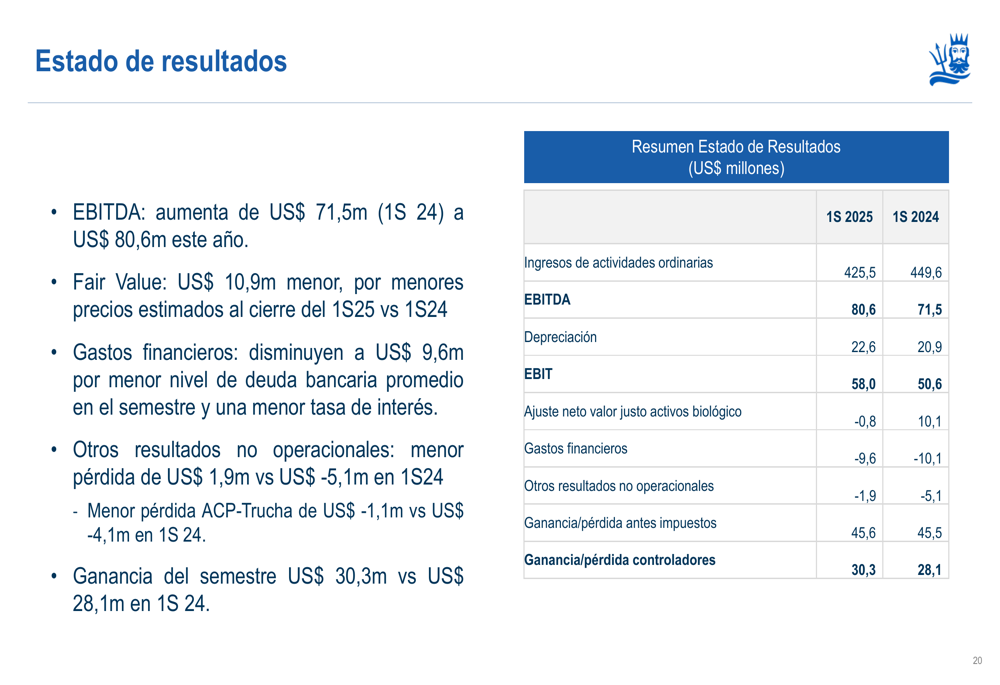

The income statement shows net profit growth to US$30.3 million in the first half of 2025, compared to US$28.1 million in the same period of 2024:

Outlook and Strategic Focus

Looking ahead, Camanchaca faces both opportunities and challenges. The company plans to increase Atlantic salmon harvests to 57-60 thousand tons WFE in 2025, up from 47.7 thousand tons in 2024, while reducing Coho salmon production to approximately 3.5 thousand tons.

The main strategic challenge will be adapting to the new fishing law’s quota reductions starting in 2026. Management is evaluating the financial impact and potential legal actions to mitigate these effects.

The company’s continued focus on cost efficiency and debt reduction positions it well to navigate market price volatility, particularly in the fishing segment. With improved financial metrics and operational efficiencies, Camanchaca appears positioned to maintain profitability despite revenue challenges, though regulatory changes remain a significant concern for future operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.