Wall St futures steady after weekly gains; Fed rate decision looms

Introduction & Market Context

Sampo Oyj (HEL:SAMPO) reported strong first-quarter results for 2025, with significant growth in both premiums and underwriting profit, prompting the Nordic insurer to raise its full-year outlook. The company presented its Q1 2025 results on May 7, highlighting robust performance across most business segments despite varying market conditions across its operating regions.

The insurer benefited from a favorable claims environment in the Nordics due to benign winter weather, while maintaining disciplined underwriting in competitive markets. Claims inflation remained stable at around 4% in Nordic regions, while UK claims inflation moderated to mid-single digit percentages, returning to long-term trends.

Quarterly Performance Highlights

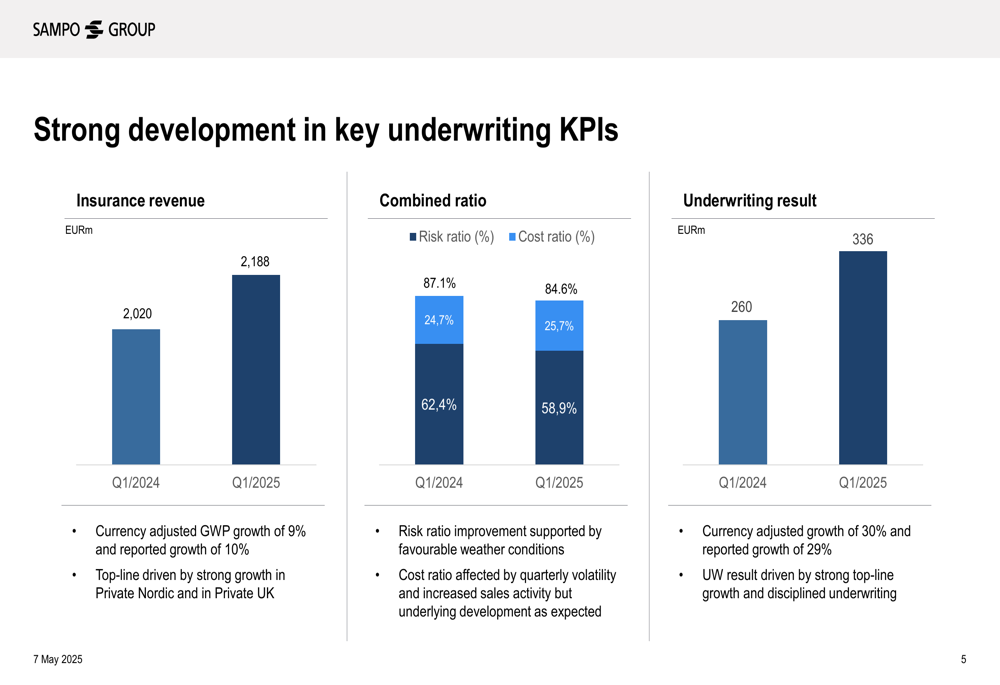

Sampo reported substantial growth in key financial metrics for Q1 2025, with gross written premiums (GWP) reaching €3,616 million, representing a 9% year-on-year increase on a currency-adjusted basis. The company’s underwriting result saw an even more impressive gain, jumping 30% to €336 million compared to the same period last year.

As shown in the following chart of key financial metrics, Sampo demonstrated improvement across most underwriting KPIs:

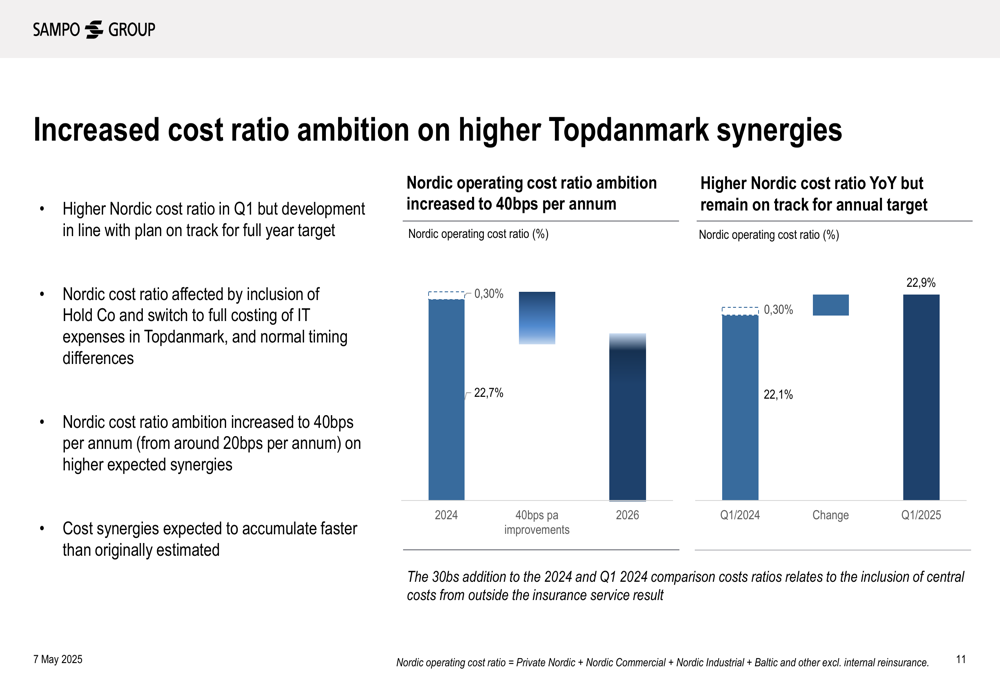

The combined ratio, a key measure of underwriting profitability, improved to 84.6% from 87.1% in Q1 2024, driven by a significant reduction in the risk ratio from 62.4% to 58.9%. This improvement was partially offset by an increase in the cost ratio from 24.7% to 25.7%, which the company attributed to quarterly volatility and increased sales activity.

Operating earnings per share rose 9% year-on-year to €0.11, while the Solvency II coverage ratio strengthened to 180%, up 3 percentage points from Q4 2024.

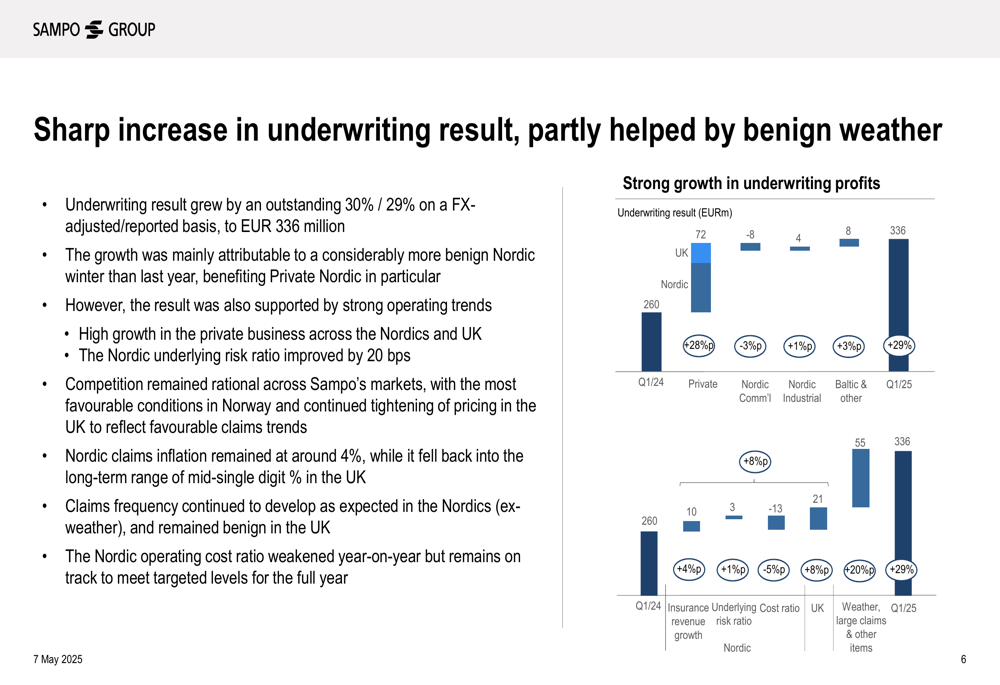

The following chart illustrates the sharp increase in underwriting result, which was partly helped by benign weather conditions:

Segment Performance Analysis

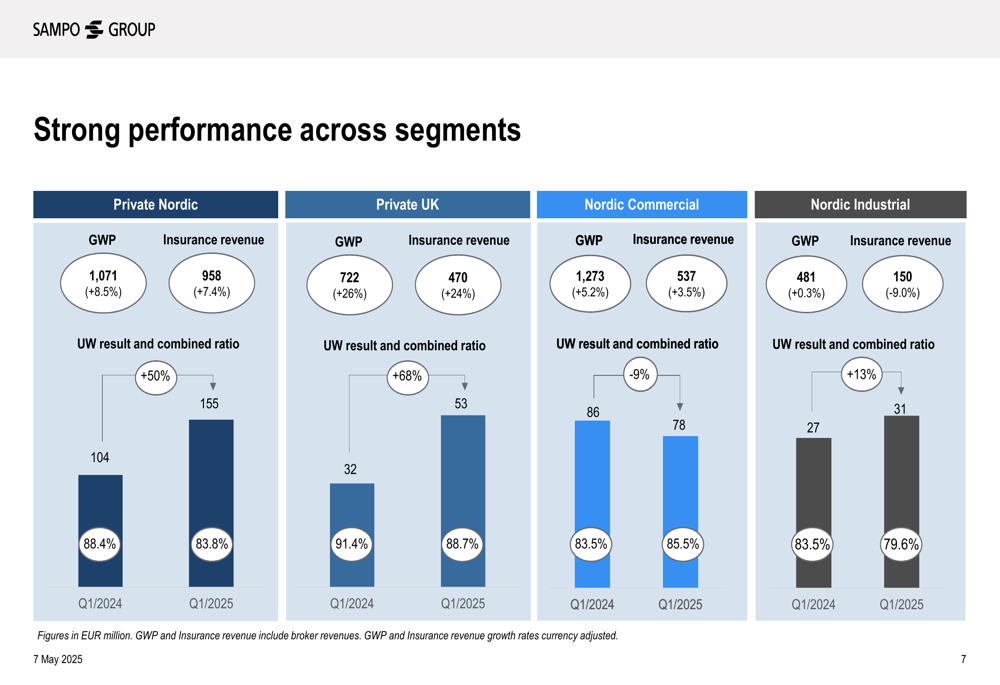

Sampo’s growth was primarily driven by strong performance in its Private Nordic and Private UK segments, while Nordic Commercial and Nordic Industrial showed more modest results.

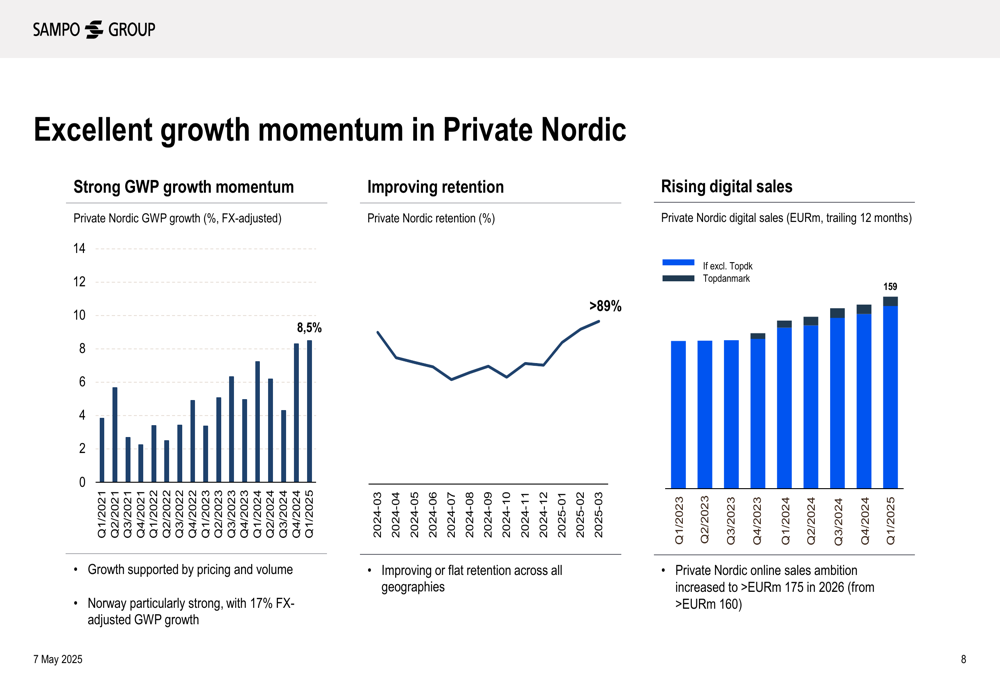

The Private Nordic segment delivered 8.5% GWP growth, with its underwriting result surging to €155 million from €104 million in Q1 2024. The combined ratio improved significantly from 88.4% to 83.8%. Norway was particularly strong, with 17% currency-adjusted GWP growth.

As illustrated in the following segment performance breakdown:

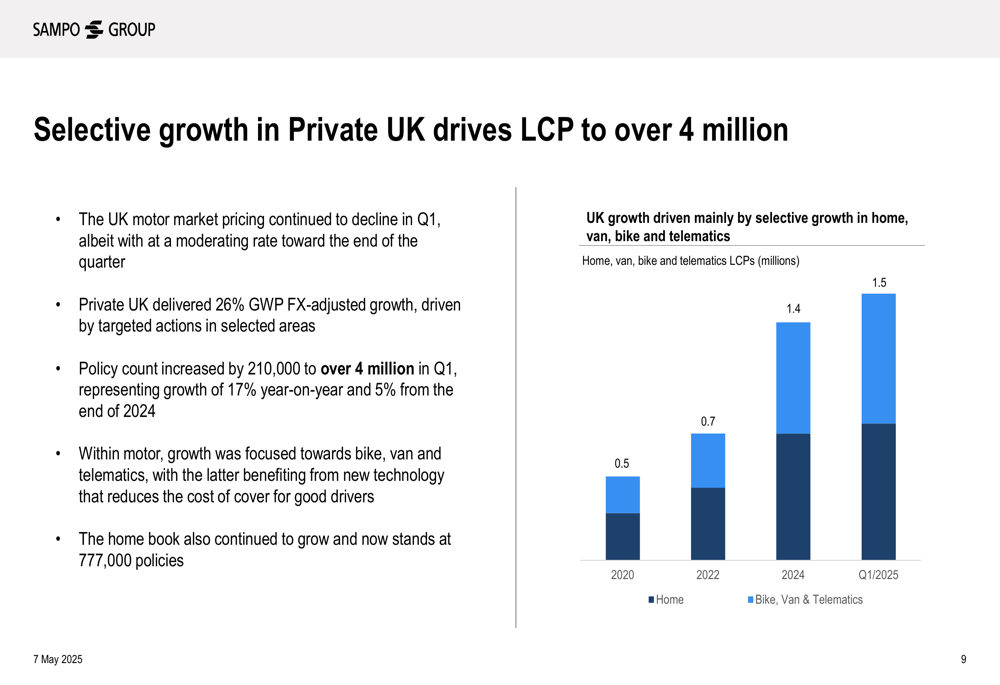

The Private UK segment was the standout performer with 26% GWP growth, driving the underwriting result up to €53 million from €32 million in Q1 2024. The combined ratio improved from 91.4% to 88.7%. Policy count increased by 210,000 to over 4 million in Q1, representing 17% year-on-year growth.

The UK growth was strategically focused on selected areas, as shown in the following chart:

Within the UK motor market, which continued to see price declines in Q1 (albeit at a moderating rate), Sampo focused growth on bike, van, and telematics segments. The home insurance portfolio also continued to expand, reaching 777,000 policies.

The Private Nordic segment maintained strong growth momentum, with improving retention rates and rising digital sales:

Strategic Initiatives

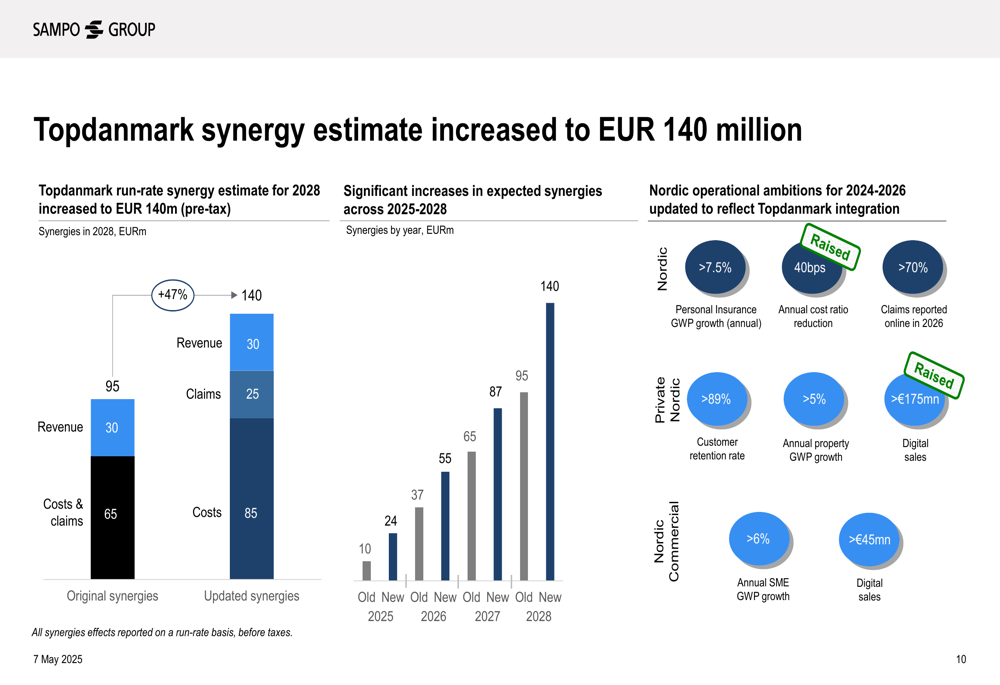

A significant development in Sampo’s strategic outlook was the increased synergy estimate from the Topdanmark integration, now projected at €140 million by 2028 on a pre-tax basis. This represents a substantial increase from previous estimates, with synergies expected to come from revenue enhancement, claims optimization, and cost efficiencies.

The following chart details the increased synergy expectations and updated operational ambitions:

Based on these higher expected synergies, Sampo has increased its Nordic cost ratio improvement ambition to 40 basis points per annum, up from the previous target of around 20 basis points per annum. The company also raised its Private Nordic online sales ambition to more than €175 million in 2026, up from the previous target of €160 million.

The cost synergies are expected to accumulate faster than originally estimated, as illustrated in this chart:

Forward-Looking Statements

Based on the strong first-quarter performance, Sampo raised its outlook for the 2025 underwriting result to €1,400-1,500 million, representing 6-14% year-on-year growth. This upgraded guidance reflects confidence in continued favorable operating trends and the accelerated realization of synergies from the Topdanmark integration.

The company maintained its focus on disciplined underwriting and selective growth in competitive markets, particularly in the UK where motor pricing remained under pressure. Management expressed confidence in the continued rational competitive environment across Nordic markets and the company’s ability to maintain pricing discipline while growing in targeted segments.

Sampo’s digital transformation continues to progress, with increased targets for online sales reflecting the company’s commitment to enhancing its digital capabilities and meeting evolving customer preferences across its markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.