Oil prices rise on US-China trade progress, supply jitters persist

Introduction & Market Context

Sandvik AB reported solid third-quarter 2025 results on October 20, showing strong organic growth despite significant currency headwinds. The Swedish engineering group’s stock responded positively, rising 2.74% to close at 277.7 SEK, approaching its 52-week high of 280.3 SEK. The stock has delivered an impressive 118.72% return year-to-date, reflecting investor confidence in the company’s strategic direction.

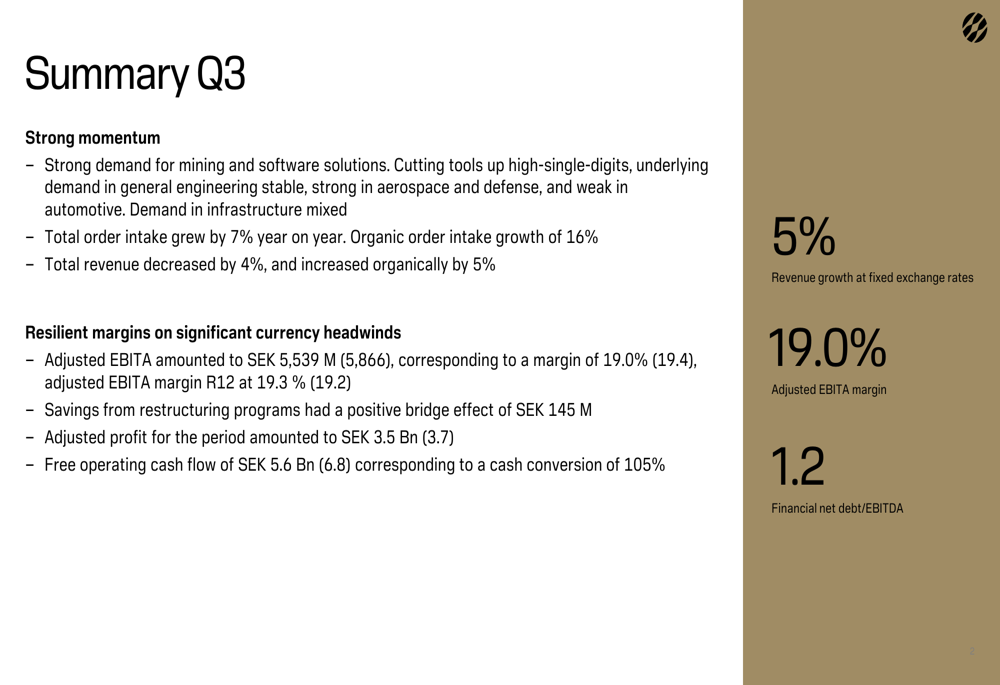

The company’s Q3 performance demonstrated resilience in challenging market conditions, with order intake growing by 7% year-on-year, driven by robust demand in mining and software solutions. While total revenue decreased by 4% to SEK 29.2 billion, organic growth reached 5%, highlighting the impact of currency fluctuations on reported figures.

Quarterly Performance Highlights

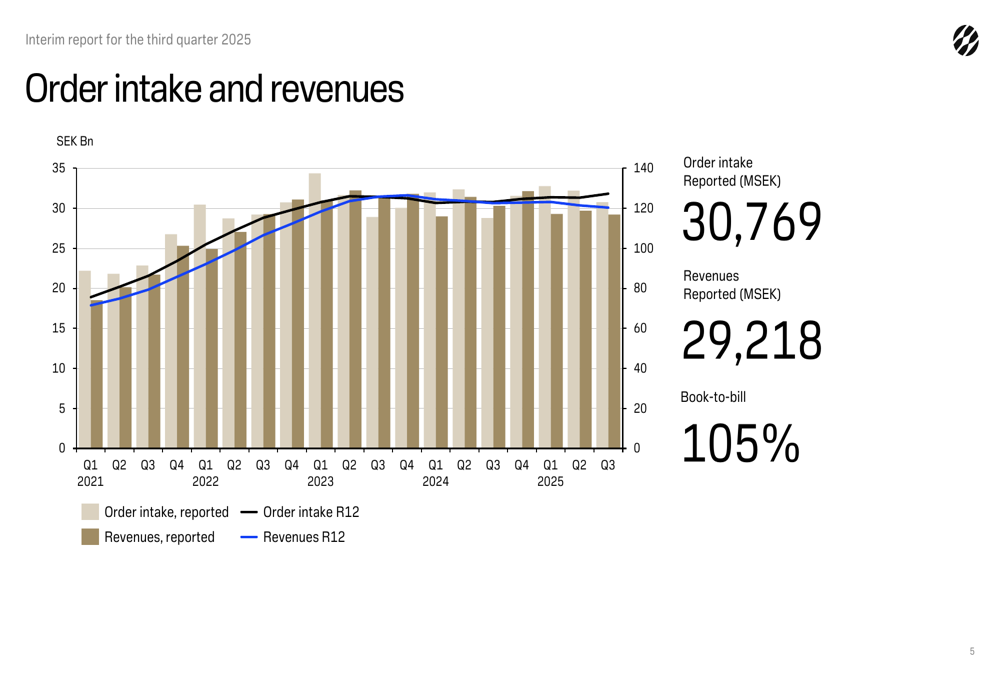

Sandvik maintained strong operational momentum in Q3 2025, with order intake reaching SEK 30.8 billion, representing a 7% increase year-on-year. The company achieved an impressive 16% organic order growth, though this was partially offset by a 9% negative currency impact.

As shown in the following summary of key financial metrics:

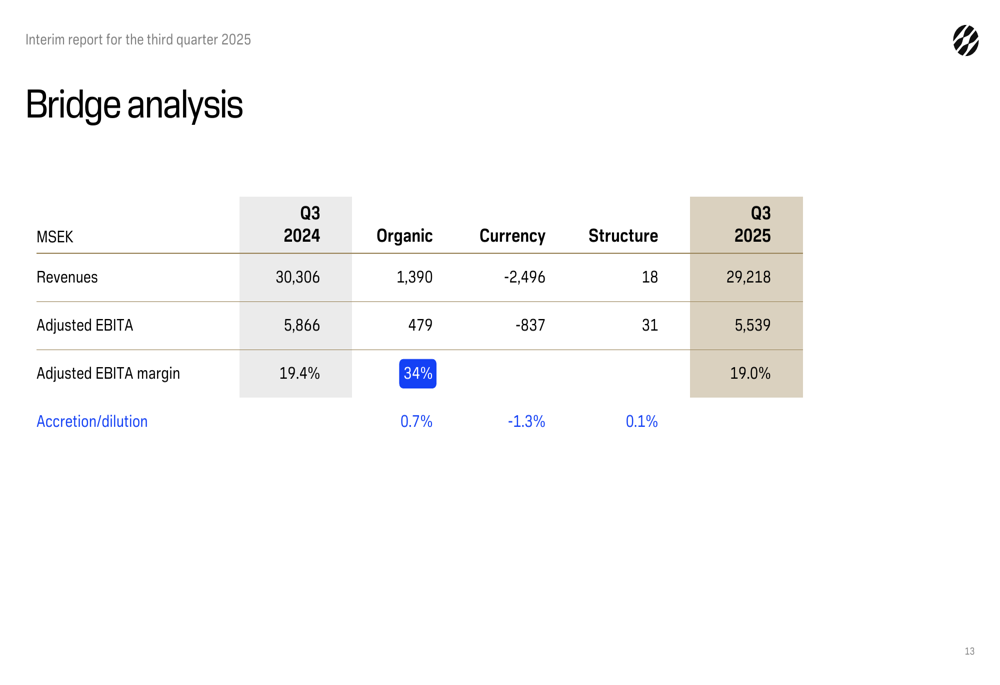

Revenue decreased by 4% to SEK 29.2 billion, but increased 5% organically, again reflecting the significant currency impact of -8%. Adjusted EBITA amounted to SEK 5.5 billion, corresponding to a margin of 19.0%, slightly below the 19.4% reported in Q3 2024. However, on a rolling 12-month basis, the adjusted EBITA margin improved to 19.3% from 19.2%.

The company’s book-to-bill ratio remained healthy at 105%, indicating continued strong demand relative to current revenue levels.

Currency headwinds had a significant impact on profitability, with a negative effect of SEK 837 million, diluting the EBITA margin by 130 basis points. Despite these challenges, Sandvik’s restructuring programs contributed positively, with savings of SEK 145 million.

The detailed EBITA bridge analysis reveals how organic growth positively contributed SEK 479 million to adjusted EBITA, while currency effects reduced it by SEK 837 million:

Geographic and Segment Analysis

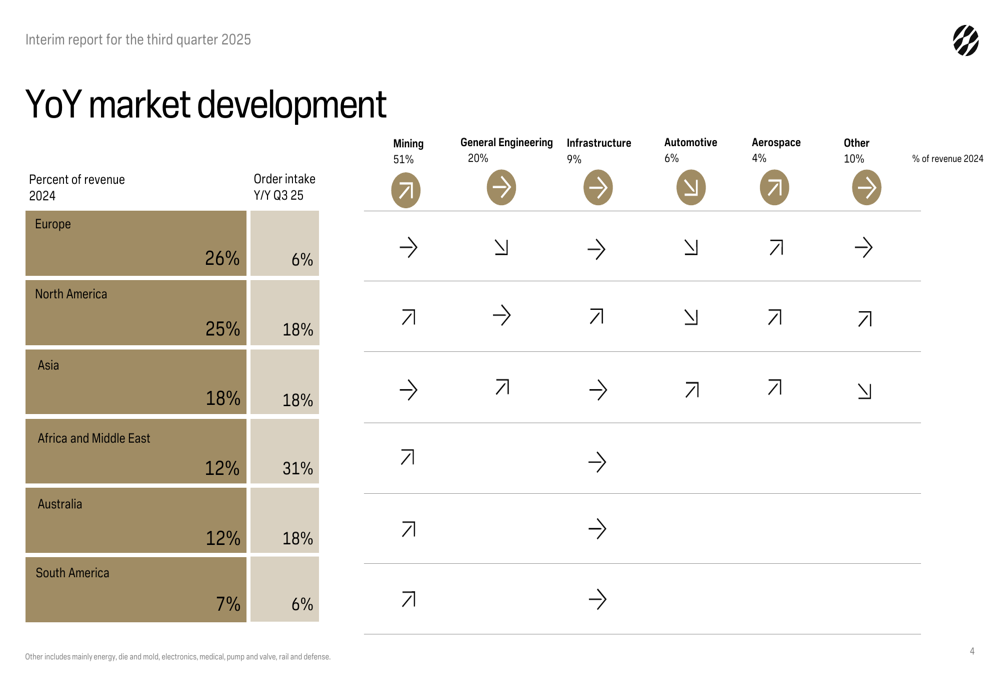

Sandvik experienced varied performance across regions, with particularly strong growth in Africa and the Middle East (+31%), followed by North America, Asia, and Australia (all +18%). Europe and South America showed more modest growth at 6% each.

The regional breakdown illustrates this geographic divergence in performance:

By business segment, the Mining division demonstrated continued strong momentum with a 13% increase in order intake (24% at fixed exchange rates). The division, which accounts for 51% of company revenues, benefited from robust demand for both equipment and aftermarket services.

The Rock Processing division, representing 9% of revenues, reported flat order intake but showed solid growth in its mining segment, while infrastructure demand remained subdued.

The Machining and Intelligent Manufacturing division, accounting for 40% of revenues, delivered mixed results with order intake increasing by 1% (8% at fixed exchange rates). Cutting tools showed high-single-digit growth, with strong performance in aerospace and defense contrasting with weakness in the automotive sector.

Strategic Initiatives and Innovation

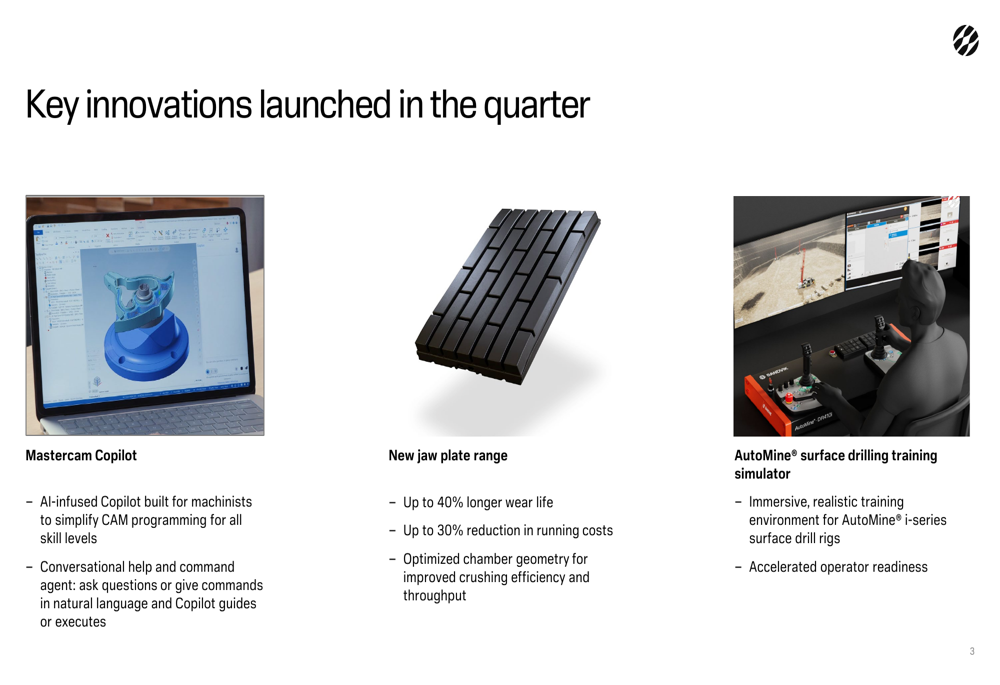

Sandvik continued to invest in innovation, launching several key products during the quarter that strengthen its competitive position. These innovations highlight the company’s focus on digitalization and productivity improvements.

The quarter saw the introduction of Mastercam Copilot, an AI-powered assistant for machinists that simplifies CAM programming through natural language interaction. The company also launched a new jaw plate range offering up to 40% longer wear life and 30% reduction in running costs, as well as an AutoMine surface drilling training simulator to accelerate operator readiness.

CEO Stefan Widing emphasized the company’s digital focus during the earnings call, stating: "We have a very solid foundation and culture that drives strong financial performance and strategic execution." He highlighted double-digit growth in Intelligent Manufacturing and Digital Mining Technologies, underscoring Sandvik’s commitment to digital transformation.

Financial Position and Cash Flow

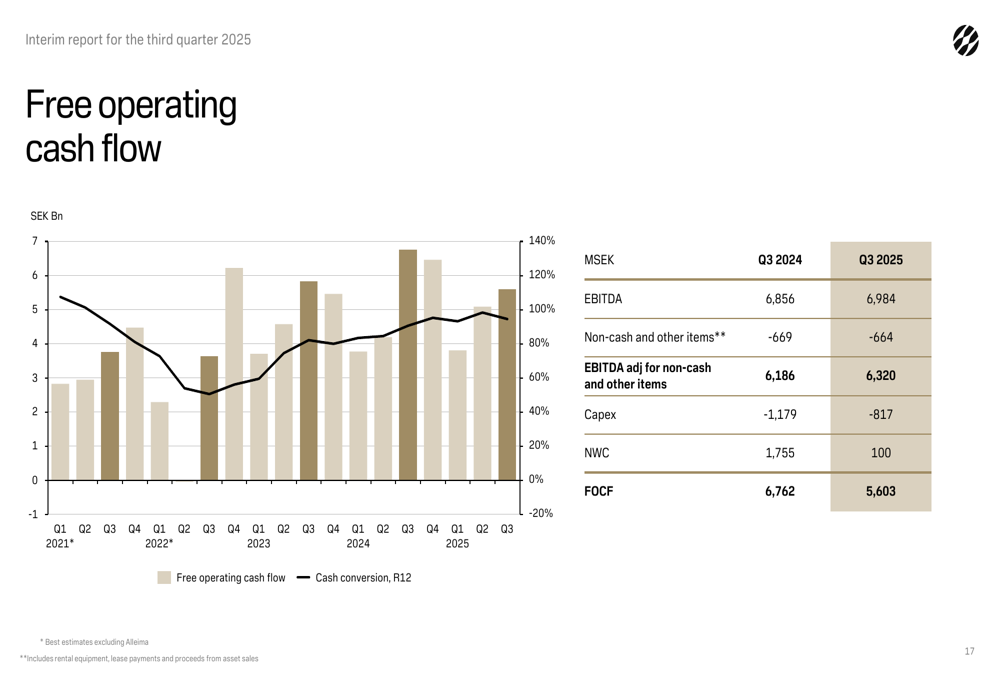

Sandvik maintained a strong financial position with free operating cash flow of SEK 5.6 billion, representing a cash conversion rate of 105%. This represents a decrease from SEK 6.8 billion in Q3 2024, primarily due to lower working capital improvement.

The company’s detailed cash flow breakdown shows the components contributing to this performance:

Net working capital improved to 29.3% of revenues from 30.2% in the prior year, while financial net debt/EBITDA remained healthy at 1.2. The company’s return on capital employed increased to 15.1% from 13.5% in Q3 2024.

Interest costs decreased significantly, with net interest expenses of SEK 201 million compared to SEK 390 million in Q3 2024. The total yield cost decreased to 3.5% from 4.9%, reflecting improved financing conditions.

Outlook and Guidance

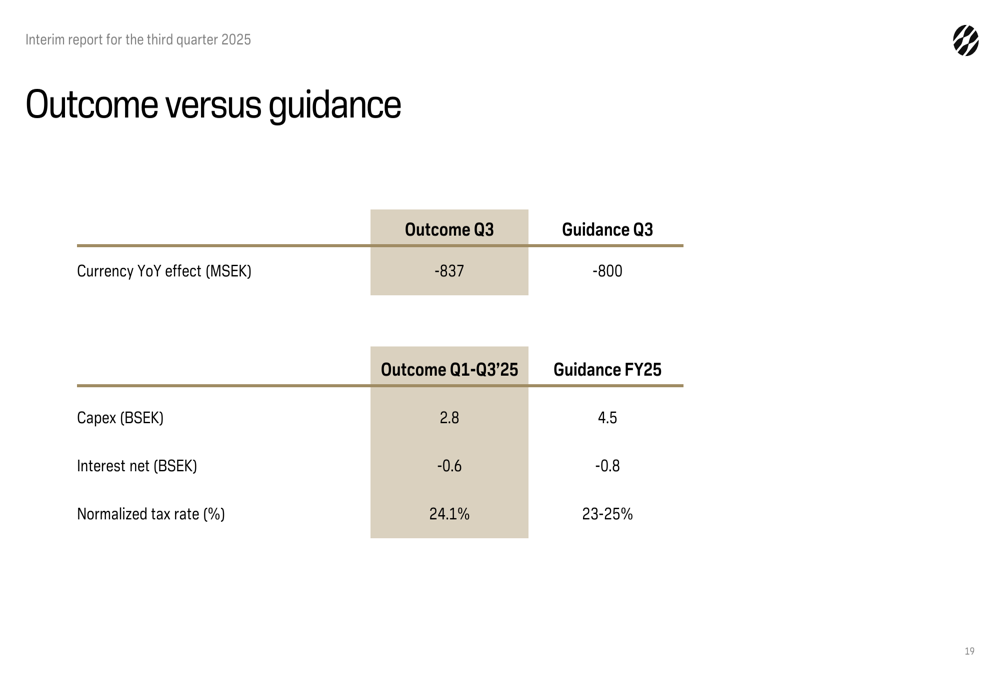

Looking ahead to Q4 2025, Sandvik expects continued currency headwinds. Based on exchange rates at the end of September, the company anticipates a negative impact of approximately SEK 1 billion on operating profit from transaction and translation effects.

The company’s performance against previous guidance shows generally positive results, with actual outcomes closely matching or exceeding projections:

For the full year 2025, Sandvik maintained its guidance for capital expenditure at approximately SEK 4.5 billion, underlying interest net at around SEK 0.8 billion, and a normalized tax rate of 23-25%.

Lead times for mining equipment remain extended at 9-12 months, indicating sustained strong demand in this segment. During the earnings call, management noted that brownfield projects account for approximately 70% of mining order intake, providing a stable foundation for future growth.

Conclusion

Sandvik’s Q3 2025 results demonstrate the company’s ability to deliver organic growth and maintain resilient margins despite significant currency challenges. The strong performance in mining and digital technologies, combined with continued innovation, positions the company well for future growth.

While currency headwinds present near-term challenges, particularly for Q4, the company’s diversified geographic presence and product portfolio provide important buffers. Sandvik’s decentralized structure enables quick responses to changing market conditions, a valuable attribute in the current uncertain geopolitical and macroeconomic environment.

Investors have responded positively to the results, as evidenced by the stock’s performance. With strong order intake, healthy margins, and continued innovation, Sandvik appears well-positioned to navigate the complex global business environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.