AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Brazilian sugar and ethanol producer São Martinho released its fourth quarter and full-year 2024/25 results in June 2025, highlighting its financial performance and strategic positioning in a challenging market environment. The presentation revealed the company’s focus on optimizing its product mix between sugar and ethanol while emphasizing the cost advantages of corn-based ethanol production.

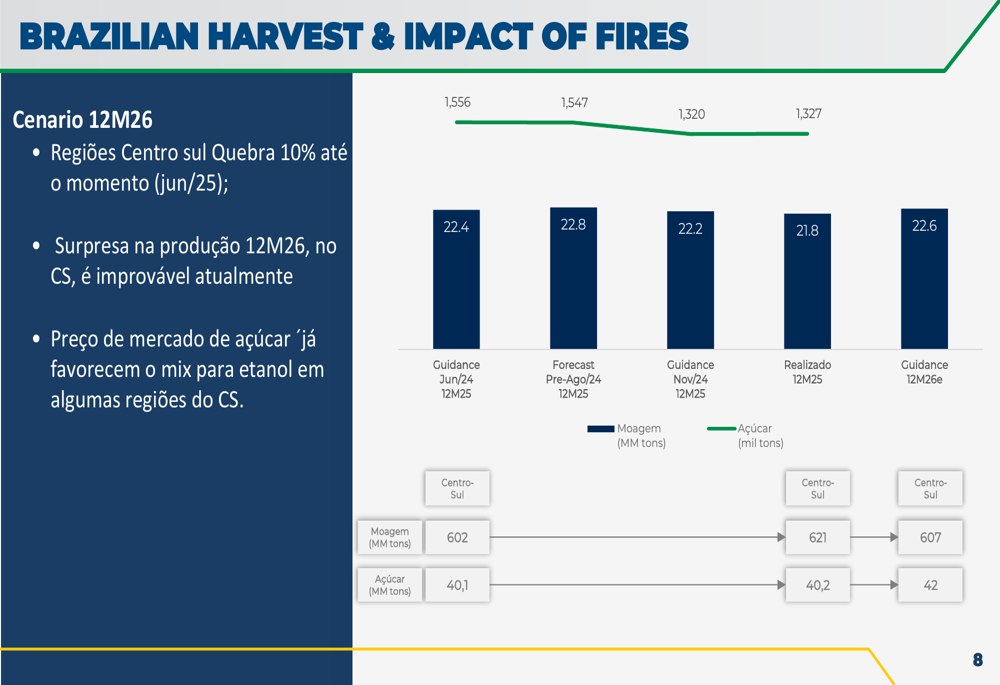

The company’s results come amid a complex backdrop for Brazilian sugar producers, with the presentation noting that sugarcane crush in the Center-South region is down 10% due to impacts from fires. Despite these challenges, São Martinho maintained relatively stable margins on sugar production while showing improvement in its ethanol segment.

Quarterly Performance Highlights

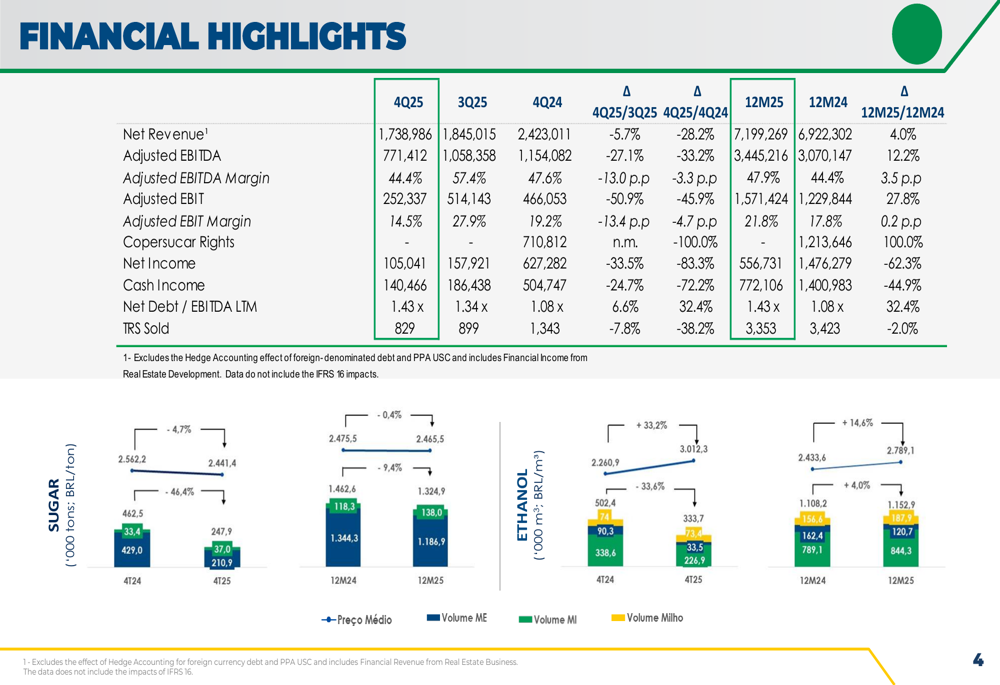

São Martinho reported net revenue of 1,738,986 (in thousands of BRL) for the fourth quarter of 2025, with an adjusted EBITDA of 771,412, representing a solid EBITDA margin of 44.4%. The company’s net income for the quarter stood at 105,041, while cash income reached 140,466.

As shown in the following detailed financial comparison across quarters:

For the full year 2024/25, the company’s sugar and ethanol metrics showed mixed results. Sugar margins declined slightly year-over-year, while ethanol margins showed modest improvement, turning from negative to positive territory.

Detailed Financial Analysis

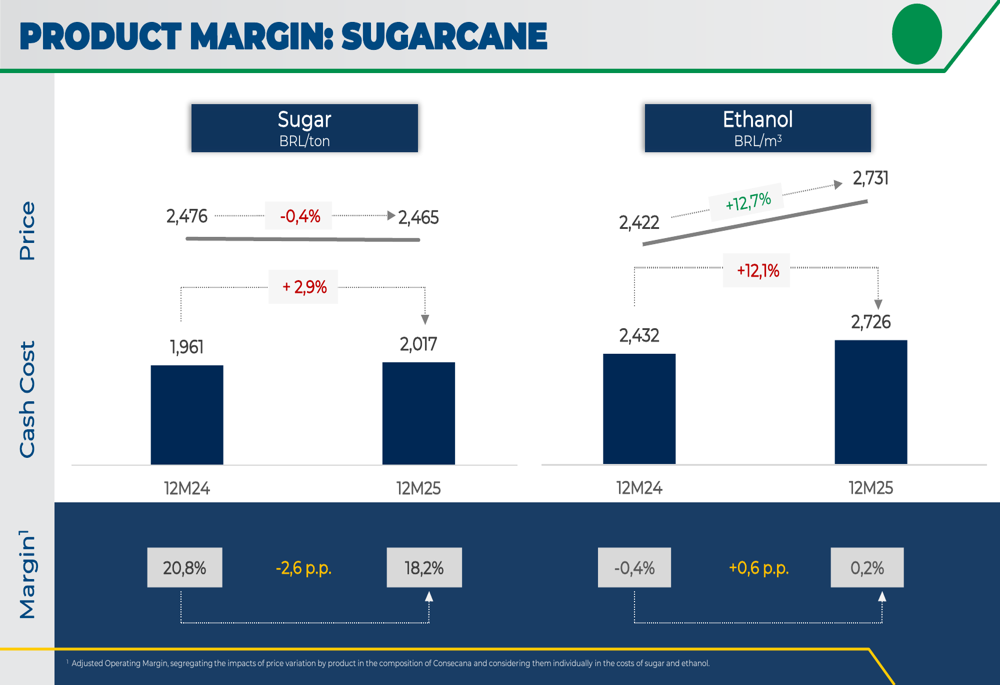

A closer examination of São Martinho’s product margins reveals the performance dynamics across its portfolio. For sugar, the price in the 12-month period was 2,465 BRL/ton, slightly down from 2,476 BRL/ton in the previous year. With cash costs rising from 1,961 to 2,017 BRL/ton, sugar margins contracted from 20.8% to 18.2%.

The ethanol segment showed improvement, with prices increasing from 2,422 to 2,731 BRL/ton year-over-year. Although cash costs also rose from 2,432 to 2,726 BRL/ton, the segment managed to turn a slight profit with margins improving from -0.4% to 0.2%.

The following chart illustrates these margin dynamics:

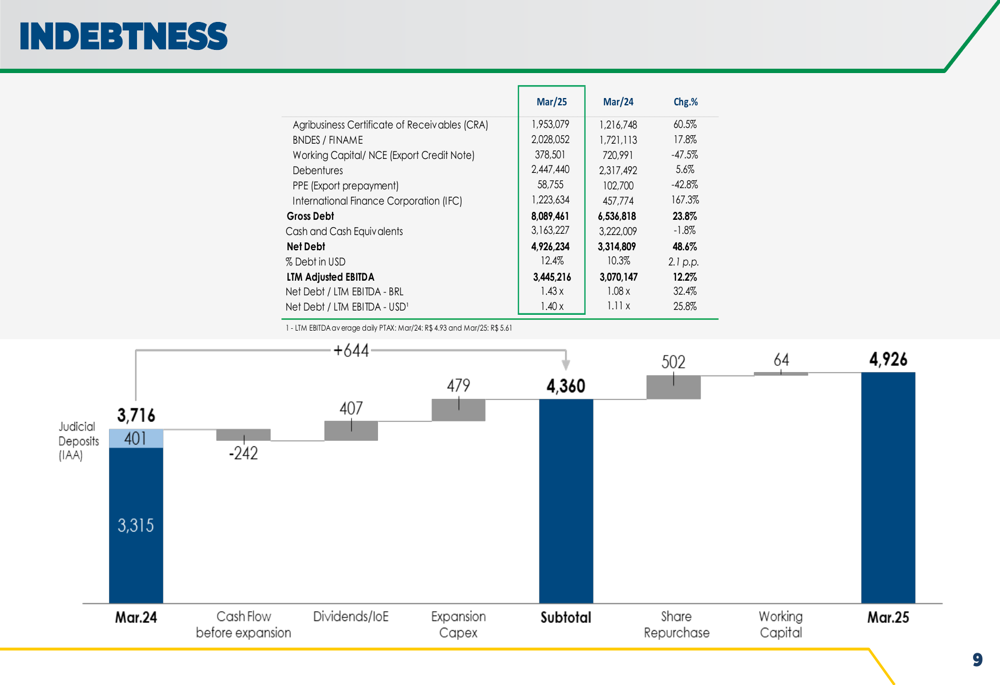

The company’s indebtedness position showed an increase, with gross debt rising to 8,089,461 in March 2025 from 6,536,818 in March 2024. Net debt grew to 4,926,234 from 3,314,809 in the same period, resulting in a Net Debt/LTM EBITDA ratio of 1.43x, which remains at a manageable level despite the increase.

The debt structure and changes are visualized in this comprehensive breakdown:

Strategic Initiatives

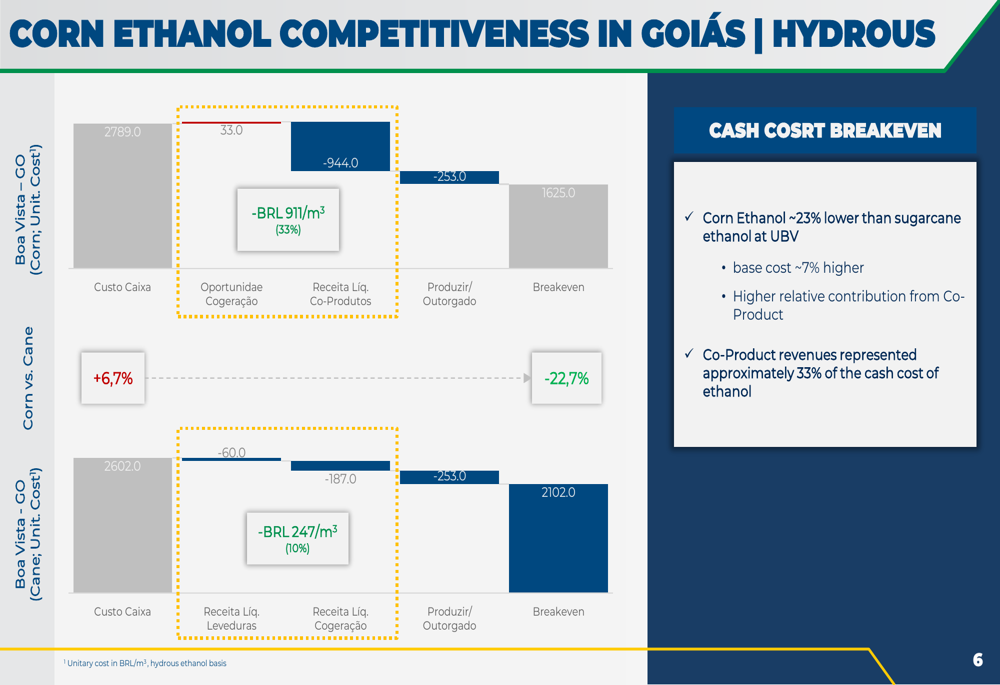

A key strategic focus highlighted in São Martinho’s presentation is the cost advantage of corn ethanol production compared to traditional sugarcane ethanol. The company’s analysis shows that corn ethanol production at its Boa Vista-GO facility is approximately 23% lower in cost than sugarcane ethanol.

This competitive advantage is particularly significant as it provides São Martinho with flexibility in its production mix and potential for margin improvement in its ethanol segment. The cost structure comparison demonstrates how co-products like DDG and electricity generation contribute to lowering the effective breakeven cost of corn ethanol production.

The following chart details this cost advantage:

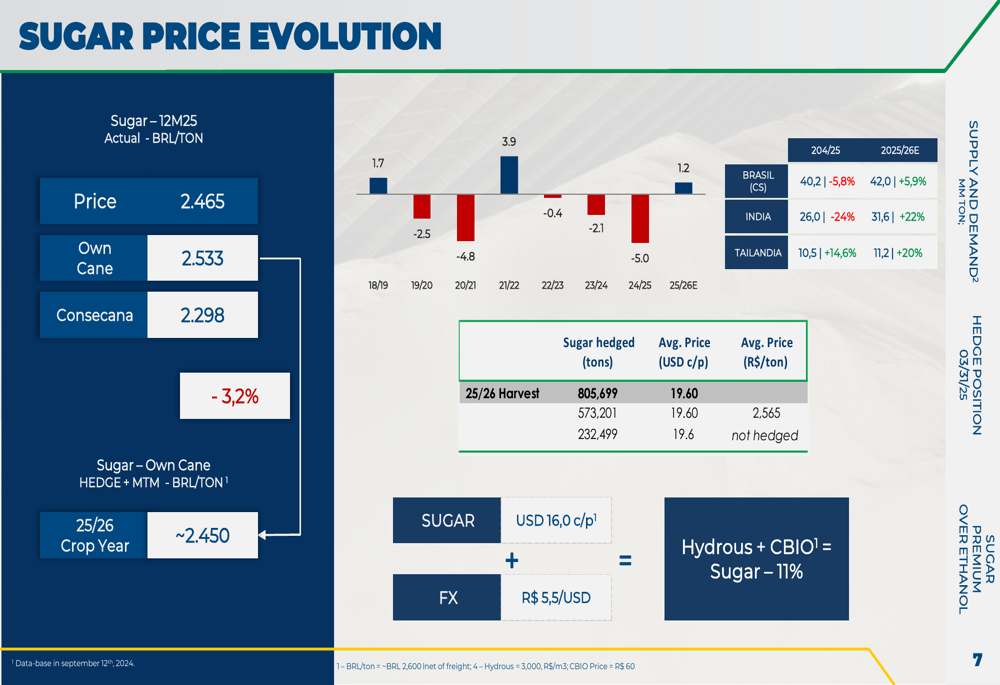

The presentation also addressed sugar price evolution and hedging strategies. São Martinho reported an average price for hedged sugar at USD 19.60 cents per pound, translating to approximately R$ 2,565/ton. This hedging approach helps the company manage price volatility in international sugar markets.

The sugar price trends and hedging information are illustrated here:

Forward-Looking Statements

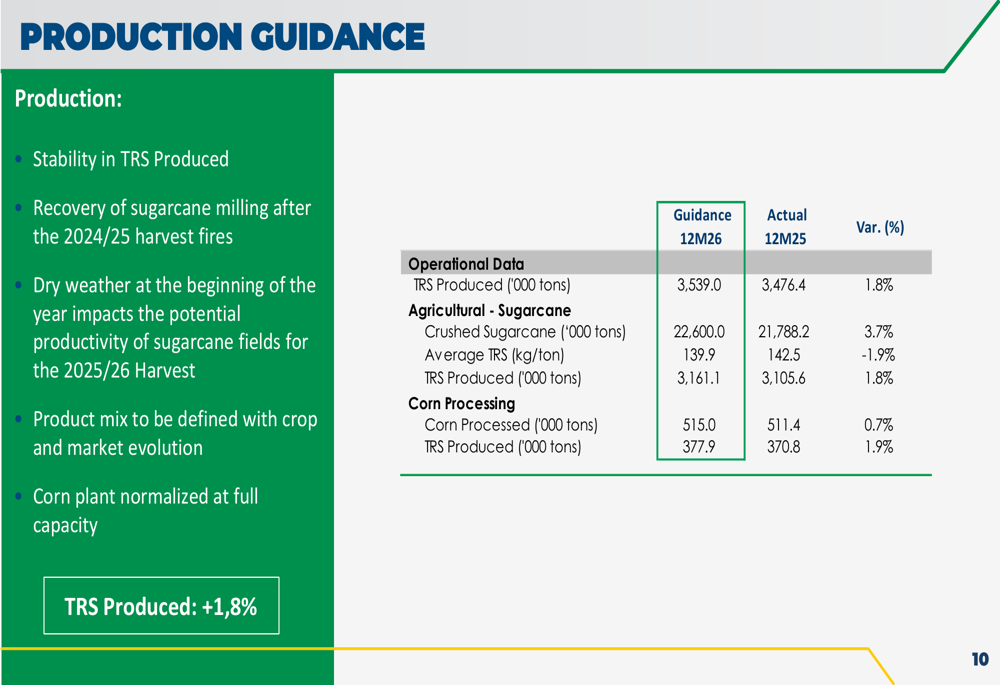

Looking ahead, São Martinho provided production guidance for the 2025/26 crop year, projecting increases in both TRS ( Total (EPA:TTEF) Recoverable Sugar) production and crushed sugarcane volumes. The company expects TRS production to reach 3,539,000 tons in 12M26, up from 3,476,400 tons in 12M25. Crushed sugarcane is projected at 22,600,000 tons, compared to 21,788,200 tons in the previous year.

These production targets suggest confidence in operational recovery despite the challenges posed by fires and other external factors affecting the Brazilian sugar industry:

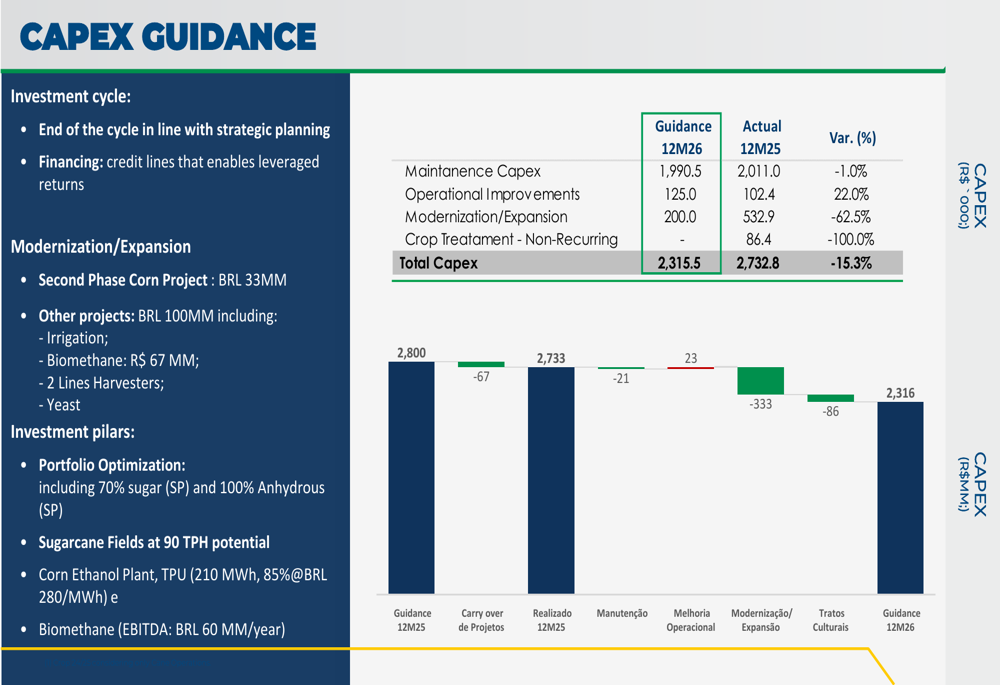

On the capital expenditure front, São Martinho plans to reduce its CAPEX for 12M26 to 2,315.5 million BRL, down from 2,732.8 million BRL in 12M25. This reduction may indicate a more cautious approach to investments as the company navigates market uncertainties and manages its increasing debt levels.

The CAPEX guidance is detailed in the following chart:

The Brazilian harvest situation remains a concern, with the presentation highlighting the impact of fires on production. Despite these challenges, São Martinho managed to meet its sugar production guidance for 12M25, producing 40.2 million tons against a guidance of 40.1 million tons.

The harvest performance and fire impacts are summarized here:

São Martinho’s presentation demonstrates the company’s resilience in a challenging market environment, with strategic emphasis on cost advantages in corn ethanol production and careful management of its product mix. While increasing debt levels and margin pressures in the sugar segment present challenges, the company’s forward-looking production guidance suggests confidence in its operational capabilities for the coming year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.